Buyer enquiries across England and Wales dropped by an estimated 26% in February 2026, according to RICS sentiment data — a figure that sends a clear signal to every valuation surveyor working in the private rented sector (PRS). When demand softens this sharply, the mechanics of valuing PRS properties shift. Lenders tighten their criteria, comparable evidence thins out, and compliance obligations under the Renters' Rights Act 2025 and Awaab's Law add fresh layers of complexity. Valuing PRS properties amid the RICS February 2026 buyer dip requires a disciplined, evidence-based approach that accounts for cautious lending conditions, evolving hazard compliance standards, and the structural changes reshaping landlord-tenant relationships across the UK.

Key Takeaways 📌

- A 26% drop in buyer enquiries in February 2026 directly compresses comparable evidence and widens valuation uncertainty bands for PRS assets.

- Cautious lender behaviour — including lower loan-to-value ratios and stricter rental income stress tests — must be factored into any Red Book valuation of a rental property.

- Renters' Rights Act 2025 provisions (pet permissions, abolition of fixed-term tenancies, and rent cap mechanisms) materially affect investment yield calculations.

- Awaab's Law hazard compliance is now a live valuation risk factor: non-compliant properties face mandatory remediation timelines that depress market value.

- Regional strategies matter: Manchester, the Midlands, and London each present distinct adjustment considerations in a subdued market.

Understanding the February 2026 RICS Buyer Dip and Its Valuation Impact

The RICS Residential Market Survey for February 2026 painted a cautious picture. New buyer enquiries fell sharply, instructions to sell remained subdued, and agreed sales volumes contracted. For PRS property owners and their advisers, this is not merely a headline statistic — it directly affects the quantity and quality of comparable transactions available to support a formal valuation.

Under RICS Red Book Global Standards (VPS 4), valuers are required to identify and analyse comparable market evidence. When transaction volumes fall by more than a quarter, the comparable pool shrinks. Surveyors must therefore:

- Widen the search radius for comparables, potentially crossing into adjacent postcodes.

- Apply time adjustments to older transactions to reflect current market sentiment.

- Increase the explicit uncertainty range in their valuation reports, as permitted under RICS guidance.

- Weight rental income evidence more heavily when investment method valuations are employed.

💬 "In a thin market, the valuer's judgement carries more weight — and so does the documentation supporting that judgement."

For landlords seeking a RICS Red Book valuation on their Manchester property, the February 2026 conditions mean that the surveyor's narrative commentary is as important as the headline figure. A well-reasoned report explaining market conditions protects both the client and the valuer.

How Buyer Sentiment Translates to Yield Compression

When fewer buyers compete for PRS stock, gross initial yields tend to rise — which, counterintuitively, means capital values fall. A buy-to-let terrace in Greater Manchester that achieved a 5.5% yield in mid-2025 may now need to offer 6.0–6.5% to attract a purchaser, simply because the buyer pool is smaller and more selective. That yield shift can represent a 5–10% reduction in capital value on a like-for-like basis.

Valuers working in this environment must resist the temptation to anchor on peak comparable evidence. The February 2026 dip is real, and valuations that ignore it expose lenders and clients to significant downside risk.

Cautious Lending Adjustments: What Surveyors Must Account For in 2026

Lender behaviour in early 2026 reflects accumulated caution built up over 18 months of elevated base rates, regulatory change, and post-Renters' Rights Act uncertainty. Understanding how lenders are stress-testing PRS portfolios is essential when valuing PRS properties amid the RICS February 2026 buyer dip.

Rental Income Stress Tests

Most high-street lenders are now applying rental income stress tests at 145–160% of the mortgage interest payment, calculated at a notional rate of 6.5–7.5%. This is meaningfully tighter than the 125% tests common before 2022. For a surveyor, this means:

- Achievable rental income must be evidenced rigorously, not estimated optimistically.

- Properties where the market rent has been suppressed by long-standing tenancies need careful open-market rent assessments.

- Any rent cap provisions under the Renters' Rights Act 2025 — which limits in-tenancy rent increases to once per year and ties them to market evidence — must be reflected in projected income streams.

