New buyer enquiries in January 2026 recorded a net balance of -15% — still negative, but a marked improvement from -21% in December 2025 and -29% just two months prior [1][2]. That trajectory tells a story: the UK residential market is not yet in full recovery, but the direction of travel has shifted. For valuation surveyors, that shift demands an immediate recalibration of approach.

The Early Signs of 2026 Housing Market Recovery: Valuation Surveyor Strategies from RICS January Survey Amid Affordability Pressures represent both an opportunity and a challenge. Sentiment is improving, but affordability constraints, regional divergence, and macroeconomic uncertainty mean that applying a single valuation lens across the UK market is no longer viable — if it ever was.

This article breaks down the RICS January 2026 survey data and translates it into actionable strategies for valuation surveyors navigating a market in transition.

Key Takeaways 📌

- New buyer enquiries improved for the third consecutive month, reaching -15% net balance in January 2026 — the least negative reading since mid-2025.

- Agreed sales hit their strongest reading in 8 months, with smaller houses and mid-market family homes leading the recovery.

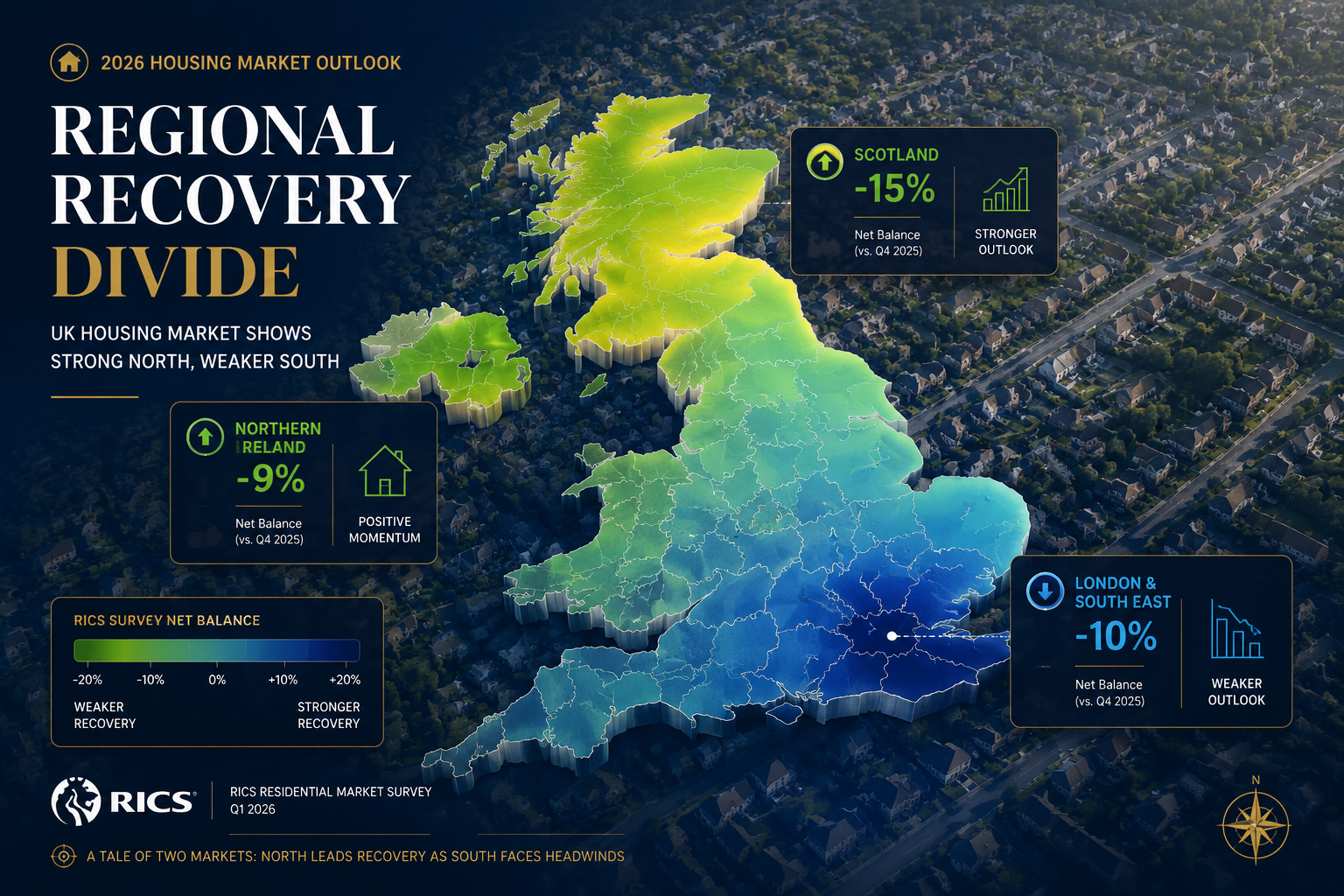

- Scotland, Northern Ireland, and the North West are outperforming London and the South East, where affordability pressures remain acute.

- 12-month sales expectations surged to +35%, yet short-term caution persists — signalling a gradual, not rapid, recovery path.

- Rental market dynamics are tightening, with tenant demand rising and landlord supply still constrained, pushing rental price growth expectations to +28%.

What the RICS January 2026 Data Actually Tells Us

Improving Demand Metrics — But Context Matters

Three consecutive months of improving buyer enquiry readings is not a coincidence. The progression from -29% (November 2025) → -21% (December 2025) → -15% (January 2026) reflects a genuine, if cautious, return of buyer confidence [1][2]. Agreed sales activity followed suit, posting a net balance of -9% — the strongest reading since June 2025 [2][3].

💬 "The data does not suggest a boom. It suggests a floor. And for valuation surveyors, identifying a floor is just as strategically important as identifying a peak."

However, context is critical. These figures remain net negative, meaning more respondents reported declining activity than improving activity. The recovery is real, but it is fragile. Short-term three-month sales expectations eased to just +4% net balance, down sharply from +22% previously — a clear signal that near-term caution persists among market professionals [1][2].

