The clock is ticking for owners of high-value UK residential properties. As 2026 unfolds, the Valuation Office Agency (VOA) is conducting a comprehensive valuation exercise that will determine which properties fall under the new high-value council tax surcharge—commonly known as the "mansion tax." With April 2026 serving as the critical benchmark date, property owners across England are turning to RICS-certified surveyors to conduct pre-emptive valuations and develop strategic approaches to minimize their tax exposure. Understanding Valuation Adjustments for the 2026 Mansion Tax Preparations: Surveyor Strategies for High-Value UK Homes has become essential for anyone with properties approaching or exceeding the £2 million threshold.

This comprehensive guide explores the professional surveying methodologies, valuation adjustment techniques, and strategic planning approaches that property owners and their advisors are employing to navigate this significant tax change before the 2028 implementation deadline.

Key Takeaways

- 🏛️ 2026 is the definitive valuation year: The VOA is conducting targeted assessments throughout 2026, with April 2026 as the likely benchmark date that will determine tax liability for the next five years

- 💰 Four-tier surcharge structure: Annual charges range from £2,500 to £7,500 depending on property value bands, with revaluations occurring every five years thereafter

- 📊 Strategic timing matters: Completing significant renovations after the 2026 valuation could save thousands in cumulative tax charges over the five-year assessment period

- 🔍 Professional RICS valuations are critical: Accurate pre-emptive assessments help property owners understand their position and plan strategic adjustments before official VOA valuations

- 📍 London and South East concentration: Over 65% of affected properties are in these regions, creating particular valuation challenges in prime residential corridors with limited comparable sales data

Understanding the 2026 Mansion Tax Framework

The high-value council tax surcharge represents a fundamental shift in how England taxes residential property wealth. Unlike traditional council tax based on 1991 property values, this new levy applies to properties valued at £2 million or more based on current market conditions.

The Four-Tier Surcharge Structure

The mansion tax operates on a banded system with four distinct tiers, each carrying specific annual charges:[1]

| Property Value Band | Annual Surcharge | Five-Year Total (2028-2033) |

|---|---|---|

| £2.0m – £2.5m | £2,500 | £12,500 |

| £2.5m – £3.5m | £3,500 | £17,500 |

| £3.5m – £5.0m | £5,000 | £25,000 |

| £5.0m+ | £7,500 | £37,500 |

These charges will be subject to Consumer Price Index (CPI) inflation adjustments beginning in the 2029-30 tax year, meaning the actual amounts will increase annually thereafter.[2][3]

"The surcharge applies based on asset value rather than usage status, meaning second homes in England valued at £2 million or more will incur the HVCTS liability, potentially in addition to existing local second home premiums."[1]

Revenue Projections and Market Impact

Treasury estimates project the mansion tax will generate approximately £400 million annually by 2031,[2] reflecting the substantial number of properties expected to fall within scope. More significantly, economists anticipate a 2.5% dampening effect on high-end property values as buyers "price in" the cumulative cost of the surcharge over their anticipated holding period.[1]

This market distortion is already creating strategic considerations for chartered surveyors across London and surrounding areas, particularly regarding properties valued near threshold boundaries.

Valuation Adjustments for the 2026 Mansion Tax Preparations: RICS Methodologies

Professional surveyors are employing sophisticated RICS Red Book compliant methodologies to conduct pre-emptive valuations that help property owners understand their potential exposure. These assessments go far beyond simple automated valuation models (AVMs) and require nuanced professional judgment.

Comparative Market Analysis in High-Value Segments

For properties in the £2 million to £5 million range, RICS-certified valuers typically employ comparative market analysis as their primary methodology. This approach involves:

Identifying Comparable Sales

- Recent transactions (typically within 6-12 months) of similar properties

- Geographic proximity (preferably within 0.5 miles in urban areas)

- Matching property characteristics (size, type, condition, features)

- Adjustments for market movement between transaction date and valuation date

Making Adjustment Factors

- Location adjustments: Properties on premium streets may command 10-20% premiums over nearby roads

- Size differentials: Price per square foot typically decreases as total size increases

- Condition variations: Properties requiring significant renovation may be discounted 15-30%

