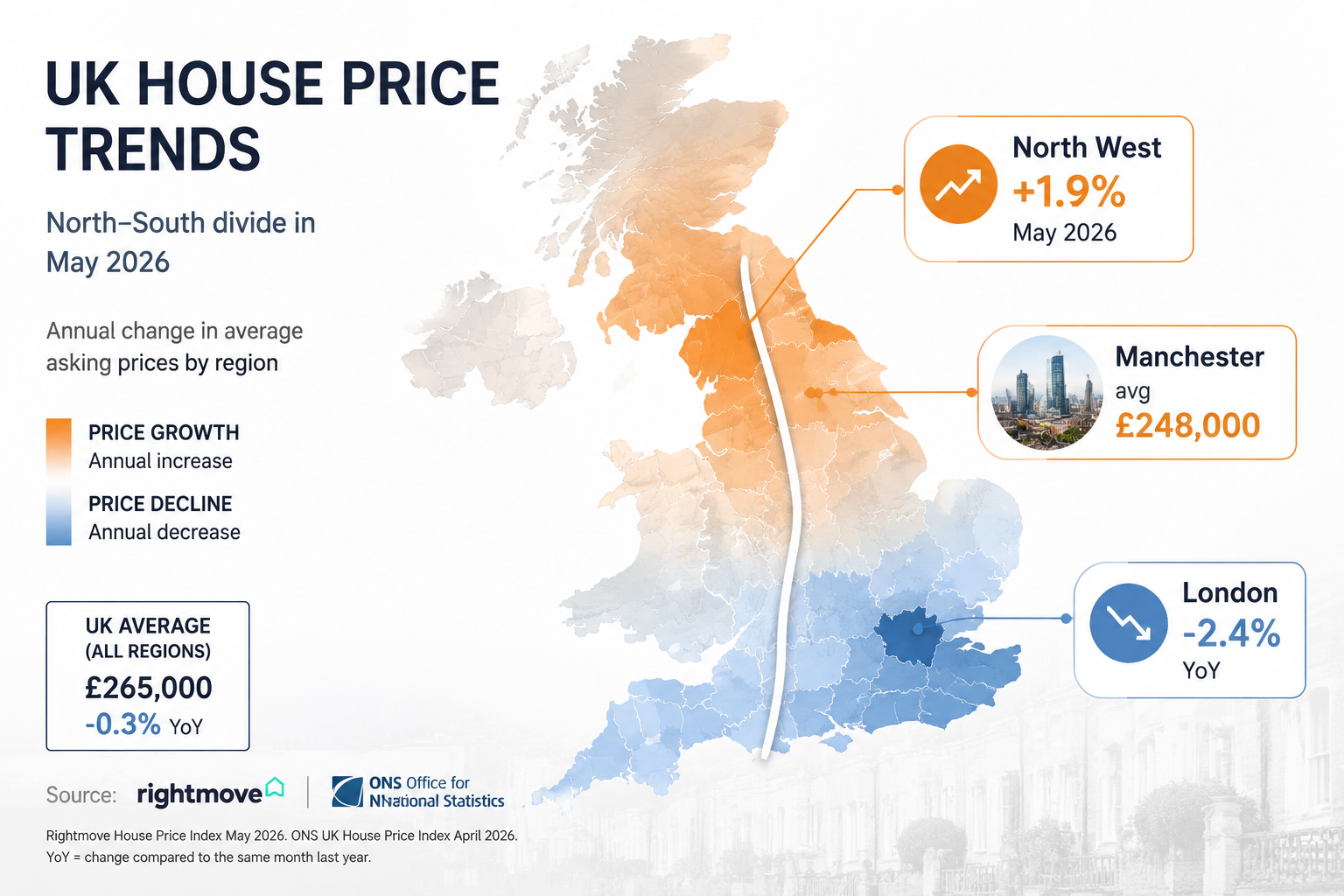

The North-South divide in UK property has rarely been this stark: in May 2026 alone, North West asking prices climbed 1.9% — the strongest single-month regional gain recorded by Rightmove across the entire country — while London asking prices have fallen 2.4% year-on-year. For buyers, sellers, investors and buy-to-let landlords active in Manchester, Salford and Trafford, this divergence is not merely a headline statistic. It is a live signal with direct implications for acquisition strategy, survey requirements and portfolio valuation.