Price Stabilisation: The End of Widespread Declines?

The three-month price net balance improved to -10% in January 2026, recovering from a low of -19% in October 2025 [1]. This is meaningful. It suggests that the broad-based price correction that characterised the second half of 2025 is moderating at a national level.

| Metric | October 2025 | December 2025 | January 2026 |

|---|---|---|---|

| New Buyer Enquiries (net %) | ~-25% | -21% | -15% |

| Agreed Sales (net %) | ~-18% | ~-14% | -9% |

| 3-Month Price Balance (net %) | -19% | ~-14% | -10% |

| 12-Month Sales Expectations (net %) | — | — | +35% |

| Rental Price Growth Expectations (net %) | — | +16% | +28% |

Sources: RICS UK Residential Market Survey, January 2026 [2]; The Intermediary [1]

Price stabilisation, however, is not uniform. Scotland, Northern Ireland, the North West, and the North of England are recording positive price growth, while London, the South East, the South West, and East Anglia continue to lag [1]. Affordability constraints in southern England remain a structural headwind that no amount of improving sentiment can quickly overcome.

Early Signs of 2026 Housing Market Recovery: Regional Divergence and Valuation Surveyor Strategies

Why Regional Calibration Is Now Non-Negotiable

The single most important strategic adjustment for valuation surveyors in 2026 is regional recalibration. The RICS January 2026 survey makes the north-south divide explicit, and surveyors who apply national averages to local valuations risk material inaccuracy in both directions [1][2].

In outperforming regions (Scotland, Northern Ireland, North West):

- Comparable evidence from late 2025 may understate current market value

- Upward adjustments to comparable sales data are increasingly justified

- Demand-side pressure from first-time buyers and family movers is measurable

In lagging regions (London, South East, South West, East Anglia):

- Affordability ratios remain stretched, suppressing buyer pools

- Comparable evidence from pre-correction periods (2023–2024) may overstate current value

- Caution is warranted in applying optimistic sentiment to hard valuation figures

For surveyors operating across multiple regions, maintaining separate regional market commentary within valuation reports is now best practice — not a luxury. This is particularly relevant for those conducting RICS Red Book valuations, where transparency of methodology is a professional requirement.

Property Type Matters: Smaller Houses vs. Flats

The RICS January 2026 data highlights a notable divergence by property type. Buyer enquiries and agreed sales improved "considerably" for smaller houses, while flat transactions showed considerably less strength [1][2].

