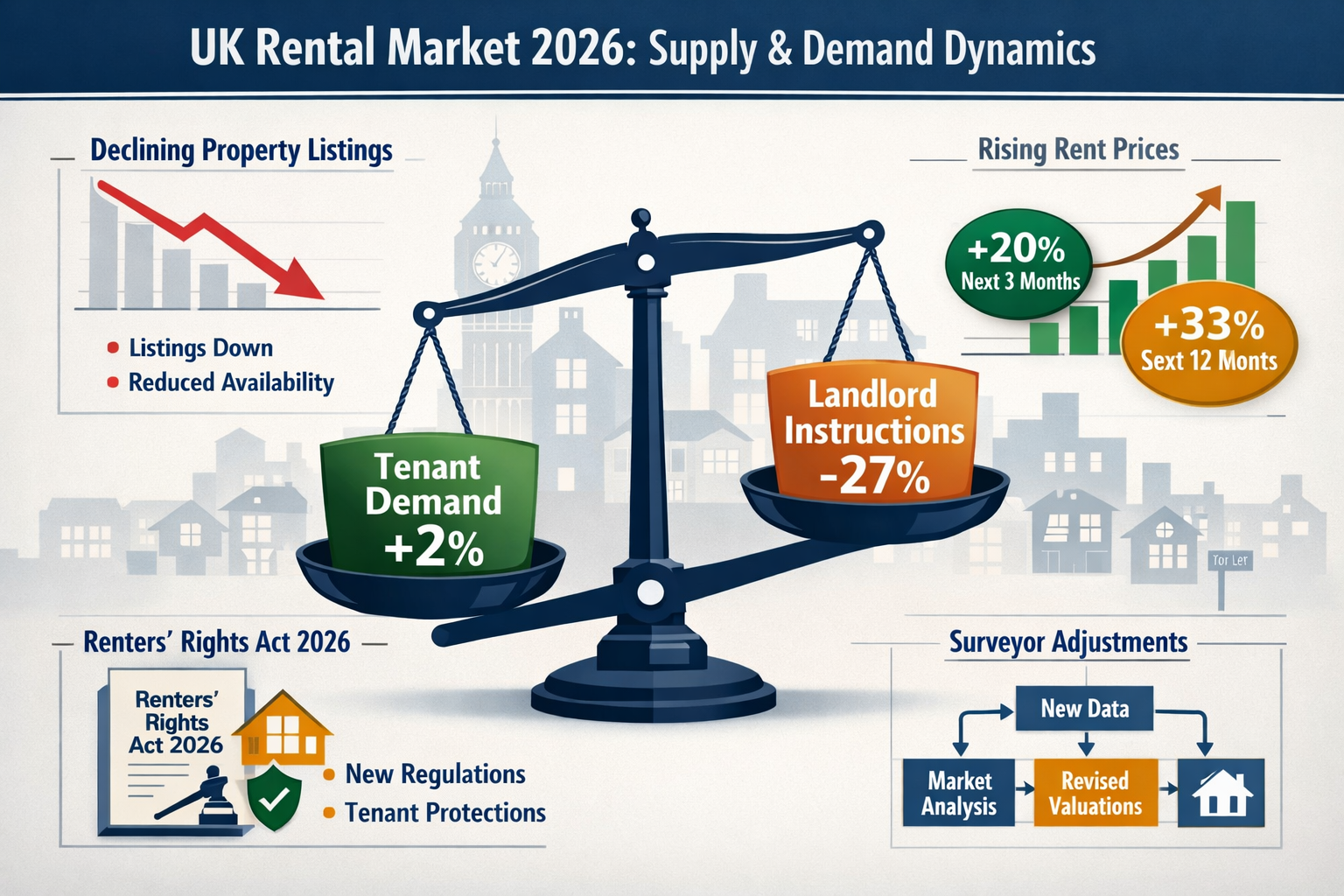

The UK rental market faces an unprecedented supply crisis: landlord instructions plummeted to -27% in February 2026, while tenant demand holds steady at +2%, creating a perfect storm that's pushing +20% of RICS surveyors to expect rent rises over the coming three months. This dramatic imbalance between supply and demand isn't just another market fluctuation—it represents a fundamental shift in how property professionals must approach rental valuations in 2026 and beyond. The Valuation Adjustments for Landlord Instructions Shortage: RICS Insights on +20% Rent Rise Expectations in 2026 reveal critical methodology changes that every surveyor, landlord, and property investor must understand to navigate this constrained market environment.