- Feature enhancements: Swimming pools, garages, gardens, and period features each carry specific value impacts

Challenges in Ultra-High-Value Property Valuations

Properties exceeding £5 million—particularly in exclusive enclaves like Mayfair, Belgravia, and Knightsbridge—present unique valuation challenges due to limited transactional comparables.[3] In these segments, surveyors must employ:

Residual Valuation Methods

- Assessing land value separately from improvements

- Calculating depreciated replacement cost for unique architectural features

- Considering development potential and alternative use values

Income Capitalization Approaches

- Estimating potential rental income for similar properties

- Applying appropriate capitalization rates based on market yields

- Particularly relevant for properties that could serve as rental investments

Hedonic Pricing Models

- Statistical analysis of how specific features contribute to overall value

- Regression analysis incorporating multiple property characteristics

- Useful for properties with unique combinations of features

Professional valuation reports prepared for mansion tax planning purposes should clearly document the methodology employed and provide detailed justification for all adjustments made to comparable sales data.

Strategic Surveyor Approaches for High-Value UK Homes

Beyond conducting accurate valuations, surveyors are advising property owners on strategic interventions that can influence where properties fall within the banded structure—or whether they fall within scope at all.

The Critical Timing of Property Improvements

Perhaps the most significant strategic consideration involves the timing of renovations and improvements. The mathematics are compelling:

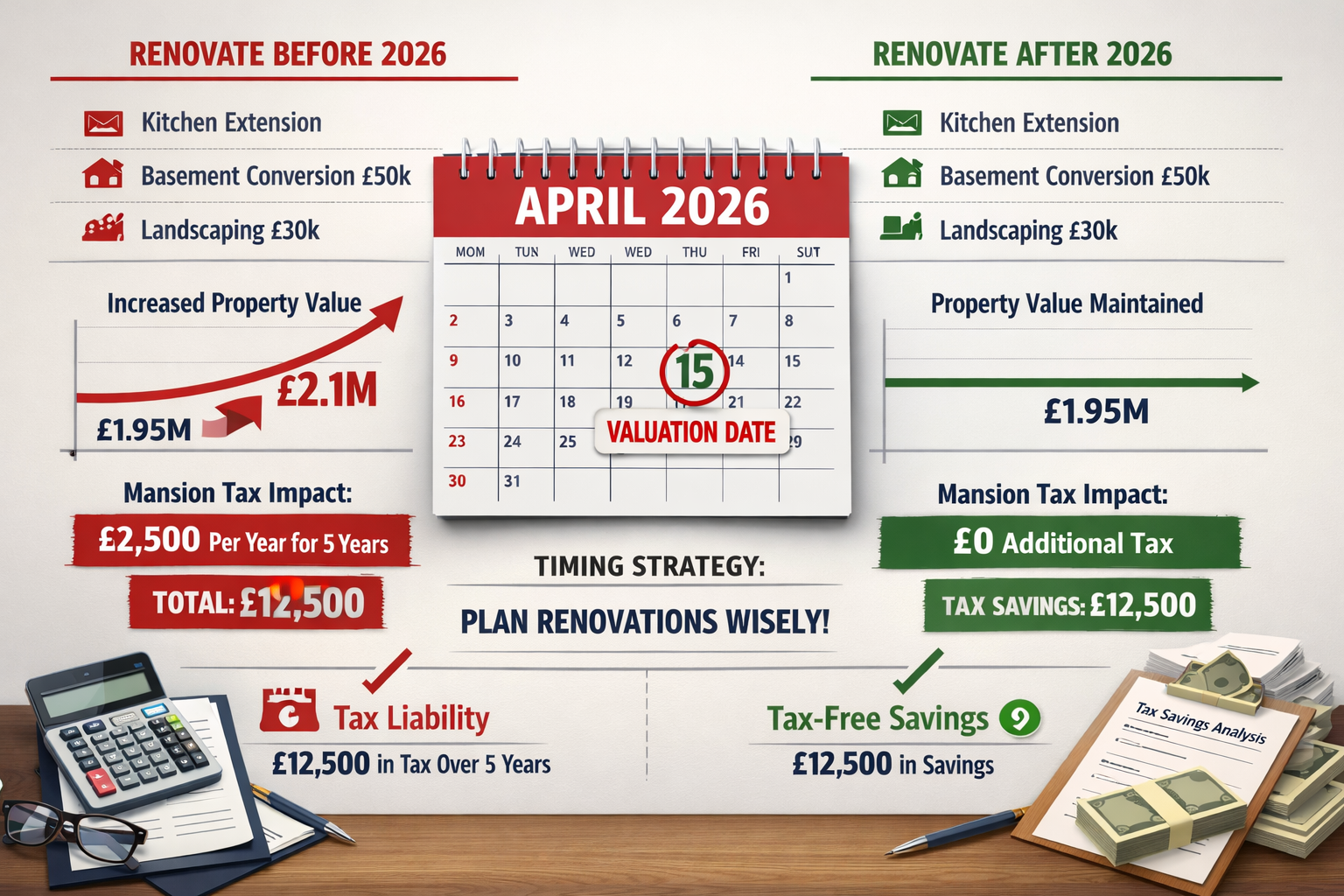

Pre-2026 Completion Scenario

- Property currently valued at £1.95 million

- Planned £200,000 kitchen and bathroom renovation

- Post-improvement value: £2.15 million

- Result: Property enters £2.0m-£2.5m band

- Five-year tax cost: £12,500

Post-2026 Completion Scenario

- Same property valued at £1.95 million in April 2026

- Renovation completed in summer 2026 (after valuation date)

- 2026 valuation: £1.95 million (below threshold)

- Five-year tax cost: £0

- Tax savings: £12,500[1][4]

This creates a powerful incentive to defer major improvements until after the April 2026 valuation window closes. Surveyors are advising clients to:

✅ Complete essential maintenance and repairs that don't significantly add value

✅ Delay luxury upgrades, extensions, and high-end renovations

✅ Postpone basement conversions, loft extensions, and outbuildings

✅ Consider temporary solutions for immediate needs until post-valuation

Valuation Date vs. Purchase Price Considerations

A critical misunderstanding among property owners is the belief that purchase price determines mansion tax liability. In reality, the surcharge is based entirely on 2026 market value, regardless of when or for how much the property was acquired.[4]

This creates particular challenges for:

Long-Term Homeowners

- Purchased properties decades ago at modest prices

- Property appreciation has pushed current values above £2 million

- No intention to sell but facing annual surcharge based on market conditions

- May benefit from professional valuations demonstrating values below threshold

Recent Purchasers

- Bought during peak market conditions in 2021-2022

- Current 2026 values may be lower than purchase price

- Professional valuations can document market corrections

- Potential to demonstrate values below threshold despite high purchase prices

Understanding these factors of valuation is essential for accurate tax planning.

Geographic Concentration and Regional Valuation Strategies

The mansion tax impact is far from uniform across England. Geographic concentration creates distinct challenges and opportunities in different regions.

London and South East Dominance

Over 65% of affected properties are concentrated in London and the South East, with London alone accounting for approximately half of all properties expected to fall within scope.[1] This concentration creates specific valuation dynamics:

Prime Central London

- Central London properties face the highest concentration

- Limited comparable sales in ultra-prime segments

- International buyer considerations affecting market values

- Potential for significant valuation disputes with VOA

Affluent Suburbs and Commuter Belt

- Areas like Richmond, Barnes, and Weybridge see high concentrations

- More robust comparable sales data available

- Family homes rather than "mansions" often affected

- Strategic positioning around £2 million threshold critical

Home Counties

- Surrey, Hertfordshire, and Hampshire properties affected

- Larger properties with land may have more valuation flexibility

- Rural property valuation methodologies differ from urban

Price Bunching Around the £2 Million Threshold

Economists predict significant "price bunching" as the market adjusts to the tax threshold. Sellers are expected to adjust asking prices to £1.99 million to escape the initial £2,500 annual surcharge,[1] creating artificial clustering just below the threshold.

