{"cover":"Professional landscape format (1536×1024) hero image featuring bold text overlay 'RICS January 2026 Residential Survey: Valuation Surveyors Navigate Market Stabilisation' in extra large 72pt white sans-serif font with dark gradient shadow, positioned in upper third with perfect center alignment. Background shows split-screen composition: left side displays modern UK residential properties with 'For Sale' signs in northern regions showing upward price arrows, right side shows surveyor reviewing property data on tablet with RICS charts and regional heat maps visible. Color scheme: professional navy blue, white, gold accents representing stability and growth. High contrast, magazine cover quality, editorial style with subtle UK map overlay showing regional price variations. Photorealistic, authoritative, business publication aesthetic","content":["Landscape format (1536×1024) detailed infographic showing UK map with color-coded regional house price performance data from RICS January 2026 survey. Scotland and Northern Ireland highlighted in deep green showing strongest growth, North West and North England in light green showing positive trends, Southern regions (London, South East, South West, East Anglia) in amber showing affordability challenges. Large data callouts display key statistics: net balance -10% for prices, -15% for buyer enquiries, -9% for agreed sales. Modern clean design with percentage indicators, directional arrows, and legend. Professional color palette of blues, greens, and golds. Chart includes timeline showing improvement from October 2025 to January 2026 with upward trajectory lines. High-quality business intelligence visualization style","Landscape format (1536×1024) professional scene showing RICS chartered surveyor conducting residential property valuation in contemporary UK home. Surveyor in business attire using digital tablet and laser measuring device, examining property features with clipboard showing valuation checklist. Background shows modern living room with large windows, neutral decor. Overlay graphics display transparent data panels with key January 2026 metrics: +35% twelve-month sales outlook, +43% price expectations, supply constraints at +1% new instructions. Split-screen effect shows comparison between northern property (higher valuation) and southern property (affordability pressures). Professional lighting, documentary photography style, authoritative business aesthetic with RICS branding elements subtly visible","Landscape format (1536×1024) sophisticated dual-panel visualization comparing sales and lettings markets from RICS January 2026 data. Left panel shows residential sales market with upward trending line graphs, buyer enquiry improvements from -29% November to -15% January, agreed sales momentum chart reaching -9%. Right panel displays lettings market dynamics with tenant demand at +13%, landlord instructions constrained at -24%, rental price expectations bar chart showing +28% growth forecast. Central dividing element features professional surveyor silhouette with briefcase. Color coding: sales market in professional blues, lettings market in warm golds and oranges. Includes forward-looking projections: rental growth acceleration from 2.2% to 4.0% by 2027. Clean infographic style with data visualization best practices, business publication quality"]"}

The UK residential property market is showing clear signs of stabilisation in early 2026, but the recovery is far from uniform. The RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market reveal a complex landscape where regional disparities are widening, buyer confidence is gradually returning, and valuation professionals face both opportunities and challenges. With house prices stabilising nationally and optimistic 12-month outlooks emerging, surveyors must adapt their appraisal strategies to reflect these evolving market dynamics.

