The RICS February 2026 Residential Survey reveals a stark contradiction: while 12-month price expectations remain positive at +33%, near-term sentiment has plummeted to -18%, creating a 12-point downward swing from January.[1] This divergence between short-term pessimism and long-term optimism presents chartered surveyors with a complex valuation challenge as spring market activity begins. Understanding how to interpret these mixed signals and apply appropriate valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts has become essential for accurate property assessments across increasingly fragmented regional markets.

The February data exposes dramatic regional paradoxes that demand sophisticated adjustment techniques. London's 12-month expectations collapsed from +56% to just +7%, while buyer demand across the UK deteriorated to -26%.[1] Yet supply remains stable, rental markets show continued strength, and Northern regions demonstrate resilience. For surveyors conducting RICS valuations, these conflicting indicators require careful calibration of comparable evidence, time adjustments, and market condition factors.

Key Takeaways

- Near-term price expectations dropped sharply to -18% in February from -6% in January, requiring immediate downward adjustments to short-term valuation scenarios and comparable evidence weighting

- Regional divergence reached extreme levels, with London sentiment falling 49 percentage points while Northern Ireland, Scotland, and North West markets maintained stability, necessitating location-specific adjustment matrices

- Buyer demand collapsed to -26% creating reliability concerns for recent comparable transactions, while stable supply at +2% supports consistent evidence collection for valuation purposes

- 12-month expectations remain positive at +33% despite near-term pessimism, creating valuation scenarios where short-term price declines may precede longer-term recovery trajectories

- Rental market strength continues with +20% expecting rent rises over three months, requiring distinct buy-to-let valuation adjustments that account for tightening stock and upward rental growth

Understanding the February 2026 Survey Data: Key Metrics for Valuation Adjustments

The RICS February 2026 Residential Survey employs seasonally adjusted methodology using X-12 techniques to provide reliable market indicators.[2] For surveyors applying valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts, understanding the specific metrics and their directional changes is fundamental to accurate property assessment.

Critical Survey Metrics and Their Valuation Implications

Near-Term Price Balance: -18% 📉

The near-term price balance represents surveyor expectations for the next three months. The February reading of -18% marks a significant deterioration from January's -6%, representing a 12-point negative swing.[1] This metric directly impacts:

- Time adjustments applied to comparable evidence from previous months

- Market condition adjustments for properties under offer or recently exchanged

- Short-term valuation scenarios for forced sale or immediate marketing situations

When conducting RICS building surveys, surveyors should incorporate this negative momentum into valuation advice sections, particularly for clients considering immediate sale strategies.

New Buyer Enquiries: -26% 🔍

Buyer demand collapsed to -26% in February from -15% in January, representing fresh deterioration after brief early-year momentum.[1] This metric affects:

- Comparable evidence reliability – recent transactions may reflect stronger demand conditions than currently prevail

- Marketing period assumptions – properties may take longer to sell than historical averages suggest

- Negotiation leverage – buyers possess increased bargaining power in current conditions

12-Month Price Expectations: +33% 📈

Despite near-term pessimism, a net balance of +33% of surveyors expect prices to edge higher over 12 months.[1] This creates a critical valuation tension:

| Timeframe | Sentiment | Valuation Application |

|---|---|---|

| 0-3 months | Negative (-18%) | Apply downward adjustments to recent comparables |

| 3-6 months | Uncertain | Use wider valuation ranges, incorporate volatility premiums |

| 6-12 months | Positive (+33%) | Support longer-term investment valuations, development appraisals |

For Red Book valuations requiring market value assessments, surveyors must carefully distinguish between current market value (reflecting near-term weakness) and investment value scenarios (incorporating longer-term recovery expectations).

Supply and Transaction Metrics

New Instructions: +2%

Fresh listings remain broadly stable with a net balance of +2%, suggesting the supply pipeline continues without dramatic shifts.[1] This stability supports:

- Consistent comparable evidence collection – the pool of available comparables remains relatively constant

- Reduced supply-side volatility – valuations need not incorporate sudden inventory shocks

- Balanced market assumptions – neither severe shortage nor oversupply conditions prevail

Agreed Sales: -12%

Transaction momentum remains subdued with agreed sales at -12%, while near-term sales expectations fell to -2%.[1] This affects:

- Transaction evidence currency – completed sales may be several months old, requiring significant time adjustments

