The UK property market in 2026 presents a unique challenge: prices have stabilized after years of volatility, yet subtle signals suggest the market is beginning to turn. For buyers, sellers, and investors navigating this "flat but turning" landscape, understanding how UK surveyors value properties in a 'flat but turning' market: 2026 methods explained for buyers, sellers and investors has never been more critical. With average UK house prices standing at approximately £271,000 and forecasters predicting 2.5% growth by Q4 2026, the accuracy of property valuations can mean the difference between securing a fair deal and leaving thousands of pounds on the table[5].

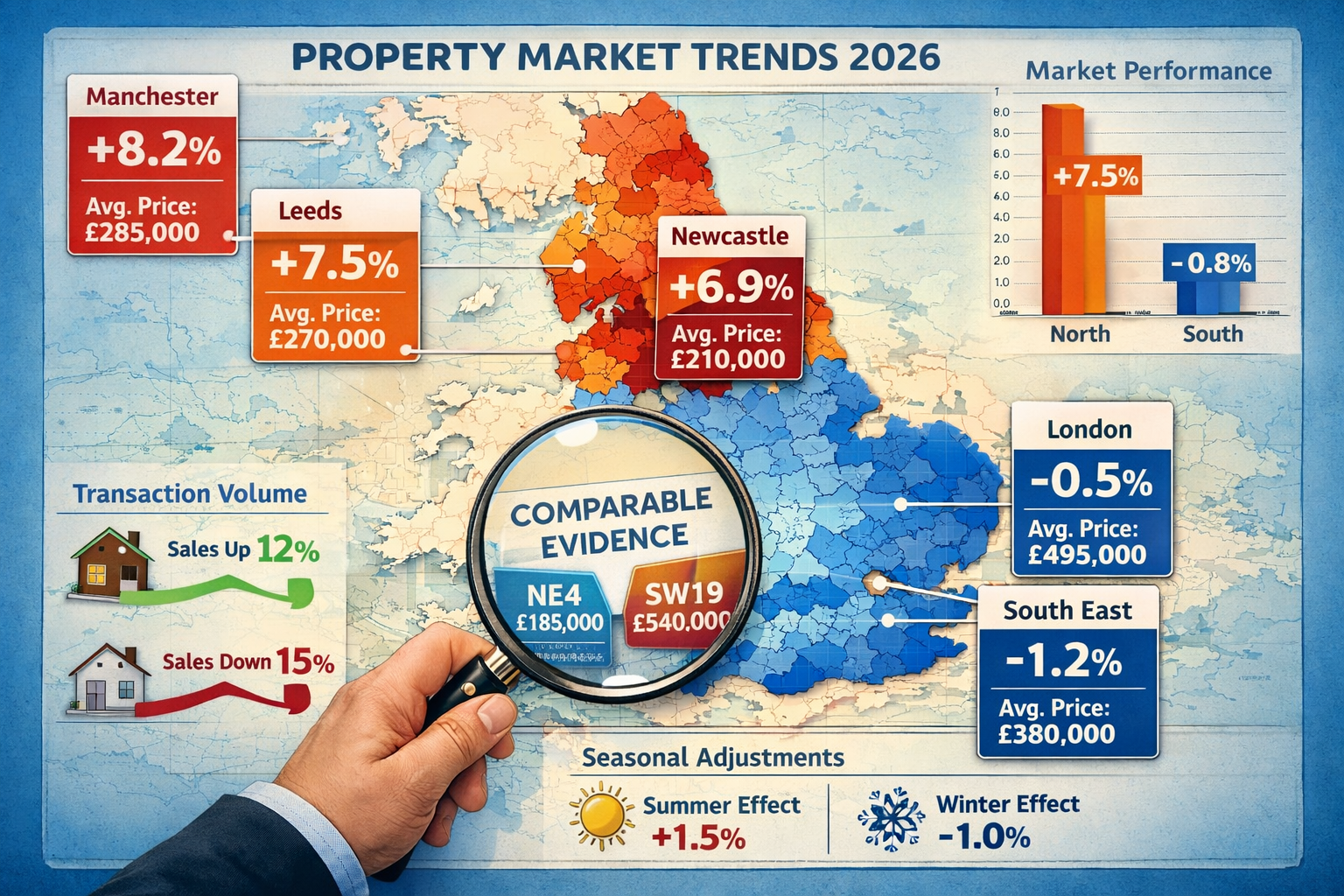

RICS chartered surveyors face particular complexities in 2026's stabilizing market. Regional disparities have intensified—the Midlands and North demonstrate stronger growth trajectories while southern markets remain subdued—creating challenges for comparable evidence selection. Limited transaction volumes in certain areas compound these difficulties, while shifting buyer sentiment and landlord tax pressures further complicate valuation adjustments. This comprehensive guide explores the methodologies professional surveyors employ to deliver accurate valuations despite these market uncertainties.

Key Takeaways

- Three distinct valuation approaches serve different purposes in 2026: automated online valuations (70-85% accuracy), free estate agent valuations (combining inspection with market analysis), and formal RICS Red Book valuations (£324-£473, essential for legal purposes)[1]

- Regional market variations require surveyors to adjust comparable evidence significantly, with northern regions showing 2.5% growth while southern markets remain flat, demanding sophisticated local knowledge[5]

- Limited comparable evidence in stabilizing markets forces surveyors to employ advanced adjustment techniques, accounting for property condition, location premiums, and market sentiment shifts

- Rental market pressures directly impact capital valuations in 2026, with landlord tax changes affecting investment property assessments and yield calculations[4]

- Fresh valuations are essential—assessments older than six months fail to reflect 2026's increased supply and shifted buyer behavior, potentially costing buyers or sellers significant amounts[1]

Understanding the Three Primary Valuation Methods in 2026's Market

How UK surveyors value properties in a 'flat but turning' market: 2026 methods explained for buyers, sellers and investors begins with understanding the three distinct valuation approaches available. Each serves specific purposes and delivers varying levels of accuracy and detail.

Automated Valuation Models (AVMs): Speed vs. Accuracy

Instant online valuations have become increasingly sophisticated in 2026, with advanced AI systems demonstrating over 96% accuracy in ideal conditions. However, typical AVM accuracy remains at 70-85% in real-world applications[1]. This margin of error can represent tens of thousands of pounds—a critical consideration in a flat market where pricing precision matters.

AVMs analyze:

- Historical sales data from Land Registry records

- Current market listings and asking prices

- Property characteristics (bedrooms, bathrooms, square footage)

- Postcode-level price trends

- Seasonal adjustment factors

Key limitations in 2026's market:

- Cannot assess property condition or unique features

- Struggle with properties in areas with limited transaction data

- Fail to account for micro-location premiums (specific streets or views)

- Miss recent market sentiment shifts that haven't yet appeared in transaction data

💡 Best used for: Initial research, tracking your property's approximate value over time, or getting a ballpark figure before engaging professional valuers.

Estate Agent Valuations: Free Professional Assessment

Estate agent valuations represent the middle ground, combining physical inspection with market expertise. These remain completely free with no obligation in 2026, making them accessible for sellers exploring their options[1].

What estate agents assess:

- Physical property condition and presentation

- Unique features and selling points

- Comparable properties currently on the market

- Recent sales in the immediate area

- Local market demand and buyer preferences

- Seasonal factors affecting the specific location

Critical consideration: In a flat market, some agents inflate valuations to win business. Industry experts recommend obtaining at least three valuations to verify accuracy and identify outliers[1]. When comparing valuations, look for agents who provide detailed comparable evidence rather than optimistic estimates.

To find experienced professionals in your area, explore options for chartered surveyors across different regions who understand local market nuances.

RICS Red Book Valuations: The Gold Standard

Formal RICS valuations represent the highest professional standard, costing £324-£473 in 2026[1]. These certified assessments follow strict Red Book standards and are conducted by RICS registered valuers who maintain professional indemnity insurance and adhere to rigorous methodologies.

When RICS valuations are essential:

- Help to Buy scheme purchases

- Shared Ownership properties

- Probate and estate settlement

- Divorce proceedings and matrimonial settlements

- Properties with complex legal issues

- Secured lending and remortgaging

- Investment portfolio assessments

RICS valuations provide legally defensible figures backed by comprehensive comparable evidence and professional judgment. In a turning market, this professional accountability becomes invaluable. For those requiring formal assessments, understanding which survey you need helps ensure you commission the appropriate level of service.

How Surveyors Navigate Regional Variations in 2026's Flat but Turning Market

The "flat but turning" characterization of 2026's market masks significant regional disparities that fundamentally affect how UK surveyors value properties. Understanding these geographical variations is crucial for buyers, sellers and investors making informed decisions.

The North-South Divide: Adjusting Comparables Across Regions

Market forecasts predict the Midlands and North will lead growth in 2026, while southern markets—particularly London and the Southeast—experience continued price stagnation[5]. This divergence creates specific challenges for surveyors selecting and adjusting comparable evidence.

Regional performance indicators (2026):

| Region | Expected Growth | Key Drivers | Valuation Challenges |

|---|---|---|---|

| North West | 2.5-3.0% | Affordability, employment growth | Limited luxury comparables |

| Yorkshire | 2.5-3.0% | Strong regional economy | Rural property evidence gaps |

| Midlands | 2.5-3.5% | Infrastructure investment | Rapid price changes |

| London | 0.5-1.0% | Affordability constraints | High-value property volatility |

| South East | 0.5-1.5% | Commuter pattern shifts | Oversupply in certain sectors |

For surveyors operating in stronger northern markets, the challenge involves identifying forward-looking comparable evidence that reflects emerging growth rather than historical stagnation. Conversely, in southern markets, surveyors must resist over-relying on historical peak values that no longer reflect current buyer appetite.

Professionals offering services in areas like chartered surveyors in Hertfordshire or chartered surveyors in Essex must carefully calibrate their comparable selections to reflect these regional realities.

Micro-Location Premiums: Street-Level Valuation Adjustments

In a flat market, micro-location factors become magnified. Two identical properties separated by a single street can command significantly different values based on:

- School catchment boundaries

- Proximity to transport links

- Street parking availability

- Noise levels and environmental factors

- Historical desirability and prestige associations

- Future development plans and planning permissions

🏘️ Example scenario: A three-bedroom semi-detached house in a desirable school catchment area in St Albans might command a £30,000-£50,000 premium over an identical property two streets away outside the catchment—even in a flat market. Surveyors must identify and quantify these premiums through detailed local knowledge and comparable analysis.

Local expertise from firms like chartered surveyors in St Albans or chartered surveyors in Guildford becomes invaluable for accurately assessing these street-level variations.

Transaction Volume Challenges: Limited Evidence in Stabilizing Markets

A stabilizing market often means reduced transaction volumes, creating evidence gaps for surveyors. When recent comparable sales are scarce, professionals must employ several strategies:

Temporal adjustments: Using older comparables (6-12 months) with appropriate market movement adjustments based on local indices

Geographical expansion: Extending the search radius while applying location adjustments for differences in desirability

Property type substitution: Using similar property types with adjustments for size, condition, and features when exact matches are unavailable

Market sentiment analysis: Incorporating asking price reductions, time-on-market data, and offer-to-asking price ratios to gauge current market dynamics

"In areas with limited transaction evidence, surveyors must balance the reliability of older comparables against the relevance of more recent but less similar properties. Professional judgment becomes paramount in these situations."

This challenge particularly affects niche property types, rural locations, and high-value properties where transaction frequency is naturally lower. For specialized assessments, services like RICS home surveys provide the detailed analysis necessary for accurate valuations in evidence-scarce scenarios.

RICS Red Book Methodology: Valuation Adjustments for Market Sentiment and Property-Specific Factors

How UK surveyors value properties in a 'flat but turning' market: 2026 methods explained for buyers, sellers and investors requires understanding the sophisticated adjustment methodologies employed by RICS professionals following Red Book standards.

The Comparable Evidence Framework

RICS valuations rely fundamentally on comparable evidence—recent sales of similar properties in similar locations. However, finding truly comparable properties is rarely straightforward. Surveyors employ a systematic adjustment process:

1. Identify potential comparables (ideally 3-6 properties)

- Similar property type and age

- Comparable location and setting

- Similar size (within 20% of subject property)

- Sold within the last 6 months (12 months maximum with adjustments)

2. Apply systematic adjustments for differences:

- Location adjustments (±5-15%): Street desirability, proximity to amenities

- Size adjustments (£X per sq ft/m): Based on local market rates

- Condition adjustments (±5-20%): Modernization, maintenance, presentation

- Feature adjustments: Extensions, parking, gardens, views

- Time adjustments: Market movement since comparable transaction

3. Weight the evidence based on reliability and similarity

4. Apply professional judgment to arrive at final valuation

Accounting for Rental Market Shifts and Landlord Tax Pressures

A unique aspect of 2026 valuations involves rental market dynamics directly impacting capital valuations. Landlord tax pressures and shifting yields require specific adjustments, particularly for investment properties[4].

Key rental market factors affecting 2026 valuations:

📊 Yield compression: Increased taxation reduces net rental income, lowering the capital value investors will pay for rental properties

Calculation example:

- Property generating £18,000 annual rent

- Previous net yield expectation: 5% = £360,000 valuation

- 2026 tax-adjusted net yield: 4% = £450,000 valuation or reduced rental income requiring downward capital adjustment

Regulatory changes: Energy Performance Certificate (EPC) requirements and upcoming rental standards create capital expenditure obligations that surveyors must factor into valuations

Tenant demand shifts: Changes in rental demand patterns affect both rental income projections and capital values

For investors requiring detailed analysis, valuation of commercial property services provide specialized expertise in yield calculations and investment return assessments.

Adjusting for Market Sentiment in a Turning Market

Perhaps the most nuanced aspect of 2026 valuations involves capturing market sentiment shifts. In a "flat but turning" market, backward-looking comparable evidence may not fully reflect emerging buyer confidence or caution.

Sentiment indicators surveyors monitor:

✅ Days on market trends: Decreasing time-to-sale suggests strengthening demand

✅ Offer-to-asking price ratios: Narrowing discounts indicate improving sentiment

✅ Mortgage approval rates: Rising approvals signal increased buyer activity

✅ Viewing-to-offer conversion rates: Higher conversion suggests serious buyer interest

✅ Multiple offer scenarios: Competitive bidding indicates demand exceeding supply

Practical application: If comparable evidence shows properties sold 3-6 months ago at £400,000, but current market indicators show strengthening demand (reduced days on market, higher offer ratios), a surveyor might apply a modest upward adjustment (1-2%) to reflect the turning market sentiment, valuing a similar property at £404,000-£408,000.

Conversely, in weakening southern markets, surveyors might apply downward sentiment adjustments even when recent comparables appear to support higher values.

Specialist Property Valuation Methods

For properties where rental comparables are limited or inappropriate, surveyors employ alternative methodologies[3]:

Rental market analysis: Primary method for standard residential and commercial properties with active rental markets

Trading information analysis: Used for properties like hotels, care homes, or pubs where value derives from business operations rather than rental potential

Replacement cost methodology: Applied to specialist properties (hospitals, schools, unique heritage buildings) where neither rental nor trading comparables exist

Understanding different types of surveys helps property owners determine which valuation approach best suits their specific circumstances.

Practical Guidance: When to Obtain Fresh Valuations and Choosing the Right Approach

The timing and type of valuation significantly impact outcomes for buyers, sellers, and investors in 2026's evolving market conditions.

Why Fresh Valuations Matter in 2026

Valuations older than six months no longer reflect current market realities in 2026's shifting landscape[1]. Several factors have changed:

- Increased property supply: More properties entering the market affects local competition

- Shifted buyer behavior: Changing mortgage rates and affordability calculations alter buyer capacity

- Seasonal variations: Spring and autumn markets perform differently from winter periods

- Regional momentum changes: Northern growth acceleration and southern stagnation have intensified

- Regulatory updates: New EPC requirements and rental regulations affect certain property values

When to commission fresh valuations:

🔄 Every 6 months for properties actively marketed

🔄 Before listing to ensure competitive pricing

🔄 After significant market news (interest rate changes, major policy announcements)

🔄 When comparable properties nearby sell at unexpected prices

🔄 Before accepting offers to verify fair value

Matching Valuation Type to Your Specific Needs

| Your Situation | Recommended Valuation | Why This Approach |

|---|---|---|

| Initial research | Online AVM | Free, instant, provides ballpark figure |

| Considering selling | 3 estate agent valuations | Free, detailed, identifies pricing consensus |

| Help to Buy purchase | RICS Red Book valuation | Legal requirement, certified accuracy |

| Divorce settlement | RICS Red Book valuation | Court-acceptable, professionally defensible |

| Probate/inheritance | RICS Red Book valuation | HMRC requirement, tax purposes |

| Investment analysis | RICS valuation + yield analysis | Incorporates rental returns, tax implications |

| Remortgaging | Lender's valuation or RICS | Depends on lender requirements |

For complex scenarios, understanding whether a mortgage valuation is the same as a survey prevents costly misunderstandings about what different valuations actually assess.

Red Flags: When Valuations Might Be Inaccurate

⚠️ Warning signs to watch for:

- Significant variance between multiple valuations (more than 10% difference)

- Lack of comparable evidence provided by the valuer

- Outdated comparables (older than 6 months without time adjustments)

- Ignoring property defects or necessary repairs in the valuation

- Overly optimistic figures from agents eager to win your business

- Failure to account for local market conditions or regional trends

Questions to ask your valuer:

- What comparable properties informed this valuation?

- What adjustments were made for differences between comparables and this property?

- How have you accounted for current market sentiment in this area?

- What market evidence supports this figure in the current "flat but turning" market?

- How does this valuation account for regional performance variations?

Cost-Benefit Analysis: When to Invest in Professional Valuations

While estate agent valuations remain free, investing £324-£473 in a RICS Red Book valuation provides significant benefits in specific scenarios[1]:

High-value properties: On a £500,000+ property, a 2% valuation error represents £10,000+—far exceeding the valuation cost

Complex properties: Period properties, listed buildings, or unusual construction types require specialist expertise

Legal proceedings: Divorce, probate, or disputes demand professionally certified valuations

Investment decisions: Accurate valuations inform buy/hold/sell decisions worth thousands in opportunity cost

Negotiation leverage: Professional valuations strengthen your position when negotiating prices

For specialized requirements like probate valuations or matrimonial valuations, professional RICS assessments provide essential documentation and legal defensibility.

Investment-Specific Considerations: Valuation Adjustments for Buy-to-Let and Portfolio Properties

Investors face unique valuation challenges in 2026's market, where landlord tax pressures and regulatory changes significantly impact property values beyond simple comparable analysis[4].

Yield-Based Valuation Adjustments

Investment property valuations increasingly incorporate yield calculations that account for:

Tax-adjusted net income:

- Mortgage interest relief restrictions

- Income tax on rental profits

- Capital gains tax implications on disposal

- Stamp duty surcharges for additional properties

Regulatory compliance costs:

- EPC improvement requirements (minimum rating targets)

- Selective licensing fees in certain local authorities

- Safety compliance (electrical testing, gas certificates, smoke alarms)

- Upcoming rental property standards

Vacancy and management factors:

- Expected void periods

- Property management fees

- Maintenance and repair reserves

- Tenant turnover costs

Example calculation:

- Gross rental income: £18,000

- Less: management (10%), maintenance (15%), void periods (5%): £5,400

- Net rental income: £12,600

- Required yield for investor: 5%

- Investment valuation: £252,000

This yield-based figure may differ significantly from owner-occupier comparable evidence, requiring surveyors to weight evidence appropriately based on the property's likely buyer profile.

Portfolio Valuation Strategies

For investors holding multiple properties, portfolio valuations provide consolidated assessments that may reveal:

- Geographic concentration risks

- Property type diversification

- Overall yield performance

- Capital growth trajectories

- Refinancing opportunities

Professional portfolio valuations help investors make strategic decisions about which properties to retain, improve, or dispose of in 2026's regional market variations.

Conclusion: Navigating 2026's Property Valuation Landscape with Confidence

Understanding how UK surveyors value properties in a 'flat but turning' market: 2026 methods explained for buyers, sellers and investors empowers all market participants to make informed decisions during this unique transitional period. The stabilizing market with emerging growth signals creates both opportunities and risks that accurate valuations help navigate.

Key principles to remember:

✅ Match valuation type to purpose: Online AVMs for research, estate agents for selling decisions, RICS valuations for legal requirements

✅ Embrace regional awareness: Northern and Midlands growth versus southern stagnation requires location-specific analysis

✅ Demand fresh evidence: Six-month-old valuations miss critical market shifts in this turning market

✅ Question the numbers: Multiple valuations and detailed comparable evidence reveal pricing accuracy

✅ Account for investment factors: Landlord tax pressures and yield calculations fundamentally affect investment property values

✅ Recognize micro-location premiums: Street-level factors create significant value variations even in flat markets

Actionable Next Steps

For sellers: Commission three estate agent valuations from reputable local agents, compare their comparable evidence, and price competitively for current market conditions rather than historical peak values.

For buyers: Obtain an independent RICS valuation on properties you're seriously considering, especially in areas with limited transaction evidence or where asking prices seem disconnected from market realities.

For investors: Conduct comprehensive yield-based valuations that incorporate 2026's tax landscape and regulatory requirements, focusing on northern regions showing stronger growth trajectories.

For all parties: Engage RICS chartered building surveyors who combine local market expertise with professional standards to deliver valuations that accurately reflect this "flat but turning" market's unique characteristics.

The 2026 property market represents a "fair value" window before anticipated stronger growth materializes. Accurate valuations ensure you neither overpay as a buyer nor undersell as a vendor during this critical transitional period. By understanding the methodologies professional surveyors employ—from comparable evidence selection to regional adjustments to sentiment analysis—you gain the knowledge necessary to evaluate valuations critically and make confident property decisions.

For personalized guidance on your specific property situation, get a quote from qualified professionals who can apply these 2026 valuation methods to your unique circumstances.

References

[1] Property Valuation Guide 2026 – https://morrisarmitage.co.uk/property-valuation-guide-2026/

[2] Globeprwire 2026 1 25 Property Valuation Uk Accurate Home Value Guide – https://investor.wedbush.com/wedbush/article/globeprwire-2026-1-25-property-valuation-uk-accurate-home-value-guide

[3] Revaluation 2026 Everything You Need To Know – https://valuationoffice.blog.gov.uk/2025/09/29/revaluation-2026-everything-you-need-to-know/

[4] Valuation Adjustments For 2026 Rental Market Shifts Impact Of Landlord Tax Pressures On Uk Yields – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-2026-rental-market-shifts-impact-of-landlord-tax-pressures-on-uk-yields

[5] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[6] The Great Reset 10 Predictions That Will Define The Uk Property Market In 2026 – https://www.hmosales.com/blog/market-reports/the-great-reset-10-predictions-that-will-define-the-uk-property-market-in-2026/