From 1 May 2026, automatic rent review clauses in every tenancy agreement in England become legally void — even those signed years before the Act came into force [1]. That single provision alone signals how deeply the Renters' Rights Act 2026 reaches into the economics of buy-to-let investment. Valuation Adjustments for Renters' Rights Act 2026: How Pet Permissions, Rent Caps, and Section 21 Abolition Reshape Property Values is not merely a compliance question for landlords — it is a live challenge for every RICS-registered valuer, mortgage lender, and investor trying to price rental property accurately in a transformed legal landscape.

Key Takeaways 📋

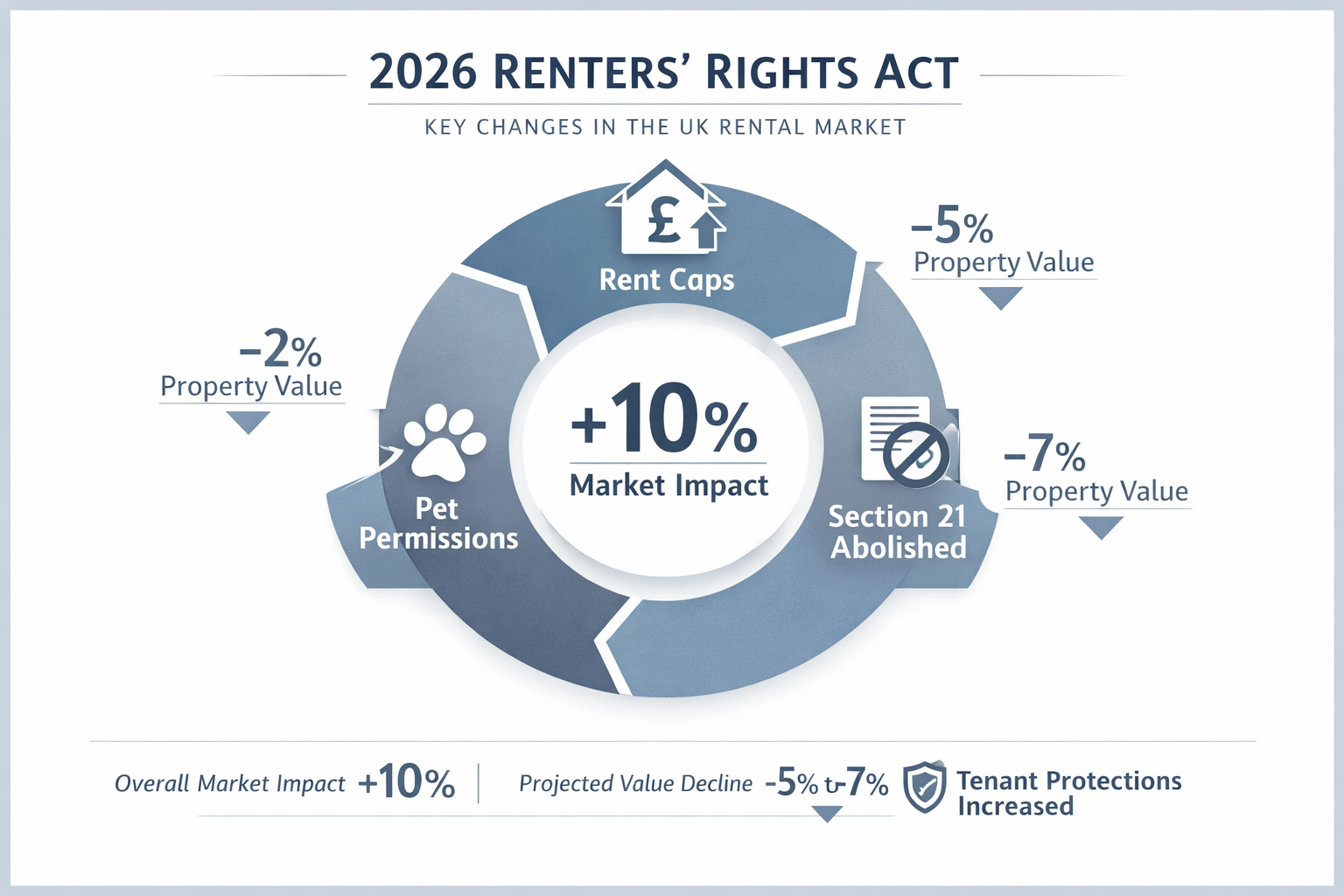

- Section 21 abolition removes landlords' fastest route to vacant possession, extending timelines and increasing litigation risk — both of which compress investment yields and market values [3].