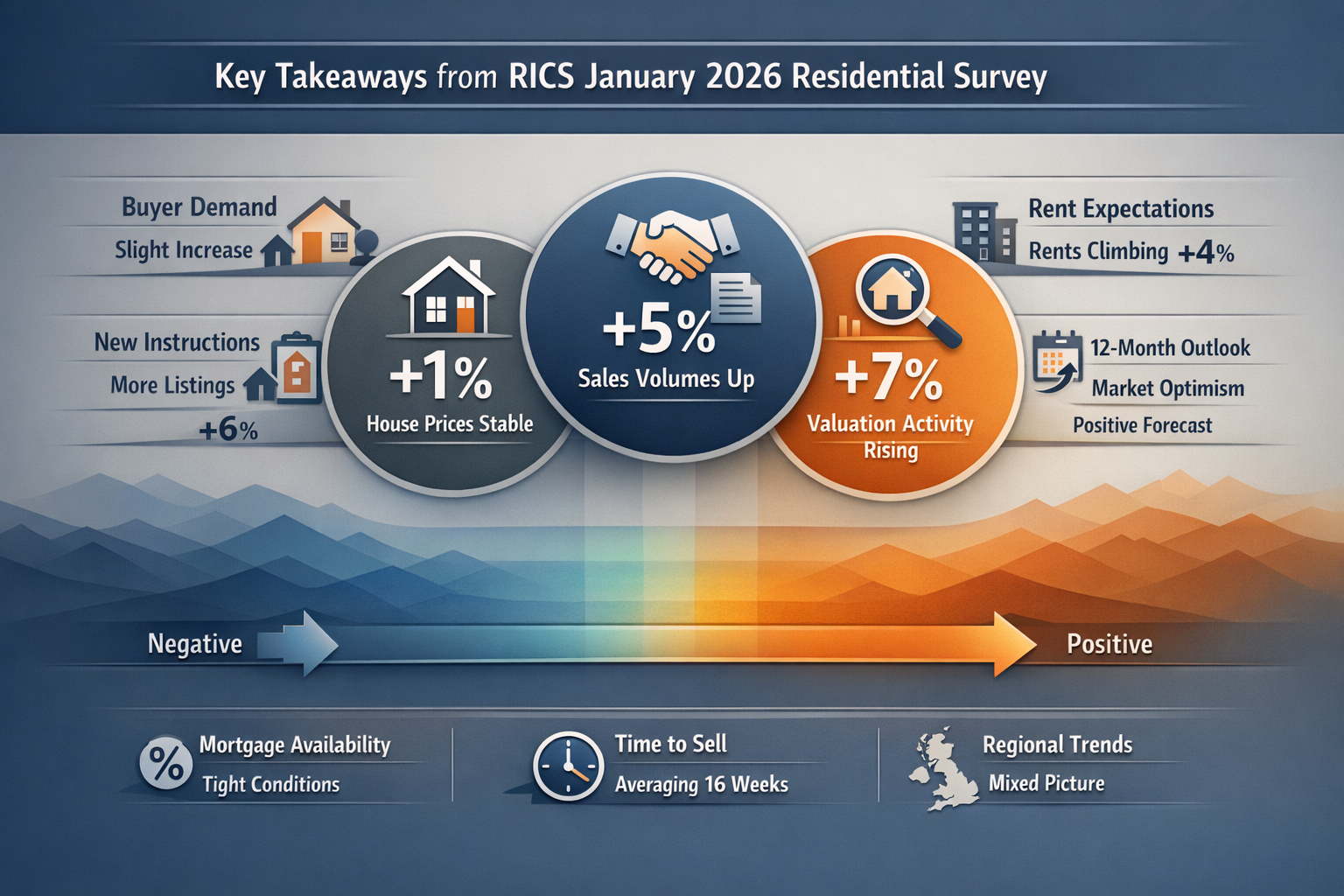

The latest data shows the net balance for prices over the past three months stood at -10%, a significant improvement from the low of -19% in October 2025[2]. This shift signals a potential turning point that valuation surveyors cannot afford to ignore. As new buyer enquiries improve and agreed sales momentum strengthens, the demand for accurate, regionally-informed RICS valuations is set to increase throughout 2026.

Key Takeaways

- 📈 House prices stabilising: The net balance improved to -10% in January 2026, up from -19% in October 2025, indicating reduced downward pressure on valuations

- 🌍 Regional divergence intensifying: Scotland and Northern Ireland lead price growth while southern regions lag due to affordability constraints, requiring differentiated valuation approaches

- 🔮 Strong 12-month outlook: A net balance of +35% for sales activity expectations and +43% for price expectations suggest sustained demand for valuation services throughout 2026

- 🏘️ Supply constraints persist: New instructions remain essentially flat at +1%, supporting property values and creating ongoing appraisal demand

- 🏢 Lettings market accelerating: Rental growth expectations at +28% with tenant demand rising and landlord supply constrained present new opportunities for investment property valuations

Understanding the RICS January 2026 Residential Survey Insights: National Trends

The RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market paint a picture of cautious optimism tempered by regional realities. The survey, which polls chartered surveyors across the UK, provides invaluable intelligence for professionals conducting RICS building surveys and property valuations.

House Price Stabilisation: The Numbers Behind the Trend

The three-month house price net balance of -10% represents a substantial improvement from the depths of late 2025[2]. While still negative, this metric indicates that fewer surveyors are reporting price declines compared to those reporting increases. This stabilisation has critical implications for valuation methodology:

- Reduced volatility in comparable property analysis

- Greater confidence in forward-looking valuation projections

- Improved accuracy in mortgage lending valuations

- Enhanced reliability of investment appraisals

The improvement in buyer enquiries—from -29% in November 2025 to -15% in January 2026[2]—suggests that demand-side pressures are easing. This trend directly impacts the volume of RICS building surveys Level 3 and other comprehensive assessments that buyers commission before completing purchases.

