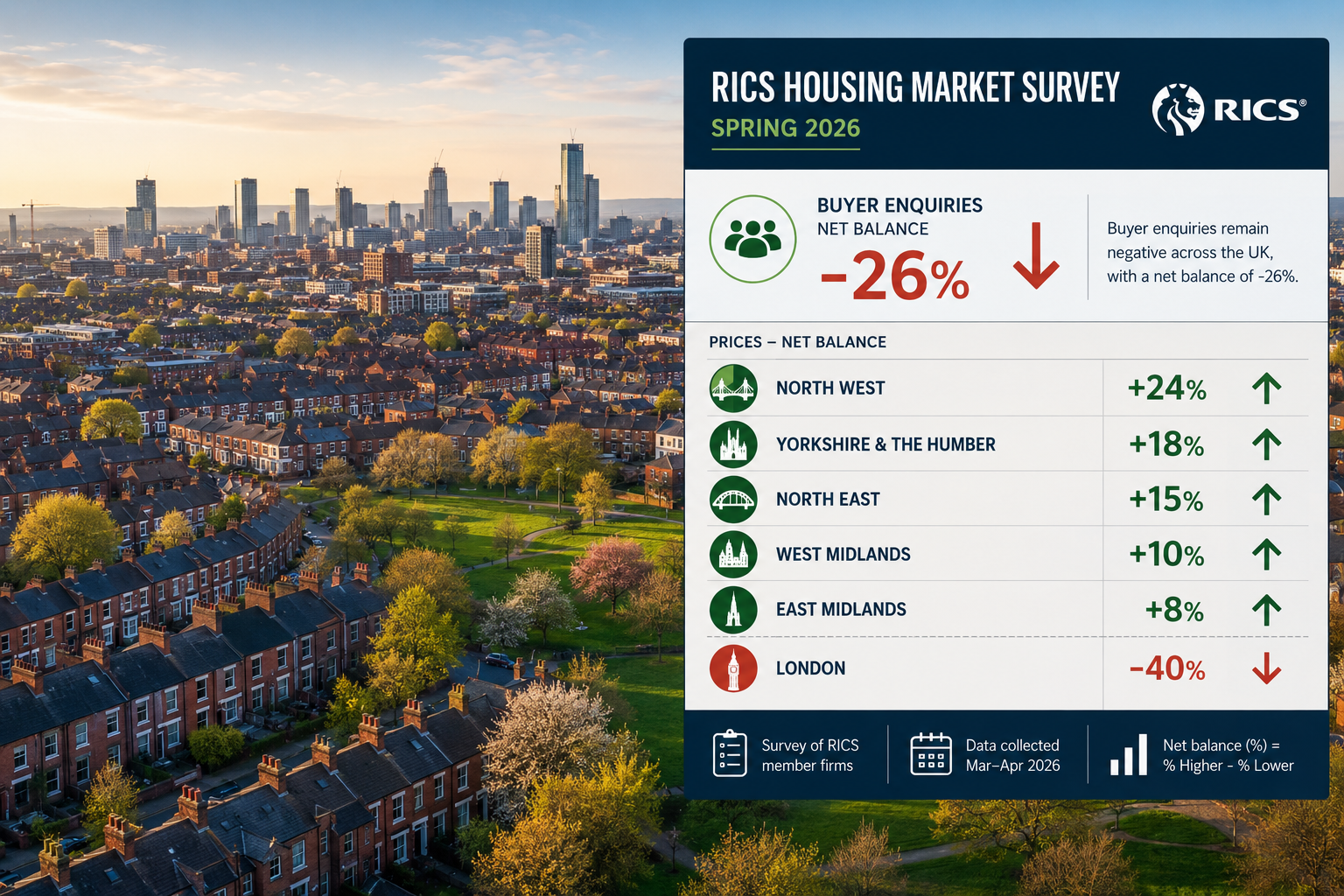

Buyer enquiries across the UK residential market fell to a net balance of -26% in February 2026, a sharp deterioration from -15% in January, and the divergence between northern and southern markets has never been more pronounced. The Valuation Insights from RICS February 2026 Survey: Northern Resilience vs London Cooling in Cautious Spring Markets reveal a property landscape where geography now determines valuation outcomes more decisively than at any point in recent memory. For surveyors, investors, and buyers alike, understanding these regional fault lines is not optional — it is essential.

Key Takeaways

- Buyer enquiries dropped to a net balance of -26% in February 2026, signalling a cautious spring market nationally.

- London house price sentiment hit -40%, while the North West, Scotland, and Northern Ireland recorded firmer price trends.

- London's 12-month price expectations collapsed from +56% to just +7%, a dramatic loss of confidence in the capital.