This phenomenon creates both challenges and opportunities:

For Sellers

- Strategic pricing to maximize marketability

- Accepting slightly lower sale prices to attract buyers avoiding tax

- Professional valuations supporting asking prices below threshold

For Buyers

- Negotiating leverage on properties priced just above £2 million

- Factoring in cumulative tax costs when making offers

- Seeking professional valuations before purchase to confirm tax position

Valuation Adjustments for the 2026 Mansion Tax Preparations: Appeal and Dispute Strategies

Given the financial stakes involved, surveyors are preparing clients for potential valuation disputes with the VOA following the 2026 assessment exercise.

Grounds for Challenging VOA Valuations

Professional surveyors can support appeals based on several grounds:

Comparable Evidence Disputes

- VOA used inappropriate or outdated comparables

- Failed to account for specific property disadvantages

- Overlooked material differences between subject property and comparables

- Incorrect adjustments for location, condition, or features

Methodology Challenges

- Inappropriate valuation approach for property type

- Failure to consider market conditions at valuation date

- Incorrect measurement or property description

- Overlooked structural issues or defects affecting value

Market Timing Considerations

- Property market fluctuations between VOA assessment and official valuation date

- Local market conditions not reflected in VOA analysis

- Recent comparable sales not considered by VOA

Building a Robust Evidence Base

Surveyors advising on potential appeals are developing comprehensive evidence portfolios including:

📋 Professional RICS Valuation Reports

- Detailed comparable sales analysis

- Clear methodology documentation

- Professional photographs and floor plans

- Market context and trends analysis

📋 Supporting Documentation

- Recent estate agent appraisals

- Evidence of property defects or issues

- Planning constraints affecting value

- Local market data and trends

📋 Expert Witness Capability

- RICS-qualified surveyors can provide expert testimony

- Professional indemnity insurance coverage

- Experience in valuation tribunals and appeals

Working with experienced chartered surveyors and valuers who understand both RICS methodology and VOA procedures is essential for successful appeals.

Second Homes and Multiple Property Considerations

The mansion tax applies to all qualifying properties regardless of usage status, creating additional complexity for owners of second homes and investment portfolios.

Second Home Surcharge Stacking

Properties used as second homes face potential double taxation:

- Local authority second home premium (up to 100% council tax surcharge in some areas)

- High-value council tax surcharge (mansion tax) based on property value

This creates annual carrying costs that can exceed £10,000-£15,000 for a £2.5 million second home in certain local authorities.[1]

Portfolio Strategy Considerations

Investors and families with multiple high-value properties must consider:

Ownership Structure Reviews

- Corporate ownership implications

- Trust structures and tax treatment

- Family member allocation strategies

- Potential restructuring before 2026 valuation

Property Disposition Timing

- Strategic sales of properties near threshold

- Consolidation of multiple moderate-value properties

- Geographic diversification to lower-tax jurisdictions

- Timing sales to occur before 2026 valuation impacts market

Rental vs. Owner-Occupation

- Income generation to offset surcharge costs

- Rental market conditions in high-value segments

- Tax treatment of rental income vs. surcharge costs

The 2031 Revaluation Cycle and Long-Term Planning

While 2026 represents the initial valuation exercise, property owners must recognize that revaluations will occur every five years thereafter (2031, 2036, etc.).[4]

Properties Currently Below Threshold

Properties currently valued at £1.7-£1.9 million face particular uncertainty:

Market Appreciation Scenarios

- Average annual property appreciation of 3-4% could push values above £2 million by 2031

- Properties currently "safe" may enter scope at first revaluation

- Long-term tax planning must account for future appreciation

Strategic Considerations

- Avoiding improvements that accelerate appreciation

- Monitoring local market trends and comparables

- Preparing for potential future liability even if currently exempt

Inflation Adjustments to Surcharge Amounts

Beginning in the 2029-30 tax year, the surcharge amounts themselves will be adjusted annually for CPI inflation.[2][3] This compounds the effective tax burden over time:

Projected Surcharge Growth (Assuming 2.5% Annual CPI)

- 2028-29: £2,500 (base year)

- 2029-30: £2,563 (+2.5%)

- 2030-31: £2,627 (+2.5%)

- 2031-32: £2,692 (+2.5%)

- 2032-33: £2,760 (+2.5%)

Over the initial five-year period, cumulative costs will exceed the simple £12,500 calculation (£2,500 × 5 years) due to these inflation adjustments.

