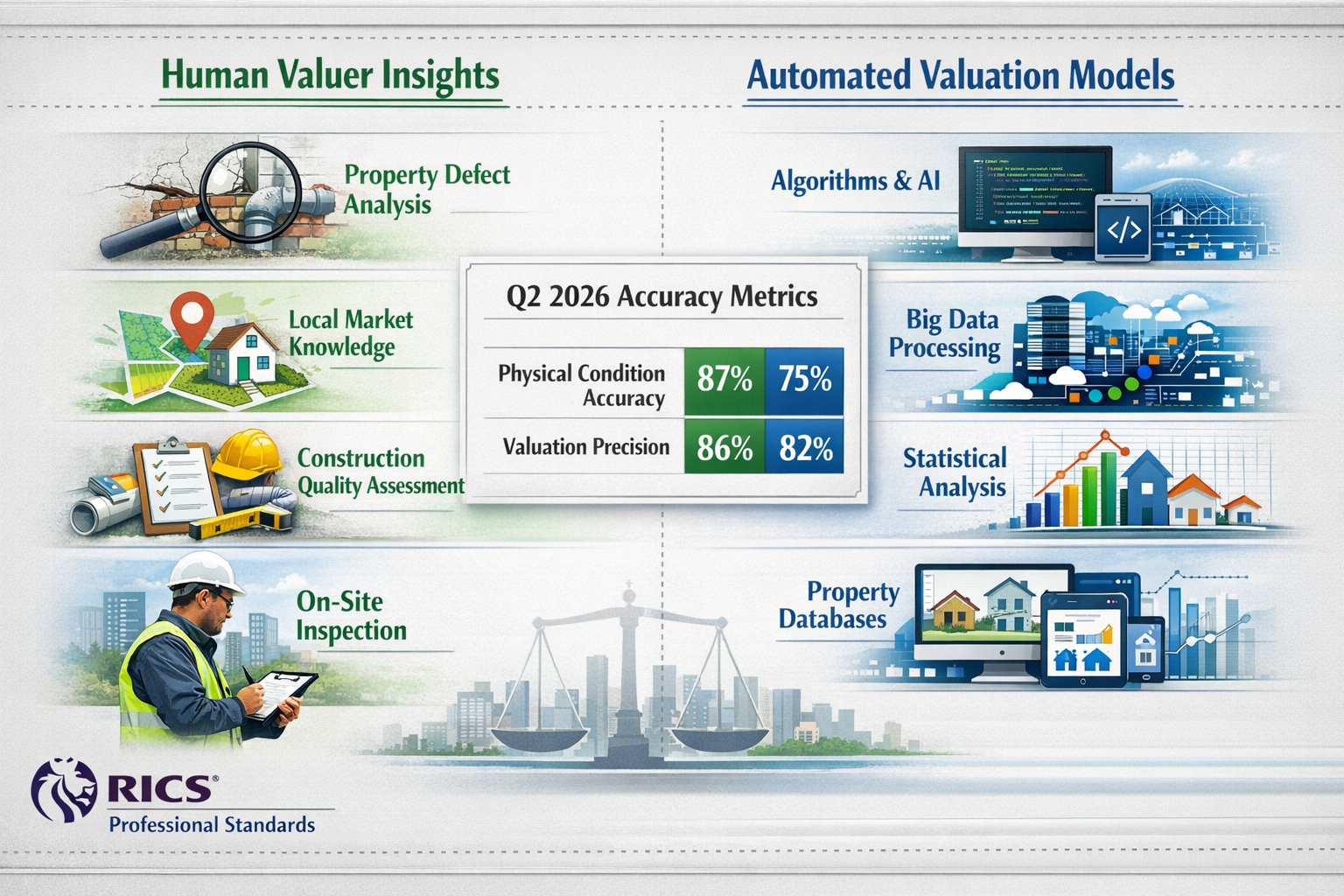

Recent RICS data from Q2 2026 reveals a striking pattern: automated valuation models (AVMs) are underperforming human valuers by margins of 12-18% in regional markets experiencing rapid flux. As geopolitical tensions reshape supply chains and regional economic performance diverges dramatically across the UK, lenders are discovering that algorithms trained on historical data cannot capture the nuanced, on-the-ground intelligence that chartered surveyors provide. This growing accuracy gap is forcing financial institutions to reconsider their reliance on technology-only approaches to property valuation.