Agreed Sales Momentum: Transaction Volume Recovery

Perhaps most encouraging for valuation surveyors is the agreed sales net balance reaching -9% in January, the least negative reading since June 2025[1]. This metric indicates that more properties are progressing from listing to sale, which translates directly into increased demand for:

- Pre-purchase building surveys

- Mortgage valuation reports

- Investment property appraisals

- Help to Buy valuations

The strengthening transaction pipeline means surveyors should prepare for sustained workload increases throughout 2026, particularly as the 12-month sales outlook surged to a net balance of +35%[2]—the strongest reading since December 2024.

Supply Constraints: The Persistent Challenge

While demand indicators improve, supply remains constrained. New instructions recorded a net balance of only +1% in January, essentially flat from December's -1%[1]. This supply-demand imbalance has several implications for valuation practice:

| Market Condition | Impact on Valuations | Surveyor Response |

|---|---|---|

| Limited inventory | Upward pressure on prices | Use extended comparable timeframes |

| Reduced choice | Faster sales for quality properties | Adjust marketing period assumptions |

| Competitive bidding | Properties exceeding asking prices | Consider recent over-asking transactions |

| Motivated sellers | Quality properties attract premium | Differentiate between distressed and quality stock |

This constrained supply environment requires surveyors to be particularly diligent when selecting comparable evidence and justifying valuation conclusions.

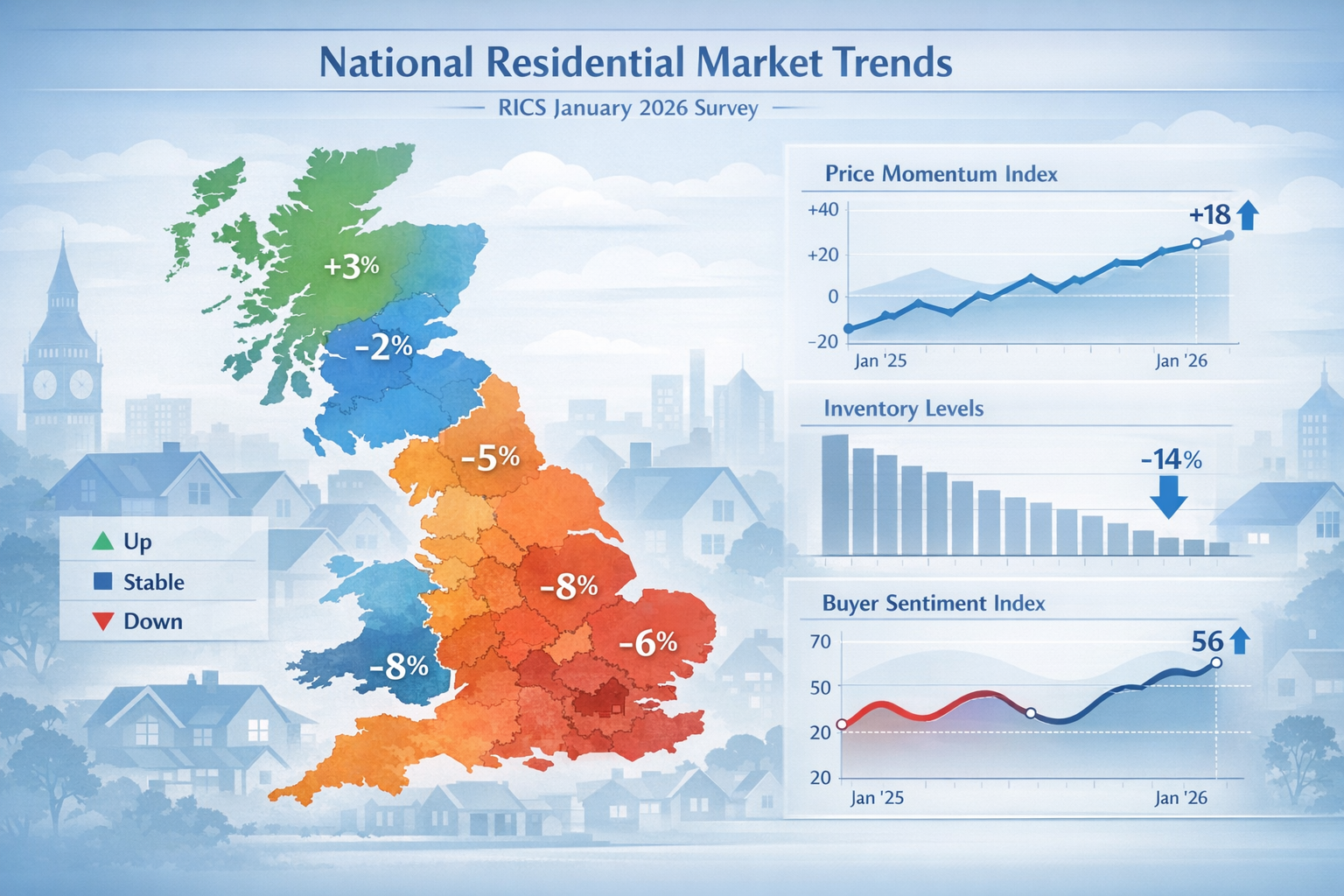

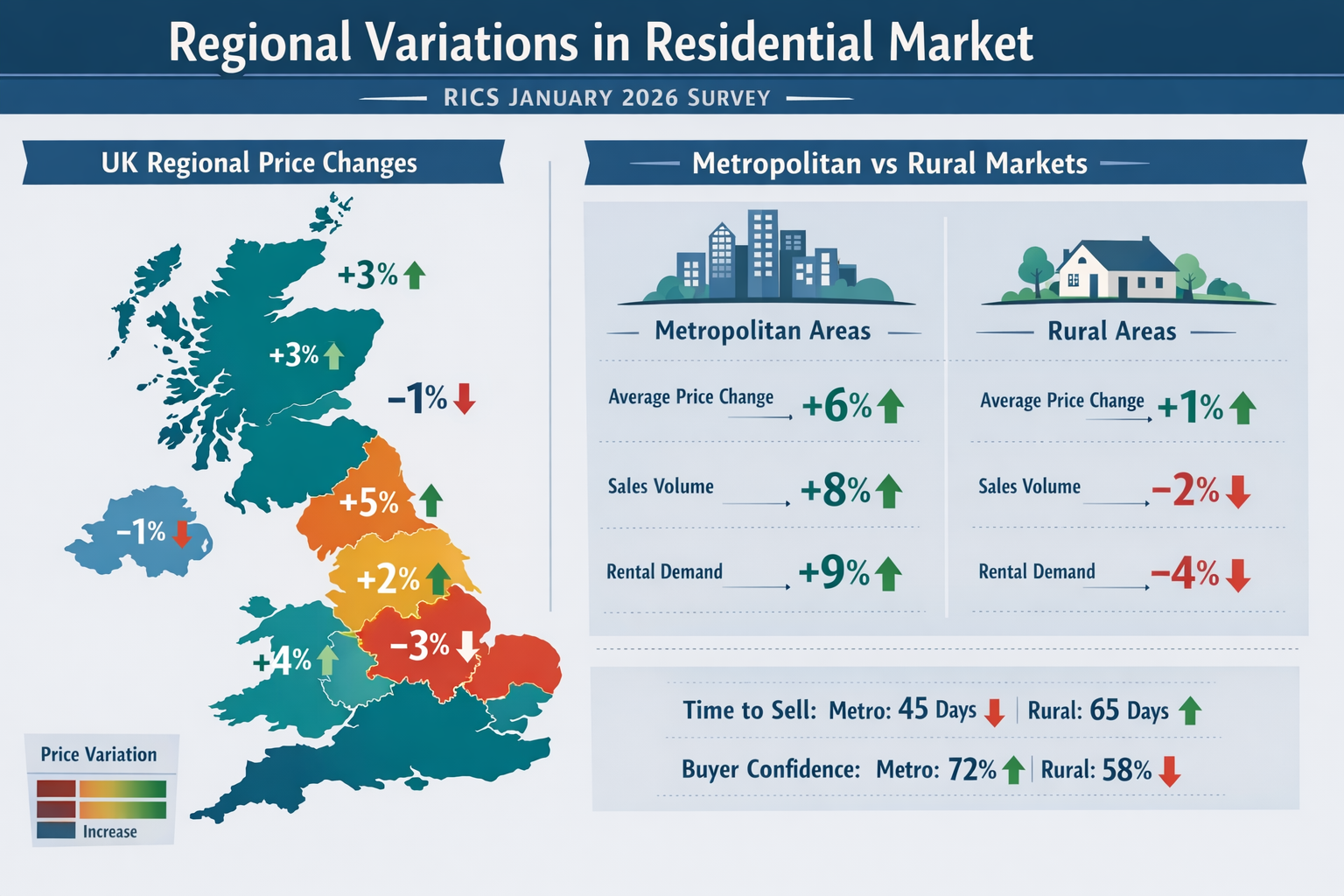

RICS January 2026 Residential Survey Insights: Regional Variations and Valuation Implications

The RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market reveal that national averages mask significant regional disparities. Understanding these variations is essential for accurate property appraisals across different UK markets.

The North-South Divide: Price Performance Gaps

Scotland and Northern Ireland are reporting the strongest price growth, with upward trends also evident in the North West and North of England[2]. This regional strength contrasts sharply with continued weakness in southern regions, where London, the South East, South West, and East Anglia lag the national average due to ongoing affordability challenges[2].

For valuation surveyors, this divergence requires:

Northern Regions Strategy

- Upward valuation adjustments: Incorporate positive momentum into comparable analysis

- Shorter comparable timeframes: Recent transactions more relevant in rising markets

- Growth assumptions: Build in modest appreciation for forward-looking valuations

- Regional expertise: Chartered surveyors in the North West possess critical local market knowledge

Southern Regions Approach

- Affordability constraints: Factor in income-to-price ratios limiting buyer pools

- Extended marketing periods: Properties may take longer to sell at asking prices

- Conservative adjustments: Apply cautious comparable analysis

- Location-specific analysis: Chartered surveyors in Central London, South East London, and Surrey must account for local micro-markets

Regional Valuation Case Studies

Consider two comparable three-bedroom semi-detached properties built in 2010:

Property A – Manchester (North West)

- Recent comparable sales showing 2-3% quarterly growth

- Strong buyer demand with multiple viewings typical

- Properties selling at or slightly above asking prices

- Valuation approach: Use recent comparables, apply modest positive adjustment for momentum

Property B – Guildford (South East)

- Comparable sales showing flat to slight decline over six months

- Reduced buyer activity with extended marketing periods

- Properties requiring price reductions to achieve sales

- Valuation approach: Use broader comparable timeframe, apply conservative adjustments, consider affordability metrics

This regional differentiation is precisely why chartered surveyors in Guildford and other southern locations must employ different methodologies than their northern counterparts.

The Affordability Factor in Southern Markets

The persistent affordability challenges in southern regions stem from:

- Higher absolute prices relative to local incomes

- Larger deposits required limiting first-time buyer access

- Stamp duty impacts more pronounced at higher price points

- Economic uncertainty affecting London's financial sector employment

Valuation surveyors working in these markets should incorporate affordability metrics into their analysis, including:

- Average earnings data for the locality

- Mortgage affordability calculations at prevailing rates

- First-time buyer accessibility analysis

- Comparative affordability versus rental costs

These factors are particularly relevant when conducting shared ownership valuations or right to buy valuations, where affordability directly impacts market value.

Applying RICS January 2026 Residential Survey Insights to Valuation Practice

The RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market provide actionable intelligence that should inform every aspect of valuation practice. Here's how to integrate these insights into professional surveying work.

Forward-Looking Valuation Adjustments

The survey's most striking finding is the +43% net balance of respondents anticipating higher prices over the year ahead—the most positive outlook since February 2025[2]. This optimism, combined with the +35% twelve-month sales outlook[2], suggests surveyors should:

Incorporate Market Momentum

When conducting valuations for different purposes, consider how market trajectory affects value:

- Mortgage lending valuations: Apply current market value with recognition of improving conditions

- Investment appraisals: Factor positive momentum into rental yield and capital growth projections

- Insurance reinstatement valuations: Consider construction cost inflation in rebuilding estimates

- Capital gains tax valuations: Document market conditions at valuation date

Adjust Comparable Analysis

The improving market requires refinements to comparable selection:

- Weighting recent transactions more heavily: In stabilising markets, recent sales better reflect current conditions

- Adjusting for market movement: Apply time adjustments to older comparables to reflect improving sentiment

- Considering agreed sales: Pending transactions provide forward-looking market intelligence

- Regional differentiation: Apply location-specific adjustments based on local market performance

The Three-Month Caution Window

While twelve-month outlooks are strongly positive, three-month sales expectations eased to a net balance of +4%[2], reflecting short-term caution. This suggests:

"Valuers should expect continued gradual momentum rather than sharp market movements in the immediate months ahead."

This measured approach is particularly important for:

- Development appraisals with near-term completion dates

- Forced sale valuations requiring quick disposal

- Specific defect surveys where remediation costs impact immediate marketability

Supply Constraints and Valuation Methodology

The persistent supply constraint—new instructions at just +1%[1]—creates specific challenges for valuation professionals:

Comparable Evidence Scarcity

When comparable transactions are limited:

- Expand geographic search area: Look to adjacent neighborhoods with similar characteristics

- Extend time period: Use older comparables with appropriate time adjustments

- Consider asking prices: Analyze listing prices alongside achieved sales for market intelligence

- Weight quality over quantity: Better to use fewer, highly relevant comparables than many poor matches

Market Value vs. Worth

In constrained supply environments, distinguish between:

- Market value: What a property would achieve in an open market transaction

- Investment worth: Value to a specific buyer with particular circumstances

- Forced sale value: Price achievable under time-constrained disposal

Understanding these distinctions is fundamental to Red Book valuation compliance and professional practice standards.

Lettings Market Implications for Investment Valuations

The lettings market data from the RICS January 2026 survey has profound implications for investment property valuations. Tenant demand reached +13% (seasonally adjusted) while landlord instructions remained constrained at -24%[1], driving rental price expectations to +28%[1].

Rental Growth Projections

Capital Economics analysis suggests market rents will accelerate from 2.2% in late 2025 to 2.8% in 2026 and 4.0% in 2027[3]. Valuation surveyors should:

- Incorporate rental growth into discounted cash flow models

- Adjust capitalization rates to reflect improving rental market fundamentals

- Consider tenant demand strength when assessing void period assumptions

- Factor supply constraints into rental growth sustainability analysis

Investment Valuation Methodology

When valuing buy-to-let or multi-unit residential investments:

| Valuation Input | Current Market Condition | Adjustment Approach |

|---|---|---|

| Current rental income | Strong tenant demand (+13%) | Use upper quartile of rental range |

| Rental growth rate | Accelerating (2.8% 2026, 4.0% 2027) | Apply progressive growth assumptions |

| Void periods | Constrained supply (-24% instructions) | Reduce void assumptions vs. historical average |

| Tenant quality | High demand environment | Assume stronger covenant strength |

| Exit yield | Improving market sentiment | Apply modest yield compression |

These adjustments should be clearly documented and justified with reference to the RICS survey data and regional market conditions.

Practical Application: Valuation Report Enhancements

To leverage the RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market, enhance valuation reports with:

Market Context Section

Include a dedicated section covering:

- National market trends from the January 2026 RICS survey

- Regional-specific data relevant to the subject property location

- Forward-looking market indicators (12-month outlook)

- Supply-demand dynamics affecting the local market

Comparable Analysis Commentary

Strengthen comparable analysis by:

- Explaining why specific comparables were selected given market conditions

- Documenting any time adjustments applied to reflect market movement

- Noting regional performance variations affecting value conclusions

- Addressing supply constraints and their impact on comparable availability

Assumptions and Special Assumptions

Clearly state assumptions about:

- Market trajectory over the valuation horizon

- Regional economic conditions

- Supply-demand balance

- Buyer financing availability

This transparency is essential for RICS-registered valuers maintaining professional standards.

Strategic Opportunities for Valuation Surveyors in 2026

The stabilising market conditions revealed in the RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market create several strategic opportunities for surveying practices.

