{"cover":"Professional landscape format (1536×1024) hero image featuring bold text overlay 'Valuing Properties in a 2% House Price Growth Market' in extra large 72pt white sans-serif font with dark gradient shadow, positioned center-upper third. Background shows split-screen composition: left side displays modern UK terraced houses with 'SOLD' signs in northern England setting, right side shows southern England Victorian properties with price tags, overlaid with transparent upward-trending 2% growth chart line and regional UK map heat zones in blue and orange. Color scheme: navy blue, white, gold accents. Magazine cover quality, editorial style, high contrast, professional real estate aesthetic with subtle data visualization elements.","content":["Detailed landscape format (1536×1024) image showing professional RICS-qualified surveyor in business attire holding digital tablet displaying property valuation software, standing in front of semi-detached UK property with clipboard. Foreground features transparent overlay of comparative market analysis spreadsheet with columns showing recent sales data, adjustment factors, and 2% growth calculations. Background shows row of similar properties for comparison context. Includes visual elements: magnifying glass icon over property details, percentage adjustment markers (+5%, -3%), and subtle northern England architectural features. Clean, professional composition with natural lighting, documentary photography style, business editorial quality.","Detailed landscape format (1536×1024) infographic-style image displaying UK map with distinct color-coded regions showing North-South property value divide. Northern regions (Manchester, Leeds, Newcastle) highlighted in cool blue tones with lower price markers (£200k-£300k average), Southern regions (London, Sussex, St Albans) in warm orange-red tones with higher price markers (£500k-£700k average). Center features large '150-200%' premium text with upward arrow. Includes data visualization elements: bar charts comparing regional prices, wage growth indicators, mortgage rate impact zones, and stamp duty threshold markers. Modern infographic aesthetic with clean typography, professional color palette, editorial data visualization quality.","Detailed landscape format (1536×1024) image showing modern surveyor's office workspace with large monitor displaying Red Book valuation software interface, property comparison charts, and April 2026 revaluation deadline calendar prominently visible. Desk features printed RICS valuation reports, mortgage documents, and calculator showing conservative valuation figures. Background wall displays framed professional certifications and regional property market trend graphs with 2% growth projection line. Includes visual elements: sticky notes with adjustment factors, coffee cup, professional surveying equipment, and tablet showing property photographs. Warm professional lighting, contemporary office aesthetic, business documentary photography style, high-quality editorial composition."]

