Fewer than six months after its May 1, 2026 implementation date, the Renters' Rights Act 2026 has already forced a fundamental rethink of how residential investment property is assessed, priced, and financed across England. Research by Handelsbanken found that professional landlords face average compliance costs of £31,411 under the new rules [2] — a figure that, when capitalised into rental yields, can meaningfully reduce open-market values. For valuers, mortgage lenders, and investors, understanding the Renters' Rights Act 2026 implications for property valuation: assessing landlord compliance costs and market impact is no longer optional; it is a core professional competency.

Key Takeaways

- The abolition of Section 21 'no-fault' evictions from May 1, 2026 reduces landlord flexibility and increases void period risk, both of which depress investment value.

- Average compliance costs of £31,411 per landlord must be factored into valuation models alongside higher legal cost provisions and extended void period assumptions.

- All assured shorthold tenancies have converted to periodic tenancies, removing fixed-term income certainty and requiring revised yield calculations.

- A quality divide is emerging: well-maintained, energy-efficient properties are holding or gaining value, while lower-grade stock faces declining yields and tighter lending conditions.

- Surveyors are revising Red Book methodologies to reflect new risk profiles, making professional RICS valuations more critical than ever for landlords, lenders, and investors.

The Legislative Framework: What Changed on May 1, 2026

The Renters' Rights Act 2026 represents the most significant overhaul of the private rented sector in England since the Housing Act 1988. Its provisions affect every stage of the landlord-tenant relationship, from marketing a property to recovering possession.

Abolition of Section 21 'No-Fault' Evictions

Effective May 1, 2026, landlords can no longer serve a Section 21 notice to recover possession without stating a legal reason. All possession claims must now proceed under Section 8 of the Housing Act 1988, using one of the prescribed grounds [1]. This change has two direct valuation consequences:

- Reduced liquidity: A landlord wishing to sell with vacant possession must now navigate a court-based process, potentially extending the time to achieve a clean sale.

- Increased void period risk: If a Section 8 claim is contested, the property may generate no income for months, a risk that valuers must price into yield assumptions.

The Law Society has called for significant additional investment in the court system to handle the anticipated surge in contested possession cases [7]. Until that capacity is in place, timelines for possession remain uncertain — and uncertainty is a discount factor in any valuation.

Transition to Periodic Tenancies

All existing assured shorthold tenancies automatically converted to assured periodic tenancies on May 1, 2026 [1]. Fixed-term agreements no longer exist for new lettings. For landlords, this means:

- Tenants can give two months' notice to leave at any point, creating unpredictable income streams.

- Landlords lose the ability to plan around fixed end dates when refinancing, selling, or undertaking planned maintenance.

- Rent review mechanisms must comply with the Act's prescribed process, removing the ability to use rent increases as an indirect tool for managing tenancies.

Understanding how these changes interact with factors of valuation is essential for any surveyor preparing a residential investment report in 2026.

The Decent Homes Standard and Pet Provisions

The Act introduces a statutory Decent Homes Standard for the private rented sector, requiring landlords to address hazardous conditions promptly [6]. Properties that fall below this standard face enforcement action from local authorities, which now have access to an additional £41 million in government funding and can impose fines of up to £40,000 on non-compliant landlords [5].

Additional provisions include:

- A ban on discriminating against benefit-receiving tenants or those with children [6].

- A requirement that landlords cannot unreasonably refuse requests to keep pets [6].

Both provisions may increase wear-and-tear assumptions in valuation models and affect insurance reinstatement calculations. Landlords should review their insurance reinstatement valuation to ensure coverage reflects the updated risk profile of their portfolio.

Quantifying Compliance Costs: What Landlords Are Actually Spending

The Renters' Rights Act 2026 implications for property valuation: assessing landlord compliance costs and market impact cannot be understood without a clear picture of what compliance actually costs. The Handelsbanken survey data points to an average of £31,411 per professional landlord [2], but the composition of that figure matters as much as the headline number.

Breakdown of Typical Compliance Expenditure

| Cost Category | Estimated Range | Notes |

|---|---|---|

| Legal fees (tenancy restructuring) | £1,500 – £4,000 | Converting ASTs, updating agreements |

| Property upgrades (Decent Homes Standard) | £5,000 – £20,000+ | EPC improvements, hazard remediation |

| Administrative systems | £500 – £2,000 | New tenancy management software |

| Increased insurance premiums | £300 – £1,200 per property | Pet damage, extended void cover |

| Legal costs for Section 8 possession | £3,000 – £8,000 per case | Court fees, solicitor costs |

| Void period losses (extended timelines) | Variable | Potentially 3-6 months' rent |

The critical point for valuers: these are not one-off costs for most landlords. Section 8 legal costs recur with every contested possession. Void period losses recur with every tenancy change. When annualised and deducted from gross rental income, they produce a materially lower net operating income — and a lower capital value.

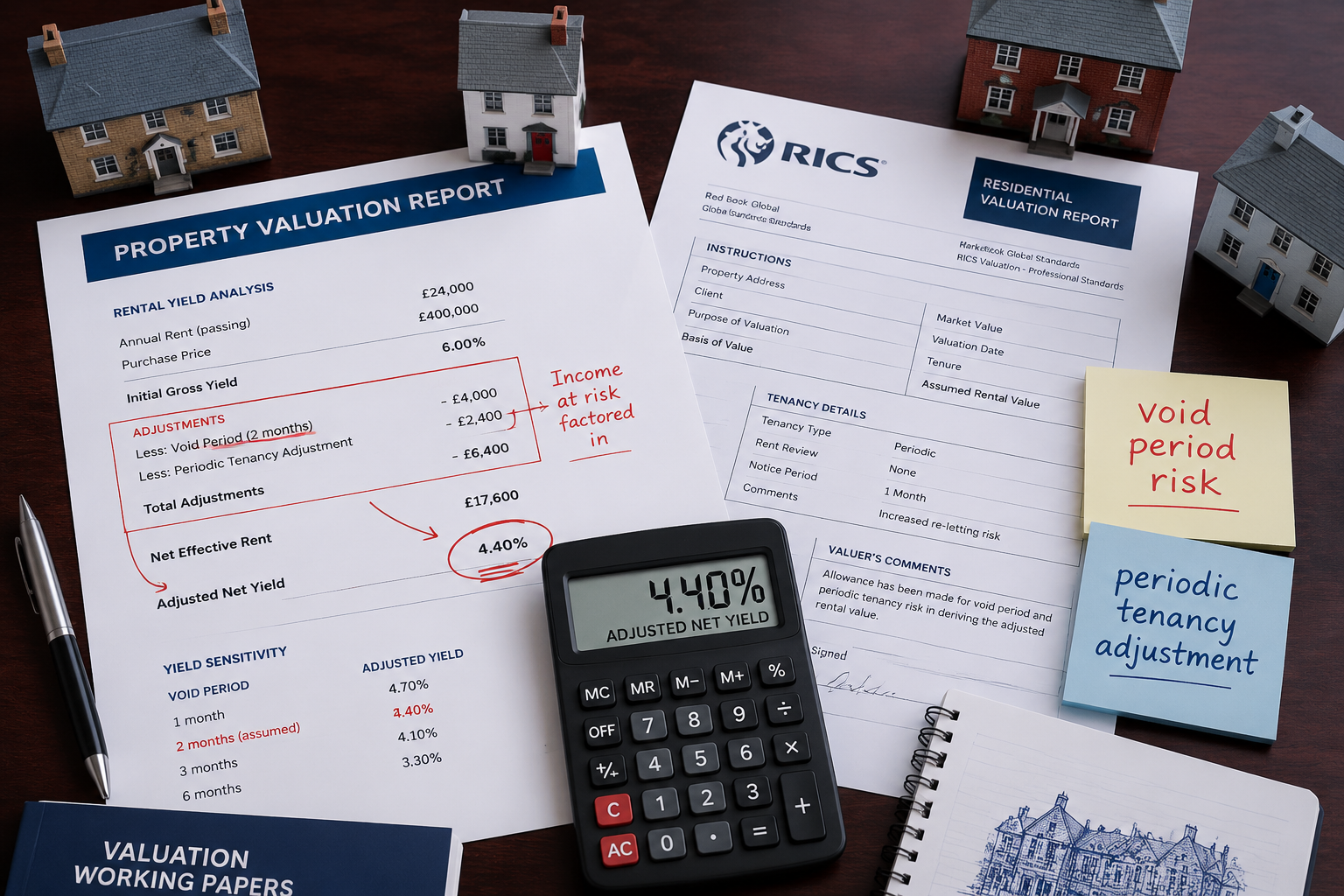

How Compliance Costs Feed Into Yield Calculations

A simplified example illustrates the mechanism:

- Gross annual rent: £18,000

- Pre-Act net operating income (after standard voids and management): £15,300

- Post-Act deductions (additional void risk, legal provisions, compliance costs amortised): £3,800

- Post-Act net operating income: £11,500

- At a 5% yield: capital value falls from £306,000 to £230,000

This is a stylised illustration, but it reflects the directional logic that RICS-registered valuers are now applying [3]. The valuation red book framework requires valuers to reflect market evidence, and as comparable sales begin to embed Act-related discounts, those discounts become self-reinforcing in the evidence base.

Rent Reviews Under the New Framework

The Act restricts how and when landlords can increase rents, removing the previous mechanism of serving a Section 13 notice and replacing it with a more structured process. Landlords who previously relied on above-inflation rent reviews to offset rising costs will find that route more constrained. Professional rent review advice is now a practical necessity rather than an optional extra for portfolio landlords.

Market Impact: The Quality Divide and Valuation Methodology Adjustments

The broader market impact of the Renters' Rights Act 2026 is not uniform. Analysis published ahead of and following implementation consistently points to a bifurcation in the private rented sector [4].

The Emerging Quality Divide

High-quality properties — those with strong EPC ratings, modern fixtures, and no outstanding hazards — are proving resilient. Institutional investors and well-capitalised private landlords are actively seeking this stock, supporting values.

Lower-quality properties — those requiring significant capital expenditure to meet the Decent Homes Standard, or those with structural issues that generate dilapidation risk — are facing a double pressure:

- Higher compliance costs to bring them up to standard.

- Tighter lending conditions, as buy-to-let mortgage lenders revise their stress tests to account for post-Act yield compression.

This quality divide has direct implications for surveyors preparing valuation for capital gains tax purposes, particularly where landlords are exiting the market and need an accurate base-date value that reflects current market conditions rather than pre-Act assumptions.

How Surveyors Are Adjusting Valuation Methodologies

RICS has formally noted that the abolition of no-fault evictions and the shift to periodic tenancies require valuers to revisit their standard assumptions [3]. The key adjustments being adopted across the profession include:

1. Void Period Assumptions

Pre-Act standard void assumptions of 4-6 weeks per year are being revised upward. Where a Section 8 possession is likely to be contested, valuers are modelling 3-6 months of additional void exposure per tenancy cycle [8].

2. Legal Cost Provisions

A standard annual legal cost provision — previously minimal for well-managed portfolios — is now being incorporated as a standing deduction in investment valuations [8].

3. Tenant Turnover Costs

With periodic tenancies allowing tenants to leave on two months' notice, turnover frequency may increase. Each turnover event carries letting agent fees, re-marketing costs, and potential refurbishment expenditure. These are now explicit line items in investment appraisals [8].

4. Discount Rate Adjustments

Some valuers are applying a modest uplift to the discount rate used in discounted cash flow appraisals to reflect the increased regulatory and operational risk of residential investment property. Even a 25-50 basis point adjustment can produce a 5-10% reduction in capital value on a long-hold asset.

"The valuation profession must move beyond pre-Act assumptions. Properties subject to periodic tenancies and Decent Homes Standard obligations carry a materially different risk profile than they did twelve months ago." — Adapted from RICS guidance [3]

Implications for Lenders and Mortgage Products

Buy-to-let lenders are responding to the same signals. Stress tests are being recalibrated to account for lower net yields, and some lenders are applying property-condition overlays that effectively require a Decent Homes Standard-compliant property before advancing funds. This tightening of credit conditions is itself a downward pressure on values in the lower-quality segment of the market.

For landlords considering refinancing, a current RICS valuation that accurately reflects post-Act market conditions is essential — both to support the mortgage application and to avoid the risk of a lender-instructed valuation coming in below expectations.

Portfolio Landlords and Capital Gains Considerations

Landlords with larger portfolios face compounded compliance costs. A ten-property portfolio facing the average £31,411 compliance burden per landlord [2] may in practice see costs distributed unevenly, with older or lower-grade properties absorbing a disproportionate share. Where landlords are restructuring portfolios — selling underperforming assets and concentrating capital in higher-quality stock — accurate valuations are needed at each disposal point.

The interaction between Act-related value adjustments and capital gains tax liability is a live issue. A property that has declined in value due to compliance cost capitalisation may generate a smaller gain on disposal than the landlord expects based on historic cost. Specialist valuation for capital gains tax advice, prepared by a RICS-registered valuer with current market knowledge, is the appropriate tool for navigating this.

Practical Steps for Landlords, Investors, and Valuers in 2026

The Renters' Rights Act 2026 implications for property valuation: assessing landlord compliance costs and market impact demand a structured response from all parties in the residential investment market. The following actions are grounded in the current regulatory and market environment.

For Landlords

- Audit your portfolio against the Decent Homes Standard immediately. Properties with outstanding hazards face fines of up to £40,000 [5] and are the most exposed to value discounts.

- Review all tenancy agreements to ensure they reflect the periodic tenancy model. Continuing to operate under pre-Act assumptions creates legal and financial risk.

- Build a legal cost reserve for each property. Section 8 possession is now the only route to recovery, and contested cases are expensive [7].

- Commission updated valuations before refinancing, selling, or restructuring a portfolio. Pre-Act valuations may no longer reflect current market conditions.

For Valuers and Surveyors

- Update void period and legal cost assumptions in all residential investment valuations to reflect post-Act market evidence [3][8].

- Apply the quality divide framework: distinguish explicitly between Decent Homes Standard-compliant and non-compliant properties in your comparable analysis.

- Document your methodology clearly. Where adjustments are made to reflect Act-related risk, the basis for those adjustments should be transparent and defensible under Red Book standards.

- Consider dilapidation risk as a standing element of investment valuations. A dilapidation survey can provide the evidence base for quantifying the cost of bringing a property up to the required standard.

For Investors and Lenders

- Stress-test acquisition yields against post-Act net operating income, not gross rent. The gap between the two has widened materially.

- Prioritise energy-efficient, well-maintained stock where possible. The quality divide is real and is being priced into both values and lending terms [4].

- Seek RICS-compliant valuations that explicitly address Act-related adjustments. Generic automated valuations do not yet reflect the full market impact of the new legislation.

Conclusion

The Renters' Rights Act 2026 is not simply a tenant protection measure — it is a structural shift in the economics of residential investment property in England. The abolition of Section 21, the mandatory conversion to periodic tenancies, the Decent Homes Standard, and the enhanced enforcement regime collectively increase the cost and complexity of being a landlord. When those costs are properly quantified and capitalised, the result is lower net yields and, in many cases, lower capital values — particularly for properties that are already marginal in quality or condition.

Actionable next steps:

- Commission a current RICS valuation that explicitly addresses post-Act risk factors before any transaction, refinancing, or portfolio restructuring decision.

- Audit every property in a portfolio against the Decent Homes Standard and quantify the cost of remediation — this figure directly affects both value and saleability.

- Engage a specialist surveyor to review void period assumptions, legal cost provisions, and yield calculations in any existing investment appraisal prepared before May 2026.

- Seek professional rent review advice to understand the constraints on income growth under the new periodic tenancy framework.

- Where disposing of assets, obtain a formal valuation for capital gains tax purposes that reflects current, post-Act market evidence.

The landlords and investors who adapt their financial models and property standards to the new framework will be best positioned to preserve and grow portfolio value. Those who do not will find that the market — and their lenders — will price the risk for them.

References

[1] Renters Rights Act An Overview For Landlords – https://www.gov.uk/guidance/renters-rights-act-an-overview-for-landlords

[2] Renters Rights Act Compliance Costs Mount As Landlords Adapt To New Rules – https://www.mpamag.com/uk/mortgage-types/buy-to-let/renters-rights-act-compliance-costs-mount-as-landlords-adapt-to-new-rules/576130

[3] Consideration Of Implications Of Renters Rights Act On Valuation – https://www.rics.org/news-insights/consideration-of-implications-of-renters-rights-act-on-valuation

[4] Quality Divide Emerges In Rental Market As Renters Rights Act Approaches – https://www.mpamag.com/uk/mortgage-types/buy-to-let/quality-divide-emerges-in-rental-market-as-renters-rights-act-approaches/573174

[5] Councils Backed With Millions To Take On Rogue Landlords – https://www.gov.uk/government/news/councils-backed-with-millions-to-take-on-rogue-landlords

[6] United Kingdom Renters Rights Act 2025 – https://www.bakermckenzie.com/en/insight/publications/2026/01/united-kingdom-renters-rights-act-2025

[7] Courts Need More Investment Ahead Of New Renters Rights Act – https://www.lawsociety.org.uk/contact-or-visit-us/press-office/press-releases/courts-need-more-investment-ahead-of-new-renters-rights-act

[8] Valuation Methodology For Renters Rights Act 2026 Properties – https://nottinghillsurveyors.com/blog/valuation-methodology-for-renters-rights-act-2026-properties-adjusting-assessments-when-section-21-abolition-and-periodic-tenancies-reduce-investor-appeal