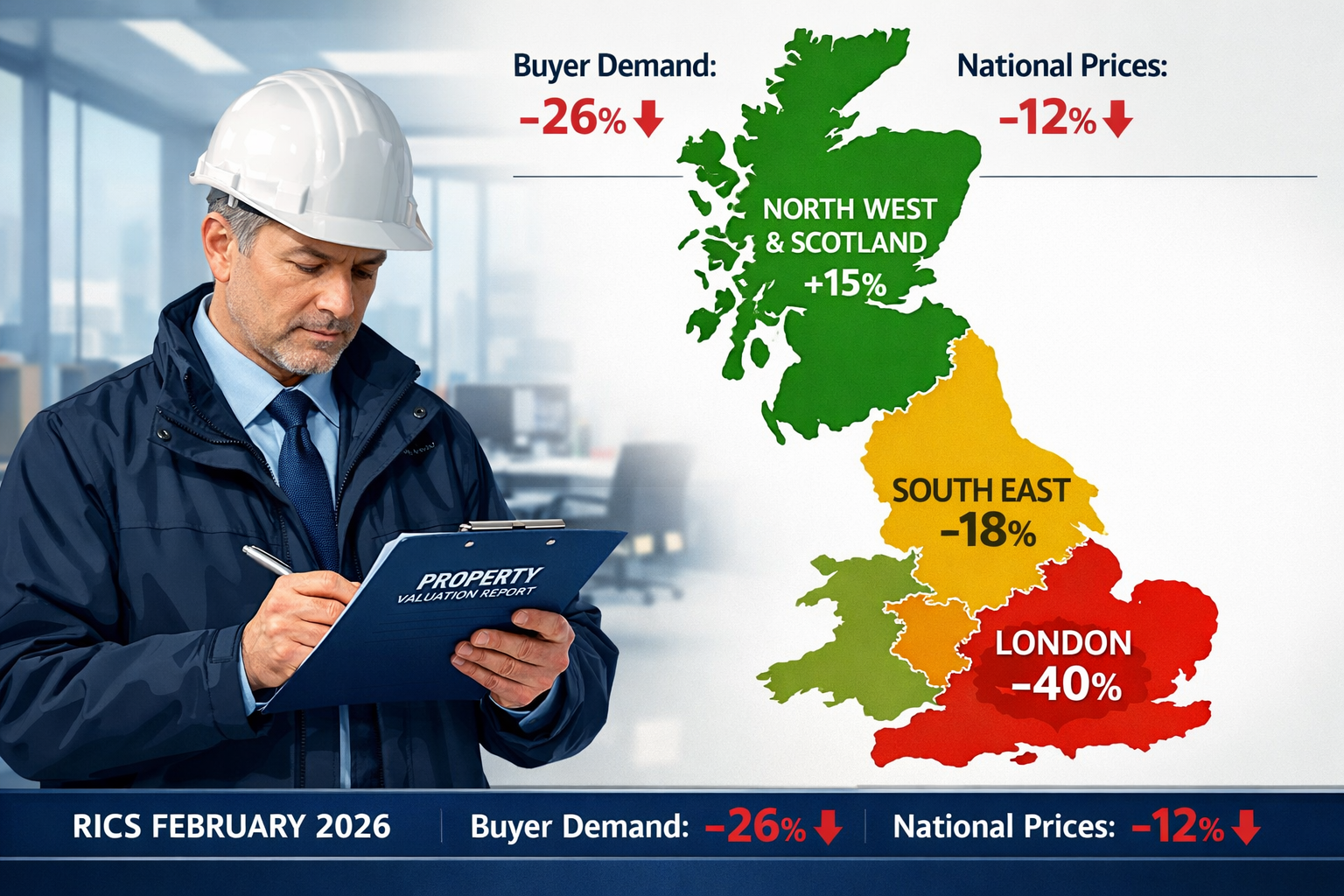

London's 12-month price expectations collapsed from +56% in January to just +7% in February 2026 — a seismic shift in surveyor sentiment that demands immediate attention from every valuation professional operating in the capital. Meanwhile, the North West, Scotland, and Northern Ireland continue to report rising prices, creating one of the starkest regional divergences the UK residential market has seen in recent years. For building surveyors navigating these contrasting conditions, understanding the Valuation Adjustments for Flat London Prices vs Northern Recovery: RICS February 2026 Survey Insights for Building Surveyors is no longer optional — it is a professional necessity. [1]

