Every year, thousands of UK homebuyers move into their dream property only to discover expensive structural defects, hidden dampness, or timber rot that could have been identified before purchase. Despite widespread warnings from surveyors and consumer groups, the confusion between mortgage valuations and building surveys continues to catch buyers off guard—often resulting in repair bills totaling tens of thousands of pounds. In 2026, even as mortgage rates ease and buyer demand shows signs of recovery, this fundamental misunderstanding remains one of the costliest mistakes in the property purchase journey.

Understanding the difference between a buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out is essential for anyone navigating today's property market. These two services serve completely different purposes, yet many first-time buyers and even experienced purchasers mistakenly believe their lender's valuation provides adequate protection against defects.

Key Takeaways

- Mortgage valuations protect lenders, not buyers—they assess loan security but deliberately avoid identifying property defects or maintenance issues

- Building surveys provide comprehensive defect detection—examining structural movement, dampness, timber condition, and providing detailed remediation recommendations

- Both services are essential—relying solely on a mortgage valuation exposes buyers to expensive post-purchase repair bills averaging £15,000-£30,000

- 2026 market conditions create additional risks—surveyors remain cautious with limited comparable evidence, creating valuation gaps particularly for older or non-standard properties

- Strategic timing enables negotiation—commissioning a building survey after offer acceptance but before exchange allows price renegotiation based on discovered defects

Understanding the Fundamental Difference Between Mortgage Valuations and Building Surveys

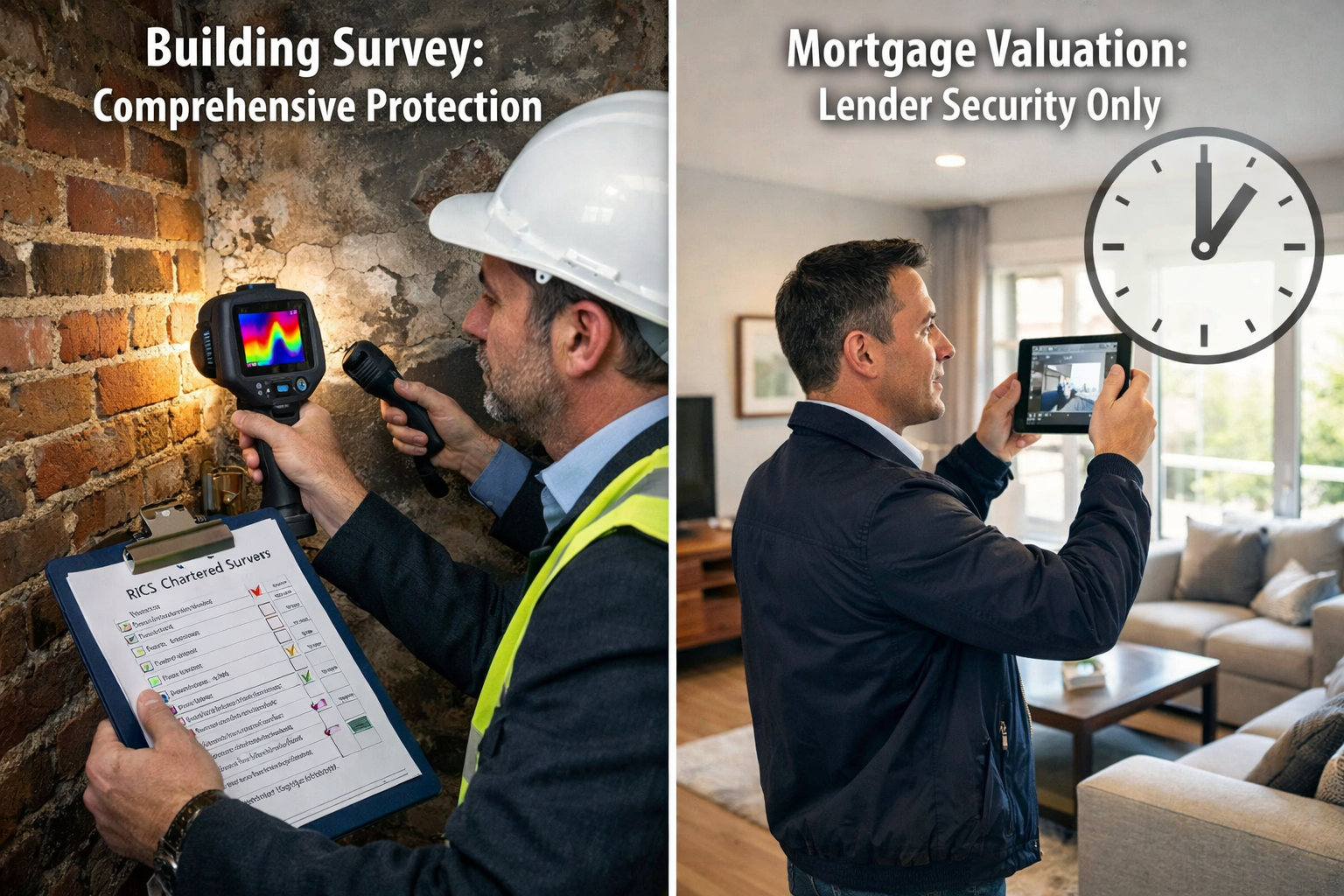

The confusion surrounding buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out stems from a fundamental misunderstanding of purpose. These are not alternative options serving the same function—they are completely different services designed to protect different parties in the property transaction.[1]

What a Mortgage Valuation Actually Does

A mortgage valuation is commissioned by the lender (not the buyer) to assess whether the property provides adequate security for the loan amount. The valuer's primary concern is determining the property's market value and ensuring the lender can recover their money if the borrower defaults.[2][3]

Key characteristics of mortgage valuations include:

- Limited scope: Quick visual inspection focusing only on obvious, visible issues

- Market value assessment: Determining current market worth based on comparable sales

- Lender protection: Ensuring the loan-to-value ratio is acceptable for lending purposes

- No defect investigation: Deliberately avoiding detailed examination of structural condition

- Restricted access: Buyers may not even receive a copy of the report (lender's discretion)[2]

The average cost of a mortgage valuation in 2026 is approximately £233, reflecting its limited scope and brief inspection time.[5] Critically, these valuations do not identify property defects and provide no protection to the buyer beyond confirming the property is worth roughly what they're paying.[1][3]

What a Building Survey Provides

In contrast, a building survey (also known as an RICS Level 3 Home Survey) is commissioned by the buyer to protect their interests by conducting a comprehensive investigation of the property's condition.[6]

Building surveys examine:

✅ Structural integrity: Identifying movement, subsidence, settlement (historic and active)

✅ Dampness: Investigating penetrating damp, rising damp, and condensation issues

✅ Timber defects: Detecting rot, beetle infestation, and structural timber deterioration

✅ Roof condition: Assessing coverings, flashings, guttering, and structural timbers

✅ Building services: Reviewing drainage, heating, electrical installations

✅ External elements: Examining walls, foundations, chimneys, and external joinery

✅ Remediation advice: Providing detailed recommendations with urgency levels and cost implications[2][6]

The cost for building surveys ranges from £445-£629 depending on property size, age, and complexity—representing significantly better value given the protection provided.[5] For those seeking comprehensive protection, working with an RICS chartered building surveyor ensures professional standards and insurance protection.

The Critical Gap That Catches Buyers Out

The fundamental problem is simple: mortgage valuations are not surveys.[3] Yet research consistently shows that many buyers believe their lender's valuation provides adequate assessment of property condition. This misconception creates a dangerous protection gap where buyers commit legally to purchasing properties without understanding their true condition or maintenance requirements.

"A mortgage valuation is not a survey and should never be relied upon as one. It's a basic assessment for the lender's benefit, not the buyer's protection." – RICS Guidance

Understanding whether a mortgage valuation is the same as a survey is the first step toward making an informed decision about property purchase protection.

Why Buyer's Building Survey vs Mortgage Valuation Confusion Persists in 2026

Despite decades of consumer education, the confusion between buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out remains remarkably persistent. Several factors contribute to this ongoing problem in 2026's property market.

Market Conditions and Surveyor Caution

Even as mortgage rates ease in 2026 and buyer demand shows tentative recovery, surveyors remain notably cautious in their valuations. This caution stems from limited comparable evidence, particularly affecting higher-value properties, non-standard constructions, and regional markets with slower transaction volumes.[4]

Many surveyors work with constrained recent completed sales data, creating a valuation gap between their conservative assessments and current market listing prices. This creates additional complexity for buyers who may receive mortgage valuations that differ significantly from agreed purchase prices—triggering renegotiations or failed sales.[4]

This market uncertainty makes comprehensive building surveys even more critical, as they provide independent assessment of actual property condition rather than market sentiment-driven valuations.

First-Time Buyer Vulnerability

First-time buyers represent a particularly vulnerable group, often operating with limited budgets and minimal property knowledge. The additional cost of a building survey (£445-£629) on top of legal fees, stamp duty, and removal costs can seem prohibitive—leading many to rely solely on the "free" mortgage valuation their lender provides.[5]

This false economy frequently results in:

- Undiscovered structural defects requiring immediate attention post-purchase

- Unexpected maintenance costs within the first year of ownership

- Negotiation opportunities missed before legal commitment

- Insurance complications when defects manifest after completion

Property Type Misconceptions

Many buyers incorrectly assume that certain property types don't require comprehensive surveys:

❌ Common Misconceptions:

- "New-build properties don't need surveys" (ignoring construction defects and snagging issues)

- "Modern flats are low-risk" (overlooking cladding concerns, shared structure issues, and building defects)

- "The mortgage valuation would flag serious problems" (it won't—that's not its purpose)

- "Estate agent descriptions are reliable" (they represent the seller's interests, not the buyer's)

In reality, building surveys provide value across all property types, with the survey level tailored to property characteristics:

| Property Type | Recommended Survey | Key Concerns |

|---|---|---|

| Victorian/Edwardian terrace | Level 3 Building Survey | Structural movement, damp, original timber condition |

| 1930s semi-detached | Level 2 or 3 | Cavity wall issues, roof condition, drainage |

| Modern flat (post-2000) | Level 2 + cladding check | Building safety, shared structure, service charges |

| Listed/period property | Level 3 Building Survey | Conservation requirements, specialist repairs, historic defects |

| Converted property | Level 3 Building Survey | Conversion quality, building regulations compliance |

For properties with suspected specific issues, targeted investigations like subsidence surveys or damp surveys complement comprehensive building surveys.

Information Asymmetry

A significant factor in why buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out continues is information asymmetry. Sellers and estate agents understand property defects but have limited legal obligation to disclose them. Meanwhile, buyers often don't know what questions to ask or what warning signs to look for.[7]

Mortgage valuations don't bridge this information gap—they're not designed to. Only a comprehensive building survey conducted by a qualified professional provides buyers with the detailed, independent information needed to make informed decisions.

Real-World Consequences: Case Examples Across Property Types

The practical implications of skipping a building survey extend far beyond theoretical risk. Examining real-world scenarios across different property types illustrates why buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out remains such a critical issue.

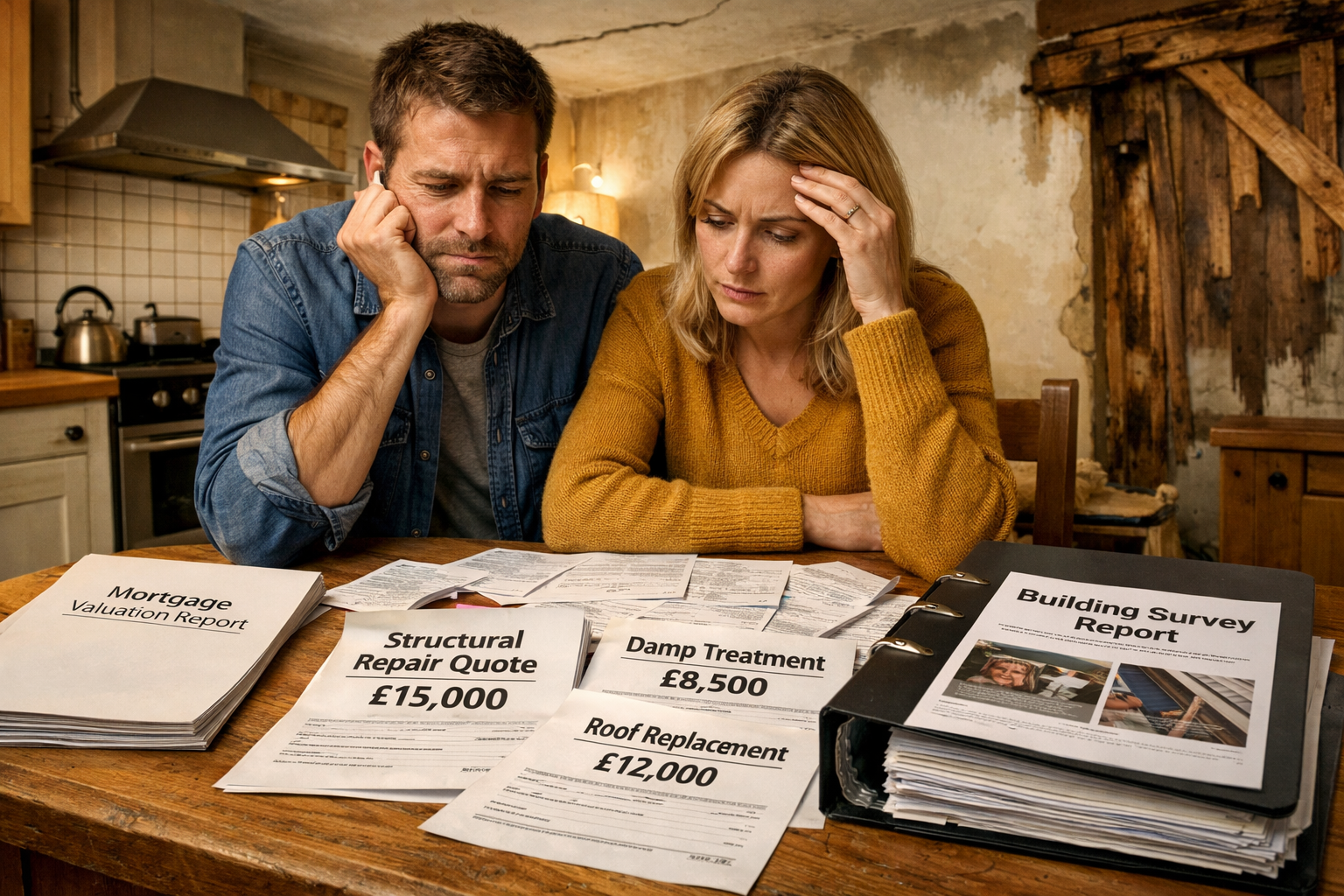

Victorian Terrace: The £28,000 Structural Movement Discovery

Scenario: First-time buyers purchase a Victorian terrace in Manchester for £285,000. The mortgage valuation notes "property appears suitable for lending purposes" with no concerns raised. The buyers proceed without commissioning a building survey to save £595.

Post-Purchase Discovery: Within three months, diagonal cracks appear in the rear extension. A structural survey reveals:

- Active subsidence affecting the rear extension foundation

- Historic movement in the main structure (poorly repaired previously)

- Inadequate drainage causing ground movement

- Estimated repair cost: £28,000 including underpinning and drainage works

Outcome: The buyers face expensive repairs with no recourse against the seller (who may not have known the full extent) or the mortgage valuer (whose report explicitly stated it was not a survey). A pre-purchase building survey would have identified these issues, enabling either price renegotiation or withdrawal from the purchase.

1930s Semi-Detached: The Hidden Damp and Timber Rot

Scenario: A couple purchases a 1930s semi-detached property for £375,000. The mortgage valuation confirms market value alignment. Light surface marks on walls are dismissed as cosmetic.

Post-Purchase Discovery: During renovation work, contractors discover:

- Extensive rising damp affecting ground floor walls

- Failed damp-proof course requiring replacement

- Timber floor joists with wet rot (20% requiring replacement)

- Secondary timber beetle infestation

- Estimated remediation cost: £18,500

Outcome: A building survey would have included moisture meter readings, timber inspection, and sub-floor examination—identifying these defects before purchase and providing leverage for a £15,000-£20,000 price reduction.

Modern Flat: The Building Safety and Defect Combination

Scenario: Buyers purchase a 2015-built apartment for £265,000. Being modern construction, they assume minimal risk and rely solely on the mortgage valuation.

Post-Purchase Discovery: Building safety assessment reveals:

- Non-compliant cladding requiring replacement (service charge implications)

- Water ingress through balcony detailing (common building defect)

- Inadequate ventilation causing condensation and mould

- Shared structure movement affecting multiple units

- Buyer's share of remediation: £35,000 (cladding) plus £4,500 (balcony repairs)

Outcome: Even new-build properties benefit from professional surveys. A comprehensive inspection would have identified construction defects and prompted investigation of building safety certificates, potentially revealing the cladding issue before legal commitment.

Listed Georgian Property: The Conservation Complexity

Scenario: Buyers fall in love with a Grade II listed Georgian townhouse (£685,000) and proceed based on mortgage valuation confirming lending viability.

Post-Purchase Discovery:

- Historic timber beetle infestation requiring specialist treatment

- Lead roof coverings at end of life (£45,000 replacement with listed building consent)

- Single-glazed sash windows with extensive rot (conservation-grade repairs required)

- Lime plaster deterioration (inappropriate previous cement repairs)

- Total immediate maintenance requirement: £78,000

Outcome: Building surveys for listed properties should always include heritage considerations and specialist knowledge. The survey would have provided detailed maintenance forecasting, enabling informed budgeting and potential price negotiation.

The Negotiation Advantage

Beyond defect identification, building surveys provide significant negotiation leverage:

- Price reductions: Documented defects justify renegotiating the purchase price

- Seller remediation: Requesting specific repairs before completion

- Informed withdrawal: Walking away from properties with excessive defects

- Maintenance planning: Budgeting accurately for post-purchase work

Research indicates that building surveys identify issues leading to price renegotiation in approximately 40% of cases, with average reductions of £8,000-£15,000—far exceeding the survey cost.[1]

Making the Right Decision: When and What to Commission

Understanding buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out is only valuable if translated into practical action. Here's how to approach survey decisions strategically.

The Essential Two-Step Approach

Step 1: Accept the Mortgage Valuation (Required)

Your lender will commission a mortgage valuation as a lending condition. This is non-negotiable and protects the lender's interests. The cost (typically £233) is usually added to your mortgage fees.[5]

Step 2: Commission Your Own Building Survey (Highly Recommended)

Independently commission a building survey to protect your interests. This should be:

- Booked after offer acceptance but before exchange of contracts

- Conducted by an RICS chartered surveyor with local market knowledge

- Appropriate level for the property type (Level 2 or Level 3)

- Reviewed carefully with follow-up questions to the surveyor

Choosing the Right Survey Level

The RICS offers three survey levels, each suited to different property characteristics:

Level 1 (Condition Report): Basic overview suitable for:

- Modern properties (post-1990)

- Conventional construction

- Good apparent condition

- Cost: £300-£400

Level 2 (Home Buyer Report): Standard survey suitable for:

- Properties built after 1900

- Conventional construction

- Reasonable condition

- Standard property types

- Cost: £445-£550[5]

Level 3 (Building Survey): Comprehensive survey essential for:

- Properties built before 1900

- Listed or unusual construction

- Properties requiring renovation

- Properties with visible defects

- High-value properties

- Cost: £550-£629+[5]

For most property purchases, a Level 3 Building Survey provides the best protection and value, particularly given 2026's cautious market conditions and valuation uncertainties.[4]

Strategic Timing Considerations

Optimal Survey Timing:

- Offer accepted: Proceed to survey immediately after offer acceptance

- Survey conducted: Allow 5-10 working days for inspection and report

- Report review: Carefully examine findings with your surveyor

- Renegotiation: Use findings to renegotiate price or request repairs

- Exchange: Only exchange contracts when satisfied with property condition

This timing provides maximum protection while maintaining transaction momentum. Commissioning surveys before making an offer wastes money if the offer is rejected; waiting until after exchange removes negotiation leverage.

Additional Specialist Surveys

Depending on building survey findings or specific concerns, consider supplementary investigations:

- Subsidence surveys: For properties with structural movement

- Drainage surveys: CCTV inspection of underground drainage

- Damp surveys: Detailed moisture investigation with laboratory analysis

- Specific defect reports: Targeted investigation of particular concerns

Cost-Benefit Analysis

Many buyers balk at survey costs, but the financial protection provided far exceeds the expense:

| Scenario | Survey Cost | Defects Identified | Outcome | Net Benefit |

|---|---|---|---|---|

| Victorian terrace | £595 | Subsidence, timber rot | £22,000 price reduction | +£21,405 |

| 1930s semi | £525 | Damp, electrical issues | £12,000 price reduction | +£11,475 |

| Modern flat | £475 | Construction defects | Withdrew from purchase | Avoided £35,000 loss |

| New-build house | £550 | Multiple snagging issues | Developer remediation | £8,000 value |

Even when surveys identify no significant defects, the peace of mind and informed decision-making justify the investment.

Questions to Ask Your Surveyor

Maximize survey value by asking:

- What are the three most significant defects identified?

- Which issues require immediate attention versus long-term monitoring?

- What are realistic cost estimates for recommended remediation?

- Are there any issues that might affect insurance or future saleability?

- Should any specialist follow-up surveys be commissioned?

Professional surveyors welcome questions and can provide valuable context beyond the written report.

Conclusion

The persistent confusion surrounding buyer's building survey vs mortgage valuation: why UK homebuyers still get caught out represents one of the most preventable yet costly mistakes in property purchase. As 2026's market shows tentative recovery amid cautious surveyor valuations and limited comparable evidence, the need for comprehensive independent surveys has never been greater.

The fundamental truth is simple: mortgage valuations protect lenders by assessing loan security, while building surveys protect buyers by identifying defects, maintenance requirements, and structural concerns. These are not alternative services—they are complementary protections serving entirely different purposes.[1][2][6]

The real-world consequences of relying solely on mortgage valuations are severe: unexpected repair bills averaging £15,000-£30,000, failed negotiations, and properties that become financial burdens rather than dream homes. Meanwhile, the cost of a comprehensive building survey (£445-£629) represents exceptional value when measured against the protection, negotiation leverage, and peace of mind provided.[5]

Your Action Plan

For anyone purchasing property in 2026, follow this essential checklist:

✅ Accept that mortgage valuations are mandatory but provide no buyer protection

✅ Budget for a building survey as a non-negotiable purchase cost

✅ Choose the appropriate survey level based on property age, type, and condition

✅ Commission surveys after offer acceptance but before exchange of contracts

✅ Work with RICS chartered surveyors with local market expertise

✅ Review reports thoroughly and ask questions about findings

✅ Use survey findings to renegotiate price or request remediation

✅ Consider specialist follow-up surveys for specific concerns

The property market's complexity, combined with 2026's cautious valuation environment, makes professional survey advice more valuable than ever. Whether purchasing a Victorian terrace, modern flat, or listed property, comprehensive building surveys provide the detailed, independent information needed to make informed decisions and avoid expensive post-purchase surprises.

Don't become another statistic in the ongoing story of why UK homebuyers still get caught out. Invest in proper survey protection and approach property purchase with eyes wide open to both opportunities and risks.

For expert survey services tailored to your property type and location, contact qualified chartered surveyors who can provide comprehensive building surveys that protect your interests throughout the purchase process.

References

[1] Survey Vs Mortgage Valuation – https://surveymatch.co.uk/survey-vs-mortgage-valuation/

[2] Building Survey Vs Mortgage Valuation Reports – https://www.kemptoncarr.co.uk/news-and-knowledge/building-survey-vs-mortgage-valuation-reports/

[3] Mortgage Valuations Are Not In Depth Surveys – https://moneyfactscompare.co.uk/mortgages/guides/mortgage-valuations-are-not-in-depth-surveys/

[4] Mortgage Valuations In 2026 Why Surveyors Are Still Cautious Even As Rates Ease – https://www.willowprivatefinance.co.uk/mortgage-valuations-in-2026-why-surveyors-are-still-cautious-even-as-rates-ease

[5] Valuation Survey – https://www.comparemymove.com/guides/surveying/valuation-survey

[6] Understanding The Difference Between A Mortgage Valuation And An Rics Home Survey – https://www.nuvensurveyors.co.uk/blog/understanding-the-difference-between-a-mortgage-valuation-and-an-rics-home-survey/

[7] Difference Between Mortgage Valuation And Survey – https://www.watsons-property.co.uk/difference-between-mortgage-valuation-and-survey/