- Exchange-to-completion periods – longer timescales increase uncertainty in valuation accuracy

- Market liquidity assumptions – properties may be harder to sell quickly at full market value

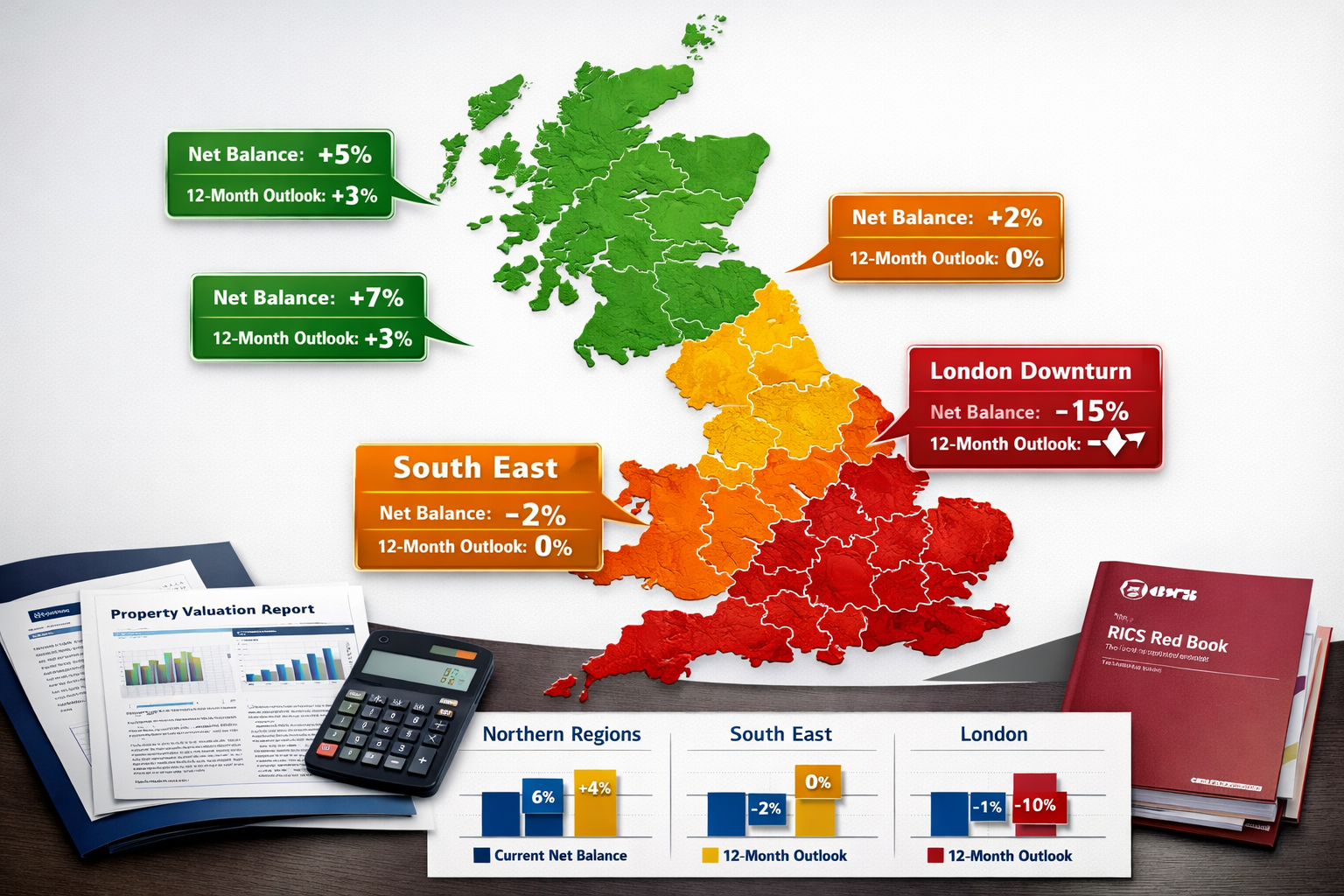

Regional Divergence: Applying Location-Specific Valuation Adjustments from RICS February 2026 Residential Survey

The February 2026 survey reveals unprecedented regional fragmentation in UK residential markets, requiring surveyors to abandon national-level adjustment factors in favor of granular, location-specific methodologies. The valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts must account for dramatic variations in market sentiment, buyer behavior, and price momentum across different geographic areas.