- Annual rent increase caps (one increase per year via Section 13 only, with two months' notice) limit income growth potential and make historic rent roll projections unreliable [1][2].

- Pet permission reforms broaden tenant rights to keep animals, increasing wear-and-tear risk and prompting valuers to reassess condition-related depreciation assumptions.

- RICS Red Book valuers must now adjust comparable evidence, yield benchmarks, and vacant possession premiums to reflect the new legislative reality [2].

- EPC compliance costs (minimum C grade proposed by 2030) add a capital expenditure layer that further suppresses net yields on older stock [3].

Understanding the Legislative Shift: What Changed on 1 May 2026

The Renters' Rights Act 2026 represents the most significant overhaul of the private rented sector (PRS) in a generation. Three structural changes carry the greatest weight for property valuation professionals.

The End of Fixed-Term ASTs

All Assured Shorthold Tenancies (ASTs) are now replaced by periodic monthly tenancies with no minimum term [2]. Tenants may exit on two months' notice at any point. For landlords, this removes the income certainty that fixed terms once provided. A valuer modelling rental income over a five-year hold period can no longer assume a tenant will remain for 12 or 24 months without interruption. Void period assumptions in discounted cash flow (DCF) models should be reviewed upward accordingly.

Section 21 Abolition: The Vacant Possession Premium Disappears

Before Spring 2026, a landlord wishing to sell with vacant possession could serve a Section 21 notice and achieve possession within two to four months in most cases. That route is now closed [3]. Landlords must rely exclusively on Section 8 grounds, which require documented evidence of a specific breach — rent arrears, anti-social behaviour, or other statutory grounds — and which frequently involve contested court hearings [3].

💬 "The process is longer, more litigious, and potentially involves court hearings if tenants refuse to leave." — Gorvins Residential, 2026 [3]

This has a direct and measurable effect on vacant possession value (VPV). Properties sold with sitting tenants have historically traded at a discount of 15–30% compared with vacant equivalents. With Section 21 gone, that discount is likely to widen, particularly for properties where tenants have long occupancy histories and no grounds for removal exist.

For landlords considering an exit, a professional freehold valuation that accounts for the new possession landscape is now essential before marketing.

Rent Caps and the Section 13 Straitjacket

The Act imposes a strict annual rhythm on rent increases [1][2]:

| Rule | Detail |

|---|---|

| First increase permitted | No earlier than 12 months after tenancy start |

| Frequency | Maximum once per year |

| Notice period | Minimum two months (doubled from previous one month) |

| Mechanism | Section 13 statutory process only |

| Contract-based review clauses | Void from 1 May 2026 |

| Backdating of increases | Not permitted |

| Tribunal cap | Cannot exceed landlord's original proposed amount |

The prohibition on backdating is particularly significant for valuation purposes [1]. Under previous rules, a landlord who successfully challenged a rent determination could receive a backdated uplift. That uplift could temporarily boost the income yield used in investment valuations. That mechanism no longer exists. Valuers must model rent income as a strictly prospective, annually-capped stream.

Valuation Adjustments for Renters' Rights Act 2026: Yield Compression and Comparable Analysis

The core challenge for any valuer working on PRS assets in 2026 is that the comparable evidence base — transactions completed before 1 May 2026 — was priced under a fundamentally different legal framework. Applying those comparables without adjustment risks systematic overvaluation.

How Yield Benchmarks Must Shift

Gross yield (annual rent ÷ purchase price) is the most commonly cited metric in buy-to-let investment. However, the Renters' Rights Act 2026 erodes the reliability of both components of that calculation:

- Annual rent is now capped at one increase per year, assessed against market value rather than tenant affordability [1]. In high-demand areas, this may still allow meaningful uplifts — but the timeline is fixed and the process is formalised.