The north south divide property May 2026 Manchester asking prices up 1.9% London down 2.4% story is grounded in fundamentals: relative affordability, regeneration momentum, improving transport infrastructure and a rental market that continues to outperform the national average. Understanding what sits behind those numbers — and what professional due diligence is required before committing capital — is the purpose of this article.

Key Takeaways

- North West asking prices rose 1.9% in May 2026, the strongest monthly regional growth in the UK (Rightmove).

- Manchester's average house price reached £248,000 in March 2026, up 1.4% year-on-year (ONS provisional).

- London asking prices are down 2.4% year-on-year; the South East has also retreated 1.6%.

- Manchester gross rental yields currently sit at 6–6.6%, making it one of the UK's most attractive BTL markets.

- A RICS Building Survey is essential before purchasing Victorian terraces, mill conversions or new-build BTR stock in Greater Manchester.

Table of Contents

- The Data Behind the North-South Divide in May 2026

- Why Manchester and the North West Are Outperforming

- What the Numbers Mean for Manchester Buyers and Investors

- Survey and Due Diligence Requirements in Greater Manchester

- BTL Investors: Yield, Valuation and Leasehold Risks

- FAQ

- Conclusion

The Data Behind the North-South Divide in May 2026

The regional picture emerging from May 2026 data represents a decisive shift in the UK's property geography.

| Region | Monthly Change (May 2026) | Annual Change (YoY) |

|---|---|---|

| North West | +1.9% | +2.6% |

| North East | N/A | +2.7% |

| Yorkshire & Humber | Positive | ~+2.0% |

| London | Negative | -2.4% |

| South East | Negative | -1.6% |

Sources: Rightmove (asking prices, May 2026); ONS/Land Registry (completed transactions)

According to Rightmove's May 2026 data, the North West's 1.9% single-month gain was the strongest of any UK region — a figure that stands in sharp contrast to London's ongoing correction. The South East has also retreated 1.6% annually, reflecting affordability ceilings and reduced demand from overseas buyers.

ONS provisional data places the Manchester average house price at £248,000 in March 2026, up 1.4% year-on-year. Land Registry completed transaction data corroborates this trajectory, with volume holding firm in M1, M2, M14 and Salford postcodes. Agents including Joseph Mews, who focus specifically on the Manchester investment market, have reported sustained demand from both domestic and international BTL purchasers, citing the city's yield profile as a primary driver.

"The North-South divide in property May 2026 — Manchester asking prices up 1.9%, London down 2.4% — is not a temporary blip. It reflects a structural rebalancing that has been building for several years."

The Bank of England base rate currently stands at 3.75%, with two-year fixed mortgage rates averaging 5.68%. While borrowing costs remain elevated relative to the pre-2022 era, they are materially lower than the peak of late 2023, and Manchester's yield profile means that BTL arithmetic remains viable in a way that is simply not possible in prime London postcodes.

Why Manchester and the North West Are Outperforming

Several converging factors explain why the north south divide property May 2026 Manchester asking prices up 1.9% London down 2.4% dynamic has emerged with such force.

Regeneration at Scale

Three major schemes are actively reshaping demand geography across Greater Manchester:

- NOMA (M1/M2): The 20-acre mixed-use district north of Manchester city centre continues to attract commercial occupiers and residential demand, lifting values in adjacent postcodes.

- Mayfield near Piccadilly: The 24-acre Mayfield development, anchored by a new city park, is creating a new residential and leisure quarter that is already influencing asking prices in M1 and M12.