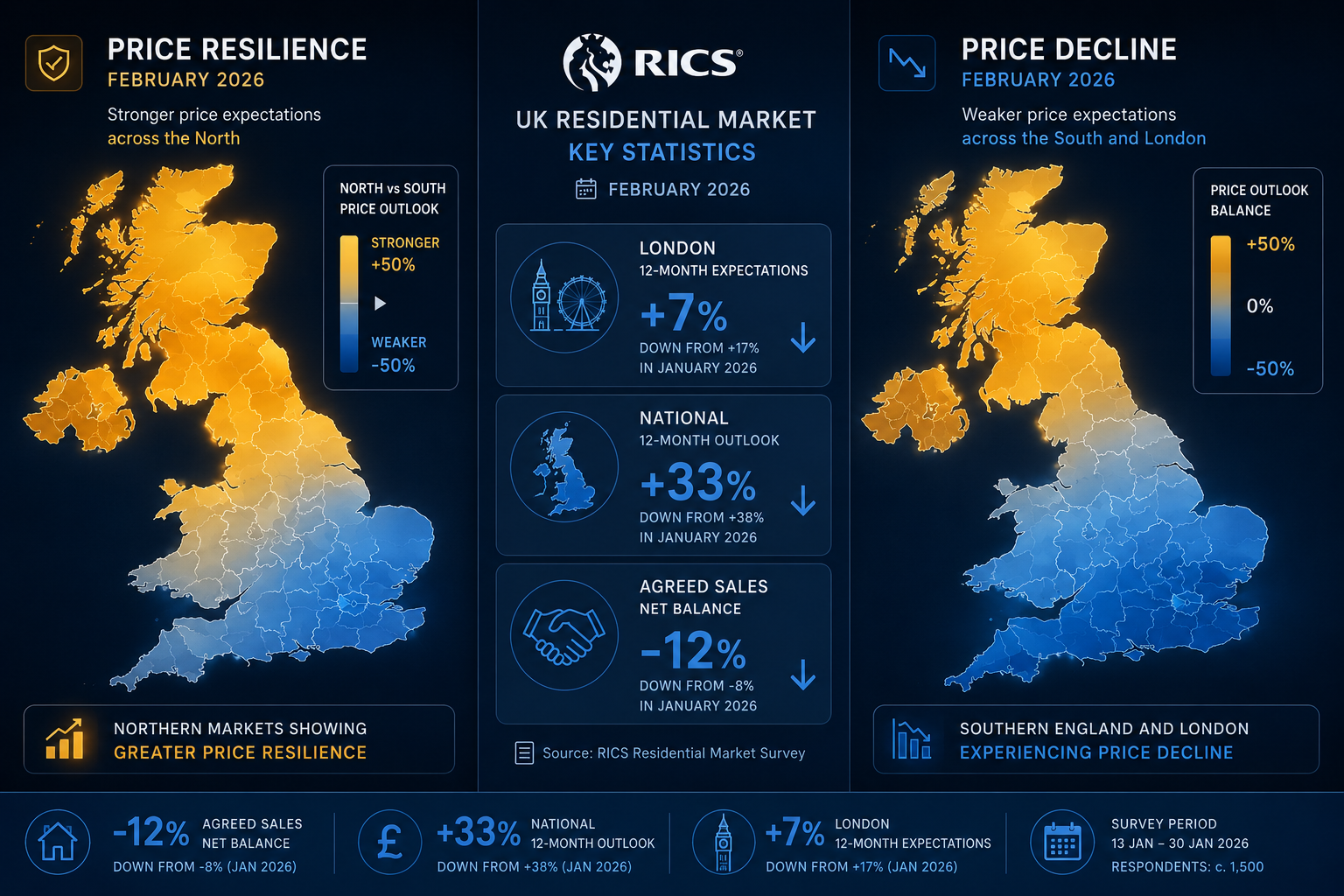

- Nationally, a net balance of +33% of surveyors expect prices to rise over the next 12 months, offering a longer-term positive signal.

- The rental market faces a structural supply crisis, with landlord instructions at -27% and rents expected to rise further.

What the RICS February 2026 Data Actually Shows

The headline numbers from the RICS February 2026 UK Residential Survey paint a picture of a market under pressure but not in freefall. Nationally, house prices registered a net balance of -12%, only marginally weaker than January's reading, suggesting broad stability rather than a dramatic correction [1]. Agreed sales remained subdued at a net balance of -12%, reflecting the difficulty buyers and sellers face in bridging the gap between expectation and reality in current conditions [1].

New instructions were broadly stable at +2%, meaning fresh supply entering the market is not surging [1]. This matters for valuation professionals: when supply stays flat and demand weakens, price discovery becomes harder, and comparable evidence thins out. Surveyors relying on recent transaction data may find fewer clean comparables, particularly in markets where sentiment has shifted faster than completed sales.