- Purchase price must now reflect the reduced optionality of ownership. A buyer cannot assume quick vacant possession, cannot rely on automatic rent reviews, and must budget for potential tribunal costs if tenants challenge increases [1].

Net yield calculations must now incorporate:

- ✅ Higher void period allowances (periodic tenancies, two-month tenant notice)

- ✅ Increased legal costs (Section 8 possession proceedings vs. Section 21)

- ✅ Compliance costs (Decent Homes Standards, deposit protection) [2]

- ✅ EPC upgrade capital expenditure (C-grade minimum proposed by 2030) [3]

- ✅ Tribunal representation costs where rent challenges arise [1]

For a property previously yielding 6.0% gross, these additional costs could reduce net yield to 4.0–4.5% — a compression that, when capitalised, implies a meaningful reduction in market value.

Comparable Evidence: The Adjustment Problem

RICS Red Book valuations require valuers to adjust comparable transactions for material differences between the comparable and the subject property [2]. Post-1 May 2026, every pre-Act transaction is a materially different legal environment. Valuers should:

- Apply a legislative adjustment factor to pre-Act comparables, reflecting reduced optionality and income certainty.

- Prioritise post-Act transactions as they emerge in the market, even where sample sizes are initially small.

- Document assumptions explicitly, particularly around void periods, possession timelines, and rent review frequency.

- Distinguish between vacant and tenanted sales with greater precision than before, given the widening VPV discount.

A RICS Red Book valuation from a surveyor who understands the post-Act landscape is now a prerequisite for any lender, investor, or litigation case involving PRS property.

The Pet Permission Factor: A New Condition Risk

The Renters' Rights Act 2026 strengthens tenants' rights to keep pets in rented properties. Landlords cannot unreasonably refuse a pet request, and refusals must be justified in writing within a defined timeframe.

For valuers, this introduces a new layer of condition-related depreciation risk:

- Properties occupied by pets over extended tenancies may show accelerated wear to flooring, doors, and garden areas.

- Dilapidations assessments at tenancy end become more complex and potentially more contentious.

- Insurance premiums for landlords may increase, further squeezing net yields.

Surveyors conducting dilapidation surveys on properties with pet-permitted tenancies should document condition benchmarks at the outset of a tenancy with greater rigour than was previously standard practice. This protects both landlord and tenant from disputed claims at exit.

From a valuation standpoint, the market value of a property with a sitting pet-permitted tenancy may carry a slightly wider discount than a non-pet tenancy, reflecting the statistical likelihood of higher end-of-tenancy reinstatement costs.

Valuation Adjustments for Renters' Rights Act 2026: Practical Guidance for Investors and Surveyors

For Landlords: Reassessing Portfolio Value

Every landlord holding PRS assets should commission a fresh valuation that explicitly accounts for the post-Act framework. Key questions to put to a valuer:

- What is the current market value with the sitting tenant in place?

- What is the estimated vacant possession value, and what is the realistic timeline to achieve it under Section 8?

- What yield does the property generate net of all compliance costs?

- What capital expenditure is required to meet the proposed 2030 EPC C-grade minimum?

For landlords in the North West, a Manchester property valuation from a locally experienced RICS surveyor will reflect regional rental market conditions alongside the national legislative changes.

For Mortgage Lenders: Stress-Testing Income Assumptions

Buy-to-let mortgage lenders typically stress-test rental income at 125–145% of the mortgage payment. With rent increases now capped at one per year and subject to a two-month notice requirement [1], the income growth trajectory for new lending cases must be modelled more conservatively.

Lenders should also factor in the increased probability of rent challenges at the First-tier Tribunal. While the Act prevents tribunals from awarding more than the landlord's proposed increase [1], the cost and delay of proceedings still represent a real risk to income continuity.

For Buyers: Due Diligence Has Expanded

Purchasing a tenanted investment property in 2026 requires deeper due diligence than in previous years. Buyers should verify:

- Current rent vs. market rent — is there headroom for a Section 13 increase within the first 12 months?

- Tenancy start date — when is the first permissible rent review?

- Any pending tribunal referrals from the existing landlord

- EPC rating — what is the cost gap to reach a C grade?

- Pet permissions granted — what is the current condition of the property?

A homebuyer survey or RICS Level 3 building survey should be commissioned alongside any investment valuation to capture physical condition risks that the new tenancy framework makes harder to remediate quickly.

Lease Extension Implications

For leasehold investment properties, the interaction between the Renters' Rights Act and lease extension value is an emerging complexity. A property with a short lease, a sitting tenant, and no viable Section 21 route to vacant possession presents a compounded valuation challenge. Lease extension valuation advice from a specialist surveyor is strongly recommended before any transaction involving leasehold PRS assets.

The Compliance Cost Equation: Decent Homes, EPC, and Deposit Rules

Beyond the headline changes, the Act introduces enhanced compliance requirements that directly affect net operating income — and therefore capital value [2]:

| Compliance Area | Requirement | Estimated Cost Impact |

|---|---|---|

| Decent Homes Standard | Properties must meet minimum habitability standards | Variable; potentially £5,000–£20,000+ for older stock |

| EPC C-grade minimum | Proposed by 2030; new EPC system launching 2026 [3] | £3,000–£15,000 for upgrading F/G-rated properties |

| Deposit protection | Stricter compliance and record-keeping | Administrative cost; risk of penalty for non-compliance |

| Section 13 process | Formal notices, correct service, tribunal readiness | Legal/administrative overhead per review cycle |

These costs are not hypothetical. They are capital expenditure items that reduce the net present value of a rental property investment. Valuers should request evidence of EPC ratings and Decent Homes compliance status as standard inputs to any PRS valuation instruction.

Understanding valuation costs upfront — including the scope of a compliant Red Book report — helps investors budget accurately for the full due diligence process.

Conclusion: Actionable Steps for a Post-Act Property Market

The Renters' Rights Act 2026 has permanently altered the risk-return profile of private rented sector property in England. Valuation Adjustments for Renters' Rights Act 2026: How Pet Permissions, Rent Caps, and Section 21 Abolition Reshape Property Values is not an abstract regulatory exercise — it is a practical necessity for anyone buying, selling, lending against, or holding rental property today.

Here are the immediate next steps for each stakeholder:

🏠 Landlords: Commission a fresh RICS valuation that explicitly models post-Act yield compression, vacant possession timelines under Section 8, and EPC upgrade costs. Review all existing tenancy agreements for void rent review clauses that became legally unenforceable on 1 May 2026 [1].

📊 Valuers: Update comparable analysis methodology to flag pre-Act transactions as requiring legislative adjustment. Document all assumptions around void periods, possession costs, and rent review frequency in Red Book reports. Engage with emerging RICS guidance on PRS valuation post-Act [2].

💼 Investors: Recalibrate yield expectations downward and stress-test acquisitions against a net yield floor that incorporates compliance, legal, and EPC costs. Prioritise properties with strong EPC ratings, recent compliance records, and realistic rent-to-market-value ratios.

🏦 Lenders: Revisit rental income stress-test assumptions and consider whether existing ICR (interest coverage ratio) thresholds remain appropriate given the constrained rent growth trajectory.

The legislation is live. The market is adjusting. The valuers and investors who adapt their frameworks now will be best positioned to navigate — and profit from — the transformed landscape of 2026 and beyond.

References

[1] Renters Rights Act New Rent Increase Rules Explained 2026 – https://felixaccountants.com/renters-rights-act-new-rent-increase-rules-explained-2026/

[2] Consideration Of Implications Of Renters Rights Act On Valuation – https://www.rics.org/news-insights/consideration-of-implications-of-renters-rights-act-on-valuation

[3] Selling A Rental Property In 2026 How The New Renters Rights Bill Affects You – https://www.gorvinsresidential.com/selling-a-rental-property-in-2026-how-the-new-renters-rights-bill-affects-you/

[4] Valuation Adjustments For Private Rented Sector Properties Impact Of Renters Rights Act 2026 Section 21 Abolition On Btl Yields – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-private-rented-sector-properties-impact-of-renters-rights-act-2026-section-21-abolition-on-btl-yields