London Market: Dramatic Sentiment Reversal

London experienced the most striking reversal in the February data, with 12-month price expectations plummeting from +56% to just +7%.[1] This 49-percentage-point collapse represents a fundamental reassessment of London's medium-term prospects and requires immediate valuation protocol adjustments.

Current price momentum in London registered -40%, indicating substantial downward pressure on values.[1] For surveyors conducting valuations in London boroughs, this necessitates:

✅ Aggressive downward time adjustments – Comparables from Q4 2025 may require 3-5% downward adjustments to reflect current conditions

✅ Increased valuation ranges – Report wider ranges (±5-7% rather than standard ±3-5%) to reflect heightened uncertainty

✅ Buyer motivation analysis – Weight recent transactions by buyer type (investors vs. owner-occupiers) as motivations differ significantly in declining markets

✅ Prime vs. secondary market differentiation – Apply distinct adjustment factors for prime central London (potentially more resilient) versus outer London markets (more sensitive to mortgage rate changes)

When preparing RICS valuation reports, surveyors should explicitly reference the London-specific sentiment collapse in market commentary sections, particularly for lender instructions where loan-to-value ratios may be affected.

Southern England: Sustained Downward Pressure

The broader Southern England region demonstrates consistent negative momentum:

- South East: -24% current price balance

- East Anglia: -26% current price balance

- South West: Negative (specific figure not disclosed but trending downward)[1]

This geographic clustering of weakness suggests systemic factors affecting southern markets, including:

🏠 Higher absolute price levels making properties more sensitive to mortgage rate increases

🏠 Greater exposure to London economic spillover as commuter belt areas follow London trends with a lag

🏠 Stamp duty threshold impacts as southern properties more frequently exceed duty-free thresholds

For surveyors working across southern regions, comparable evidence selection should prioritize:

- Recent transactions (within 3 months) over older evidence

- Properties that actually sold rather than withdrawn listings or price reductions

- Similar buyer profiles to the subject property's likely purchaser demographic

- Mortgage-dependent transactions rather than cash purchases (if subject property will require financing)

Northern Regions and Scotland: Relative Resilience

In stark contrast to southern weakness, several northern markets demonstrate stability or modest strength:

- Northern Ireland: Positive momentum

- Scotland: Stable to positive trends

- North West: Firmer conditions than national average[1]

This resilience creates valuation opportunities and challenges:

Opportunities 🌟

- More reliable comparable evidence due to stable market conditions

- Reduced need for aggressive time adjustments

- Stronger buyer demand supports marketing period assumptions

- Investment valuations can incorporate steadier growth assumptions

Challenges ⚠️

- National media coverage may emphasize southern weakness, affecting buyer psychology even in stable northern markets

- Mortgage lenders may apply national-level caution to lending policies regardless of local conditions

- Comparable evidence from southern regions cannot be reliably adjusted for use in northern valuations

Surveyors conducting building surveys in locations across northern regions should emphasize local market conditions in valuation commentary, explicitly distinguishing regional performance from national headlines.

Adjustment Matrix for Regional Divergence

| Region | Current Price Balance | 12-Month Expectation | Recommended Time Adjustment (per month) | Valuation Range Width |

|---|---|---|---|---|

| London | -40% | +7% | -0.8% to -1.2% | ±6-7% |

| South East | -24% | Moderate positive | -0.5% to -0.8% | ±5-6% |

| East Anglia | -26% | Moderate positive | -0.5% to -0.8% | ±5-6% |

| North West | Stable/positive | Positive | -0.2% to +0.2% | ±4-5% |

| Scotland | Stable/positive | Positive | -0.1% to +0.3% | ±4-5% |

| Northern Ireland | Positive | Positive | +0.2% to +0.5% | ±4-5% |

Note: These adjustment factors should be applied to comparable evidence on a monthly basis, with cumulative adjustments for older transactions.

Practical Valuation Strategies: Implementing Adjustments from RICS February 2026 Residential Survey

Translating survey data into actionable valuation methodology requires systematic approaches that maintain RICS Red Book compliance while accurately reflecting current market realities. The following strategies enable surveyors to implement valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts with professional rigor and defensible reasoning.