Professional Surveyor Selection for Mansion Tax Valuations

Choosing the right professional surveyor for pre-emptive mansion tax valuations requires careful consideration of specific qualifications and experience.

Essential Qualifications and Credentials

Property owners should seek surveyors with:

✓ RICS Membership (MRICS or FRICS designation)

✓ Red Book Valuation Certification

✓ Experience in high-value residential sector

✓ Local market knowledge in relevant geographic area

✓ Professional indemnity insurance (minimum £1 million coverage)

✓ VOA appeal experience (for potential dispute support)

Understanding valuation costs and fee structures is important, but the cheapest option rarely provides the comprehensive analysis needed for effective tax planning.

Scope of Professional Valuation Services

A comprehensive mansion tax preparation valuation should include:

Physical Inspection

- Detailed internal and external property examination

- Measurement verification

- Condition assessment

- Feature and amenity documentation

Market Analysis

- Comprehensive comparable sales research

- Local market trend analysis

- Geographic and feature adjustment calculations

- Valuation date market conditions assessment

Reporting

- Detailed written valuation report

- Photographic documentation

- Floor plans and measurements

- Clear methodology explanation

- Comparable sales evidence appendix

Advisory Services

- Strategic improvement timing recommendations

- Threshold positioning advice

- Appeal preparation support if needed

- Ongoing valuation monitoring through 2026

For those uncertain about which type of assessment they need, reviewing guidance on which survey do you need can provide helpful context.

Conclusion

Valuation Adjustments for the 2026 Mansion Tax Preparations: Surveyor Strategies for High-Value UK Homes represents a critical planning imperative for property owners across England's prime residential markets. With the VOA's 2026 valuation exercise now underway and the April 2026 benchmark date approaching rapidly, the window for strategic action is narrowing.

The financial implications are substantial: properties valued just above the £2 million threshold face minimum five-year tax costs of £12,500, while those in higher bands could pay £37,500 or more before inflation adjustments. For properties hovering near threshold boundaries, professional RICS valuations and strategic timing of improvements could mean the difference between significant tax liability and complete exemption.

Actionable Next Steps

Property owners should take the following immediate actions:

-

Commission a Professional RICS Valuation – Engage qualified surveyors now to understand current property value and proximity to tax thresholds

-

Review Planned Improvements – Assess whether significant renovations should be deferred until after the April 2026 valuation date to avoid pushing properties into higher tax bands

-

Gather Documentation – Compile evidence of property defects, market conditions, and comparable sales that could support lower valuations or potential appeals

-

Consider Strategic Options – Evaluate ownership structures, disposition timing, and portfolio strategies with professional tax and legal advisors

-

Monitor Market Conditions – Track local property market trends and comparable sales through 2026 to understand how valuations may evolve

-

Prepare for Long-Term Implications – Recognize that 2031 revaluation and ongoing inflation adjustments will affect long-term property ownership costs

The mansion tax represents a permanent shift in the UK's approach to taxing residential property wealth. Property owners who engage professional surveyors now to conduct thorough valuations, develop strategic adjustment plans, and prepare robust evidence bases will be best positioned to minimize their tax exposure and navigate this significant change in the property taxation landscape.

Working with experienced RICS-certified professionals who understand both valuation methodology and the specific nuances of the mansion tax framework is not merely advisable—it is essential for protecting property wealth in the years ahead.

References

[1] Hvcts Guide – https://www.crownluxuryhomes.com/hvcts-guide/

[2] Everything You Need To Know About The Mansion Tax – https://www.bateman-group.co.uk/everything-you-need-to-know-about-the-mansion-tax/

[3] Implications Of The Mansion Tax For High Value Residential Property Owners And Investors – https://www.barnes-law.co.uk/blogs-and-articles/implications-of-the-mansion-tax-for-high-value-residential-property-owners-and-investors

[4] Mansion Tax In The Uk A Complete Guide For Property Owners – https://www.ukpropertyaccountants.co.uk/mansion-tax-in-the-uk-a-complete-guide-for-property-owners/