Key Takeaways

- Landlord instructions hit -27% in February 2026, creating an acute shortage of rental stock entering the spring market, the most severe supply constraint recorded in recent years [2]

- +20% of RICS surveyors expect rents to rise over the next three months, with +33% anticipating increases over a 12-month horizon, directly responding to supply shortages [2]

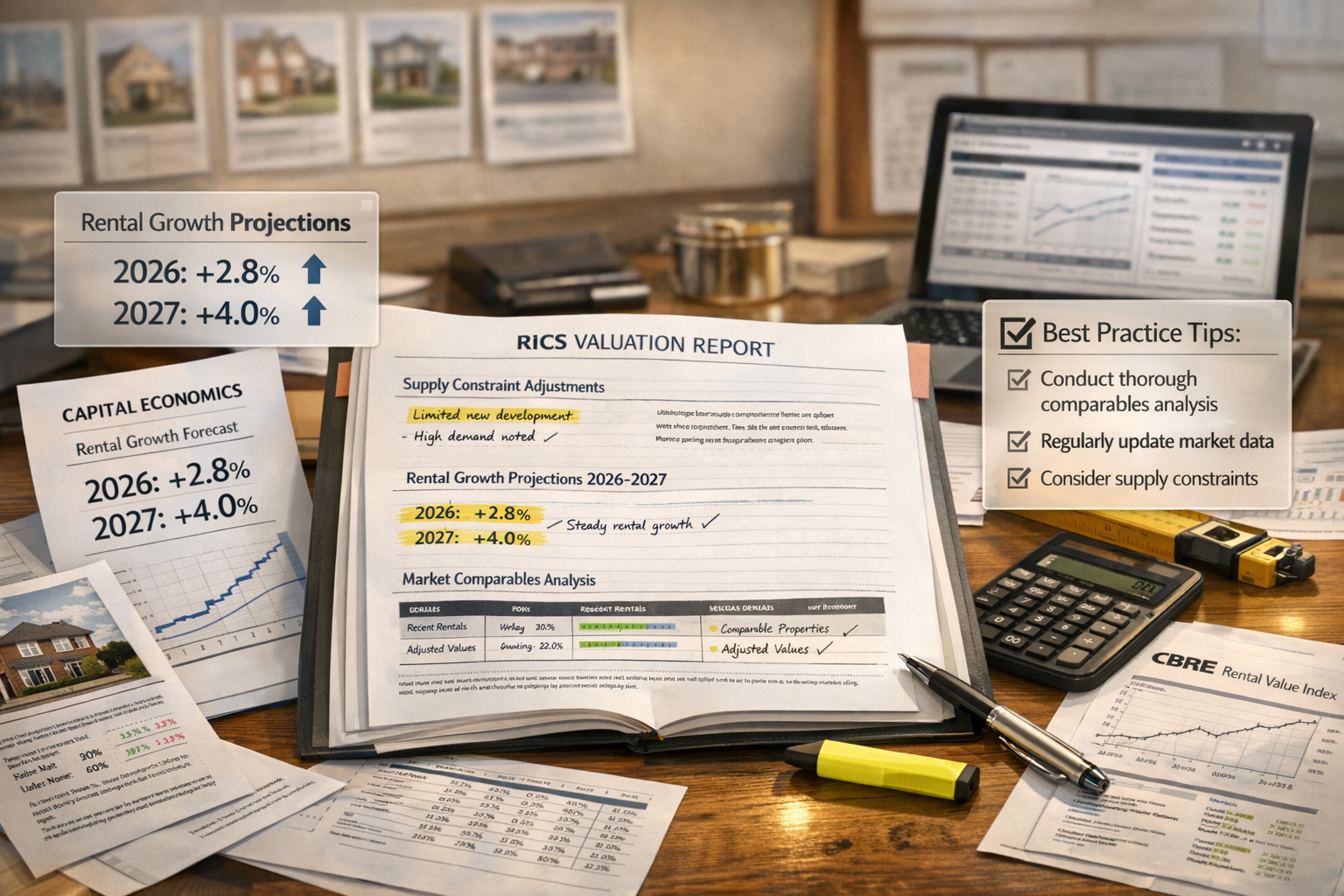

- Rental growth forecasts accelerate from 2.2% (late 2025) to 2.8% (2026) and 4.0% (2027), according to Capital Economics analysis of RICS data [6]