This has direct implications for valuation methodology:

- 🏠 Smaller terraced and semi-detached houses: Upward demand pressure; comparable evidence should weight recent transactions more heavily

- 🏢 Flats and apartments: Weaker demand profile; service charge exposure, leasehold reform uncertainty, and cladding legacy issues continue to suppress buyer confidence

- 👨👩👧 Mid-market family properties: Emerging as the recovery's sweet spot — particularly in northern regions

Surveyors conducting RICS HomeBuyer Survey Level 2 reports should reflect these demand differentials in their market commentary sections, ensuring clients receive a realistic picture of saleability alongside structural condition.

Adjusting Valuation Models for Buyer Caution

Even in improving markets, the data signals that buyers remain price-sensitive and cautious. The gap between 12-month optimism (+35% net sales expectations) and short-term restraint (+4% net three-month expectations) suggests that recovery will be gradual and conditional [1][2].

Practical adjustments for valuation surveyors include:

- Weighting comparable evidence carefully — transactions from Q3–Q4 2025 may reflect distressed or discounted conditions; transactions from early 2026 are more representative of current sentiment

- Applying conservative adjustments for time — the market is improving, but not at a pace that justifies aggressive upward time adjustments

- Flagging market conditions explicitly — RICS Red Book standards require surveyors to note market volatility; January 2026 conditions warrant clear commentary on the transitional nature of the market

- Scenario-testing valuations — particularly for mortgage purposes, where lenders are scrutinising affordability metrics closely

For those providing RICS valuations for residential purposes, transparent methodology and well-documented comparable selection are essential safeguards in a transitional market.

Early Signs of 2026 Housing Market Recovery: Rental Market Dynamics and Affordability Pressures

The Rental Market: Tightening Supply Meets Rising Demand

The rental sector presents a distinct but related challenge for surveyors. Landlord instructions remained negative at -24% net balance in January 2026, though this represents an improvement from -34% previously [2]. Meanwhile, tenant demand increased for the first time in two quarters, pushing rental price growth expectations to +28% net balance — up sharply from +16% [1][2].

This supply-demand imbalance has several implications:

- Rental values are rising faster than sales values in most regions, affecting affordability calculations for prospective buyers

- Buy-to-let investment valuations require careful consideration of yield compression versus capital value uncertainty

- Shared ownership and right-to-buy schemes are becoming more attractive as outright purchase remains unaffordable for many households

Surveyors involved in RICS Shared Ownership valuations or Right to Buy valuations will find demand for these services increasing as households seek alternative pathways to ownership amid high rental costs.

Affordability Pressures: The Structural Constraint

Despite improving sentiment, affordability remains the dominant structural constraint on UK housing market recovery in 2026. Mortgage rates, while lower than their 2023 peaks, remain elevated relative to the pre-2022 environment. Real wage growth has helped at the margins, but house price-to-income ratios in southern England remain historically high.

Key affordability indicators for surveyors to monitor:

| Indicator | Implication for Valuations |

|---|---|

| Mortgage rate trajectory | Affects buyer purchasing power and demand depth |

| Regional house price-to-income ratios | Guides comparable weighting by geography |

| Rental yield vs. capital growth balance | Relevant for investment property valuations |

| First-time buyer activity levels | Signals lower-end market health |

Surveyors conducting homebuyer surveys should be prepared to address affordability-related questions from clients who are increasingly aware of market conditions and seeking professional guidance beyond structural assessment alone.

New Supply: Stabilising But Not Expanding

New instructions recorded a net balance of just +1% in January 2026 (versus -1% in December 2025), indicating that supply is stabilising but not yet meaningfully expanding [2]. This matters for valuers because:

- Limited comparable evidence from recent transactions makes it harder to establish robust market value

- Vendor expectations may still be anchored to pre-correction price levels, creating negotiation gaps

- Instruction volumes for surveyors may remain below 2022–2023 levels in the near term, even as sentiment improves

The supply constraint also supports the case for cautious optimism rather than aggressive upward revaluation — a balanced position that reflects both the improving trajectory and the ongoing structural limitations.