Loan-to-Value Caution

Lenders are increasingly capping PRS buy-to-let mortgages at 65–70% LTV for standard properties, and lower still for houses in multiple occupation (HMOs) or properties with identified hazards. This directly affects the mortgage valuation a surveyor must provide.

Understanding whether a mortgage valuation is the same as a survey is critical context here. A mortgage valuation is a brief lender-focused opinion of value; it does not replace a full building survey. In the current climate, lenders are scrutinising mortgage valuations more closely and querying any figure that appears to outpace the subdued market evidence.

Renters' Rights Act 2025: The Three Valuation Pressure Points

The Renters' Rights Act 2025, which received Royal Assent and came into force progressively through late 2025 and early 2026, introduces three provisions with direct valuation consequences:

| Provision | Valuation Impact |

|---|---|

| Abolition of fixed-term tenancies | Increases void risk perception; reduces certainty of income stream |

| Pet permissions (default right to keep pets) | Potential for accelerated wear and dilapidation; affects reinstatement cost assumptions |

| Annual rent increase cap (market-linked) | Limits upside rental growth; compresses yield improvement potential |

Each of these factors feeds into an investment method valuation. A surveyor who ignores them risks producing a figure that a lender's review team will immediately challenge.

Awaab's Law Hazard Compliance: A Live Valuation Risk Factor

Awaab's Law — extended to the private rented sector through the Renters' Rights Act 2025 — imposes mandatory timelines for investigating and remedying hazards, particularly damp and mould. For valuers, this is no longer a background regulatory note. It is a front-line valuation adjustment.

What Awaab's Law Requires

Under the legislation, landlords must:

- Investigate a reported hazard within 14 days

- Begin emergency repairs within 24 hours where there is an immediate risk

- Complete all remediation within a defined period (typically 7 weeks for non-emergency hazards)

Failure to comply exposes landlords to tribunal claims, rent repayment orders, and potential civil liability. For a valuer, a property with unresolved hazards or a history of non-compliance is a materially different asset from a compliant one.

Hazard Categories That Affect PRS Valuations

🔴 Category 1 HHSRS hazards (e.g., severe damp, structural instability, excess cold) trigger the most significant valuation adjustments. A property with an outstanding Category 1 hazard may be unmortgageable until remediation is complete.

🟡 Category 2 hazards (e.g., minor damp, inadequate ventilation) require disclosure and typically attract a negotiated price reduction or a retention on completion.

Surveyors conducting damp surveys or structural surveys on PRS properties must now explicitly cross-reference their findings against Awaab's Law compliance timelines and flag the valuation implications clearly.

Practical Adjustment Methodology

When a hazard is identified, the valuation adjustment should reflect:

- Cost of remediation — obtained from contractor estimates or schedule of dilapidations

- Loss of rental income during remediation works

- Risk premium for potential tribunal exposure if the hazard has already been reported by a tenant

- Stigma discount where the property has a documented compliance history

A specific defect report is often the most efficient way to quantify items 1 and 2 before a formal valuation is finalised.