- Valuation adjustments must account for Private Rented Sector (PRS) supply constraints intensified by regulatory changes including the Renters' Rights Act implementation

- Professional surveyors require enhanced methodologies to accurately reflect market distortions caused by landlord exodus and persistent tenant demand

Understanding the Landlord Instructions Shortage: February 2026 RICS Data

The February 2026 RICS Residential Market Survey documents a troubling trend that has profound implications for property valuations across the UK. Landlord instructions—the metric measuring new rental properties entering the market—registered at -27%, indicating that significantly more surveyors reported decreases rather than increases in new landlord instructions [2]. This represents one of the most negative readings in the survey's history and signals a structural problem rather than seasonal variation.

The Supply-Demand Disconnect

While landlord instructions collapsed, tenant demand remained remarkably stable at +2% over the three months to February 2026 [2]. This modest but positive figure masks the intensity of competition for available properties. When supply contracts sharply while demand holds steady, the inevitable result is upward pressure on rental prices—exactly what RICS surveyors are now forecasting.

The mathematics of this imbalance are straightforward but consequential:

| Metric | February 2026 Reading | Market Impact |

|---|---|---|

| Landlord Instructions | -27% | Severe supply shortage |

| Tenant Demand | +2% | Stable, consistent pressure |

| Near-term Rent Expectations (3 months) | +20% | Strong upward momentum |

| 12-month Rent Expectations | +33% | Sustained growth confidence |

This divergence between supply and demand creates what economists call a "seller's market"—or in rental terms, a "landlord's market"—where property owners hold significant pricing power. For valuers registered with the RICS, this environment demands careful recalibration of valuation methodologies to accurately reflect these market distortions.

Why Landlords Are Exiting the Market

The landlord instruction shortage didn't emerge in a vacuum. Several converging factors have driven property owners to reduce their rental portfolios or exit the Private Rented Sector entirely:

🏛️ Regulatory Pressure: The anticipated implementation of the Renters' Rights Act has created uncertainty around landlord-tenant relationships, eviction procedures, and property management obligations.

💰 Tax Changes: Cumulative effects of Section 24 mortgage interest relief restrictions, higher stamp duty surcharges on additional properties, and capital gains tax considerations have eroded rental investment returns.

📊 Rising Costs: Increased mortgage rates, energy efficiency requirements (EPC regulations), and maintenance costs have squeezed profit margins for smaller landlords.

⚖️ Compliance Burden: Growing regulatory complexity around licensing, safety certificates, and tenant protections has made portfolio management more resource-intensive.

These structural pressures explain why the landlord instruction shortage persists despite rising rents—the very conditions that would typically attract new supply. Professional surveyors conducting Manchester valuation reports and similar assessments must factor these supply-side constraints into their rental value projections.

RICS Insights on +20% Rent Rise Expectations: Valuation Methodology Implications

The +20% net balance of surveyors expecting rent rises over the coming three months represents a significant shift in market sentiment that directly impacts how professionals approach rental valuations in 2026 [2]. This figure—up from +16% in earlier surveys—indicates growing confidence that rental price growth will accelerate rather than moderate.

Short-term vs. Long-term Rental Growth Projections

RICS data reveals two distinct timeframes for rental growth expectations, each requiring different valuation considerations:

Three-Month Outlook (+20% Net Balance): This near-term expectation reflects immediate supply-demand pressures. Surveyors anticipating rent rises in this timeframe are responding to current market conditions—the -27% landlord instructions shortage meeting stable tenant demand. For valuations with short holding periods or imminent lease renewals, this metric provides crucial guidance [2].

12-Month Outlook (+33% Net Balance): The longer-term projection shows even stronger confidence in rental growth, with +33% of respondents expecting higher prices over a 12-month horizon [2]. This suggests surveyors believe the supply shortage will persist and potentially intensify, creating sustained upward pressure on rents.

Capital Economics' analysis of the RICS data projects specific growth rates:

- 2026 Forecast: 2.8% annual rental growth (up from 2.2% in late 2025)

- 2027 Forecast: 4.0% annual rental growth, reflecting continued supply-demand imbalances [6]

These projections represent a sharp moderation from the 12% peak rental growth experienced in 2022/early 2023, but they still exceed general inflation expectations and wage growth in many sectors [5].