Key Takeaways 📌

- London prices face severe downward pressure with a net balance of -40%, while Northern regions and Scotland report rising values — creating a two-speed market.

- Buyer demand nationally fell sharply to -26% in February 2026, driven by interest rate uncertainty and macroeconomic headwinds.

- Near-term price expectations deteriorated to -18%, but 12-month national sentiment remains at +33%, signalling medium-term resilience.

- Building surveyors must apply region-specific valuation adjustments to reflect this divergence accurately in Red Book and comparable evidence appraisals.

- The lettings market faces a structural supply crisis, with landlord instructions at -27%, reinforcing the investment case for Northern residential stock.

Understanding the RICS February 2026 Residential Survey: The National Picture

The RICS UK Residential Survey for February 2026 paints a sobering picture of the national housing market. The headline house price net balance fell to -12%, indicating that more surveyors reported falling prices than rising ones across the country. [1] This stagnation follows a period of cautious optimism seen in January, where early signs of recovery had begun to emerge. [2]

Buyer demand deteriorated sharply. The net balance of new buyer enquiries dropped to -26% in February, down from -15% in January — a significant deterioration driven largely by renewed concerns over interest rate trajectories and broader macroeconomic uncertainty. [1] Agreed sales also remained subdued, recording a net balance of -12%, while near-term sales expectations softened to -2%. [1]

💬 "The February data represents a meaningful step backwards from the cautious optimism of January. Surveyors are pricing in a more prolonged period of adjustment." — Interpretation of RICS February 2026 findings [1]

Despite the near-term gloom, longer-term sentiment provides some counterbalance. +17% of respondents expect sales activity to rise over the next 12 months, and the 12-month price expectation net balance, while moderated to +33% from +43% in January, remains firmly positive. [1] For building surveyors, this divergence between near-term caution and medium-term optimism is critical context for any valuation instruction received in spring 2026.

New instructions remained broadly stable at +2%, suggesting the pipeline of fresh listings is neither expanding nor contracting materially — a market in a holding pattern rather than freefall. [1]

Regional Divergence: London's Decline vs Northern Resilience

The most compelling story within the Valuation Adjustments for Flat London Prices vs Northern Recovery: RICS February 2026 Survey Insights for Building Surveyors data is the sheer scale of regional divergence. Understanding this split is essential for any RICS-registered professional producing Red Book valuations or advising clients on pricing strategy.

London: A Market Under Significant Pressure

London recorded a net balance of -40% for house prices in February 2026 — the weakest reading of any region surveyed. [1] This is not a mild softening; it represents a broad-based consensus among London surveyors that prices are falling. The capital's 12-month outlook collapsed dramatically, dropping from +56% in January to just +7% in February — a 49-percentage-point swing in a single month. [1]

Several factors compound this pressure in London specifically:

- 🏙️ Stamp duty changes affecting higher-value transactions disproportionately

- 📉 Affordability constraints at the upper end of the market

- 🏢 Flat and leasehold sector weakness, particularly in the wake of ongoing building safety legislation

- 💷 Interest rate sensitivity on large loan-to-value mortgages typical in the capital

For surveyors working across central London, north London, and west London, this data demands a reassessment of comparable evidence. Transactions completed in Q4 2025 may no longer represent reliable benchmarks for current market value, particularly in the flat and leasehold sector.

South East and East Anglia: Following London's Lead

The weakness is not confined to the M25. The South East recorded a net balance of -24% and East Anglia -26%, both substantially below the national average. [1] These regions have historically tracked London sentiment with a lag, and February 2026 data confirms that pattern is holding. Surveyors operating in commuter belt locations — including areas such as Oxfordshire and Berkshire — should treat comparable evidence from 2025 with particular scrutiny.

Northern Regions: A Genuine Recovery Story

In stark contrast, Scotland, Northern Ireland, and the North West of England all reported rising prices in February 2026. [1] This is not a statistical anomaly — it reflects fundamental differences in affordability, demand-supply dynamics, and the profile of buyers active in these markets.

| Region | Price Net Balance (Feb 2026) | 12-Month Outlook |

|---|---|---|

| London | -40% | +7% |

| South East | -24% | Moderated |

| East Anglia | -26% | Moderated |

| North West | Positive ✅ | Positive ✅ |

| Scotland | Positive ✅ | Positive ✅ |

| Northern Ireland | Positive ✅ | Positive ✅ |

| National | -12% | +33% |

Source: RICS UK Residential Survey February 2026 [1]

For surveyors providing RICS Red Book valuations in Manchester and across the North West, this data supports a more confident approach to current market value assessments — provided comparable evidence is drawn from genuinely comparable transactions within the same regional market.

Practical Valuation Adjustments for Building Surveyors in 2026

The Valuation Adjustments for Flat London Prices vs Northern Recovery: RICS February 2026 Survey Insights for Building Surveyors data creates specific, actionable obligations for RICS professionals. Here is how to translate the survey findings into sound valuation practice.

1. Revisiting Comparable Evidence in Declining Markets

In markets where the net balance is deeply negative — particularly London at -40% — surveyors must apply time adjustments to comparable sales evidence. A transaction completed in mid-2025 in a London postcode may overstate current market value by a material margin. Best practice in 2026 requires:

- ✅ Prioritising comparables from Q4 2025 onwards where available

- ✅ Applying a documented downward time adjustment where older comparables are used

- ✅ Noting market conditions explicitly within the valuation report

- ✅ Seeking corroboration from active listing data and agreed (not just completed) sales

For leasehold flats in particular — already subject to valuation complexity around service charges, cladding, and EWS1 requirements — the additional market headwind of -40% sentiment requires careful narrative within any RICS building survey or formal valuation report.

2. Upward Adjustments in Northern Recovery Markets

The mirror challenge applies in the North West, Scotland, and Northern Ireland. Where prices are rising, surveyors risk undervaluing properties if they rely too heavily on older comparables that pre-date the recovery. Key considerations include:

- 📈 Identifying whether a property sits within a genuinely recovering micro-market

- 📈 Noting the direction of travel in the valuation narrative

- 📈 Avoiding over-reliance on distressed or unusual sales that may skew comparables downward

Surveyors conducting property inspections in Manchester should be particularly attentive to the pace of change in specific sub-markets, where demand from investors and owner-occupiers is outpacing supply in certain property types.

3. The Flat and Leasehold Sector: A Special Case

The weakness in London is disproportionately concentrated in the flat and leasehold sector. Building safety legislation, EWS1 certification requirements, and rising service charges have created a structural discount for many leasehold properties in the capital. Surveyors should:

- Document any building safety-related factors explicitly

- Consider whether a specific defect survey is warranted where cladding or structural concerns are present

- Ensure reinstatement cost assessments reflect current build cost inflation, which remains elevated despite market softening

4. Near-Term vs Medium-Term Valuation Basis

The divergence between near-term expectations (-18%) and 12-month expectations (+33%) nationally [1] creates a specific challenge for valuations prepared for different purposes:

| Valuation Purpose | Key Consideration |

|---|---|

| Mortgage security (current) | Apply near-term caution; note market conditions |

| Capital gains tax | Use date-specific evidence; document market context |

| Probate / matrimonial | Clearly state the valuation date and prevailing conditions |

| Shared ownership | Apply regional adjustment; note recovery or decline trajectory |

| Help to Buy redemption | London properties may require downward adjustment from earlier estimates |

For capital gains tax valuations and shared ownership valuations, the date of valuation is paramount — and the February 2026 data makes clear that even a one-month shift can materially alter market context.

The Lettings Market: A Structural Supply Crisis

The lettings market data from February 2026 deserves separate attention. Tenant demand was broadly stable at +2%, but landlord instructions remained firmly negative at -27%. [1] This persistent imbalance between supply and demand has significant implications for:

- Rental yield calculations in investment valuations — yields are being supported by rental growth even as capital values soften in London

- Buy-to-let portfolio appraisals — particularly in Northern markets where both capital growth and rental demand are positive

- Dilapidations assessments — as landlord exit from the sector continues, dilapidation surveys on vacated properties are likely to increase

The structural supply shortage in the rental sector reinforces the investment case for Northern residential property, where yields are more attractive and capital growth prospects are stronger than in the South East. [1] [5]

What This Means for Building Surveyors in Spring 2026

The February 2026 RICS data arrives at a critical juncture. The stamp duty threshold changes that came into effect in April 2025 continue to reverberate through transaction volumes, and interest rate uncertainty is suppressing buyer confidence nationally. [1] [6]

For building surveyors, the professional obligations are clear:

- Maintain regional granularity — national averages mask the true picture. A -12% national balance obscures a -40% London reading and a positive North West reading.

- Document market conditions thoroughly — RICS Red Book requirements demand that valuers explain the market context in which a valuation is prepared. February 2026 conditions are materially different from January.

- Revisit comparable selection criteria — the speed of sentiment change (London 12-month outlook: +56% to +7% in one month) means that comparable hierarchies need active review.

- Communicate uncertainty appropriately — where market conditions are volatile, the use of Special Assumptions or explicit caveats within reports is both professionally appropriate and client-protective.

- Stay current with RICS guidance — the February 2026 survey [4] should be read alongside the January 2026 report [2] to understand the direction and velocity of change, not just the point-in-time reading.

Conclusion: Acting on the Data in a Divergent Market

The Valuation Adjustments for Flat London Prices vs Northern Recovery: RICS February 2026 Survey Insights for Building Surveyors represent more than a set of statistics — they are a professional roadmap for navigating one of the most regionally divergent UK housing markets in recent memory.

Actionable next steps for building surveyors in 2026:

- 🗺️ Map your instruction pipeline by region and apply the appropriate sentiment context to each valuation

- 📋 Update your comparable evidence protocols to weight recent transactions more heavily in volatile markets

- 🏢 Flag London flat and leasehold instructions for enhanced scrutiny, particularly where building safety issues may compound market weakness

- 📈 Recognise Northern recovery as a genuine trend, not a statistical outlier, and reflect this in valuation narratives for North West, Scottish, and Northern Irish properties

- 📚 Read the full RICS February 2026 survey PDF [4] and cross-reference with Capital Economics commentary [6] for a rounded macroeconomic view

- 🤝 Communicate proactively with clients about the implications of a -26% buyer demand reading for transaction timelines and achievable prices

The data is clear. The professional response must be equally clear: regional divergence demands regional precision. Building surveyors who apply a national brush to a market this fragmented risk producing valuations that fail both their clients and the standards of their profession.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[3] Property Market Turning Corner RICS Survey Suggests – https://todaysconveyancer.co.uk/property-market-turning-corner-rics-survey-suggests/

[4] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[5] Valuation Adjustments Post RICS February 2026 Residential Survey Strategies For Flat Prices And Stable Lettings Demand – https://nottinghillsurveyors.com/blog/valuation-adjustments-post-rics-february-2026-residential-survey-strategies-for-flat-prices-and-stable-lettings-demand

[6] UK RICS Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026