Strategic Recommendations for Valuation Surveyors in 2026

Adapting Professional Practice to a Transitional Market

The Early Signs of 2026 Housing Market Recovery: Valuation Surveyor Strategies from RICS January Survey Amid Affordability Pressures point to a clear set of professional priorities for 2026:

✅ Enhance regional market intelligence

Invest in granular local data. National averages are misleading in a market with such pronounced regional divergence. Surveyors in the North West, for example, are operating in a fundamentally different environment than colleagues in the South East.

✅ Prioritise transparency in comparable selection

Document why specific comparables were chosen or rejected. In a transitional market, the rationale for comparable weighting is as important as the comparables themselves.

✅ Update market commentary in every report

Static boilerplate market commentary is insufficient. Each report should reflect current conditions — including the improving-but-cautious trajectory evidenced by the RICS January 2026 survey [2][3].

✅ Engage with lender requirements proactively

Mortgage lenders are applying heightened scrutiny to valuations in regions with affordability pressures. Surveyors should anticipate queries and provide pre-emptive justification for value conclusions.

✅ Expand service offerings to meet evolving demand

As the market transitions, demand for specialist valuations — including lease extension valuations, freehold valuations, and matrimonial or probate valuations — tends to increase. Diversifying service capacity positions surveyors well for the recovery phase.

✅ Leverage technology for market monitoring

Real-time transaction data, automated valuation model (AVM) outputs, and digital comparable databases can supplement traditional research, particularly where transaction volumes remain thin.

For a comprehensive understanding of what RICS-certified surveyors assess during property inspections, the RICS-certified property inspection guide provides valuable context on professional standards and methodology.

Long-Term Confidence vs. Short-Term Caution: Calibrating the Balance

The most nuanced challenge for valuation surveyors in 2026 is holding two truths simultaneously: long-term confidence is rising (12-month sales expectations at +35%, price growth expectations at 43% of respondents) while short-term caution is warranted (+4% three-month sales expectations) [1][2][4].

💬 "A valuation is a point-in-time assessment, not a forecast — but understanding the trajectory of the market is essential context for any credible opinion of value."

This means:

- Current market value conclusions should reflect January 2026 conditions, not anticipated future recovery

- Market commentary can legitimately reference improving sentiment as context

- Clients should be advised that conditions are transitional and that values may move in either direction over the short term

Conclusion: Navigating Recovery With Professional Precision

The RICS January 2026 survey data represents a genuine inflection point for the UK residential market. Buyer enquiries are improving, agreed sales are at their strongest in eight months, and long-term confidence is building [1][2][3]. Yet affordability pressures, regional disparities, and near-term uncertainty mean that the recovery path is gradual and uneven.

For valuation surveyors, this environment demands heightened precision, regional granularity, and transparent methodology. The professionals who will serve their clients best in 2026 are those who resist both excessive pessimism and premature optimism — anchoring their opinions of value in robust comparable evidence while providing clear, informed market context.

Actionable Next Steps for Valuation Surveyors 🎯

- Review and update regional market files — ensure comparable databases reflect Q4 2025 and Q1 2026 transaction evidence

- Audit existing report templates — update market commentary sections to reflect the transitional conditions evidenced by RICS January 2026 data

- Engage with RICS guidance — review any updated RICS Red Book guidance on market uncertainty disclosures

- Segment your pipeline by property type — apply different analytical frameworks to smaller houses versus flats versus mid-market family homes

- Monitor rental market data — rental price growth has implications for affordability calculations and investment property valuations

- Communicate proactively with clients — buyers, sellers, and lenders all benefit from clear, evidence-based guidance in a transitional market

The early signs of 2026 housing market recovery are real. Capitalising on them professionally requires the same discipline that has always defined excellent valuation practice: evidence, transparency, and sound professional judgement.

References

[1] Residential Market Shows Signs Of Early Recovery In January 2026 RICS – https://theintermediary.co.uk/2026/02/residential-market-shows-signs-of-early-recovery-in-january-2026-rics/

[2] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[3] RICS Hails Early Signs of Housing Market Improvement in Latest Survey – https://www.housingtoday.co.uk/news/rics-hails-early-signs-of-housing-market-improvement-in-latest-survey/5140683.article

[4] UK Housing Market Early Signs Of Recovery – https://www.thetimes.com/business/economics/article/uk-housing-market-early-signs-of-recovery-fh0n07b6x