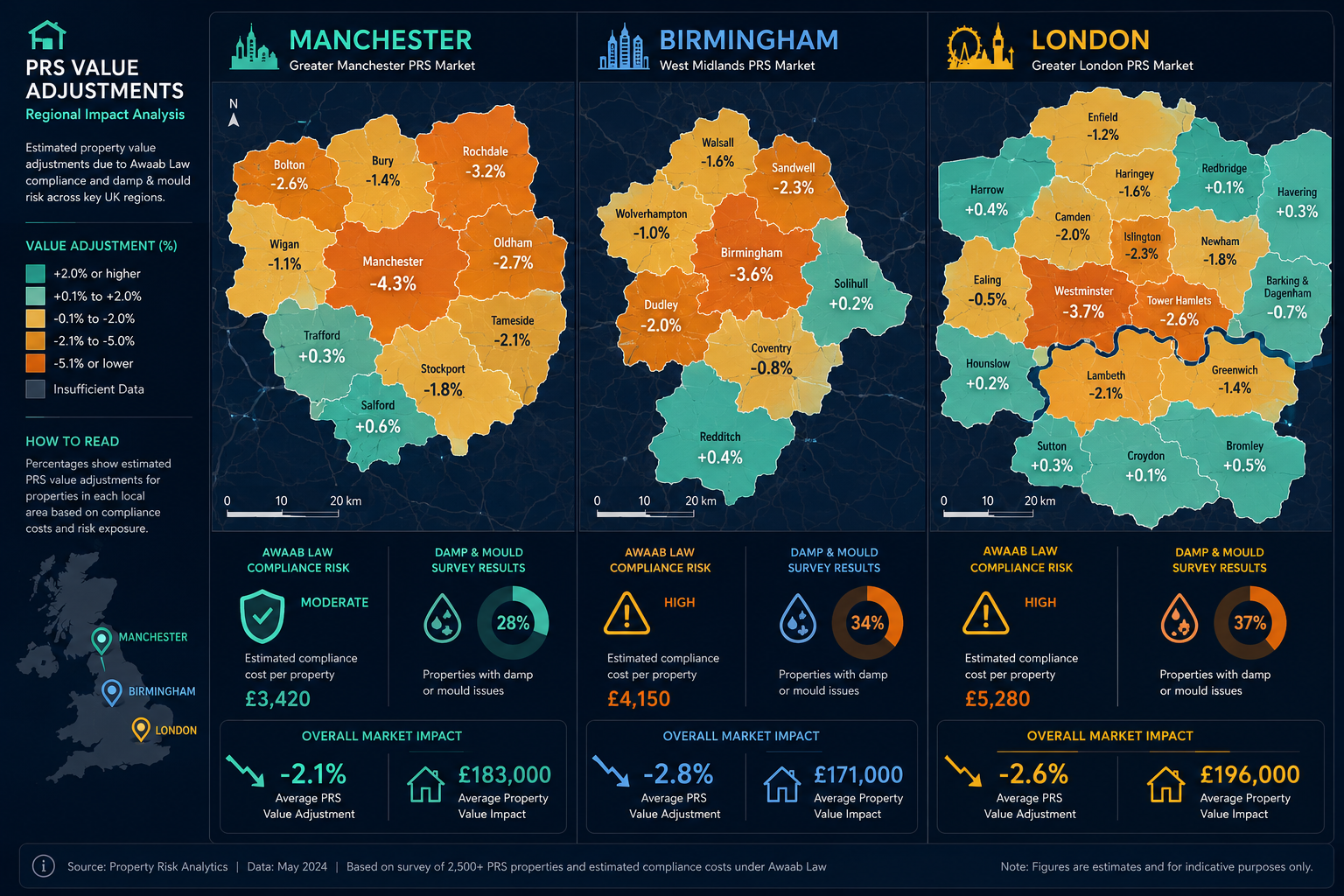

Regional Strategies for Valuing PRS Properties Amid the RICS February 2026 Buyer Dip

The February 2026 buyer dip is not uniform across the country. Regional PRS markets are responding differently, and valuing PRS properties amid the RICS February 2026 buyer dip requires location-specific calibration.

Greater Manchester

Manchester's PRS market entered 2026 with strong underlying rental demand — driven by student population, young professionals, and net inward migration — but transaction volumes have softened alongside the national trend. Key adjustment considerations include:

- HMO premium compression: The HMO premium over standard buy-to-let has narrowed as lender appetite for multi-let properties has reduced.

- EPC compliance pressure: Greater Manchester's large Victorian terrace stock faces significant EPC upgrade costs ahead of proposed minimum EPC C requirements, which must be factored into valuations.

- Awaab's Law exposure: Older stock in areas like Salford, Oldham, and parts of the city centre carries elevated damp and mould risk, requiring careful damp survey evidence before any valuation is finalised.

Working with RICS-certified experts in Manchester who understand the local stock profile is essential for accurate PRS valuations in this market.

The Midlands

Birmingham and the wider West Midlands PRS market is characterised by higher yields but greater sensitivity to lender caution. With average gross yields of 6.5–8% on terraced stock, the investment case remains compelling — but the February 2026 buyer dip has reduced the number of active purchasers who can actually complete transactions.

Valuers here should pay particular attention to:

- Article 4 Direction areas affecting HMO conversions

- Selective licensing scheme costs, which reduce net yields

- Properties affected by historical industrial contamination, which may trigger additional hazard assessments

London

London's PRS market presents the most complex valuation environment in 2026. High capital values mean that small yield movements translate to large absolute value changes. The February buyer dip has been most acute in outer London boroughs where affordability was already stretched.

Specific London considerations include:

- Leasehold structures: Short leases (under 80 years) face additional lender restrictions; a lease extension cost assessment may be required before a valuation can be finalised.

- Rent stabilisation pressure: Inner London rents have attracted political attention, and valuers should apply conservative rental growth assumptions.

- HMO licensing complexity: Multiple overlapping licensing regimes in boroughs like Newham, Southwark, and Haringey add compliance cost that must be reflected in valuations.

Pet Permissions, Rent Caps, and Tenancy Reform: Adjusting Investment Method Valuations

The investment method of valuation — which capitalises a net income stream at an appropriate yield — is the standard approach for PRS assets. The Renters' Rights Act 2025 changes three inputs to this calculation in ways that compound each other.

Pet Permissions and Dilapidation Risk

The default right for tenants to keep pets (subject to landlord consent, which cannot be unreasonably refused) introduces a higher dilapidation allowance into net income calculations. Valuers should:

- Increase the annual maintenance reserve by 5–15% depending on property type

- Review whether the landlord holds adequate insurance reinstatement valuation cover, as pet damage may affect reinstatement cost assumptions

- Note that pet damage is recoverable from tenants in principle, but enforcement adds cost and delay

Rent Cap Mechanics

The annual rent increase cap — tied to the lower of CPI or market rent evidence — reduces the reversionary potential of PRS assets. In a valuation context, this means:

- Passing rent (current contractual rent) and market rent must both be assessed

- Where passing rent is below market, the reversionary uplift is now constrained by the annual cap mechanism

- Discounted cash flow (DCF) models should incorporate a capped rental growth rate, not an unconstrained market growth assumption

Tenancy Certainty and Void Risk

The abolition of fixed-term assured shorthold tenancies means all new tenancies are periodic from the outset. While this provides tenants with greater security, it changes the void risk profile for investors. Valuers should apply a slightly higher void allowance (typically 8–10% of gross rent, up from 5–7%) to reflect the reduced certainty of income timing.

Practical Steps for Surveyors and Landlords in 2026

Navigating valuing PRS properties amid the RICS February 2026 buyer dip requires both surveyors and landlords to take proactive steps:

For Surveyors:

- ✅ Expand comparable search parameters and document all time-adjustment rationale

- ✅ Explicitly address Awaab's Law compliance status in every PRS valuation report

- ✅ Apply Renters' Rights Act adjustments to all three investment method inputs

- ✅ Engage RICS-registered valuers who are current on 2026 regulatory changes

- ✅ Consider whether a building survey is needed alongside the valuation to identify hazards early

For Landlords:

- ✅ Commission a pre-valuation hazard assessment to identify and remediate Awaab's Law issues

- ✅ Ensure all tenancy documentation reflects Renters' Rights Act 2025 requirements

- ✅ Review EPC ratings and obtain upgrade cost estimates before marketing

- ✅ Provide clear rental income evidence — including any rent arrears history — to support the valuation

- ✅ Get a quote from a qualified surveyor before agreeing a sale price in the current subdued market

Conclusion: Precision Valuation in a Cautious Market

The February 2026 buyer dip is a defining moment for PRS property valuation in England and Wales. With enquiries down sharply, lenders applying tighter stress tests, and the Renters' Rights Act 2025 reshaping the investment landscape, there is no room for optimistic assumptions or thin comparable evidence.

Actionable next steps for 2026:

- Commission a full RICS Red Book valuation — not just a mortgage valuation — for any PRS asset being sold, refinanced, or restructured in the current market.

- Address Awaab's Law hazards before marketing: remediated properties command better values and attract more lenders.

- Rebuild your investment model to incorporate pet dilapidation allowances, capped rental growth, and higher void rates under the Renters' Rights Act.

- Use regional expertise: a surveyor who understands Manchester's Victorian terrace stock, or London's leasehold complexity, will produce a more defensible valuation than a generalist.

- Document everything: in a thin market, the quality of the valuation narrative is as important as the headline figure.

The surveyors and landlords who treat these adjustments as a one-time exercise will be caught out. Those who embed them into their standard valuation and asset management processes will navigate the 2026 market with confidence.