- Trafford Waters: This 100-acre waterside development in Stretford is drawing significant BTL and owner-occupier interest, with Trafford's connectivity and school catchments adding further appeal.

Metrolink Expansion

Metrolink improvements are enhancing connectivity to M14 (Fallowfield, Withington), M20 (Didsbury) and across Salford. Improved journey times to the city centre are directly capitalising into residential values in postcodes that were previously considered secondary. Understanding how transport improvements affect property values is an important part of any acquisition appraisal in these areas.

Relative Affordability

At £248,000, Manchester's average house price is roughly one-fifth of the London average. Even accounting for lower average wages, the price-to-income ratio in Manchester remains significantly more accessible, sustaining a broader pool of owner-occupier demand that underpins investor exits.

What the Numbers Mean for Manchester Buyers and Investors

For buyers and investors responding to the north south divide property May 2026 Manchester asking prices up 1.9% London down 2.4% data, the opportunity is real — but so are the risks specific to Greater Manchester's housing stock.

Forecasts and Yield Context

Manchester is forecast to deliver 3–4% capital growth across 2026 (Joseph Mews), with gross rental yields of 6–6.6% across core investment postcodes including Salford, Ancoats, Hulme and Didsbury. At current mortgage rates, this yield level allows experienced investors to structure deals with positive or near-neutral cash flow, which is not achievable in most London markets.

Stock-Specific Risks

Manchester's housing stock is diverse, and each property type carries distinct survey requirements:

- Victorian terraces (common in Salford, Gorton, Levenshulme): Subject to damp penetration, original timber floors, ageing drainage and partial or full lack of cavity wall insulation.

- Mill and warehouse conversions (Ancoats, Castlefield, Northern Quarter): Structural modifications, flat roof sections, complex leasehold arrangements and potential residual industrial contamination.

- New-build BTR blocks (Deansgate, Salford Quays, NOMA): Cladding and fire safety compliance, EWS1 certification requirements on buildings over 11 metres, and snagging defects on recently completed units.

Survey and Due Diligence Requirements in Greater Manchester

A mortgage valuation is not a survey. This distinction matters enormously in a rising market where buyers face competitive pressure to move quickly. A RICS Level 3 Building Survey from a qualified Manchester surveyor is the appropriate standard for Victorian terraces, mill conversions and any property where structural or damp risk is a material concern.

Key survey considerations by property type:

Victorian and Edwardian Terraces

- Rising and penetrating damp in solid-wall construction

- Chimney stack stability and flaunching condition

- Roof covering, lead valleys and guttering

- Timber floor joist condition and woodworm/rot

- A professional damp survey in Manchester should be commissioned separately where the Level 3 survey flags moisture readings

Mill Conversions and Apartments

- Leasehold terms: ground rent escalation clauses, service charge history and reserve fund adequacy

- EWS1 (External Wall System) certification: essential for any flat in a building over 11 metres — without it, mortgage lenders will decline, and resale is severely restricted

- Understanding freehold versus leasehold is critical before committing to an apartment purchase in Manchester city centre

New-Build BTR

- A snagging report identifies defects before legal completion, while the developer's warranty is still active

- Structural surveys may be warranted on large-format concrete frame buildings where post-construction movement is suspected

Buyers uncertain about which survey level is appropriate can compare different survey types to match the right product to the property.

BTL Investors: Yield, Valuation and Leasehold Risks

For BTL landlords, the north south divide property May 2026 Manchester asking prices up 1.9% London down 2.4% picture translates into a clear strategic case for Greater Manchester — provided that investment decisions are underpinned by accurate, independent valuations rather than developer marketing materials.

Why an Independent RICS Valuation Matters

Off-plan and new-build BTL units in Manchester are frequently marketed at prices that reflect anticipated demand rather than current comparable evidence. An independent RICS Red Book valuation provides a defensible, lender-acceptable figure and protects investors from overpaying in a market where sentiment is running ahead of fundamentals in some micro-locations.