Strategy 1: Enhanced Comparable Evidence Weighting 📊

Traditional comparable evidence analysis typically weights recent transactions most heavily. However, the February 2026 survey data suggests a more nuanced approach:

Optimal Weighting Framework:

Tier 1 (Highest Weight – 40-50%): Transactions from February-March 2026 that reflect current negative sentiment conditions. These comparables most accurately represent the market the subject property will enter.

Tier 2 (Moderate Weight – 30-40%): Transactions from December 2025-January 2026, adjusted downward by 1-2% to reflect deteriorating sentiment. These provide volume when recent evidence is limited.

Tier 3 (Lower Weight – 10-20%): Transactions from October-November 2025, adjusted downward by 2-4% to reflect the -18% near-term sentiment shift. Use primarily for trend analysis rather than direct value indication.

Tier 4 (Minimal Weight – 5-10%): Transactions from summer/autumn 2025, adjusted downward by 4-6%. Use only when insufficient recent evidence exists, with explicit caveats in the valuation report.

When conducting Level 3 building surveys, surveyors should document this tiered approach in the valuation methodology section, demonstrating how survey data informed the weighting decisions.

Strategy 2: Volatility Premium Integration

RICS analysis characterizes current market conditions as experiencing "renewed volatility" with weakened confidence.[1] In volatile markets, professional valuation standards support incorporating volatility premiums:

Volatility Premium Application:

- Standard markets: Valuation range of ±3-5% around central value

- Current volatile conditions: Valuation range of ±5-7% around central value

- Extreme regional volatility (London): Valuation range of ±6-8% around central value

This wider range acknowledges:

✓ Increased uncertainty in comparable evidence reliability

✓ Rapid sentiment shifts that may continue through spring 2026

✓ Divergent buyer motivations creating wider bid ranges

✓ External factors (geopolitical events, energy prices) affecting rate expectations[1][3]

For lender instructions requiring single-point valuations, surveyors should adopt conservative positions within the range, while investment valuations may justify central or optimistic positions depending on client strategy.

Strategy 3: Dual-Scenario Valuation Modeling

The contradiction between near-term pessimism (-18%) and 12-month optimism (+33%) supports dual-scenario modeling for certain instruction types:

Scenario A: Near-Term Market Value (0-3 months)

- Reflects current negative sentiment

- Applies full downward adjustments to comparables

- Assumes weak buyer demand conditions

- Appropriate for: forced sales, immediate marketing, lender security valuations

Scenario B: Medium-Term Market Value (6-12 months)

- Incorporates expected modest recovery

- Applies moderate adjustments to comparables

- Assumes gradual demand improvement

- Appropriate for: development appraisals, investment acquisitions, strategic holdings

For matrimonial valuations or capital gains tax valuations, this dual-scenario approach provides courts or tax authorities with comprehensive value perspectives across different timeframes.

Strategy 4: Rental Market Integration for Investment Properties

The February survey reveals continued rental market strength with tenant demand stable at +2% and 20% of participants expecting rents to rise over three months, despite landlord instructions remaining negative at -27%.[1] This creates distinct valuation considerations for buy-to-let properties:

Investment Valuation Adjustments:

🏘️ Yield compression risk: Falling capital values combined with rising rents compress yields, potentially making properties more attractive to investors on an income basis

🏘️ Rental growth assumptions: Support 2-3% annual rental growth projections in base case scenarios, with 3-5% in supply-constrained areas

🏘️ Void period reductions: Tightening rental stock suggests shorter void periods between tenancies, improving cash flow assumptions

🏘️ Tenant quality improvements: Strong demand enables landlords to be more selective, potentially reducing default risk in discounted cash flow models

When conducting shared ownership valuations or Right to Buy valuations, surveyors should explicitly model the rental component separately from capital value components, as these markets are diverging significantly.

Strategy 5: Geopolitical Risk Factor Incorporation

The survey explicitly highlights Middle East tensions and rising energy prices as factors increasing the likelihood that mortgage rates will remain higher for longer.[1][3] This external risk factor should inform:

Mortgage Rate Sensitivity Analysis:

- Base case: Current mortgage rates persist through 2026

- Optimistic case: 0.25-0.5% reduction by Q4 2026

- Pessimistic case: 0.25-0.5% increase if geopolitical conditions deteriorate

Energy Efficiency Premium Adjustments:

Properties with superior EPC ratings (A-B) may command increasing premiums as energy price concerns persist. Consider:

- Standard premium: 2-3% for EPC A-B vs. EPC D

- Enhanced premium in current conditions: 3-5% for EPC A-B vs. EPC D

- Discount for poor efficiency: 5-7% for EPC F-G vs. EPC D

These adjustments should be documented in the valuation report with explicit reference to the energy price concerns highlighted in the RICS survey data.

Strategy 6: Transaction Evidence Currency Verification

With agreed sales at -12% and weak transaction momentum,[1] the currency of comparable evidence becomes critical. Implement rigorous verification protocols:

Evidence Currency Checklist:

☑️ Verify actual completion dates rather than relying on initial agreement dates

☑️ Confirm no renegotiations occurred between agreement and completion

☑️ Identify any seller concessions (furniture, legal fee contributions, repairs) that affect reported price

☑️ Assess buyer financing (mortgage vs. cash) as mortgage-dependent sales may be more distressed

☑️ Review marketing period – properties that sold quickly may not reflect current market conditions

For surveyors working on valuation cost assessments, this enhanced due diligence may justify slightly higher fee structures given the additional verification work required in volatile markets.

Sector-Specific Considerations: Applying Survey Data Across Property Types

While the RICS February 2026 survey focuses on residential markets broadly, different property sectors within the residential category respond differently to the identified market shifts. Surveyors must calibrate valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts according to specific property types and buyer segments.

First-Time Buyer Properties (Sub-£300k)

Market Characteristics:

- Most sensitive to mortgage rate changes due to high loan-to-value requirements

- Buyer demand collapse to -26% disproportionately affects this segment[1]

- Limited cash buyer competition provides less price support

Valuation Adjustments:

- Apply full regional adjustment factors without moderation

- Increase time adjustments by 20-30% relative to higher-value properties

- Assume extended marketing periods (8-12 weeks vs. historical 6-8 weeks)

- Consider stamp duty threshold effects carefully for properties near £250k-£300k bands

Family Homes (£300k-£750k)

Market Characteristics:

- Moderate mortgage dependency but larger deposit cushions

- More stable buyer pool with established equity from previous properties

- School catchment and location factors provide resilience

Valuation Adjustments:

- Apply standard regional adjustment factors as outlined in adjustment matrix

- Maintain moderate time adjustments (0.5-0.8% per month in negative markets)

- Location-specific factors (schools, transport) may justify premium stability even in weak markets

- Consider seasonal factors more carefully as family buyers concentrate activity around school terms

Prime Properties (£750k+)

Market Characteristics:

- Higher cash buyer proportion reduces mortgage rate sensitivity

- London prime market particularly affected by sentiment collapse[1]

- International buyer exposure adds currency and geopolitical risk factors

Valuation Adjustments:

- Bifurcated approach: London prime requires aggressive adjustments; regional prime more stable

- Weight recent transactions very heavily (60-70% of evidence base)

- Consider international buyer sentiment as separate factor beyond RICS survey data

- Luxury features and specifications maintain value better than location premiums in weak markets

Buy-to-Let Investment Properties

Market Characteristics:

- Rental market strength (+20% expecting rent rises) provides value support[1]

- Landlord instructions negative at -27% creating supply constraint[1]

- Investor buyers less emotional, more yield-focused than owner-occupiers

Valuation Adjustments:

- Dual methodology: Both comparable sales and investment method (yield-based)

- Yield-based valuations may exceed comparable evidence in current market

- Apply rental growth assumptions of 2-4% annually

- Consider regulatory risk (potential further landlord legislation) as downward pressure

- Tenant demand strength supports reduced void period assumptions

When conducting Help to Buy valuations, surveyors should particularly note the first-time buyer market weakness, as this segment forms the core Help to Buy demographic.

Reporting and Communication: Conveying Valuation Adjustments to Clients and Lenders

Professional valuation reporting must transparently communicate how valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts have been incorporated into the final value conclusion. Clear documentation protects surveyors from future challenge while helping clients understand current market complexities.

Essential Report Components

1. Market Conditions Section (Enhanced)

Standard market conditions commentary should be expanded to include:

- Specific RICS survey metrics relevant to the subject property location and type

- Regional divergence explanation if property is in particularly strong or weak area

- Sentiment trend analysis showing how near-term pessimism contrasts with 12-month expectations

- External risk factors (geopolitical, energy prices, mortgage rate outlook) cited in survey[1][3]

Example Commentary:

"The RICS February 2026 Residential Survey indicates near-term price expectations of -18% nationally, with the South East region recording -24% current price momentum. This represents a significant deterioration from January's -6% reading. However, 12-month expectations remain positive at +33%, suggesting current weakness may be temporary. These conditions have informed the valuation approach as detailed below."

2. Comparable Evidence Adjustment Table (Detailed)

Create explicit adjustment tables showing:

| Comparable | Sale Date | Unadjusted Price | Time Adjustment | Market Condition Adjustment | Other Adjustments | Adjusted Price |

|---|---|---|---|---|---|---|

| Comp 1 | Jan 2026 | £450,000 | -1.5% (-£6,750) | -1.0% (volatility) | +2.0% (condition) | £443,250 |

| Comp 2 | Dec 2025 | £465,000 | -2.5% (-£11,625) | -1.5% (volatility) | -1.0% (location) | £447,600 |

| Comp 3 | Feb 2026 | £440,000 | 0% | 0% | +1.5% (size) | £446,600 |

This transparency demonstrates how survey data directly influenced time and market condition adjustments.

3. Valuation Range and Uncertainty Disclosure

Explicitly state the valuation range and reasoning:

"Given current market volatility as evidenced by the RICS February 2026 survey, a valuation range of ±6% has been applied (compared to standard ±4%). This wider range reflects heightened uncertainty in comparable evidence reliability and rapid sentiment shifts affecting buyer behavior."

4. Scenario Analysis (Where Appropriate)

For investment, development, or strategic instructions, include scenario modeling:

Scenario A (Near-term – pessimistic): £445,000

Scenario B (Base case – current conditions): £465,000

Scenario C (12-month – modest recovery): £485,000

Link each scenario to specific RICS survey metrics and explain which scenario is most appropriate for the instruction purpose.

Lender-Specific Reporting Considerations

When preparing valuations for mortgage lending purposes, additional considerations apply:

🏦 Loan-to-Value Impact: Explain if current market weakness affects LTV calculations and security adequacy

🏦 Marketability Assessment: Address whether negative buyer demand (-26%)[1] affects forced sale scenarios or repossession values

🏦 Forward Value Opinions: If lender requests forward value (e.g., for new-build completions), explicitly model the near-term negative sentiment vs. 12-month recovery expectations

🏦 Regional Risk Flagging: Highlight if property is in London or South East where sentiment collapse is most severe[1]

Client Communication Strategies

For clients unfamiliar with valuation methodology, consider supplementary communication:

Simplified Summary Document:

- One-page summary of key RICS survey findings relevant to their property

- Visual graphics showing regional performance differences

- Explanation of why their valuation may differ from expectations based on older market data

- Timeline showing near-term weakness vs. medium-term recovery expectations

This educational approach helps manage client expectations and reduces disputes over valuation conclusions that may be lower than anticipated.

Future Outlook: Monitoring Market Evolution Beyond February 2026

The RICS survey operates on a monthly cycle, with the next embargo date announced as March 9, 2026.[2] Surveyors applying valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts must recognize that current adjustments represent a snapshot of rapidly evolving conditions requiring ongoing monitoring and methodology refinement.

Key Indicators to Monitor

Monthly RICS Survey Metrics:

📈 Near-term price expectations: Watch for stabilization (movement back toward zero) or further deterioration (deeper negative readings)

📈 Buyer demand trends: Monitor whether -26% represents a trough or continued decline[1]

📈 Regional divergence patterns: Track whether London/South East weakness spreads northward or remains geographically contained

📈 12-month expectations: Assess if +33% optimism holds or erodes as near-term weakness persists[1]

External Economic Indicators:

💷 Mortgage rate movements: Bank of England policy decisions and swap rate trends affecting fixed-rate mortgage pricing

💷 Inflation trajectory: Core inflation trends influencing rate-cut timing expectations

💷 Employment data: Labor market strength supporting buyer confidence and mortgage affordability

💷 Geopolitical developments: Middle East tensions and energy price movements affecting rate outlook[1][3]

Adjustment Methodology Evolution

As market conditions evolve through spring and summer 2026, valuation adjustment factors should be recalibrated:

If Near-Term Sentiment Stabilizes (moves toward zero):

- Reduce time adjustment factors by 30-50%

- Narrow valuation ranges back toward standard ±4-5%

- Increase weighting on older comparable evidence (4-6 months)