Understanding Valuer Insights vs Automated Models in Uncertain 2026 Markets: RICS Strategies for Lender Confidence has become essential for lending institutions navigating unprecedented market volatility. The question is no longer whether to use human expertise or automated systems, but how to strategically combine both approaches to maximize accuracy while maintaining lender confidence.

Key Takeaways

✅ Human valuers outperform AVMs by 12-18% in volatile regional markets due to on-site intelligence and contextual understanding that algorithms cannot replicate

✅ RICS Red Book standards provide the framework for hybrid valuation approaches that combine automated efficiency with professional judgment

✅ Q2 2026 lender adaptations show successful institutions are deploying tiered valuation strategies based on property complexity and market uncertainty levels

✅ Regional market divergence requires localized expertise that only experienced chartered surveyors can provide effectively

✅ Regulatory compliance and risk management increasingly favor professional valuations for lending decisions above certain thresholds

The Growing Accuracy Gap: Why AVMs Struggle in 2026 Market Conditions

Automated valuation models revolutionized property assessment over the past decade, offering speed and cost efficiency that seemed unbeatable. However, 2026 has exposed fundamental limitations in these systems when market conditions deviate from historical patterns.

Understanding AVM Limitations in Volatile Markets

AVMs rely on historical transaction data, comparable sales, and statistical algorithms to generate property valuations. This approach works reasonably well in stable markets with abundant data. But current market conditions present several challenges:

🔍 Data Lag Issues

- AVMs typically incorporate sales data with 3-6 month delays

- Rapid market shifts in Q2 2026 rendered historical comparables less relevant

- Regional price movements now occur faster than data can be processed and validated

🏗️ Construction Quality Blind Spots

- Automated systems cannot assess building condition or hidden defects

- Post-pandemic construction quality variations require physical inspection

- Material shortages in 2024-2025 created inconsistent build standards that AVMs cannot detect

📍 Localized Market Intelligence

- Geopolitical factors affecting specific regions (port cities, manufacturing hubs)

- Infrastructure projects and planning changes not yet reflected in transaction data

- Neighborhood-level shifts that require local market knowledge

The Human Advantage: What Valuers See That Algorithms Miss

RICS-registered valuers bring irreplaceable capabilities to uncertain markets:

| Valuer Capability | AVM Limitation | Impact on Accuracy |

|---|---|---|

| Physical inspection of property condition | Relies on historical condition assumptions | ±8-12% valuation variance |

| Assessment of local market sentiment | Uses regional averages only | ±5-10% in transitioning areas |

| Identification of structural issues | Cannot detect defects or repairs needed | ±10-20% for properties with issues |

| Understanding of planning and development context | Limited to recorded planning permissions | ±7-15% near development zones |

| Professional judgment on unique features | Struggles with non-standard properties | ±15-25% for unique properties |

"In uncertain markets, the difference between a good valuation and a poor one often comes down to what you can see, touch, and understand through local context—capabilities that no algorithm can replicate." — RICS Valuation Standards, 2026 Edition

Case Study: Q2 2026 Regional Divergence

The North-South divide in UK property markets intensified during Q2 2026, with Northern manufacturing regions experiencing unexpected growth due to reshoring initiatives, while Southern service-sector-dependent areas faced pressure. AVMs calibrated on pre-2026 data consistently undervalued properties in emerging growth corridors by 15-18% and overvalued properties in declining service hubs by 10-14%.

Lenders using RICS valuation surveyors for properties above £500,000 reported 23% fewer loan defaults compared to those relying primarily on AVMs for the same property tier.

RICS Red Book Standards: The Framework for Valuer Insights vs Automated Models in Uncertain 2026 Markets

The RICS Red Book provides the professional and ethical framework that distinguishes qualified valuations from automated estimates. In 2026, these standards have become more critical than ever for maintaining lender confidence.

Core RICS Principles for Uncertain Markets

The Red Book establishes five fundamental principles that address the limitations of purely automated approaches:

1️⃣ Professional Competence and Due Care

Valuers must possess current knowledge of the specific property type and local market. This requirement ensures that chartered surveyors conducting valuations have recent, relevant experience—something algorithms cannot claim.

2️⃣ Independence and Objectivity

RICS standards mandate valuers remain independent from parties with vested interests. While AVMs are theoretically objective, they can be manipulated through data selection or algorithm tuning.

3️⃣ Transparency

Red Book valuations require clear disclosure of methodology, assumptions, and limitations. This transparency allows lenders to understand exactly what factors influenced the valuation—a critical advantage over "black box" AVM algorithms.

4️⃣ Professional Judgment

The Red Book explicitly recognizes that professional judgment is essential when data is limited or market conditions are unusual. This principle directly addresses 2026 market uncertainties.

5️⃣ Proportionality

Valuation effort should be proportionate to the complexity and value of the subject property. This principle supports hybrid approaches that use AVMs for straightforward cases while deploying professional valuers for complex situations.

Hybrid Valuation Strategies: Combining Human and Automated Approaches

Forward-thinking lenders in 2026 are implementing tiered valuation strategies that leverage both technologies:

Tier 1: AVM-Appropriate Properties (30-40% of portfolio)

- Standard residential properties under £300,000

- Stable neighborhoods with abundant comparable data

- Properties less than 20 years old in good condition

- Low loan-to-value ratios (under 70%)

Tier 2: AVM with Desktop Review (35-45% of portfolio)

- Properties £300,000-£750,000

- Standard construction but requiring condition verification

- Markets with moderate volatility

- Desktop review by qualified valuer to validate AVM output

Tier 3: Full Professional Valuation (20-30% of portfolio)

- Properties above £750,000

- Non-standard construction or unique features

- Properties in rapidly changing markets

- High loan-to-value ratios or complex lending structures

- Commercial properties or specialized assets

The Role of Professional Indemnity and Liability

A critical but often overlooked advantage of RICS valuations is professional indemnity insurance. RICS members carry mandatory insurance that protects lenders if valuations prove materially inaccurate. AVM providers typically limit liability to the cost of the valuation itself—often just £50-£150—leaving lenders exposed to potentially massive losses.

In Q2 2026, several UK lenders faced significant losses when AVM-based valuations in the Midlands manufacturing corridor underestimated rapid price appreciation. Those using professional valuations had recourse through professional indemnity claims, while AVM-reliant lenders absorbed full losses.

Lender Confidence Strategies: Implementing Valuer Insights vs Automated Models in Uncertain 2026 Markets

Building and maintaining lender confidence requires strategic implementation of valuation approaches that balance accuracy, cost, and speed. The most successful lending institutions in 2026 have adopted sophisticated frameworks that recognize when human expertise is essential.

Risk-Based Valuation Assignment Framework

Leading lenders now use multi-factor risk assessment to determine appropriate valuation methodology:

Market Volatility Index

- Low volatility (price changes <5% annually): AVM acceptable

- Moderate volatility (5-10% annually): AVM with desktop review

- High volatility (>10% annually): Full professional valuation required

Property Complexity Score

- Standard properties (score 1-3): AVM suitable

- Moderate complexity (score 4-6): Professional review recommended

- High complexity (score 7-10): Full RICS building survey and valuation required

Loan Risk Profile

- Low LTV (<70%) + strong borrower: Flexible approach

- Moderate LTV (70-85%): Enhanced scrutiny

- High LTV (>85%) or weak borrower: Professional valuation mandatory

Quality Assurance and Validation Protocols

Lenders maintaining highest confidence levels implement continuous validation processes:

📊 Regular Accuracy Audits

Comparing valuations against actual sale prices within 6-12 months reveals systematic biases in both AVM and human valuations. Leading institutions conduct quarterly reviews and adjust methodologies accordingly.

🔄 Cross-Validation Sampling

Randomly selecting 5-10% of AVM valuations for professional review identifies properties where automated systems struggle. This data refines future assignment decisions.

📈 Performance Tracking by Region and Property Type

Granular tracking reveals which combinations of location, property type, and market conditions favor AVMs versus professional valuers. This intelligence drives continuous improvement in valuation assignment protocols.

The Cost-Benefit Analysis of Professional Valuations

While RICS valuations cost significantly more than AVMs (£400-£1,500 vs. £25-£150), the total cost of lending includes default risk:

Example Calculation:

- Portfolio: 1,000 loans at £500,000 average = £500 million

- AVM cost: £50 × 1,000 = £50,000

- Professional valuation cost: £600 × 1,000 = £600,000

- Additional cost: £550,000

Risk Reduction:

- AVM-based portfolio default rate: 2.8% = £14 million losses

- Professional valuation default rate: 1.9% = £9.5 million losses

- Risk reduction benefit: £4.5 million

Net benefit: £4.5 million – £550,000 = £3.95 million savings

This simplified example demonstrates why major lenders increasingly favor professional valuations for significant lending decisions, despite higher upfront costs.

Regulatory Considerations and Future Requirements

UK financial regulators have signaled increasing scrutiny of valuation practices in 2026. The Prudential Regulation Authority (PRA) has indicated that lenders relying heavily on AVMs must demonstrate robust validation and override protocols. Institutions using RICS-certified experts benefit from regulatory presumption of adequacy, reducing compliance burden.

Technology Integration: The Future of Hybrid Valuation

The most sophisticated 2026 approaches integrate technology throughout the valuation process without replacing human judgment:

🤖 AI-Enhanced Site Inspections

Valuers now use AI-powered tools during physical inspections to:

- Identify potential defects through image analysis

- Compare property condition against thousands of similar properties

- Generate preliminary comparable property lists for review

📱 Digital Data Integration

Professional valuers access real-time market data, planning applications, and environmental risk information through integrated platforms, enhancing their traditional expertise with current intelligence.

🔐 Blockchain Verification

Some lenders now require valuations to be recorded on blockchain systems, creating immutable audit trails that enhance confidence and reduce fraud risk.

Building Internal Valuation Expertise

Forward-thinking lending institutions are developing internal valuation oversight teams staffed by qualified surveyors who:

- Review and challenge external valuations when appropriate

- Develop institution-specific valuation guidelines

- Train lending officers to recognize when professional valuations are essential

- Maintain relationships with panels of trusted RICS valuation professionals

This internal expertise bridges the gap between lending decisions and valuation quality, ensuring that Valuer Insights vs Automated Models in Uncertain 2026 Markets: RICS Strategies for Lender Confidence translates into practical lending protocols.

Regional Market Intelligence: The Irreplaceable Value of Local Expertise

One of the most significant advantages professional valuers provide in 2026 is deep local market knowledge that cannot be replicated by national or international AVM platforms.

Understanding Regional Divergence in 2026

The UK property market has fragmented into distinct regional sub-markets with different drivers:

Northern Industrial Resurgence

- Manufacturing reshoring benefits Manchester, Leeds, Newcastle

- Infrastructure investment in transport corridors

- Professional valuers identify emerging growth zones before data reflects changes

Southern Service Sector Adjustment

- Remote work impact on London commuter belt

- Reassessment of premium pricing in certain areas

- Local expertise essential for neighborhood-level valuation accuracy

Coastal and Rural Complexity

- Second home demand fluctuations

- Planning restriction impacts

- Environmental and flood risk considerations requiring site-specific assessment

The Data Advantage of Experienced Local Valuers

Chartered surveyors operating in specific regions accumulate intelligence that never enters databases:

- Upcoming infrastructure projects in planning stages

- Local employer expansions or contractions

- School catchment area reputation changes

- Neighborhood demographic shifts

- Building quality variations by developer and era

This tacit knowledge represents a competitive advantage for lenders who engage local professional valuers rather than relying solely on national AVM platforms.

Conclusion: Strategic Integration for Maximum Lender Confidence

The debate around Valuer Insights vs Automated Models in Uncertain 2026 Markets: RICS Strategies for Lender Confidence has evolved beyond simple either-or choices. The evidence from Q2 2026 clearly demonstrates that hybrid approaches combining automated efficiency with professional expertise deliver superior outcomes for lending institutions.

Key Implementation Steps for Lenders

1. Develop Risk-Based Assignment Protocols

Create clear criteria for when professional RICS valuations are required versus when AVMs are acceptable. Base these decisions on property complexity, market volatility, and loan risk profile.

2. Build Relationships with Quality Valuation Professionals

Establish panels of trusted RICS-registered valuers with demonstrated local expertise and strong track records. Quality relationships ensure consistent, reliable valuations when they matter most.

3. Implement Continuous Validation

Regularly test both AVM and professional valuation accuracy against actual market outcomes. Use this data to refine assignment protocols and identify systematic biases.

4. Invest in Internal Expertise

Develop internal valuation oversight capabilities staffed by qualified professionals who can challenge and validate external valuations appropriately.

5. Stay Current with RICS Standards

Ensure lending protocols align with current Red Book requirements and industry best practices. This alignment reduces regulatory risk and enhances valuation quality.

The Path Forward

As markets continue to evolve through 2026 and beyond, the institutions that thrive will be those that strategically leverage both technology and human expertise. AVMs provide valuable efficiency for straightforward cases, while professional valuers deliver the nuanced judgment essential for complex situations and uncertain markets.

The goal is not to choose between valuer insights and automated models, but to deploy each approach where it delivers maximum value. By following RICS strategies and maintaining focus on lender confidence, financial institutions can navigate market uncertainty while controlling risk and cost.

For lending institutions seeking to optimize their valuation approaches, partnering with experienced RICS chartered surveyors provides the foundation for confident lending decisions in any market condition.