Flood damage costs the UK economy an estimated £2.2 billion every year — and that figure is set to climb sharply as climate change accelerates [1]. The 2026 spring floods, which inundated stretches of the South West and East Coast with historic intensity, have forced a reckoning across the property industry. For surveyors, lenders, and buyers alike, understanding Valuation Adjustments for Flood Risk in Coastal Properties: RICS Guidance Post-2026 Spring Floods is no longer optional — it is a professional and commercial necessity.

This article breaks down the latest RICS guidance, explains how flood resilience data is reshaping coastal property valuations, and provides practical steps for surveyors working in high-risk zones.

Key Takeaways 📌

- Flood risk must be formally assessed across five flooding types in every coastal property valuation, per the RICS October 2025 practice paper.

- Value reductions vary widely — from marginal to significant — depending on flood zone designation, construction type, and installed defences.

- Post-flood price recovery typically takes up to three years, but repeat flooding events can permanently suppress values.

- Environment Agency data and BS 85500:2025 are now core reference tools for surveyors preparing flood-adjusted valuations.

- Flood Re has improved insurance accessibility, but surveyors must still document insurability status as part of due diligence.

Understanding the RICS Framework: What the 2025 Guidance Paper Changes

The landmark RICS practice paper published in October 2025 — Flooding and Its Implications for Property Professionals — represents the most comprehensive update to flood-related surveying guidance in over a decade [1]. Authored by Charles Cowap of Harper Adams University with cross-profession expert input, it establishes a clear framework that surveyors must now apply when assessing coastal and flood-prone properties [6].

The Five Flood Types Surveyors Must Assess

The guidance is explicit: not all flooding is the same, and a one-size-fits-all approach to risk assessment is professionally inadequate [2]. Surveyors must consider:

- 🌊 Fluvial flooding — rivers and watercourses overtopping banks

- 🌊 Coastal flooding — tidal surges and sea-level rise

- 🌧️ Surface water flooding — overwhelmed drainage systems during heavy rainfall

- 💧 Groundwater flooding — rising water tables, particularly in chalk and limestone areas

- 🏗️ Infrastructure-related flooding — burst mains, sewer overflow, or failed drainage

For coastal properties specifically, the combination of fluvial and coastal flooding creates compounding risk scenarios that require layered assessment rather than single-source data checks.

Seven Professional Responsibilities

The RICS paper also defines seven key areas of professional responsibility for surveyors [2]:

| Responsibility | Description |

|---|---|

| Flood risk assessments | Identify and classify risk level |

| Drainage & adaptation advice | Assess SuDS and resilience measures |

| Valuation implications | Apply evidence-based adjustments |

| Insurance support | Document Flood Re eligibility and cover |

| Recovery assistance | Post-flood reinstatement guidance |

| Cross-profession collaboration | Work with planners, engineers, insurers |

| Occupier guidance | Advise on flood preparedness |

💬 "Flooding is designated as one of the most severe climate hazards in the UK Climate Change Risk Assessment — surveyors who treat it as a footnote in a valuation report are exposed to significant professional liability." — RICS Insight Paper, October 2025 [6]

Valuation Adjustments for Flood Risk in Coastal Properties: RICS Guidance Post-2026 Spring Floods in Practice

The 2026 spring flooding events have provided a live stress test of how well the profession was applying the October 2025 guidance. The results were mixed — but they also clarified exactly where adjustments must be made and why.

How Surveyors Incorporate Flood Resilience Reports

The core shift in post-2026 practice is the integration of flood resilience reports directly into the Red Book valuation process. Rather than treating flood risk as a caveat or footnote, RICS-registered valuers are now expected to:

- Cross-reference Environment Agency (EA) flood zone maps (Zones 1, 2, and 3) as a baseline

- Review any Strategic Flood Risk Assessment (SFRA) produced by the local planning authority

- Inspect physical flood resilience measures on site, including flood doors, air brick covers, non-return valves, and tanking

- Assess compliance with BS 85500:2025, the updated standard for flood resilient and resistant construction [2]

- Document Sustainable Drainage Systems (SuDS) where present, as these can materially reduce surface water risk

For a RICS Red Book valuation, the surveyor must now clearly state the flood zone designation, identify any defence infrastructure, and apply a reasoned adjustment to the Market Value figure.

Quantifying the Value Adjustment

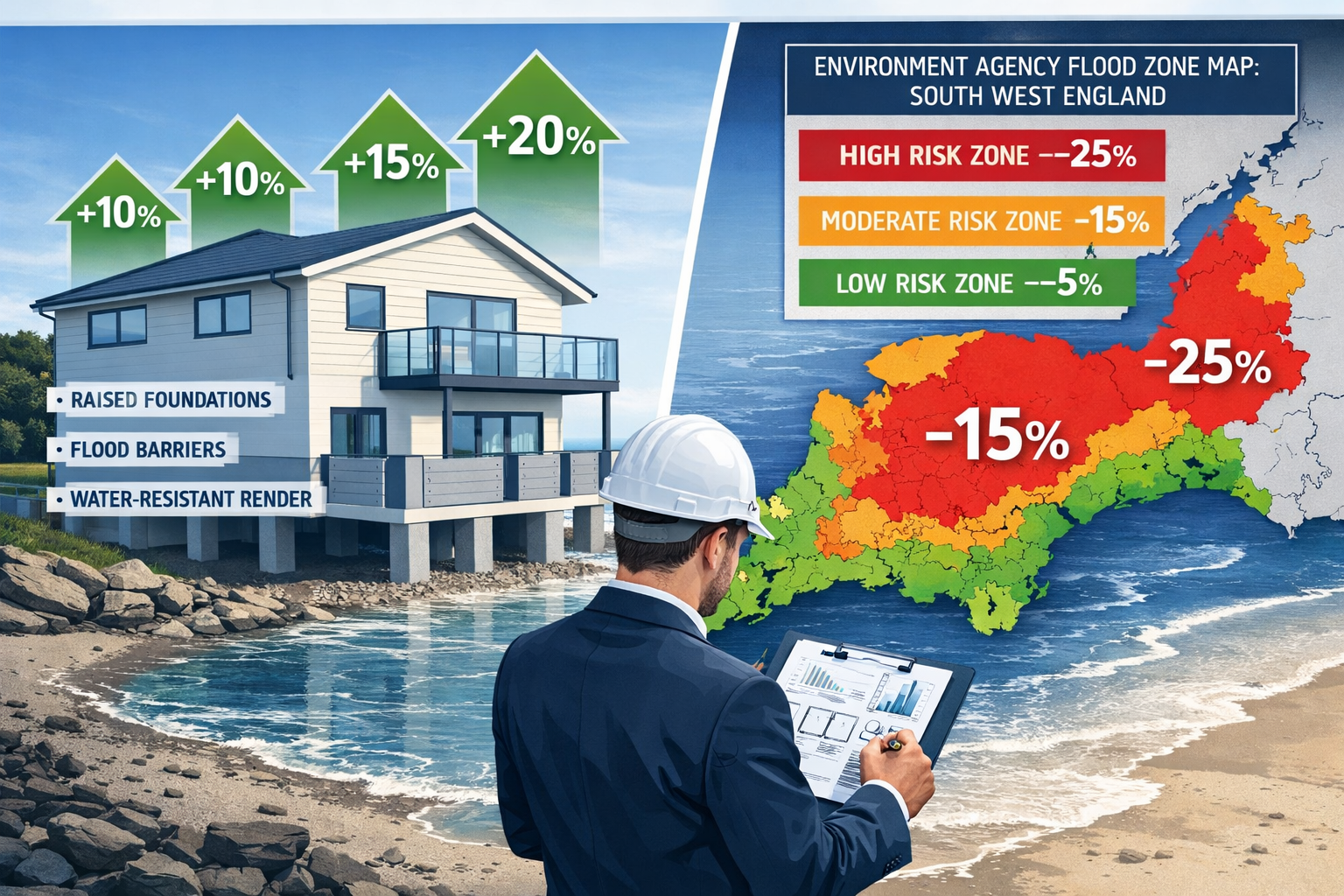

Research cited by RICS indicates that property value reductions range from small to significant depending on multiple variables [3]. The table below summarises the key factors and their typical directional impact:

| Factor | Impact on Value |

|---|---|

| EA Flood Zone 3 (high risk) designation | Moderate to significant reduction |

| History of actual flooding | Significant reduction |

| No flood defences installed | Greater reduction |

| Flood Re-eligible insurance available | Partial mitigation |

| Certified flood resilience measures (BS 85500:2025) | Reduction offset |

| Strong local defence infrastructure | Partial to full mitigation |

| Repeat flooding events | Compounding reduction |

The critical principle: adjustments must be evidence-based and individually reasoned, not applied as a blanket percentage. A coastal property in Cornwall with a recently upgraded sea wall and flood-resilient construction will warrant a very different adjustment to an undefended East Anglian property in a Zone 3 designation.

For surveyors also preparing reinstatement cost assessments, flood risk adds a further layer — reinstatement costs for flood-damaged coastal properties can significantly exceed standard build cost benchmarks due to specialist drying, decontamination, and flood-resilient rebuilding requirements.

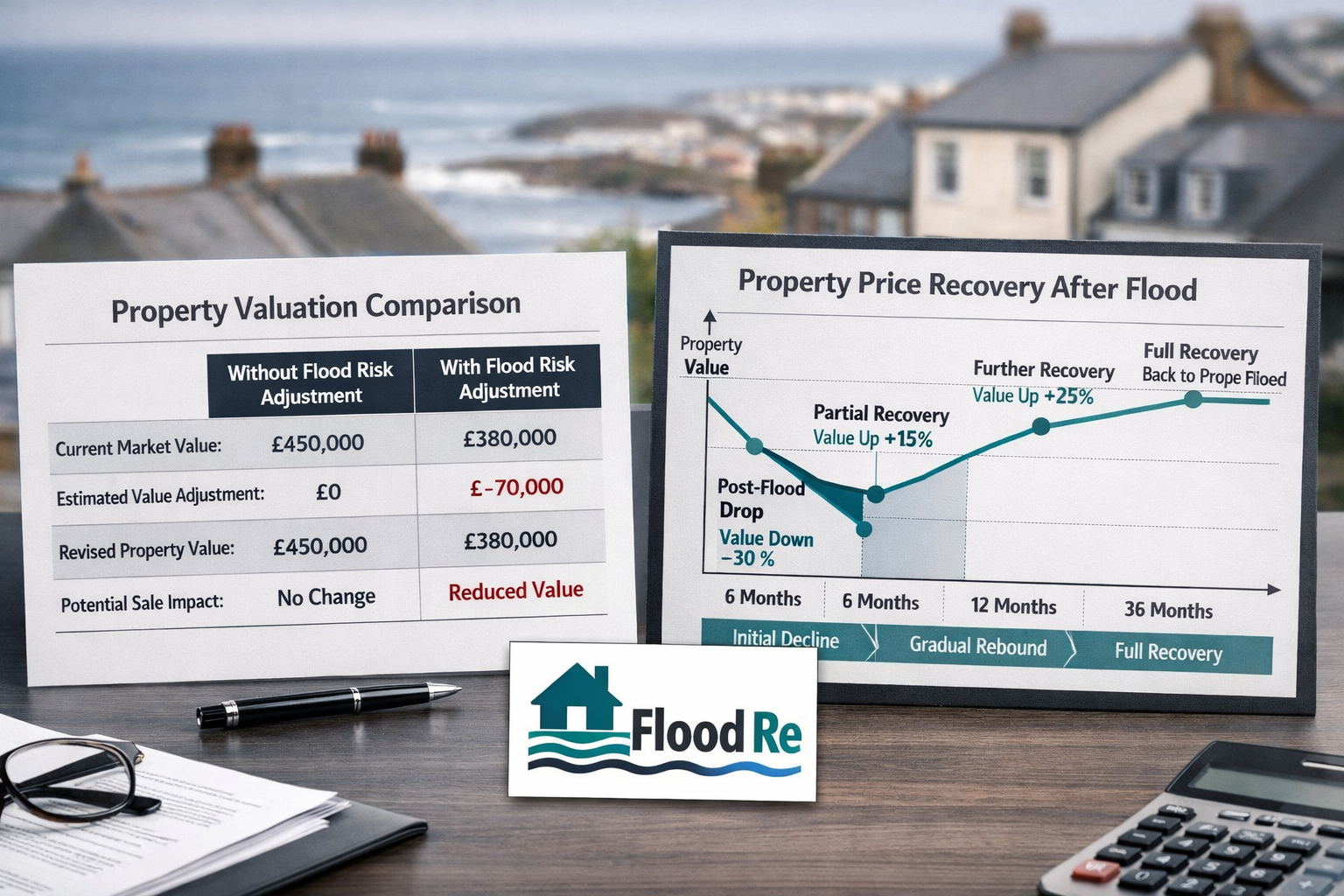

The Three-Year Recovery Window

One of the most practically important findings in the RICS research is the post-flood price recovery timeline [5]. Evidence suggests:

- ✅ Property values in flooded areas typically return to normal market levels within three years

- ⚠️ This recovery is not guaranteed where flood risk designation has been upgraded

- ❌ Properties that flood repeatedly show permanent value suppression rather than recovery

This has direct implications for valuations carried out in 2026 in areas affected by the spring floods. Surveyors must distinguish between:

- Temporary event-driven depression — where the market is expected to recover

- Structural risk repricing — where the flood event has triggered a permanent reassessment of the area's risk profile

Applying the Guidance: South West and East Coast Case Considerations

The 2026 spring floods were particularly severe across Devon, Cornwall, Somerset, Norfolk, and Lincolnshire — regions where coastal flood risk intersects with high concentrations of older housing stock, holiday lets, and second homes.

South West England

Properties in the South West face a dual challenge: coastal erosion risk compounds flood risk, meaning that some properties face not just inundation but eventual loss of the land itself. Surveyors operating in this region must:

- Reference the Shoreline Management Plans (SMPs) published by coastal groups, which classify coastlines as hold-the-line, managed retreat, or no active intervention

- Consider long-term insurability — properties on no-active-intervention coastlines may become uninsurable within a mortgage term

- Apply additional deductions where EA data shows accelerating coastal erosion alongside flood risk

For those working on commercial property valuations in coastal tourism hotspots, the disruption caused by the 2026 floods — including road closures, business interruption, and infrastructure damage — must also be factored into income-based valuation approaches.

East Coast Properties

The East Coast presents a different profile: flat, low-lying land with significant tidal surge exposure. Post-2026, surveyors in Essex, Norfolk, and Lincolnshire are seeing:

- Increased mortgage lender scrutiny, with some lenders requiring independent flood risk assessments before approving lending

- Greater buyer awareness and longer transaction times as due diligence deepens

- A growing market for flood resilience upgrades as sellers seek to protect or recover value

A thorough RICS building survey (Level 3) is increasingly the minimum standard expected by buyers and lenders in these areas — a HomeBuyer Report is often insufficient to capture the full scope of flood-related defects and risks.

💬 "Without adaptation measures, the number of high-risk flood properties in the UK could double by 2050 — making today's valuations a critical baseline for long-term asset risk management." [1]

Valuation Adjustments for Flood Risk in Coastal Properties: RICS Guidance Post-2026 Spring Floods and Insurance Considerations

The Role of Flood Re

The Flood Re scheme — a reinsurance arrangement between the government and insurers — has significantly improved the affordability of flood cover for eligible residential properties [3]. Key points for surveyors:

- Flood Re covers household policies only — buy-to-let and commercial properties are excluded

- Properties built after 1 January 2009 are not eligible for Flood Re

- Surveyors should document Flood Re eligibility in valuation reports as it directly affects mortgageability and saleability

Where a property is not Flood Re eligible and sits in a high-risk zone, the surveyor must flag the potential for unaffordable or unavailable insurance — a factor that can materially affect market value and lender appetite.

Documenting Insurability in Valuation Reports

Post-2026, RICS guidance expects surveyors to treat insurance status as a material valuation factor, not a separate matter for solicitors. The valuation report should address:

- Whether standard buildings insurance is available at reasonable cost

- Whether Flood Re applies

- Any exclusions or excesses that would leave the owner exposed

- The impact of insurance status on comparable evidence used in the valuation

For properties subject to lease extension valuations or shared ownership schemes, flood risk and insurance costs can also affect the affordability calculations that underpin those specialist assessments.

Practical Steps for Surveyors: A Post-2026 Checklist

The following checklist consolidates the RICS guidance into actionable steps for surveyors preparing flood-adjusted valuations of coastal properties in 2026:

Pre-Inspection

- Check EA Flood Map for Planning — confirm Zone 1, 2, or 3 designation

- Review local SFRA and any site-specific flood risk assessment

- Check planning history for any flood risk conditions attached to consent

- Verify Flood Re eligibility based on construction date and property type

- Review Shoreline Management Plan classification for coastal sites

On-Site Inspection

- Identify and record all flood resilience and resistance measures

- Check for evidence of previous flooding (tide marks, replaced finishes, salt damage)

- Assess drainage condition — gutters, downpipes, gullies, and SuDS features

- Note proximity to sea defences, flood walls, or embankments

- Consider commissioning a specialist drainage survey where drainage condition is uncertain

Valuation Report

- State flood zone designation explicitly

- Apply and justify any value adjustment with reference to comparable evidence

- Document insurance status and Flood Re eligibility

- Note any BS 85500:2025 compliance measures that offset risk

- Flag long-term risk factors including projected sea-level rise and erosion

Conclusion: Actionable Next Steps for Surveyors and Property Owners

The 2026 spring floods have accelerated a shift that was already underway. Valuation Adjustments for Flood Risk in Coastal Properties: RICS Guidance Post-2026 Spring Floods is not a theoretical exercise — it is a live professional obligation with real consequences for clients, lenders, and the surveyors who advise them.

The RICS October 2025 practice paper provides a robust framework, but applying it effectively requires surveyors to move beyond checkbox compliance and develop genuine expertise in flood risk assessment, resilience measures, and insurance markets [6][7].

For surveyors, the immediate priorities are:

- Upskill on Environment Agency data tools and flood resilience construction standards

- Update report templates to include mandatory flood risk sections aligned with RICS guidance

- Build relationships with specialist flood risk consultants for complex coastal cases

For property owners and buyers in coastal areas:

- Commission a Level 3 building survey before purchase — not a basic mortgage valuation

- Invest in certified flood resilience measures — these demonstrably protect and recover value

- Check Flood Re eligibility early in any transaction to avoid late-stage surprises

For lenders and investors, the data is clear: properties with documented flood resilience measures, strong local defences, and Flood Re-eligible insurance represent materially lower risk than undefended equivalents in the same flood zone.

The property market will continue to price flood risk more accurately over time. Surveyors who lead that process — rather than follow it — will provide the greatest value to their clients and the profession.

📞 Need expert flood-risk valuation advice for a coastal property? Contact a chartered surveyor to discuss your specific requirements.

References

[1] Rics Releases New Insight Paper Flooding Property – https://www.rics.org/news-insights/rics-releases-new-insight-paper-flooding-property

[2] Rics Releases New Insight Paper On Flooding And Property – https://propertyindustryeye.com/rics-releases-new-insight-paper-on-flooding-and-property/

[3] Flooding – https://www.rics.org/consumer-guides/flooding

[4] Rics Relaunches Updated Consumer Flooding Guide Amid Climate Cha – https://www.rics.org/news-insights/rics-relaunches-updated-consumer-flooding-guide-amid-climate-cha

[5] Flood Risk – https://www.isurv.com/downloads/1073/flood_risk

[6] Flooding And Its Implications For Property Professionals October 2025 – https://www.rics.org/content/dam/ricsglobal/documents/research/Flooding-and-its-implications-for-property-professionals-October-2025.pdf

[7] Flooding And Its Implications For Property Professionals – https://www.rics.org/news-insights/research-and-insights/flooding-and-its-implications-for-property-professionals

[8] Rics Releases Information Paper On Flooding And Property – https://theintermediary.co.uk/2025/10/rics-releases-information-paper-on-flooding-and-property/