Expanding Service Offerings

As transaction volumes increase, consider expanding into:

- Pre-purchase surveys: The improving sales outlook (+35% for 12 months) will drive demand for comprehensive building surveys

- Investment appraisals: Strong lettings market fundamentals create opportunities for portfolio valuations

- Development appraisals: Stabilising prices reduce risk in development finance valuations

- Lease extension valuations: Improving market conditions affect lease extension calculations

Geographic Expansion

The regional performance variations suggest opportunities for practices to:

- Establish presence in high-growth regions: Scotland, Northern Ireland, and northern England

- Develop specialist expertise: Focus on specific regional markets with strong fundamentals

- Build referral networks: Partner with local agents in diverse geographic areas

- Offer remote valuation services: Leverage technology for broader geographic coverage

Technology Integration

The stabilising market provides an ideal environment to invest in:

- Data analytics platforms: Better track regional market trends and comparable evidence

- Digital reporting systems: Enhance report quality and delivery speed

- Market intelligence tools: Subscribe to real-time market data feeds

- Client portals: Improve communication and service delivery

Professional Development

Stay ahead of market developments through:

- RICS continuing professional development: Focus on market analysis and regional variations

- Specialist qualifications: Pursue additional credentials in investment valuation or specific property types

- Market research: Regularly review RICS surveys and economic forecasts

- Peer networking: Share insights with colleagues across different regions

Risk Management and Professional Standards

While market stabilisation is positive, valuation surveyors must maintain rigorous professional standards and risk management practices.

Avoiding Over-Optimism

The strong forward-looking sentiment (+43% price expectations) requires balanced judgment:

- Don't extrapolate excessively: Base valuations on current market evidence, not hoped-for future growth

- Maintain professional skepticism: Question whether local conditions match national trends

- Document conservatism: Explain any cautious adjustments in valuation reports

- Consider downside scenarios: Particularly for long-term investment appraisals

Regional Differentiation Discipline

The North-South divide demands rigorous regional analysis:

- Avoid national assumptions: Don't apply national trends to local markets without verification

- Verify local data: Cross-reference RICS survey findings with local transaction evidence

- Consult local experts: Engage chartered surveyors with specific regional expertise

- Document regional factors: Clearly explain how local conditions differ from national averages

Red Book Compliance

Ensure all valuations comply with RICS Valuation – Global Standards (Red Book):

- Basis of value: Clearly state whether market value, investment value, or other basis applies

- Assumptions and special assumptions: Document all material assumptions affecting value conclusions

- Comparable evidence: Provide sufficient detail on comparable transactions

- Market context: Include relevant market commentary based on current conditions

For guidance on Red Book valuation requirements, ensure your practice maintains current knowledge of professional standards.

Professional Indemnity Considerations

As transaction volumes increase, review professional indemnity insurance:

- Coverage limits: Ensure adequate for increased valuation volumes and property values

- Geographic coverage: Verify coverage extends to all regions where you practice

- Specialist activities: Confirm coverage for investment valuations, development appraisals, etc.

- Claims history: Maintain robust quality control to minimize claims risk

Conclusion

The RICS January 2026 Residential Survey Insights: Implications for Valuation Surveyors in a Stabilising Market reveal a property market at an important inflection point. With house prices stabilising, buyer enquiries improving, and strong 12-month outlooks emerging, valuation surveyors face both opportunities and responsibilities in 2026.

The key findings—a net balance of -10% for house prices (improving from -19% in October 2025), +35% for 12-month sales expectations, and +43% for price expectations—signal a market moving from decline to gradual recovery[2]. However, the widening North-South divide and persistent supply constraints at +1% for new instructions[1] require nuanced, regionally-informed valuation approaches.

Actionable Next Steps for Valuation Surveyors

To capitalize on these market conditions and maintain professional excellence:

- Update valuation methodologies to reflect stabilising market conditions and regional variations

- Enhance comparable analysis by weighting recent transactions more heavily and applying appropriate time adjustments

- Develop regional expertise through focused market research and local networking, particularly in high-growth areas

- Expand service offerings to capture increased demand for pre-purchase surveys, investment appraisals, and lettings market valuations

- Invest in technology to improve data analysis, market intelligence, and reporting capabilities

- Maintain rigorous standards by ensuring Red Book compliance and avoiding over-optimism despite positive sentiment

- Document market context thoroughly in all valuation reports, referencing RICS survey data and regional conditions

The stabilising market of 2026 presents valuation surveyors with the best operating environment since early 2024. Those who adapt their methodologies to reflect regional variations, incorporate forward-looking market intelligence, and maintain professional rigor will position themselves for success as transaction volumes increase throughout the year.

Whether conducting a comprehensive Level 3 building survey, preparing an investment valuation, or advising clients on which survey they need, the insights from the RICS January 2026 survey provide essential market intelligence for accurate, defensible property valuations in this evolving landscape.

References

[1] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[2] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[3] UK RICS Residential Market Survey Jan 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-jan-2026