Yield-Based Valuation for Commercial and HMO Stock

Investors acquiring HMOs, student accommodation or small commercial units should commission a commercial property valuation that applies an income capitalisation methodology. This approach anchors value to achievable rent rather than speculative capital appreciation.

Ground Rent and Leasehold Reform

The Leasehold and Freehold Reform Act 2024 has changed the landscape for ground rent, but legacy leases with doubling ground rent clauses remain in circulation in Manchester's apartment stock. Investors must instruct solicitors to scrutinise lease terms and, where necessary, factor lease extension valuation costs into their acquisition modelling.

FAQ

What is driving Manchester asking prices up 1.9% in May 2026?

The primary drivers are relative affordability compared to southern England, large-scale regeneration projects (NOMA, Mayfield, Trafford Waters), Metrolink expansion improving connectivity, and sustained rental demand that supports investor confidence.

Why are London asking prices falling while Manchester rises?

London's correction reflects affordability exhaustion, reduced overseas buyer activity, higher stamp duty costs on higher-value properties and a structural shift in remote-working patterns that has reduced the premium placed on proximity to central London.

Do I need a full RICS Building Survey on a Manchester Victorian terrace?

Yes, in most cases. Victorian solid-wall terraces carry elevated risks of damp, structural movement and outdated services. A Level 3 Building Survey provides the detailed assessment needed to negotiate price, budget for repairs and avoid costly surprises post-completion.

What is EWS1 and why does it matter for Manchester flat buyers?

EWS1 (External Wall System) is a fire safety certificate required by mortgage lenders for flats in buildings over 11 metres. Without a valid EWS1, buyers cannot obtain a mortgage and resale is effectively blocked. Always confirm EWS1 status before exchanging contracts on a Manchester apartment.

Are Manchester gross rental yields genuinely 6–6.6% in 2026?

Gross yields of 6–6.6% are achievable in postcodes such as Salford, Hulme, Ancoats and parts of M14, based on current asking rents and purchase prices. Net yields will be lower after voids, management fees, maintenance and mortgage costs. An independent RICS valuation and cash-flow analysis are essential before committing.

Should BTL investors in Manchester use a RICS valuation or rely on developer pricing?

Always commission an independent RICS Red Book valuation. Developer pricing on new-build and off-plan stock frequently reflects marketing premiums that are not supported by comparable evidence, which can result in negative equity on completion and lender down-valuations.

Conclusion

The north south divide property May 2026 Manchester asking prices up 1.9% London down 2.4% data represents one of the clearest regional divergences in the UK market for over a decade. Manchester and the wider North West are benefiting from a compelling combination of affordability, regeneration, infrastructure investment and rental demand — factors that are likely to sustain the 3–4% capital growth forecast for 2026 and keep gross yields firmly in the 6–6.6% range.

However, strong market momentum does not eliminate property risk. It can obscure it. Victorian terraces carry damp and structural vulnerabilities. Mill conversions carry leasehold complexity. New-build towers carry EWS1 and snagging exposure. Every acquisition in Greater Manchester deserves independent, professional scrutiny before funds are committed.

Actionable next steps for buyers, sellers and investors in Manchester, Salford and Trafford:

- Commission a RICS Level 3 Building Survey on any Victorian, Edwardian or converted property before exchange.

- Obtain an independent RICS Red Book valuation on any BTL acquisition, particularly new-build or off-plan units.

- Confirm EWS1 status on any apartment in a building exceeding 11 metres before proceeding.

- Review leasehold terms carefully — ground rent clauses and service charge histories must be scrutinised.

- Factor Metrolink connectivity and regeneration proximity into yield modelling for M14, M20 and Salford postcodes.

- Contact Manchester Surveyors to discuss the right survey or valuation product for your specific property type and investment objective.