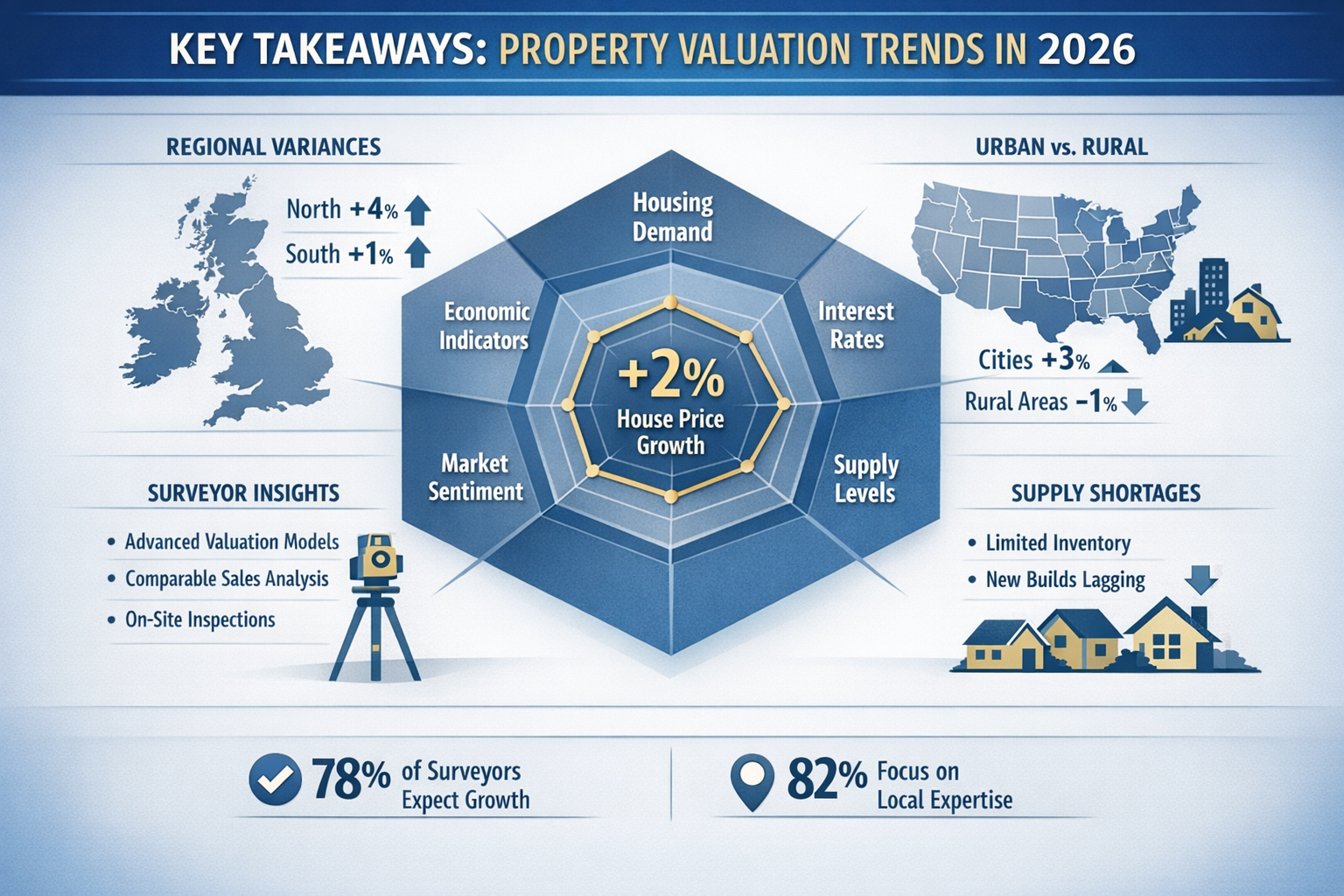

The UK property market enters 2026 with cautious optimism. Rightmove forecasts a modest 2% house price growth this year, with northern regions showing unexpected strength while southern markets face headwinds from new taxation measures. For property buyers, sellers, and investors, understanding how chartered surveyors adjust their valuations in this evolving landscape has never been more critical. Valuing Properties in a 2% House Price Growth Market: Surveyor Adjustments for 2026 Regional Forecasts requires sophisticated techniques that account for regional disparities, wage growth patterns, mortgage rate fluctuations, and stamp duty impacts on buyer negotiations.

The days of straightforward property valuations based solely on recent comparable sales are fading. Today's surveyors must navigate unprecedented regional divides, conservative lending practices embedded since the 2023-2024 volatility, and new government wealth taxation measures affecting properties over £2 million. This comprehensive guide explores how professional valuers adapt their methodologies to deliver accurate assessments in a market where a 2% national average masks dramatic regional variations.

Key Takeaways

- Conservative valuations are now permanent practice: Surveyors prioritize downside risk protection over optimistic assessments, even as mortgage rates stabilize, creating potential gaps between market expectations and formal valuations.

- Regional disparities demand specialized adjustment techniques: Southern properties command 150-200% premiums over comparable northern homes, requiring surveyors to apply sophisticated regional adjustment factors when selecting comparables.

- Mortgage valuations consistently lag market values: Lenders adopt defensive assumptions to protect against default risk across full mortgage terms, meaning formal valuations often come in below current market prices.

- RICS-qualified surveyors remain the gold standard: Professional competence, local knowledge, and adherence to strict ethical standards make chartered surveyors essential for accurate property assessments in 2026's complex market.

- April 2026 revaluation deadline drives methodology updates: Surveyors must carefully adjust comparables for market movements and new taxation impacts as regulatory deadlines approach.

Understanding the 2026 Market Context for Property Valuations

The 2% Growth Forecast and Regional Variations

Rightmove's prediction of 2% house price growth for 2026 represents a national average that conceals significant regional complexity. Northern regions—particularly areas around Manchester, Leeds, and Newcastle—are experiencing stronger demand driven by relative affordability and improved wage growth. Meanwhile, southern markets face pressure from new taxation measures targeting high-value properties.

This regional divide creates unprecedented challenges for surveyors practicing Valuing Properties in a 2% House Price Growth Market: Surveyor Adjustments for 2026 Regional Forecasts. A three-bedroom semi-detached property in northern England might see 3-4% annual growth, while a comparable property in Sussex or St Albans experiences flat or negative growth due to affordability constraints.