Short-term price expectations fell sharply to -18% from -6% in January, indicating that surveyors across the country are bracing for near-term softness [1]. However, the 12-month outlook tells a different story: a net balance of +33% of respondents expect prices to edge higher over the coming year, suggesting the current caution is viewed as temporary rather than structural [1].

"The gap between short-term caution and long-term optimism is precisely where skilled surveyors add the most value — helping clients navigate the noise to reach sound decisions."

For those commissioning valuations right now, this environment underscores the importance of working with a RICS chartered building surveyor who understands both the local market dynamics and the broader survey data shaping lender and buyer behaviour.

Regional Price Divergence: The Core Story in Valuation Insights from RICS February 2026 Survey

The regional breakdown is where the Valuation Insights from RICS February 2026 Survey: Northern Resilience vs London Cooling in Cautious Spring Markets becomes most actionable. The data reveals a stark north-south divide that has been building for years but has now crystallised into concrete survey numbers.

London and the South: Significant Downward Pressure

London recorded a net balance of -40% for house prices in February 2026 — the weakest reading of any region surveyed [1]. The South East posted -24% and East Anglia -26%, confirming that the price weakness is not confined to the capital alone but extends across the broader southern property belt [1].

The capital's longer-term outlook has also deteriorated sharply. London's 12-month price expectations balance dropped from +56% to just +7% [1]. That is a collapse in confidence of extraordinary speed. Between 2016 and 2026, London's property market grew by only 10%, compared to 41% nationally, a chronic underperformance driven by an oversupply of lower-priced flats and successive waves of economic turbulence [3].

For surveyors operating in London, these conditions demand particular care. Valuations in a falling sentiment environment require robust justification, careful selection of comparable evidence, and clear communication to clients about market direction. Those working across North West London or South West London should pay close attention to hyper-local supply and demand signals, as borough-level data can diverge significantly from the London-wide average.

Northern England, Scotland, and Northern Ireland: Relative Strength

By contrast, Northern Ireland, Scotland, and the North West of England reported firmer price trends in February 2026 [1]. This resilience is not a short-term blip. Research shows that Oldham, in Greater Manchester, led the entire country with a 44.83% increase in property values since 2020 [2]. The North of England's housing market has consistently outperformed southern markets on growth metrics over the five-year period, driven by affordability, infrastructure investment, and demographic shifts [2].

The table below summarises the regional price sentiment divergence from the RICS February 2026 survey:

| Region | Price Net Balance (Feb 2026) |

|---|---|

| London | -40% |

| East Anglia | -26% |

| South East | -24% |

| National Average | -12% |

| North West England | Positive |

| Scotland | Positive |

| Northern Ireland | Positive |

This divergence has direct implications for valuation methodology. A property in Manchester or Leeds sits in a fundamentally different market context than an equivalent asset in Croydon or Cambridge. Surveyors must resist applying national-level sentiment to local valuations without adjustment.

Strategies for Surveyors and Buyers in a Cautious Spring Market

The Valuation Insights from RICS February 2026 Survey: Northern Resilience vs London Cooling in Cautious Spring Markets do not just describe the market — they demand a response from professionals and property buyers. Several strategic adjustments are warranted given current conditions.

Recalibrating Valuation Approaches by Region

In softening markets such as London and the South East, surveyors should:

- Widen the comparable search radius carefully, while accounting for micro-market differences.

- Apply greater weight to recent listings and price reductions rather than relying solely on completed sales from three to six months ago.

- Flag market condition caveats clearly in reports, particularly where sentiment indicators are moving rapidly.

- Consider instructing a specific defect survey for properties showing signs of deferred maintenance, as buyers in a cooling market are less willing to absorb risk.

In stronger northern markets, the challenge is different. Rising values can create pressure to over-value, particularly where demand from first-time buyers is concentrated. The RICS data points to buyer enquiries falling even in resilient regions, suggesting that affordability constraints and mortgage rate sensitivity are limiting demand even where fundamentals are positive.

First-Time Buyer Considerations

First-time buyers represent a significant portion of activity in northern markets, where price points remain more accessible. For this group, understanding the difference between a RICS home survey and a full Level 3 building survey is critical. In a market where agreed sales are subdued nationally (-12% net balance), buyers who move forward with confidence and proper due diligence are better positioned to negotiate and complete successfully.

Shared ownership schemes continue to attract first-time buyers in both northern and London markets. Those considering this route should ensure they commission a proper RICS shared ownership valuation before proceeding, as the valuation basis for shared ownership differs from standard market value assessments and requires specialist knowledge.

The 12-Month Uplift Forecast: Planning Ahead

The +33% net balance expecting price growth over 12 months is a significant signal for medium-term planning [1]. Investors and developers who can absorb short-term softness stand to benefit if this forecast proves accurate. However, the London figure of just +7% for 12-month expectations — down from +56% — suggests that the capital's recovery will lag the national trend considerably [1].