Adjusting Comparable Evidence for Supply Constraints

Traditional rental valuation methodology relies heavily on comparable evidence—recent lettings of similar properties in the same area. However, the current market environment introduces significant distortions that require careful adjustment:

1. Transaction Volume Adjustments: With fewer properties available, the pool of comparable evidence shrinks. Surveyors must cast wider geographical nets or accept older comparables, then adjust for market movement using RICS survey data as a benchmark.

2. Time-on-Market Weighting: Properties letting quickly (within days rather than weeks) indicate undersupply and suggest rental values may be understated by historical comparables. The speed of transactions becomes as important as the achieved rent.

3. Tenant Concession Analysis: In tight markets, landlords withdraw previous incentives (reduced deposits, included utilities, rent-free periods). Valuations must account for the removal of these concessions, which effectively increases the net rental value.

4. Yield Compression Recognition: As rental values rise faster than property prices (which face their own headwinds), gross and net yields improve. This affects investment valuations and may justify higher capital values for rental properties with secure tenancies.

For professionals conducting lease extension valuations or shared ownership valuations, understanding these rental market dynamics is essential, as rental value assumptions underpin many leasehold valuation calculations.

Regional Variation in Landlord Instructions and Rent Expectations

While the national picture shows -27% landlord instructions, significant regional variation exists. Urban areas with strong employment markets and limited development capacity typically experience more acute supply shortages. Conversely, regions with weaker economic fundamentals may see less dramatic supply constraints.

RICS regional data (where available) should inform location-specific valuation adjustments. A property in central Manchester or London may warrant more aggressive rental growth assumptions than one in areas with declining population or employment challenges.

Implementing Valuation Adjustments for Landlord Instructions Shortage in 2026

Translating RICS survey insights into practical valuation adjustments requires a systematic approach that balances market evidence with professional judgment. The Valuation Adjustments for Landlord Instructions Shortage: RICS Insights on +20% Rent Rise Expectations in 2026 provide a framework for this process.

Step-by-Step Adjustment Methodology

Step 1: Establish Baseline Comparable Evidence

Begin with traditional comparable analysis, identifying recent lettings of similar properties within the local market. Document achieved rents, lease terms, and transaction dates. For RICS valuations, this forms the foundation of any rental assessment.

Step 2: Apply Time Adjustment Factor

Using RICS survey data as a guide, apply time adjustments to older comparables. If the survey indicates +20% of respondents expect rent rises over three months, this suggests quarterly growth of approximately 0.5-1.0% depending on local market intensity. Adjust historical comparables accordingly:

- Comparables 0-3 months old: Minimal adjustment (0-1%)

- Comparables 3-6 months old: Moderate adjustment (1-2%)

- Comparables 6-12 months old: Significant adjustment (2-4%)

- Comparables >12 months old: Use with caution; adjust 4%+ or seek more recent evidence

Step 3: Factor Supply Constraint Premium

In markets experiencing acute landlord instruction shortages (like the -27% national reading), consider applying a supply constraint premium of 2-5% to reflect reduced tenant negotiating power and increased competition. This adjustment recognizes that current market conditions favor landlords more than historical comparables might suggest.

Step 4: Assess Property-Specific Advantages

Properties with characteristics that appeal to current tenant priorities may command additional premiums:

- Energy efficiency (high EPC ratings) amid rising utility costs

- Home office space reflecting hybrid work patterns

- Outdoor space (gardens, balconies)

- Secure tenancies with responsible landlords (increasingly valued)

Step 5: Document Assumptions and Limitations

Transparency is critical when applying market-condition adjustments. Valuation reports should clearly state:

- The RICS survey data informing the adjustments

- The specific percentage adjustments applied and their rationale

- The limitations of comparable evidence in constrained markets

- The assumptions about future market conditions

This documentation protects both the surveyor and the client, ensuring all parties understand the basis for the valuation in an unusual market environment.

Case Study: Rental Valuation Adjustment Example

Consider a two-bedroom apartment in a Manchester suburb:

Baseline Comparable: Similar property let 6 months ago at £1,200 pcm

Adjustments:

- Time adjustment (6 months @ 1.5% quarterly growth): +£36 pcm (+3%)

- Supply constraint premium (moderate market tightness): +£36 pcm (+3%)

- Property advantage (EPC rating B vs. comparable's C): +£24 pcm (+2%)

Adjusted Rental Value: £1,296 pcm (8% above 6-month-old comparable)

This systematic approach provides defensible justification for the valuation adjustment, grounded in RICS market intelligence and property-specific factors.

Valuation Standards and Professional Obligations

All rental valuations must comply with the RICS Valuation – Global Standards (Red Book), which requires valuers to:

✅ Exercise reasonable care and diligence in gathering market evidence

✅ Provide clear and accurate advice based on appropriate methodology

✅ Disclose any limitations in available comparable evidence

✅ State assumptions explicitly when market conditions are uncertain

✅ Maintain professional independence and objectivity

When conducting RICS help to buy valuations or right to buy valuations, rental value assessments often form part of the overall valuation approach, particularly for investment method calculations. The same rigorous adjustment methodology applies.

Technology and Data Sources for Enhanced Accuracy

Modern valuation practice increasingly incorporates technology to improve accuracy and efficiency:

📊 Rental Index Data: Services like Zoopla, Rightmove, and HomeLet provide rental index data that can corroborate RICS survey trends and inform time adjustments.

🖥️ Automated Valuation Models (AVMs): While not substitutes for professional judgment, AVMs can provide additional data points and identify outliers in comparable analysis.

📱 Real-time Market Intelligence: Digital platforms offer insights into current listing volumes, time-on-market statistics, and tenant inquiry levels that complement RICS survey data.

🗺️ Geographic Information Systems (GIS): Mapping tools help identify micro-market variations and ensure comparables are drawn from genuinely similar locations.

However, technology should augment rather than replace professional expertise. The nuanced interpretation of market conditions—particularly in distorted environments like the current landlord instruction shortage—requires experienced surveyor judgment that algorithms cannot replicate.

The Impact of Renters' Rights Act and Regulatory Changes on Valuations

The regulatory environment significantly influences both landlord behavior (driving the instruction shortage) and future rental value trajectories. Understanding these policy impacts is essential for accurate long-term valuation projections.

Key Provisions of the Renters' Rights Act

The Renters' Rights Act, progressing through Parliament in 2026, introduces several provisions affecting the rental market:

🏠 Abolition of Section 21 "No-Fault" Evictions: Landlords will no longer be able to evict tenants without providing specific grounds, fundamentally changing tenancy security.

📝 Strengthened Section 8 Grounds: While Section 21 disappears, reformed Section 8 grounds aim to provide legitimate routes for landlords to regain possession when necessary.

💷 Rent Increase Limitations: New provisions may restrict the frequency and magnitude of rent increases during tenancies, though market rents for new lettings remain largely unaffected.

🔍 Enhanced Property Standards: Stricter enforcement of property condition standards and faster routes for tenants to address disrepair.

🐕 Pet-Friendly Provisions: Restrictions on landlords' ability to refuse tenants with pets, potentially affecting property wear considerations.

How Regulatory Changes Drive Supply Constraints

The -27% landlord instructions figure directly reflects landlord responses to these regulatory changes [2]. Many smaller landlords—who comprise the majority of the Private Rented Sector—cite increased regulatory burden and reduced flexibility as primary reasons for exiting the market.

This creates a paradox: regulations intended to improve tenant security and housing quality may inadvertently reduce housing supply, driving up rents and making affordability worse. For valuers, this means the supply constraint isn't merely cyclical but potentially structural, justifying sustained rental growth assumptions in valuation models.

Valuation Considerations for Different Property Types

Regulatory impacts vary by property type and landlord category:

Professional/Corporate Landlords: Larger operators with professional management are better positioned to navigate regulatory complexity. Properties in professionally managed portfolios may command premium valuations due to perceived lower risk.

HMOs (Houses in Multiple Occupation): Already heavily regulated, HMO landlords face additional compliance costs but may benefit from supply constraints as smaller landlords exit. HMO valuations require specialist knowledge of licensing requirements and yield expectations.

Student Accommodation: Purpose-built student accommodation (PBSA) operates under different regulatory frameworks and may be less affected by Renters' Rights Act provisions, though traditional student houses face similar pressures to other HMOs.

Build-to-Rent Developments: Institutional build-to-rent schemes may gain competitive advantages as regulatory compliance becomes more complex, potentially supporting higher valuations for professionally managed developments.

When conducting building surveys or homebuyer surveys, understanding these regulatory contexts helps inform advice to clients considering rental investment strategies.

Market Outlook: Rental Growth Trajectories Through 2027

The Valuation Adjustments for Landlord Instructions Shortage: RICS Insights on +20% Rent Rise Expectations in 2026 must be contextualized within broader market forecasts to support long-term valuation assumptions.

Capital Economics Rental Growth Projections

Capital Economics, analyzing the February 2026 RICS survey data, projects:

📈 2026: 2.8% annual rental growth (accelerating from 2.2% in late 2025)

📈 2027: 4.0% annual rental growth (further acceleration) [6]

These projections reflect the view that supply constraints will persist and intensify. The forecast 4.0% growth in 2027 significantly exceeds expected wage growth and inflation, raising affordability concerns but supporting positive valuation adjustments for rental properties.

Comparative Index Data: CBRE and Zoopla Insights

The CBRE rental value index shows a 3% gain measured against the beginning of 2025, corroborating the moderate rental growth momentum captured in RICS surveys [5]. Meanwhile, Zoopla data indicates rent increases on new lets running at just over 2%, considerably below wage growth and representing a sharp moderation from the 12% peak in 2022/early 2023 [5].

This apparent discrepancy between different data sources highlights the importance of understanding what each measures:

- CBRE Index: Tracks rental values across a broad portfolio, including existing tenancies

- Zoopla Data: Focuses on new lettings, capturing current market rates

- RICS Survey: Measures surveyor sentiment and expectations, a forward-looking indicator

For valuation purposes, new letting data (Zoopla) provides the most relevant comparable evidence, while RICS sentiment guides future projections and time adjustments.

Regional Divergence and Local Market Analysis

National statistics mask significant regional variation. London and the Southeast, Manchester, Edinburgh, and other economically strong cities experience more acute supply shortages and stronger rental growth. Conversely, regions with weaker employment markets or population decline may see minimal rental growth despite national trends.

Professional valuers must supplement national RICS data with local market intelligence:

🔍 Local Authority Housing Data: Understanding social housing supply and waiting lists indicates demand pressure

🏗️ Development Pipeline Analysis: New build rental supply can ease constraints in specific localities

💼 Employment Market Trends: Job growth correlates strongly with rental demand and affordability

🚆 Infrastructure Investment: Transport improvements can shift demand patterns between submarkets

For chartered surveyors operating in specific regions, developing deep local market knowledge is essential for accurate valuation adjustments that reflect genuine market conditions rather than national averages.

Risk Factors and Downside Scenarios

While RICS data points toward sustained rental growth, several risk factors could moderate or reverse these trends:

⚠️ Economic Recession: Significant unemployment growth would reduce tenant affordability and demand

⚠️ Mortgage Rate Reductions: Lower rates could shift demand from renting to buying, easing rental pressure

⚠️ Policy Intervention: Government action to increase social housing or incentivize landlord retention

⚠️ Build-to-Rent Acceleration: Rapid expansion of institutional rental supply could ease constraints

Prudent valuation practice considers these scenarios, particularly for longer-term projections. Sensitivity analysis showing valuation outcomes under different rental growth assumptions provides clients with a fuller picture of potential value ranges.

Practical Guidance for Property Professionals and Investors

Understanding the Valuation Adjustments for Landlord Instructions Shortage: RICS Insights on +20% Rent Rise Expectations in 2026 translates into actionable strategies for different market participants.

For Chartered Surveyors and Valuers

📋 Stay Current with RICS Survey Data: Monthly RICS residential surveys provide the most timely market intelligence. Incorporate this data systematically into valuation reports.

📊 Document Adjustment Methodology: Given unusual market conditions, transparent documentation of valuation adjustments protects professional liability and builds client confidence.

🎓 Continuous Professional Development: Attend RICS training on valuation in constrained markets and regulatory impacts on rental values.

🤝 Collaborate with Letting Agents: Local letting agents provide real-time market intelligence that complements RICS national data.

⚖️ Consider Valuation Costs: Ensure fee structures reflect the additional analysis required in complex market environments.

For Landlords and Property Investors

💰 Review Rental Values Regularly: With +20% of surveyors expecting near-term rent rises, existing tenancies may be underrented. Consider professional valuations to inform lease renewal negotiations.

📈 Factor Growth into Investment Decisions: Projected 2.8-4.0% rental growth through 2027 improves investment returns and may justify higher acquisition prices for well-located rental properties.

🏛️ Understand Regulatory Impacts: The Renters' Rights Act affects property management strategies. Professional advice on compliance is essential.

🔧 Invest in Property Quality: High EPC ratings and desirable features command premiums in tight markets. Strategic improvements can deliver strong ROI through higher rents.

📝 Maintain Professional Management: As regulations increase, professional property management becomes more valuable, supporting rental values and reducing void periods.

For Tenants and Prospective Renters

🔍 Expect Continued Rent Increases: RICS data suggests rental growth will persist. Budget accordingly and consider longer-term tenancies to lock in current rates.

⚖️ Understand Your Rights: The Renters' Rights Act strengthens tenant protections. Familiarize yourself with new provisions.

🏠 Prioritize Property Quality: In tight markets, quality properties may offer better value than cheaper alternatives with higher utility costs or maintenance issues.

📍 Consider Alternative Locations: Supply constraints vary by area. Expanding search parameters may reveal better value in adjacent neighborhoods.

For Policymakers and Housing Professionals

🏗️ Address Supply Constraints: The -27% landlord instructions figure indicates policy interventions may be counterproductive. Consider incentives to retain and attract rental supply.

📊 Monitor Market Impacts: Regular review of RICS and other market data helps assess policy effectiveness and identify unintended consequences.

🤝 Balance Regulation and Supply: Tenant protections must be balanced against the need to maintain adequate rental housing supply.

💷 Support Affordability Initiatives: With rents growing faster than wages, targeted support for vulnerable renters becomes increasingly important.

Conclusion

The Valuation Adjustments for Landlord Instructions Shortage: RICS Insights on +20% Rent Rise Expectations in 2026 represent more than technical methodology refinements—they reflect fundamental shifts in the UK rental market that will shape housing affordability and investment returns for years to come. The February 2026 RICS data paints a clear picture: landlord instructions at -27% combined with stable tenant demand at +2% creates supply-demand imbalances that are driving rental growth expectations to their highest levels since the post-pandemic surge [2].

For property professionals, these market conditions demand enhanced valuation methodologies that account for supply constraints, regulatory impacts, and accelerating rental growth projections. The systematic adjustment approach outlined in this article—combining comparable analysis with RICS survey insights, supply constraint premiums, and property-specific factors—provides a defensible framework for accurate rental valuations in this challenging environment.

Looking ahead, Capital Economics' projections of 2.8% rental growth in 2026 accelerating to 4.0% in 2027 suggest the supply shortage will persist rather than resolve quickly [6]. This trajectory has profound implications for housing affordability, investment strategy, and policy development. Whether the market can achieve better balance depends largely on whether regulatory reforms can be refined to protect tenants without further discouraging landlord participation in the Private Rented Sector.

Next Steps for Property Professionals

✅ Review Current Valuation Methodologies: Ensure your approach incorporates RICS survey data and accounts for supply constraint impacts

✅ Enhance Market Intelligence: Develop systematic processes for monitoring RICS monthly surveys, local letting agent feedback, and rental index data

✅ Update Client Communications: Educate clients about market conditions driving rental value changes and the evidence supporting valuation adjustments

✅ Invest in Professional Development: Pursue RICS training on valuation in constrained markets and regulatory impact assessment

✅ Strengthen Documentation: Ensure valuation reports clearly articulate the methodology, assumptions, and limitations when applying market condition adjustments

The rental market of 2026 presents both challenges and opportunities. For valuers registered with the RICS, maintaining professional standards while adapting to unprecedented market conditions requires vigilance, expertise, and commitment to evidence-based practice. By incorporating the insights from RICS surveys and applying rigorous adjustment methodologies, property professionals can deliver accurate valuations that serve clients effectively while upholding the highest standards of the profession.

References

[1] Uk Rics Residential Market Survey Mar 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-mar-2026

[2] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] Uk Residential Survey Dec 2025 Confidence Rebound – https://www.rics.org/news-insights/uk-residential-survey-dec-2025-confidence-rebound

[5] Uk Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[6] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[7] Valuation Strategies Amid January 2026 Rics Residential Survey Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals