Nearly one in five UK homebuyers who opted for a basic survey later discovered significant defects that a more thorough inspection would have flagged — defects costing an average of £5,750 to £12,000 to repair. In 2026, with mortgage affordability still stretched and lenders applying cautious criteria, that kind of post-completion surprise can derail household finances for years. Upgrading from a HomeBuyer Report to a Full Building Survey: When the Extra Cost Is Worth It in 2026 is not a question of luxury — it is a question of risk management, and the answer depends heavily on the property you are buying.

This article provides a clear decision framework for buyers weighing the two main residential survey levels, with particular focus on older housing stock, non-standard construction, coastal and high-exposure locations, and properties with a history of alterations.

Key Takeaways 📋

- A Full Building Survey (RICS Level 3) costs more upfront but provides a far deeper analysis of structural integrity, hidden defects, and repair costs.

- A HomeBuyer Report (RICS Level 2) suits modern, well-maintained properties in good condition — but leaves significant gaps for older or complex homes.

- Properties built before 1920, those using non-standard construction, coastal homes, and those with past extensions or alterations carry higher risk under a Level 2 inspection.

- In 2026's cautious lending climate, an undetected defect can affect remortgaging, insurance, and resale value — not just immediate repair bills.

- The upgrade cost (typically £300–£600 more) is almost always justified when the risk profile of the property is elevated.

Understanding the Two Survey Levels

Before weighing the upgrade decision, it helps to be precise about what each survey actually delivers.

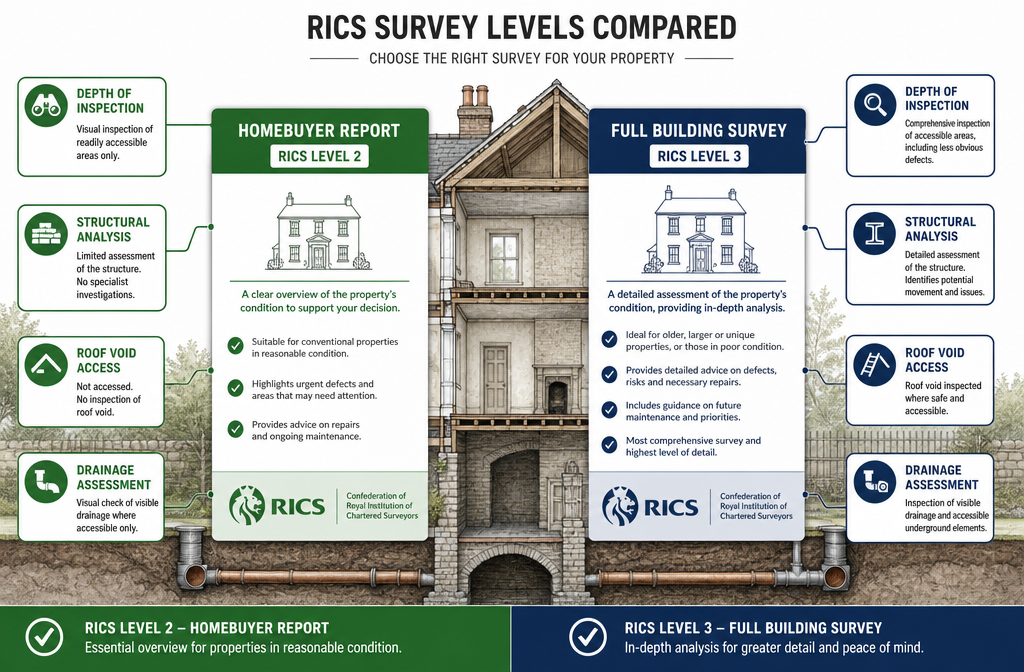

RICS Level 2: The HomeBuyer Report

The HomeBuyer Survey is a standardised, traffic-light-coded report designed for conventional properties in reasonable condition. A surveyor conducts a visual inspection of accessible areas, rating elements from condition 1 (no repair needed) to condition 3 (urgent attention required). It includes a market valuation and insurance reinstatement figure.

What it covers:

- Visible structural elements (walls, roof, floors)

- Dampness, timber condition, and insulation (where accessible)

- Services (a visual check only)

- Legal issues to raise with a solicitor

What it does not cover:

- Areas behind furniture, under fitted carpets, or inside roof voids requiring specialist access

- Detailed analysis of structural movement or subsidence

- In-depth assessment of non-standard materials

- Specific defect investigation

RICS Level 3: The Full Building Survey

A Full Building Survey — also known as a structural survey — is a bespoke, highly detailed inspection. There is no standard template; the report is tailored to the specific property. The surveyor investigates as thoroughly as safely possible, lifting inspection hatches, probing timbers, and assessing the building fabric in depth.

What it adds:

- Detailed description of construction methods and materials

- Analysis of structural movement, cracking, and subsidence risk

- Roof void and subfloor inspection (where accessible)

- Advice on repair methods and likely costs

- Assessment of past alterations and their implications

💬 "A Level 3 survey does not just tell you what is wrong — it tells you why it is wrong, how serious it is, and what fixing it will involve."

For a side-by-side breakdown of all survey types, the guide to comparing different types of survey provides a useful reference point.

The Decision Framework: When Upgrading Is Worth It in 2026

Upgrading from a HomeBuyer Report to a Full Building Survey: When the Extra Cost Is Worth It in 2026 comes down to five key risk factors. If a property scores highly on even two or three of these, the upgrade is almost certainly justified.

1. 🏚️ Age of the Property

Properties built before 1920 were constructed using materials and methods that behave very differently from modern builds. Lime mortar, solid brick walls, slate roofs, and timber frames all require specialist knowledge to assess accurately. A HomeBuyer Report's visual-only approach can miss:

- Interstitial condensation within solid walls

- Hidden timber decay in floor joists and roof structures

- Chimney stack deterioration not visible from ground level

- Lead pipework and original drainage systems

Properties from the 1920s–1960s introduce a different set of concerns, particularly around non-standard construction (see below). Even well-maintained period homes carry inherent complexity that a Level 2 survey is not designed to fully address.

Rule of thumb: If the property was built before 1970, the upgrade conversation should start immediately.

2. 🧱 Non-Standard Construction

Standard construction in the UK means brick or stone outer walls with a timber or concrete floor structure. Anything outside this — and there is a great deal outside it — is considered non-standard. This matters enormously for survey depth.

| Construction Type | Common Issues | Survey Recommendation |

|---|---|---|

| Concrete panel (e.g. BISF, Airey, Reema) | Carbonation, reinforcement corrosion | Level 3 essential |

| Timber frame | Moisture ingress, panel deterioration | Level 3 strongly advised |

| Steel frame | Corrosion, thermal bridging | Level 3 essential |

| Thatched roof | Fire risk, vermin, deterioration | Level 3 + specialist |

| Cob or earth construction | Moisture damage, structural movement | Level 3 essential |

Many non-standard construction types are also unmortgageable or difficult to insure without a detailed structural report. In 2026, lenders remain cautious about these property types. A Level 3 survey — and in some cases a specific defect report — may be required before a mortgage offer is confirmed.

3. 🌊 Coastal and High-Exposure Locations

Properties within roughly 2–3 miles of the coast, or in exposed upland locations, face accelerated deterioration from wind-driven rain, salt spray, freeze-thaw cycles, and persistent moisture. A HomeBuyer Report will note visible surface defects, but it will not probe the extent of:

- Spalling brickwork caused by salt crystallisation

- Corroded lintels and ties within cavity walls

- Roof tile and pointing failure from wind exposure

- Window frame and sill decay from persistent moisture

In coastal areas particularly, what looks like a cosmetic issue on the surface can represent deep structural damage underneath. The additional cost of a Level 3 survey in these locations is negligible compared to the repair bills that can follow an uninformed purchase.

4. 🔨 Properties with Past Alterations

Extensions, loft conversions, garage conversions, knocked-through walls, and basement excavations are all extremely common in the UK housing stock. Each one introduces risk — particularly when carried out without proper building regulations approval or by unqualified contractors.

A HomeBuyer Report will note the presence of an extension but will not investigate whether:

- Structural calculations were properly followed

- Lintels and beams are adequately sized

- Damp-proof courses were correctly installed at the junction

- Party walls were properly managed (relevant for terraced and semi-detached properties)

In 2026, with a large proportion of UK homes having undergone some form of alteration in the past two decades, this is one of the most common reasons buyers regret not upgrading their survey level. A Full Building Survey will assess the quality and safety of alterations in detail.

5. 💷 The Price of the Property

The survey upgrade cost — typically £300–£600 more than a HomeBuyer Report — represents a tiny fraction of the property price. On a £350,000 purchase, that is less than 0.2% of the transaction value. Against potential repair costs of £10,000–£50,000 for undetected structural issues, the risk-reward calculation is straightforward.

Consider this: A buyer who saves £400 on a survey but later discovers undisclosed subsidence requiring £30,000 of underpinning has made a very poor financial decision. In tighter household budget conditions, that kind of unexpected expenditure can force a sale at a loss.

When a HomeBuyer Report Is Genuinely Sufficient

Fairness demands acknowledging that a Level 2 survey is the right choice for some buyers. The RICS Home Survey Level 2 is appropriate when:

✅ The property is a modern new-build or near-new home (post-2000) in good condition

✅ It uses standard brick-and-block construction with no unusual features

✅ There is no visible evidence of structural movement, damp, or significant defects

✅ The property has not been significantly altered

✅ It is in a sheltered, inland location with no unusual exposure

Even in these cases, buyers should consider whether a mortgage valuation alone is sufficient. As explained in the article on whether a mortgage valuation is the same as a survey, a lender's valuation is conducted purely to protect the lender — not the buyer.

The Real Cost Comparison in 2026

Upgrading from a HomeBuyer Report to a Full Building Survey: When the Extra Cost Is Worth It in 2026 requires a clear-eyed look at the numbers.

| Survey Type | Typical Cost (2026) | Depth of Inspection | Repair Cost Guidance |

|---|---|---|---|

| Mortgage Valuation | £150–£350 | Minimal | None |

| HomeBuyer Report (Level 2) | £400–£700 | Moderate | Limited |

| Full Building Survey (Level 3) | £700–£1,500+ | Comprehensive | Detailed estimates |

Costs vary by property size, location, and surveyor. London and the South East typically attract higher fees.

The price difference between a Level 2 and Level 3 survey is often £300–£600. Against the backdrop of a six-figure property purchase, this is a modest insurance premium. Buyers who have already stretched budgets to meet deposit requirements and stamp duty costs sometimes resist the upgrade — but this is precisely the situation in which an undetected defect causes the most financial damage.

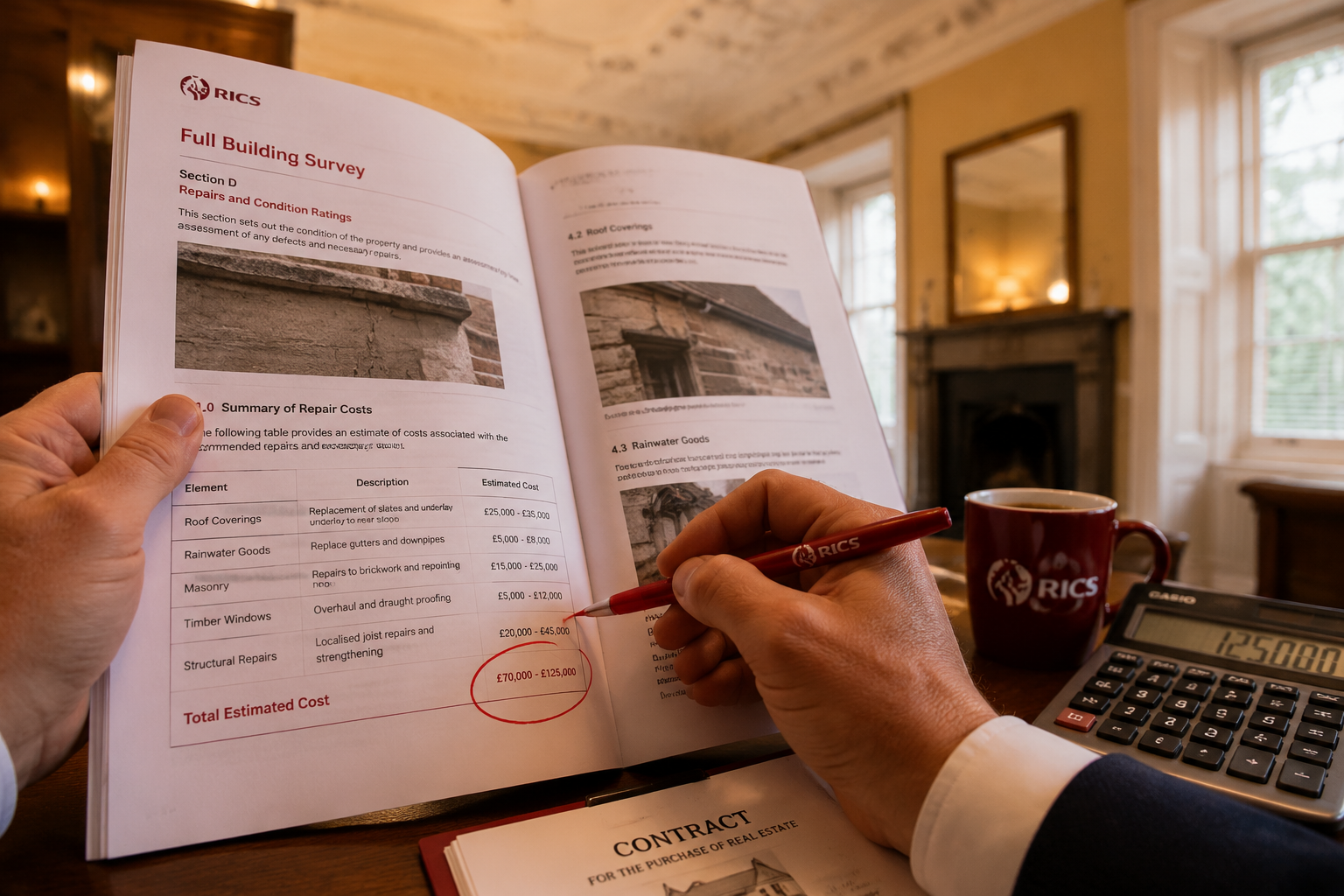

What a Full Building Survey Can Save

Consider these realistic scenarios:

- Victorian terrace with original roof: A Level 2 survey notes "some slipped tiles." A Level 3 survey reveals the entire roof structure needs replacing — estimated cost: £18,000. Buyer renegotiates £12,000 off the asking price.

- 1960s concrete panel house: A Level 2 survey gives a condition 2 rating on walls. A Level 3 survey identifies carbonation of the concrete frame — the property is unmortgageable without remediation. Buyer withdraws, saving a catastrophic purchase.

- Extended semi-detached: A Level 2 survey notes a rear extension. A Level 3 survey finds the structural beam over the knocked-through wall is undersized and showing deflection — estimated repair: £8,500. Buyer uses this to negotiate the price.

Specialist Add-Ons Worth Considering

Even a Full Building Survey has limits. For certain properties, additional specialist investigations add further protection:

- Damp surveys: Where a surveyor flags moisture concerns, a dedicated damp survey provides a detailed diagnosis and treatment plan.

- Drainage surveys: A drainage survey using CCTV cameras identifies collapsed or root-invaded drains — a common and expensive problem in older properties.

- Structural engineering: Where significant movement or alteration is identified, a structural engineering assessment provides professional calculations and remediation advice.

These add-ons typically cost £150–£400 each and are well worth commissioning when a surveyor recommends further investigation.

How to Make the Final Decision

Use this quick checklist before committing to a survey level:

Upgrade to a Full Building Survey if the property:

- Was built before 1970

- Uses non-standard construction materials

- Is in a coastal or high-exposure location

- Has had extensions, conversions, or structural alterations

- Shows any visible signs of cracking, damp, or movement

- Has been empty or poorly maintained

- Is a listed building or in a conservation area

- Has an unusual layout, mixed construction, or complex history

A HomeBuyer Report may be sufficient if the property:

- Was built after 2000 using standard construction

- Is in good visible condition with no alterations

- Has a recent building regulations completion certificate

- Is in a sheltered inland location

If in doubt, the help choosing which survey you need resource provides further guidance based on property type and buyer circumstances.

Conclusion: Make the Upgrade Decision Before, Not After

The decision about upgrading from a HomeBuyer Report to a Full Building Survey: when the extra cost is worth it in 2026 should be made at the start of the conveyancing process — not after problems emerge. In a housing market where older stock dominates, non-standard construction is widespread, and household budgets leave little room for post-purchase surprises, the Level 3 survey is one of the most cost-effective risk management tools available to any buyer.

Actionable Next Steps ✅

- Assess the property's risk profile using the checklist above before instructing any surveyor.

- Request a quote for both Level 2 and Level 3 from a RICS-accredited surveyor — the price difference is often smaller than expected.

- Ask the surveyor directly whether they would recommend an upgrade given the specific property — a good surveyor will give an honest answer.

- Commission specialist add-ons (damp, drainage, structural) if the Full Building Survey flags areas of concern.

- Use the survey findings as a negotiation tool — repair estimates in a Level 3 report provide concrete grounds for price renegotiation.

- Contact a qualified chartered surveyor to discuss the right survey level for your specific purchase before exchange of contracts.

The few hundred pounds saved by choosing a lighter survey rarely justifies the risk. In 2026, with property values high and repair costs rising, the Full Building Survey is not an extravagance — it is the sensible choice for any property that carries meaningful complexity or age.