Key regional factors influencing 2026 valuations:

- 🏘️ Northern strength: Wage growth outpacing southern regions, improved transport links, and corporate relocations

- 📉 Southern headwinds: High-value property taxation, affordability ceilings, and limited first-time buyer access

- 💷 Stamp duty effects: Transaction costs disproportionately affecting mid-range properties in southern markets

- 🏢 Hybrid working impacts: Continued demand for space outside traditional commuter zones

The Permanent Shift to Conservative Valuations

Following the market volatility of 2023-2024, surveyors have embedded defensive practices into their professional methodology. This represents a permanent shift rather than a temporary response to uncertain conditions[1]. Even as mortgage rates ease from their recent peaks, valuers continue prioritizing downside risk protection.

This conservative approach affects multiple property categories:

| Property Type | Valuation Impact | Surveyor Adjustment |

|---|---|---|

| High-value residential (£2M+) | Significant downward pressure | 10-15% discount to market expectations |

| Non-standard construction | Enhanced scrutiny | 15-20% conservative adjustment |

| Rural locations | Limited comparable evidence | 8-12% caution premium |

| Buy-to-let properties | Rental yield focus | Income-based valuation floor |

Professional surveyors now distinguish between saleability and value—what a property might achieve in today's market versus what lenders should advance against it across a full mortgage term[1]. This separation creates valuation gaps that can frustrate buyers and sellers expecting assessments aligned with current listing prices.

High-Value Property Tax Impacts

The 2026 budget introduced new government fees for homes valued over £2 million as part of wealth taxation measures[4]. This policy change significantly affects valuation expectations in premium locations, particularly Central London, Fulham, and Richmond.

Surveyors must now factor these taxation impacts into their assessments, considering:

- Reduced buyer pools: Fewer purchasers willing to exceed the £2M threshold

- Negotiation leverage: Buyers using tax liability as negotiation tool

- Comparable selection: Difficulty finding recent sales reflecting post-budget conditions

- Investment value: Reduced attractiveness for portfolio investors

Properties valued at £1.8-£2.2 million face particular challenges, as buyers seek to negotiate below the taxation threshold while sellers resist price reductions that would trigger significant equity losses.

Surveyor Methodologies for Valuing Properties in a 2% House Price Growth Market

Comparative Market Analysis: The Dominant Approach

UK valuers rely primarily on comparative market analysis (CMA), examining comparable sales from the past three to six months and adjusting for differences in size, condition, features, and location[2]. This method works effectively when sufficient recent comparable sales exist and market conditions remain relatively stable.

The CMA process for 2026 valuations:

- Identify comparable properties: Select 3-5 recent sales within 0.5-1 mile radius

- Apply adjustment factors: Modify comparable values for differences (size, condition, features)

- Weight by relevance: Prioritize most similar properties and recent transactions

- Apply market trend adjustments: Factor in 2% growth trajectory and regional variations

- Consider unique characteristics: Account for property-specific features affecting value

However, CMA faces significant challenges in 2026's fragmented market. Many surveyors work with restricted recent sales data, particularly for higher-value, non-standard, or regional properties[1]. Where comparables are thin, surveyors default to caution, creating valuation gaps that can feel disconnected from buyer expectations.

Regional Adjustment Techniques for North-South Divides

The unprecedented 150-200% premium southern properties command over comparable northern properties represents the most significant challenge for Valuing Properties in a 2% House Price Growth Market: Surveyor Adjustments for 2026 Regional Forecasts[3]. Surveyors must apply sophisticated regional adjustment factors when comparables cross regional boundaries.

Regional adjustment framework:

Northern regions (Manchester, Leeds, Newcastle):

- Base wage growth adjustment: +2.5% to +3.5% annually

- Affordability premium: Properties under £300k seeing strongest demand

- Infrastructure investment factor: Transport improvements adding 5-8% value

- Corporate relocation impact: Major employers driving localized growth

Southern regions (London, Surrey, Sussex):

- Taxation drag: Properties near £2M threshold facing 5-10% discount

- Affordability ceiling: Limited buyer pools above £600k in commuter zones

- Wage stagnation adjustment: Flat real wage growth constraining demand

- Stamp duty impact: Transaction costs reducing effective values by 3-5%

Professional surveyors practicing in areas like North London or Battersea must carefully document these regional adjustments in their valuation reports to justify valuations that may differ significantly from seller expectations.

Mortgage Rate and Affordability Calculations

Mortgage rates significantly influence property valuations in 2026, even as rates stabilize from recent peaks. Surveyors must consider affordability constraints when assessing value, particularly for properties dependent on mortgage financing rather than cash purchases.

Affordability-based valuation adjustments:

- Income multiple limits: Properties priced beyond 4.5x median household income face demand constraints

- Monthly payment thresholds: Values adjusted to keep mortgage payments within 30-35% of gross income

- Stress testing: Lenders requiring affordability at rates 2-3% above current levels

- Deposit requirements: Higher deposits for properties above £500k limiting buyer pools

For example, a property in Epsom valued at £550,000 requires a £55,000 deposit (10%) and household income of approximately £110,000 to secure mortgage approval. If local median household income is £65,000, the surveyor must consider reduced demand from local buyers and adjust valuation accordingly.

This affordability-focused approach differs from traditional valuation methods that emphasized comparable sales without considering buyer financing capacity. It's particularly relevant for RICS Homebuyer Surveys where lenders require conservative assessments.

Wage Growth and Local Economic Indicators

Regional wage growth patterns significantly influence property valuations in 2026. Surveyors increasingly incorporate local economic indicators into their assessments, recognizing that sustainable property values depend on local earning capacity.

Economic indicators affecting valuations:

- 📊 Wage growth rates: Northern regions showing 3-4% annual wage growth vs. 1-2% in southern regions

- 🏢 Employment stability: Major employer presence and sector diversity

- 🚆 Infrastructure investment: Transport improvements and connectivity enhancements

- 🎓 Education quality: School ratings affecting family home premiums

- 🏪 Retail and amenity access: Local services supporting property desirability

Surveyors in areas like Harrow or Hemel Hempstead must balance national 2% growth forecasts against local economic conditions that may drive significantly different outcomes.

Stamp Duty Impact on Buyer Negotiations

Stamp duty remains a significant transaction cost affecting property valuations in 2026. The tax structure creates threshold effects where properties priced just above band thresholds face reduced demand as buyers seek to negotiate below these levels.

Current stamp duty thresholds (England & Northern Ireland):

- £0 – £250,000: 0%

- £250,001 – £925,000: 5%

- £925,001 – £1.5 million: 10%

- £1.5 million+: 12%

Properties priced at £260,000, £950,000, or £1.6 million face particular negotiation pressure as buyers attempt to reduce purchase prices below threshold levels. Surveyors must consider this negotiation dynamic when assessing market value, particularly in areas like Weybridge or Godalming where many properties cluster around these thresholds.

Additional stamp duty considerations:

- Second home surcharge: Additional 3% on buy-to-let and second homes

- First-time buyer relief: Exemption up to £425,000 (£625,000 in some regions)

- Non-resident surcharge: Additional 2% for overseas buyers

- Corporate purchases: Higher rates for company acquisitions

Professional Standards and Best Practices for 2026 Valuations

RICS Qualification and Professional Competence

RICS-qualified surveyors represent the gold standard for UK property valuations in 2026[2]. The Royal Institution of Chartered Surveyors maintains rigorous professional standards requiring:

- ✅ Comprehensive training and examination

- ✅ Continuing professional development (CPD)

- ✅ Adherence to RICS Red Book valuation standards

- ✅ Professional indemnity insurance

- ✅ Ethical conduct and independence

Lenders and solicitors typically require RICS-qualified valuations for mortgage and legal purposes. When commissioning a RICS Building Survey or valuation report, clients should verify the surveyor's RICS membership and relevant experience.

"Understanding neighbourhood nuances significantly impacts assessment quality. Local knowledge improves comparable selection and adjustment judgements, making valuation accuracy highly dependent on surveyor expertise." – Property Valuation UK Guide 2026[2]

The Importance of Local Knowledge and Experience

Valuer experience and local knowledge critically impact assessment quality in 2026's complex market. Surveyors practicing in specific areas like Putney, Barnes, or Kilburn develop deep understanding of:

- Micro-market variations: Street-by-street value differences

- Development pipeline: Planned infrastructure affecting future values

- School catchment premiums: Education-driven demand patterns

- Historical price trends: Long-term value trajectories

- Buyer demographics: Typical purchaser profiles and preferences

This local expertise enables more accurate comparable selection and adjustment calculations, particularly in areas experiencing rapid change or where recent sales data is limited.

Distinguishing Mortgage Valuations from Market Valuations

A critical concept for 2026 property transactions is understanding that mortgage valuations differ from market valuations. Lenders adopt conservative assumptions to protect against default risk, meaning mortgage valuations often come in below market valuations for the same property[2].

Key differences:

| Aspect | Market Valuation | Mortgage Valuation |

|---|---|---|

| Purpose | Estimate likely sale price | Determine lending security |

| Timeframe | Current market conditions | Full mortgage term (25-30 years) |

| Risk perspective | Balanced assessment | Conservative/defensive |

| Comparable weighting | Recent sales emphasized | Sustainable values prioritized |

| Adjustment factors | Current demand conditions | Downside risk protection |

This gap widens in uncertain or volatile conditions. Properties in premium locations like Leatherhead or Esher may achieve strong sale prices but receive lower mortgage valuations due to lender caution about sustaining these values across multi-decade mortgage terms.

April 2026 Revaluation Deadline Considerations

Surveyors must carefully adjust comparables for market movements as the April 2026 revaluation deadline approaches[5]. This regulatory date is driving updated valuation methodology reviews across the surveying profession.

Deadline-driven considerations:

- Time-adjusted comparables: Applying monthly adjustment factors to sales from earlier periods

- Forward-looking assessments: Incorporating anticipated post-deadline market conditions

- Documentation requirements: Enhanced justification for adjustment factors and methodology

- Quality assurance: Additional review processes for valuations near deadline

Professional surveyors are updating their comparable databases and adjustment frameworks to ensure compliance with revised standards while maintaining accuracy in their assessments.

Limited Comparable Evidence and Fragmented Markets

Many surveyors work with restricted recent sales data, particularly for higher-value, non-standard, or regional properties[1]. This challenge is especially acute in areas like Bromley or Oxfordshire where property types vary significantly.

Strategies for limited comparable situations:

- Expand geographic search radius: Include sales from adjacent areas with adjustment factors

- Extend time period: Use older comparables with time-adjustment calculations

- Alternative property types: Consider similar-sized properties with different configurations

- Income approach: Apply rental yield calculations for investment properties

- Cost approach: Assess land value plus construction costs for unique properties

Where comparables remain insufficient, surveyors default to caution, applying conservative adjustments that protect lenders and clients from overvaluation risk. This defensive approach can create frustration for sellers expecting valuations aligned with optimistic market conditions.

The Role of Property Presentation in Valuations

While strong property presentation can play an indirect role in achieving sale prices, surveyors in 2026 remain focused on facts, figures, and recent sales data rather than staging presentation[6]. Professional valuers assess:

- Structural condition: Building integrity and maintenance quality

- Specification level: Fixtures, fittings, and finish quality

- Layout efficiency: Practical space utilization and flow

- Energy performance: EPC ratings and sustainability features

- Compliance status: Building regulations and necessary certifications

Home staging may help properties achieve quicker sales or attract more offers, but it does not directly influence formal surveyor valuations. Buyers commissioning RICS valuations should understand that cosmetic presentation has minimal impact on the professional assessment.

Practical Applications: Valuing Different Property Types

High-Value Residential Properties (£2M+)

Properties exceeding £2 million face unique valuation challenges in 2026 due to new taxation measures and limited buyer pools. Surveyors must apply specialized techniques when valuing high-value properties:

High-value property adjustments:

- Taxation impact discount: 5-15% reduction reflecting buyer tax liability

- Limited comparable pool: Fewer recent sales requiring broader search parameters

- Unique feature premiums: Swimming pools, home cinemas, extensive grounds

- Location specificity: Prime location premiums vs. secondary location discounts

- International buyer factors: Currency fluctuations and overseas buyer surcharges

Areas like Camden and North West London contain significant high-value property stock requiring specialized valuation expertise.

Buy-to-Let and Investment Properties

Investment property valuations in 2026 must account for landlord tax pressures reducing rental supply[4]. Surveyors apply income-based valuation methods alongside traditional comparable analysis:

Investment property valuation factors:

- Gross rental yield: Annual rent as percentage of property value

- Net yield calculations: Accounting for maintenance, management, and tax costs

- Tenant demand: Local rental market strength and void period risks

- Regulatory compliance: EPC requirements and licensing costs

- Exit strategy: Resale potential to owner-occupiers vs. investors

Professional surveyors conducting commercial property valuations or rent reviews must balance current rental income against capital value trends in a market where fewer landlords compete for tenants.

Non-Standard Construction Properties

Properties featuring non-standard construction methods face enhanced scrutiny in 2026 valuations. Surveyors apply significant caution premiums for:

- Concrete construction: Pre-cast concrete or large panel systems

- Steel frame buildings: Particularly older steel-framed properties

- Timber frame: Where not built to modern standards

- Thatched roofs: Specialist insurance and maintenance requirements

- Listed buildings: Restrictions on modifications and higher maintenance costs

These properties typically receive 15-20% conservative adjustments due to limited buyer pools and mortgage availability challenges. Buyers should commission specialist surveys to identify construction-related risks before purchase.

Rural and Isolated Properties

Rural properties face unique valuation challenges due to limited comparable evidence and specific buyer requirements. Surveyors must consider:

- Access and services: Road quality, utilities availability, broadband connectivity

- Land value: Agricultural land, gardens, woodland, and development potential

- Maintenance costs: Septic tanks, private water supplies, heating systems

- Buyer pool limitations: Reduced demand from lifestyle vs. practical buyers

- Local employment: Commuting distances and remote working suitability

Rural properties typically receive 8-12% caution premiums reflecting these additional risks and limited resale markets.

Conclusion

Valuing Properties in a 2% House Price Growth Market: Surveyor Adjustments for 2026 Regional Forecasts requires sophisticated professional expertise that balances national growth predictions against unprecedented regional variations, conservative lending practices, and new taxation impacts. The modest 2% national growth forecast masks dramatic differences between northern regions showing 3-4% growth and southern markets facing flat or negative trends.

Professional RICS-qualified surveyors have permanently embedded defensive practices into their valuation methodologies, prioritizing downside risk protection over optimistic assessments even as mortgage rates stabilize. This conservative approach creates potential gaps between seller expectations and formal valuations, particularly for high-value properties, non-standard construction, and properties in fragmented markets with limited comparable evidence.

The unprecedented 150-200% premium southern properties command over comparable northern homes demands sophisticated regional adjustment techniques that account for wage growth patterns, affordability constraints, stamp duty threshold effects, and local economic indicators. Surveyors must distinguish between what properties might achieve in today's market and what lenders should advance against them across full mortgage terms.

Actionable Next Steps

For property buyers:

- Commission RICS Building Surveys from locally experienced chartered surveyors

- Understand that mortgage valuations typically come in below market valuations

- Factor regional economic indicators and wage growth into purchase decisions

- Consider stamp duty threshold effects when negotiating purchase prices

For property sellers:

- Set realistic price expectations accounting for conservative valuation practices

- Provide comprehensive documentation supporting property value claims

- Address maintenance issues before formal valuations

- Consider timing sales to avoid threshold effects

For property investors:

- Focus on rental yield calculations alongside capital value assessments

- Account for landlord taxation impacts on net returns

- Prioritize regions with strong wage growth and employment stability

- Commission professional valuations before acquisition

The 2026 property market rewards informed participants who understand how professional surveyors adjust their methodologies for regional variations, market conditions, and regulatory requirements. By working with experienced RICS-qualified surveyors and understanding the factors influencing contemporary valuations, buyers, sellers, and investors can navigate this complex landscape successfully.

References

[1] Mortgage Valuations In 2026 Why Surveyors Are Still Cautious Even As Rates Ease – https://www.willowprivatefinance.co.uk/mortgage-valuations-in-2026-why-surveyors-are-still-cautious-even-as-rates-ease

[2] Property Valuation Explained Uk Guide 2026 – https://kefihub.co.uk/trending/property-valuation-explained-uk-guide-2026/

[3] Valuation Techniques For Widening North South Divides Rics Adjustments For 2026 Regional Price Gaps – https://nottinghillsurveyors.com/blog/valuation-techniques-for-widening-north-south-divides-rics-adjustments-for-2026-regional-price-gaps

[4] The 2026 Property Reset Market Forecasts Budget Impacts Investor Focus – https://surveyingcorp.com/2025/12/the-2026-property-reset-market-forecasts-budget-impacts-investor-focus/

[5] Post Budget 2026 Valuation Challenges Surveyor Strategies For High Value Properties Over 2 Million – https://nottinghillsurveyors.com/blog/post-budget-2026-valuation-challenges-surveyor-strategies-for-high-value-properties-over-2-million

[6] Does Home Staging Affect Property Valuations What Surveyors Say In 2026 – https://londonhomeexpert.co.uk/does-home-staging-affect-property-valuations-what-surveyors-say-in-2026/