For investors evaluating northern buy-to-let opportunities, the combination of price resilience and rental market tightness creates a compelling case. Landlord instructions were firmly negative at -27% nationally, while tenant demand remained broadly stable at +2%, and a net +20% of survey participants expect rents to rise over the next three months [1]. This structural imbalance between rental supply and demand is unlikely to resolve quickly.

The Rental Market: A Structural Supply Crisis

The rental market data embedded within the RICS February 2026 survey deserves separate attention. Landlord instructions at -27% represent an ongoing withdrawal of rental stock from the market [1]. This is not a new trend, but February's data confirms it is accelerating rather than stabilising.

The causes are well-documented: tax changes affecting landlord profitability, regulatory burden increases, and the broader economic uncertainty affecting confidence in property as an investment vehicle. The result is a rental market where tenants face rising rents and shrinking choice, while landlords who remain in the market benefit from strong yields and low vacancy rates.

For surveyors, this creates demand for several specialist services:

- RICS right-to-buy valuations as social housing tenants seek to exit the rental market through purchase.

- Reinstatement cost valuations for landlords reviewing their insurance coverage as property values and rebuild costs shift.

- Commercial building surveys as some landlords pivot from residential to commercial letting strategies.

The rental supply shortage also has a knock-on effect on the sales market. When renting becomes more expensive and less available, the pressure on potential buyers to purchase increases — but if mortgage affordability constraints prevent purchase, households are trapped. This dynamic is particularly acute in northern cities where the rental market has tightened most sharply alongside rising values.

What This Means for Valuation Practice in 2026

The cumulative picture from the RICS February 2026 survey requires surveyors to operate with greater regional sensitivity than at any recent point. Several practical implications stand out.

Comparable evidence selection must now account explicitly for the regional divergence in sentiment. A national average price movement figure is almost meaningless when London sits at -40% and the North West is positive. Surveyors should document their regional adjustment rationale clearly.

Client communication needs to address the gap between short-term caution (-18% near-term expectations) and medium-term optimism (+33% 12-month outlook) [1]. Buyers and sellers often anchor on one or the other; a skilled surveyor helps them understand both timeframes and make decisions accordingly.

Lender scrutiny is likely to increase in softening markets. Mortgage valuations in London and the South East will face greater challenge if market values are moving downward. Surveyors should ensure their reports are thoroughly evidenced and that any downward adjustments from asking price are clearly justified.

Survey type selection becomes more important in uncertain markets. Buyers tempted to cut costs by opting for a basic valuation alone should be encouraged to consider a full RICS building survey to identify defects that could affect value or create post-purchase liabilities. In a market where agreed sales are already subdued, a defect discovered after exchange can derail a transaction entirely.

The north-south divide also has implications for comparing different types of survey across different property ages and conditions. Northern housing stock, often older and with more complex construction histories, may require more detailed inspection than newer southern developments — yet the reverse assumption is sometimes made based on price point alone.

Conclusion: Acting on the February 2026 RICS Data

The Valuation Insights from RICS February 2026 Survey: Northern Resilience vs London Cooling in Cautious Spring Markets offer a clear directive: regional differentiation is no longer a nuance in UK property analysis — it is the central story. A buyer enquiry net balance of -26%, London price sentiment at -40%, and a rental supply crisis running at -27% landlord instructions all point to a market requiring careful, evidence-based navigation [1].

Actionable next steps for different stakeholders:

- Buyers in northern markets: Move forward with proper due diligence. Commission a full RICS survey rather than a basic valuation, and use the current subdued transaction environment to negotiate on price and conditions.

- Buyers in London and the South East: Exercise caution on pricing assumptions. The 12-month outlook of just +7% for London means short-term overpaying carries real risk. Seek specialist valuation advice before committing.

- Landlords: Review reinstatement cost coverage and consider whether current rental yields justify continued investment. The supply shortage works in your favour on rents, but regulatory risk remains elevated.

- Surveyors: Update regional adjustment frameworks, strengthen comparable evidence documentation, and ensure client-facing communications address both the short-term caution and the 12-month positive outlook clearly.

- Investors: The +33% national 12-month price expectation, combined with northern market resilience and rental supply tightness, makes well-selected northern property a credible medium-term opportunity — provided due diligence is thorough.

The spring 2026 market is cautious, not broken. Those who read the regional signals accurately and act with appropriate professional rigour are best positioned to make sound decisions in the months ahead.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026?utm_source=openai

[2] UK Property Five Year Analysis 2026 – https://moveinsights.co.uk/research/uk-property-five-year-analysis-2026?utm_source=openai

[3] London House Prices – https://moneyweek.com/investments/property/london-house-prices?utm_source=openai