- Reduce volatility premiums in yield-based investment valuations

If Near-Term Sentiment Deteriorates Further (exceeds -20%):

- Increase time adjustment factors by 20-30%

- Expand valuation ranges to ±7-8% in most affected regions

- Consider formal "material uncertainty" declarations under RICS guidance[4]

- Implement mandatory dual-scenario modeling for all instruction types

If Regional Divergence Intensifies:

- Develop location-specific adjustment matrices at sub-regional level (borough/county rather than broad region)

- Increase comparable evidence radius restrictions (prioritize hyper-local evidence)

- Weight local surveyor sentiment over national data where significant divergence exists

Professional Development and Knowledge Sharing

Surveyors should engage in continuous professional development focused on volatile market valuation:

✓ RICS guidance review: Monitor for updated guidance on valuing in extreme or uncertain conditions[4]

✓ Peer consultation: Engage with local surveyor networks to compare adjustment approaches and evidence interpretation

✓ Lender liaison: Maintain dialogue with mortgage lender valuation panels to understand their risk appetite and reporting expectations

✓ Client education: Proactively communicate market changes to regular clients before instructions arise

✓ Methodology documentation: Maintain detailed records of adjustment rationale to support consistency and defend approaches if challenged

For surveyors offering specific defect surveys or commercial building surveys, similar monitoring and adjustment principles apply, adapted to commercial market indicators and sentiment data.

Conclusion

The RICS February 2026 Residential Survey presents chartered surveyors with one of the most complex valuation environments in recent years, characterized by sharp near-term pessimism (-18%), collapsed buyer demand (-26%), and dramatic regional divergence, particularly London's 49-percentage-point sentiment collapse.[1] Yet this challenging landscape also reveals opportunities: stable supply conditions, continued rental market strength, and persistent 12-month optimism (+33%) suggest current weakness may prove temporary rather than structural.

Implementing effective valuation adjustments from RICS February 2026 Residential Survey: Strategies for Spring Market Shifts requires abandoning one-size-fits-all approaches in favor of sophisticated, multi-layered methodologies. Surveyors must calibrate adjustments to specific regions (applying aggressive factors in London and South East, moderate adjustments in Northern regions), property types (differentiating first-time buyer properties from prime homes), and timeframes (distinguishing near-term market value from medium-term investment scenarios).

The practical strategies outlined—enhanced comparable evidence weighting, volatility premium integration, dual-scenario modeling, rental market integration, geopolitical risk incorporation, and rigorous transaction verification—provide a framework for maintaining RICS Red Book compliance while accurately reflecting current market realities. Transparent reporting that explicitly documents how survey data influenced adjustment decisions protects professional standards while educating clients about complex market dynamics.

Actionable Next Steps

For Surveyors:

- Review current adjustment matrices against February 2026 survey data and recalibrate regional factors immediately

- Implement enhanced comparable evidence weighting protocols prioritizing transactions from February-March 2026

- Expand valuation ranges to ±5-7% (or ±6-8% in London) to reflect heightened volatility

- Enhance report commentary sections to explicitly reference RICS survey metrics and explain adjustment rationale

- Schedule monthly review of RICS survey updates to track market evolution and adjust methodologies accordingly

For Property Professionals:

- Obtain current RICS valuations before listing properties to understand realistic market value in current conditions

- Review existing valuations conducted in Q4 2025 or earlier, as these may not reflect February sentiment deterioration

- Consider timing strategies weighing near-term weakness against 12-month recovery expectations for non-urgent transactions

- Assess regional exposure particularly for portfolios with significant London or South East concentration

For Buyers and Investors:

- Recognize valuation adjustments reflect genuine market weakness rather than surveyor conservatism

- Request scenario analysis for investment purchases to understand value across different timeframes

- Prioritize locations showing resilience (Northern Ireland, Scotland, North West) if seeking stability

- Consider rental market strength when evaluating buy-to-let opportunities, as income returns may offset capital value uncertainty

The spring 2026 market presents challenges but also opportunities for those who understand and appropriately respond to the mixed signals revealed in the RICS February survey. By applying rigorous, data-informed valuation adjustments while maintaining transparent professional standards, chartered surveyors can navigate this complex environment while serving clients effectively and protecting their own professional positions.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[4] Real Estate Valuation Extreme Conditions – https://ww3.rics.org/uk/en/journals/property-journal/real-estate-valuation-extreme-conditions.html

[5] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets