East Anglia stands as one of only two regions in England where property professionals reported more pronounced downward pressure on prices in May 2026 — a stark contrast to the cautious recovery signals emerging elsewhere in the country [1]. While northern markets edge forward and national sentiment begins to stabilise, East Anglia's housing market continues to lag, creating a specific and pressing challenge for buyers, sellers, and the surveyors who serve them.

Valuing East Anglia properties in 2026 lagging recovery: building survey integration for modest growth is not simply a technical exercise. It demands a combined approach — one that fuses rigorous physical inspection with market-calibrated valuation methods — to produce figures that genuinely reflect current conditions rather than outdated comparables or wishful thinking.

This article examines the regional data, explains why building surveys have become central to accurate valuation in this environment, and sets out a practical framework for navigating a market where caution is the dominant mood.

Key Takeaways

- East Anglia is among the weakest-performing regions for property pricing in 2026, with RICS data confirming sustained downward pressure on values.

- National buyer demand has stabilised but remains deeply subdued, with a net balance of -34% for new inquiries in May 2026.

- Building surveys are experiencing a surge in demand in Q2 2026, driven by cautious buyers seeking to understand physical risk before committing.

- Integrating structural defect findings — particularly RAAC, cladding, and drainage issues — directly into valuation adjustments is now considered best practice in lagging markets.

- A systematic, evidence-based approach using RICS Red Book methodology and recent comparable transactions is essential for defensible valuations in East Anglia's current conditions.

Understanding East Anglia's Position in the 2026 Property Market

The Regional Divergence Problem

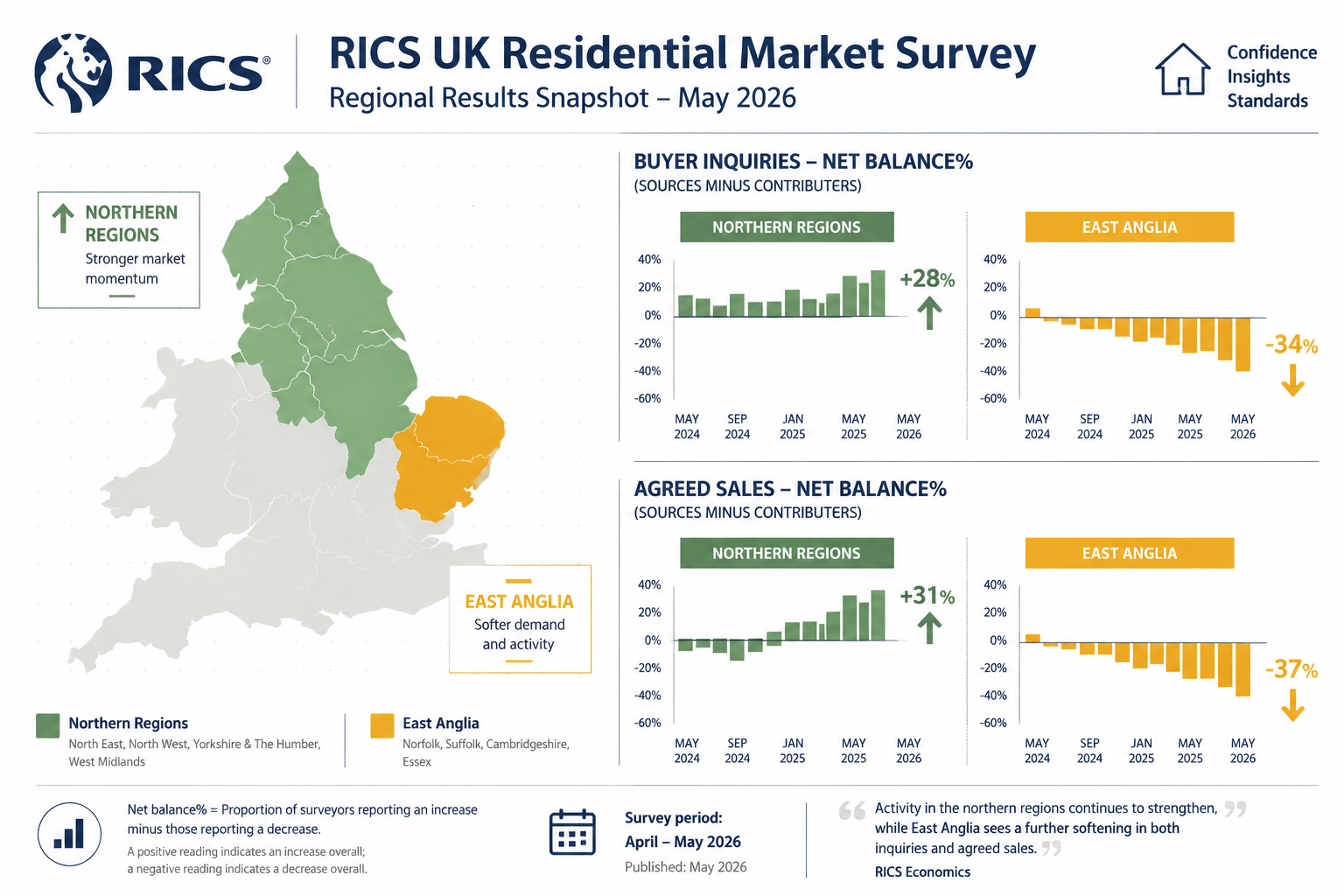

The national picture in mid-2026 is one of cautious stabilisation rather than genuine recovery. RICS reported a net balance of -34% for new buyer inquiries in May 2026, unchanged from April — a reading that signals the decline has halted rather than reversed [1]. Agreed sales held at a net balance of -37%, again showing that the rate of deterioration has stopped worsening [1]. A slim 2% net balance of professionals expect sales to improve over the next 12 months, reflecting cautious optimism at best [1].

Within this already subdued national picture, East Anglia occupies a particularly difficult position. RICS specifically identified the region as one of the weakest for pricing conditions, with local professionals reporting more pronounced downward pressure than their counterparts in most other parts of England [1]. Northern regions, by contrast, are showing comparatively stronger momentum — a divergence that makes applying national trends to East Anglia a significant valuation risk.

Why East Anglia Is Lagging

Several structural factors contribute to this regional underperformance:

- Affordability stretch: Pandemic-era price inflation pushed values in parts of East Anglia — particularly commuter zones around Cambridge, Ipswich, and Norwich — to levels that are now difficult to sustain without strong wage growth.

- Remote working reversal: The "escape to the country" premium that boosted rural East Anglian properties in 2020-2022 has partially unwound as employers reassert office attendance expectations.

- Transaction timeline extension: The average time from listing to completion has reached 21.5 weeks nationally — the longest since RICS began recording this metric in 2017 [1]. In slower regional markets like East Anglia, this figure is likely to be even more extended.

- New supply pressure: Residential and mixed-use development pipelines that stalled during 2023-2024 are beginning to move forward again [5], adding supply into a market where demand remains constrained.

Understanding these dynamics is the essential starting point for any professional engaged in valuing East Anglia properties in 2026's lagging recovery.

Building Survey Integration for Modest Growth: The Core Framework

Why Building Surveys Have Become Central to Valuation

Q2 2026 has seen a notable surge in demand for building surveys, driven by renewed mortgage lending volumes and a market where buyers are acutely risk-conscious [2]. This is not coincidental. In a market where prices are under pressure and transaction timelines are extended, buyers and their lenders need a far more granular understanding of physical condition before committing to a price.

The traditional approach — commissioning a valuation and a survey as separate exercises — is increasingly inadequate in lagging markets. When a property has structural defects, drainage problems, or legacy material risks, those findings must feed directly into the valuation figure rather than sitting in a separate report that may or may not be read by the valuer.

Building survey integration means that the physical inspection informs the valuation methodology from the outset. This produces:

- A more defensible valuation figure

- Clearer risk disclosure for mortgage lenders

- Stronger negotiating evidence for buyers

- Reduced likelihood of post-completion disputes

For those unfamiliar with the range of survey types available, comparing different types of survey is a useful starting point before selecting the appropriate level of inspection for a given property.

High-Risk Defects Requiring Valuation Adjustment in 2026

Surveyors operating in East Anglia in 2026 are placing particular emphasis on a set of defect categories that carry disproportionate financial risk [3]:

| Defect Category | Valuation Impact | Typical Adjustment Range |

|---|---|---|

| RAAC (Reinforced Autoclaved Aerated Concrete) | Severe — potential unmortgageability | 15-40% reduction or full write-down |

| Cladding non-compliance | Severe — EWS1 issues | 10-30% reduction |

| Structural movement / subsidence | Moderate to severe | 5-25% reduction |

| Drainage failure | Moderate | 3-10% reduction |

| Flat roof deterioration | Moderate | 2-8% reduction |

| Damp and timber decay | Mild to moderate | 2-12% reduction |

Each of these requires not just identification but quantification. A surveyor noting "evidence of historic movement" without specifying whether it is active, the likely cause, and the remediation cost provides insufficient information for a valuation adjustment.

Detailed subsidence surveys and drainage surveys are increasingly being commissioned as standalone follow-up investigations where initial building surveys flag concerns, allowing valuers to apply specific rather than estimated cost adjustments.

The RICS Red Book Approach in Lagging Markets

Accurate valuation in East Anglia's current conditions requires strict adherence to RICS Red Book methodology, with particular attention to comparable selection and adjustment [6]. The key principles in practice are:

1. Recency weighting of comparables

In a falling or stabilising market, comparables from 12-18 months ago may significantly overstate current value. Valuers should weight recent transactions — ideally within the last three to six months — most heavily, with older comparables used only where recent evidence is thin.

2. Systematic adjustment frameworks

Rather than applying intuitive adjustments, RICS guidance supports a structured approach where each material difference between the subject property and a comparable is assigned a specific monetary or percentage adjustment. Physical condition findings from the building survey feed directly into this framework.

3. Transparency of reasoning

In a market where values are under pressure, any valuation figure that cannot be clearly supported by comparable evidence and condition-based adjustments is vulnerable to challenge. The RICS Red Book valuation standard requires that reasoning be documented and defensible.

4. Avoiding anchoring to asking prices

In East Anglia's current market, asking prices frequently reflect vendor expectations rather than market reality. Valuers must resist anchoring to listed prices and instead build upward from transaction evidence.

"The discipline of integrating physical condition findings into a systematic adjustment framework is what separates a defensible valuation from an educated guess in a lagging market."

For properties where insurance reinstatement values also need to be established — a separate but related exercise — RICS reinstatement build cost valuations provide the appropriate methodology.

Practical Strategies for Surveyors and Buyers in East Anglia's 2026 Market

Commissioning the Right Survey for the Property Type

East Anglia's housing stock is diverse, ranging from Victorian terraces in Ipswich and Norwich to exposed rural farmhouses, post-war housing estates, and modern new-build developments on the urban fringe. The appropriate survey type varies significantly by property age, construction type, and intended use.

For most pre-1980 properties in the region, a full RICS home survey or Level 2 homebuyer survey provides the baseline, but properties with visible defects, unusual construction, or significant age should be directed toward a full building survey. The RICS homebuyer survey Level 2 is appropriate for properties in reasonable condition where no significant defects are anticipated, but this should not be the default choice in a market where physical risk is elevated.

For commercial properties in the region — including the mixed-use developments now moving forward as the pipeline stirs [5] — a RICS commercial building survey provides the depth of analysis required for investment-grade decisions.

Roof Condition as a Valuation Trigger

East Anglia's flat landscape and exposure to North Sea weather systems mean that roof condition is a particularly significant defect category in the region. Deteriorating flat roofs, failed flashings, and inadequate drainage are common findings in older stock.

A specialist roof survey should be commissioned wherever a building survey flags roof concerns, providing cost-specific evidence that can be translated directly into a valuation adjustment or a negotiated price reduction.

Party Wall Considerations for Development Properties

In East Anglia's slow-moving market, developers and investors pursuing refurbishment or extension projects must manage party wall risk carefully. Proper party wall procedures are being actively used in the region to prevent costly disputes and protect investment returns [4]. For properties where works are planned, early engagement with party wall procedures — before exchange of contracts — is strongly advisable.

Asbestos and Non-Standard Construction

East Anglia contains a significant proportion of post-war housing built using non-standard construction methods, including properties with asbestos-containing materials. Asbestos surveys are a necessary precaution for properties built before 2000, and findings must be factored into both the valuation and any planned refurbishment budget.

Similarly, non-standard construction assessments are essential for properties built using concrete frame, prefabricated, or other non-traditional methods — categories that can significantly affect mortgageability and therefore market value.

Valuation for Specific Purposes

Beyond standard market valuations, several specialist valuation types are relevant in East Anglia's 2026 market:

- Shared ownership valuations: As affordable housing schemes expand in the region, shared ownership valuations must reflect current market conditions rather than historic purchase prices.

- Matrimonial valuations: In a market where values are under pressure, matrimonial valuations require particular care to ensure that both parties receive a fair assessment based on current rather than peak-market evidence.

- Insurance reinstatement: Separate from market value, insurance reinstatement valuations ensure that rebuild costs are adequately covered — an issue that becomes more acute when construction costs remain elevated relative to market values.

The Role of Comparable Evidence in Thin Markets

One of the practical challenges in valuing East Anglia properties in 2026's lagging recovery is the scarcity of recent comparable transactions in some sub-markets. Extended transaction timelines mean that the volume of completed sales evidence is lower than in more active markets [1]. Surveyors must therefore:

- Cast a wider geographic net for comparables, with appropriate adjustments for location differences

- Use Land Registry data alongside agent-reported transactions to maximise the evidence base

- Apply greater weight to condition-based adjustments where comparable evidence is limited

- Document the limitations of the comparable evidence base transparently in valuation reports

Building Sector Recovery and Its Implications for East Anglia Values

Early 2026 brought signs of recovery in the broader construction and building sector, with previously delayed residential and mixed-use projects beginning to move forward [5]. For East Anglia, this has a dual implication.

On one hand, renewed development activity signals returning confidence and will eventually support values as economic activity increases. On the other, new supply entering a market where demand remains subdued can exert additional downward pressure on existing stock — particularly older properties competing with new-build incentives.

Surveyors and valuers must monitor local planning permissions and development completions as part of their market analysis, treating new supply as a material factor in comparable selection and value adjustment.

The building survey demand surge of Q2 2026 [2] reflects buyers' recognition that in this environment, understanding physical condition is not optional — it is the primary tool for managing financial risk in a market where price discovery is genuinely difficult.

Conclusion

Valuing East Anglia properties in 2026 lagging recovery: building survey integration for modest growth requires a disciplined, evidence-based approach that treats physical inspection and market valuation as a single integrated process rather than two separate exercises.

The regional data is clear: East Anglia faces more pronounced pricing pressure than most of England, transaction timelines are at historic highs, and buyer demand — while stabilising — remains deeply subdued [1]. In this environment, a valuation that does not account for physical condition findings is not merely incomplete; it is potentially misleading to buyers, lenders, and sellers alike.

Actionable next steps for those operating in East Anglia's 2026 market:

- Commission a full building survey — not just a Level 2 homebuyer report — for any pre-1980 property or any property showing visible defects.

- Ensure that building survey findings are formally communicated to the valuer before the valuation is completed, so that adjustments can be applied systematically.

- Request specialist follow-up surveys (roof, drainage, subsidence, asbestos) wherever the building survey flags material concerns.

- Insist on comparable evidence from the last three to six months, and scrutinise any valuation that relies heavily on older transactions.

- Factor extended transaction timelines into financial planning — 21.5 weeks is the current national average, and East Anglia is likely to exceed this [1].

- For development or refurbishment projects, engage with party wall procedures and non-standard construction assessments before exchange.

The modest growth that East Anglia's market may achieve over the coming 12 months will be captured most effectively by those who understand the physical condition of what they are buying or valuing — and who use that understanding to make genuinely informed decisions.

References

[1] Subdued Housing Market May Be Starting To Stabilise Surveyors – https://www.itv.com/news/2026-06-10/subdued-housing-market-may-be-starting-to-stabilise-surveyors?utm_source=openai

[2] Building Survey Demand Surge In Q2 2026 Capitalising On Market Recovery While Managing Regional Price Divergence – https://wimbledonsurveyors.com/building-survey-demand-surge-in-q2-2026-capitalising-on-market-recovery-while-managing-regional-price-divergence/?utm_source=openai

[3] Building Survey Priorities In 2026 Market Recovery Raac Cladding And Latent Defects For Stabilising Prices – https://nottinghillsurveyors.com/blog/building-survey-priorities-in-2026-market-recovery-raac-cladding-and-latent-defects-for-stabilising-prices?utm_source=openai

[4] Party Wall Surveys For East Anglias Lagging Recovery Rics Strategies To Mitigate Developer Risks In Slow Moving Markets – https://kingstonsurveyors.com/party-wall-surveys-for-east-anglias-lagging-recovery-rics-strategies-to-mitigate-developer-risks-in-slow-moving-markets/?utm_source=openai

[5] Signs Of A Building Recovery As Pipeline Begins To Stir – https://www.constructionenquirer.com/2026/02/20/signs-of-a-building-recovery-as-pipeline-begins-to-stir/?utm_source=openai

[6] Valuing Stabilised House Prices In Lagging Regions Rics Techniques For South East And East Anglia 2026 – https://nottinghillsurveyors.com/blog/valuing-stabilised-house-prices-in-lagging-regions-rics-techniques-for-south-east-and-east-anglia-2026?utm_source=openai