The UK government's proposed homebuying reforms could fundamentally shift when and how property valuations occur, with upfront condition assessments potentially becoming mandatory before properties even reach the market. As of April 2026, the Royal Institution of Chartered Surveyors (RICS) continues to shape the professional response to these transformative changes, while the industry awaits final implementation details following consultation feedback reviews that closed in December 2025.[5] This seismic shift in the homebuying process represents the most significant structural change to property transactions in decades, placing Valuation Surveys for Upfront Property Condition Assessments: RICS Playbook Under 2026 Homebuying Reforms at the centre of industry preparation and professional development.

The proposed reforms aim to reduce transaction fall-through rates, accelerate completion timelines, and provide buyers with critical property information earlier in their decision-making process. For chartered surveyors, this creates both unprecedented demand and new professional challenges around capacity, standardisation, and valuation methodology in a shifting market environment.

Key Takeaways

- 🏠 Upfront assessments mandated: Government reforms propose making property condition surveys a standard requirement before marketing, fundamentally changing transaction timelines

- ⏱️ 24-month implementation window: RICS has requested at least two years to build capacity, develop standards, and train professionals before reforms take effect[5]

- 📊 Market volatility impacts valuations: February 2026 data shows buyer enquiries at -26% net balance, with regional house price divergence requiring sophisticated adjustment techniques[2]

- 👷 Capacity building underway: RICS is enhancing graduate pathways and CPD platforms to meet anticipated surge in early-stage survey demand[1]

- 📋 Professional standards evolving: New guidance frameworks are being developed to ensure consistency and quality across upfront condition assessments

Understanding the 2026 Homebuying Reform Landscape

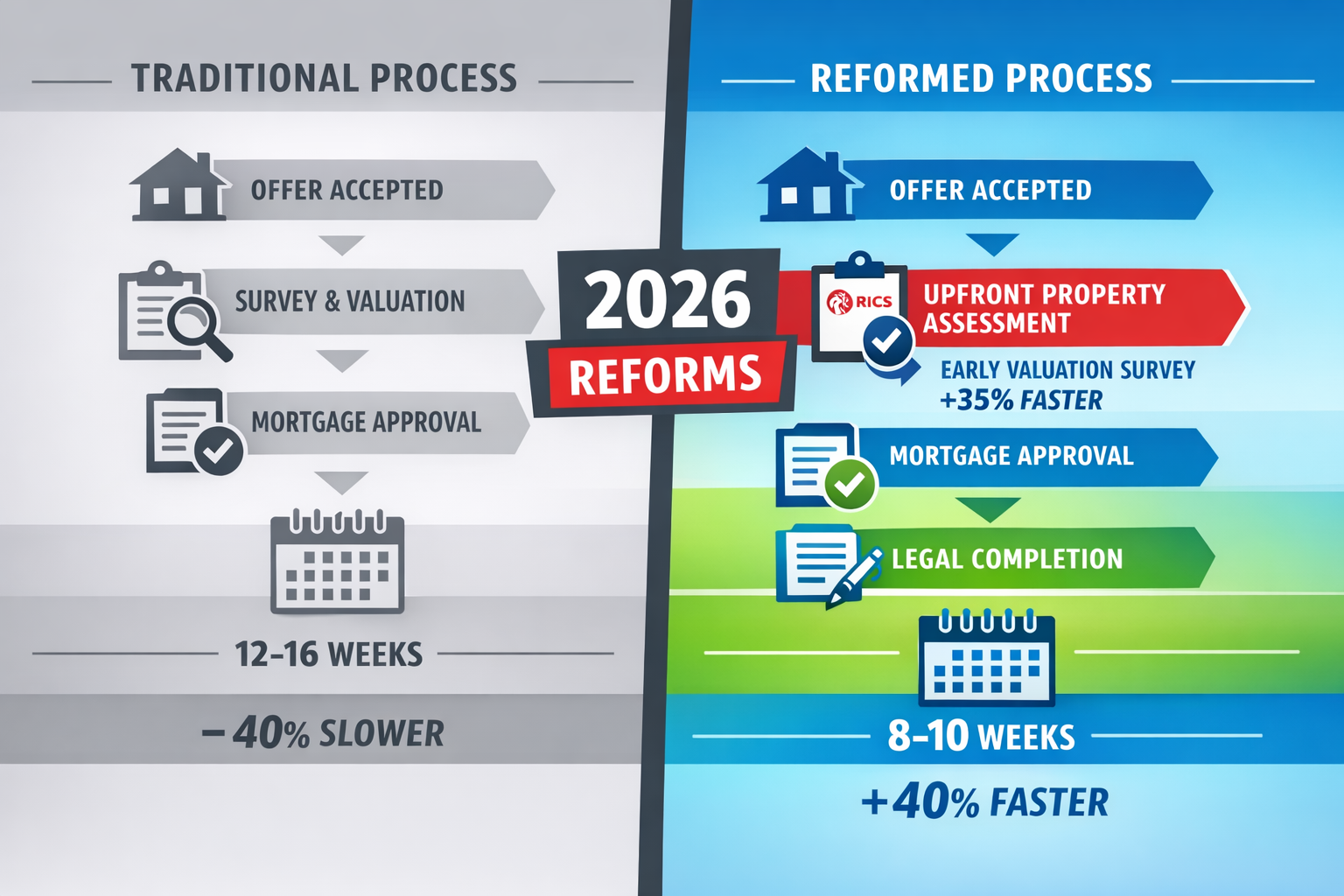

The proposed homebuying reforms represent a comprehensive overhaul of the traditional UK property transaction process. Under the current system, buyers typically commission surveys and valuations only after making an offer and having it accepted—a sequence that contributes to the UK's notoriously high transaction fall-through rates and extended completion periods.

The Current vs Reformed Process

Traditional Timeline:

- Property marketed

- Buyer makes offer

- Offer accepted

- Survey commissioned

- Mortgage valuation arranged

- Issues discovered

- Renegotiation or withdrawal

Proposed Reformed Timeline:

- Property condition assessment completed upfront

- Property marketed with survey information

- Buyer makes informed offer

- Mortgage valuation (simplified)

- Faster completion with fewer surprises

This fundamental restructuring places RICS valuations at the beginning rather than the middle of the transaction journey, creating what industry experts describe as a "front-loaded" process that prioritises transparency and informed decision-making.[3]

Government Consultation Status and Timeline Uncertainty

As of April 2026, no definitive implementation timeline has been established. The government continues reviewing feedback from consultations that concluded in December 2025, with significant uncertainty around which elements will require further consultation versus primary legislation.[5] This ambiguity creates planning challenges for surveying firms investing in capacity expansion and technology infrastructure.

RICS has been vocal in requesting clarity and adequate preparation time. The institution formally requested a minimum 24-month implementation period to allow the industry to:

- Build sufficient surveyor capacity to handle increased early-stage demand

- Develop standardised assessment frameworks and reporting templates

- Create clear guidance on liability and professional standards

- Train existing professionals on new methodologies

- Establish quality assurance mechanisms[5]

The professional body has also offered to support government research into industry capacity and resourcing requirements, emphasising that realistic timelines are essential to avoid market disruption and maintain professional standards.[5]

Valuation Surveys for Upfront Property Condition Assessments: Technical Framework

The shift to upfront property condition assessments requires surveyors to adapt their methodologies, reporting formats, and client engagement models. Unlike traditional surveys commissioned by motivated buyers, upfront assessments serve multiple potential audiences and must balance comprehensiveness with cost-effectiveness for sellers.

Survey Types and Their Role in Reformed Process

Different survey levels serve distinct purposes within the upfront assessment framework:

| Survey Type | Scope | Typical Cost Range | Best For |

|---|---|---|---|

| RICS Level 2 (HomeBuyer) | Condition overview, significant defects | £400-£900 | Standard properties in reasonable condition |

| RICS Level 3 (Building Survey) | Comprehensive inspection, detailed defects | £600-£1,500 | Older properties, unusual construction, major alterations |

| Valuation Only | Market value assessment | £250-£500 | Mortgage lending purposes (simplified under reforms) |

| Condition Report | Basic condition assessment | £300-£600 | New-build or recently renovated properties |

Under the proposed reforms, sellers would likely commission a standardised upfront condition assessment—potentially a modified Level 2 survey—that provides sufficient detail for buyers to make informed offers while remaining cost-proportionate for sellers. Understanding which survey you need becomes crucial for both sellers preparing properties for market and buyers deciding whether additional investigation is warranted.

RICS Red Book Compliance and Valuation Standards

RICS Red Book standards provide the authoritative framework for property valuations in the UK. Under upfront assessment reforms, Red Book compliance becomes even more critical as valuations must withstand scrutiny from multiple parties throughout the transaction lifecycle.

Key Red Book principles for upfront assessments:

- Objectivity and independence: Surveyors must remain impartial despite being commissioned by sellers

- Transparency: Assumptions, limitations, and data sources must be clearly documented

- Competence: Valuers must possess appropriate knowledge of local markets and property types

- Market value definition: Valuations must reflect "the estimated amount for which an asset should exchange on the valuation date"

The reformed process may require enhanced disclosure protocols, ensuring that upfront valuations commissioned by sellers are shared with buyers in a standardised, accessible format that supports informed decision-making without creating undue liability for the commissioning surveyor.

Adjusting Valuations in Volatile Market Conditions

2026 has presented significant market volatility that directly impacts valuation methodology. February 2026 data revealed new buyer enquiries falling to -26% net balance, down from -15% in January, driven by renewed interest rate concerns and geopolitical uncertainty.[2] This deterioration continued into March, with house price net balances reaching -15% amid rising mortgage rates following Middle East conflict escalation.[6]

Regional divergence has been particularly pronounced:

- London: -40% price net balance

- South East: -24% price net balance

- East Anglia: -26% price net balance

- Northern regions: Relatively more stable with modest positive sentiment[2]

For surveyors conducting upfront assessments, this volatility requires sophisticated adjustment techniques:

✅ Time-sensitive valuations: Clearly dating valuations and including validity periods (typically 3-6 months)

✅ Comparable evidence weighting: Prioritising recent transactions over older comparables in rapidly changing markets

✅ Adjustment transparency: Documenting specific adjustments for condition, location, and market momentum

✅ Scenario analysis: Providing valuation ranges or sensitivity analyses for properties in uncertain markets

✅ Regular revalidation: Establishing protocols for updating valuations if properties remain unsold beyond validity periods

Capital Economics forecasts house prices will rise by just 1.5% in the year to Q4 2026, though analysts note increasing downside risks due to mortgage rate pressures.[4] This modest growth outlook, combined with regional variation, demands careful calibration of valuation assumptions and transparent communication of market context.

Understanding factors of valuation becomes particularly important when market conditions are fluid and comparable evidence may quickly become outdated.

RICS Playbook: Professional Standards and Capacity Building

RICS has responded to the reform proposals with a comprehensive strategy focused on maintaining professional standards while building the capacity needed to meet anticipated demand increases.

Graduate Pathways and Workforce Development

The institution is actively working on clearer pathways for graduates to gain qualifications, recognising that the surveying profession needs substantial workforce expansion to handle the volume shift created by upfront assessments.[1] Current initiatives include:

- Streamlined Assessment of Professional Competence (APC): Simplified pathways for candidates to achieve chartered status

- University partnerships: Enhanced collaboration with property and surveying degree programmes

- Apprenticeship routes: Alternative qualification pathways for non-graduate entrants

- Specialisation tracks: Focused training in residential valuation and condition assessment

These workforce development efforts aim to address what many in the industry view as a critical capacity constraint. If every property entering the market requires an upfront condition assessment, the volume of surveys could increase by 30-50% compared to current levels, where many transactions proceed without comprehensive surveys.

Enhanced CPD and Digital Tools

For existing professionals, RICS is enhancing Continuing Professional Development (CPD) platforms with improved digital tools and a new RICS member app designed to support adaptation to regulatory changes.[1] These resources focus on:

- Market analysis techniques: Training on valuation adjustments in volatile conditions

- Technology integration: Using thermal imaging, drone surveys, and digital reporting platforms

- Liability management: Understanding professional indemnity implications of upfront assessments

- Client communication: Managing expectations when surveys serve multiple audiences

The chartered surveyors and valuers who embrace these enhanced capabilities will be best positioned to thrive in the reformed market environment.

Quality Assurance and Standardisation

A critical element of the RICS playbook involves establishing consistent quality standards across upfront assessments. Without standardisation, there's risk that:

- Different surveyors produce incomparable reports

- Buyers struggle to interpret varying formats and terminology

- Liability disputes arise from inconsistent scoping

- Market confidence in upfront assessments erodes

RICS is developing standardised templates and reporting frameworks specifically for upfront condition assessments, balancing comprehensiveness with readability for non-specialist audiences. These frameworks will likely include:

📋 Standardised condition ratings (e.g., 1-5 scale for building elements)

📋 Mandatory disclosure sections (structural issues, damp, services condition)

📋 Estimated repair cost bands (helping buyers budget for remedial works)

📋 Clear limitation statements (defining scope and non-invasive nature of inspections)

📋 Digital-first formats (enabling easy sharing and integration with property listings)

This standardisation effort mirrors approaches in other markets where upfront assessments are already common, such as Scotland's Home Report system, while adapting to England and Wales' distinct market characteristics.

Market Context: 2026 Surveying Sector Outlook

Despite short-term market headwinds, the broader outlook for surveying in 2026 remains cautiously optimistic, with structural factors supporting increased demand for professional property assessments.

Lending Volume Recovery and Survey Demand

Industry forecasts suggest 2026 will be a positive year for the surveying sector with anticipated uplift in volumes across both lending and surveys.[1] Many mortgage lenders are forecasting increased volumes, contributing to optimistic sector sentiment despite February and March's market softness.

This recovery is supported by:

- Pent-up demand: Buyers who delayed purchases in 2024-2025 re-entering the market

- Mortgage product innovation: More competitive fixed-rate offerings as inflation stabilises

- First-time buyer schemes: Government support programmes maintaining entry-level activity

- Professional landlord investment: Continued buy-to-let activity from institutional investors[1]

The combination of natural market recovery and potential reform-driven demand creates a unique growth opportunity for surveying practices that invest in capacity and capability development now.

Buy-to-Let Sector and Professional Landlords

Institutional and professional landlords continue to invest bullishly in the buy-to-let sector, with expert landlords increasingly working with property professionals and understanding the value of proper surveys.[1] This segment represents a particularly attractive market for surveyors because:

- Professional landlords commission surveys proactively rather than reactively

- Portfolio investors require consistent valuation methodologies across properties

- Regulatory compliance (EPC ratings, safety standards) drives demand for specialist assessments

- Long-term investment horizons justify comprehensive condition surveys

For surveyors, cultivating relationships with professional landlord clients provides stable, recurring revenue that's less sensitive to residential market volatility. Services such as stock condition surveys and reinstatement valuations become particularly relevant for this client segment.

Regional Variations and Local Market Expertise

The pronounced regional divergence in 2026 market conditions underscores the importance of local market expertise in delivering accurate valuations. While London and the South East experience significant downward price pressure, other regions maintain more stable or even positive momentum.[2]

This regional variation creates opportunities for surveyors with deep local knowledge who can:

- Identify micro-market trends within broader regional patterns

- Adjust valuations based on neighbourhood-specific factors

- Provide context on local supply-demand dynamics

- Advise clients on optimal timing for transactions

Practices operating across multiple regions must develop robust knowledge-sharing systems to ensure valuers have access to current market intelligence for their specific areas. Understanding Manchester valuation dynamics, for example, requires different expertise than valuing properties in the Home Counties or Scotland.

Practical Implementation: Preparing for Reformed Homebuying

While final implementation timelines remain uncertain, surveying practices can take concrete steps now to position themselves advantageously for the reformed market environment.

Technology Investment and Digital Transformation

Modern surveying increasingly relies on technology to enhance accuracy, efficiency, and client communication. Key technology investments include:

🔧 Inspection tools:

- Thermal imaging cameras for damp and insulation assessment

- Drone surveys for roof and chimney inspection

- Moisture meters and environmental monitoring equipment

- Laser measuring devices for precise dimensional recording

💻 Software platforms:

- Digital survey reporting systems with standardised templates

- Mobile apps for on-site data capture and photo annotation

- Cloud-based document management for secure client access

- Integration with property portals and conveyancing platforms

📊 Data analytics:

- Automated comparable property identification

- Market trend analysis and valuation adjustment tools

- Quality assurance algorithms flagging outlier valuations

- Client relationship management systems

Practices that invest in these technologies now will be better positioned to scale operations efficiently when reform-driven demand materialises.

Client Education and Expectation Management

The shift to upfront assessments requires significant client education, particularly for sellers who may be unfamiliar with commissioning surveys before marketing properties. Effective communication strategies include:

- Cost-benefit analysis: Demonstrating how upfront surveys can attract serious buyers and reduce fall-through rates

- Scope clarity: Explaining what assessments will and won't cover to manage liability expectations

- Timing guidance: Advising on optimal survey timing relative to marketing plans

- Valuation context: Providing market context for valuations in volatile conditions

For buyers, education focuses on interpreting upfront assessments and understanding when additional investigation may be warranted. A seller-commissioned Level 2 survey might provide sufficient information for a standard property, but buyers of older or unusual properties may still benefit from commissioning their own RICS Building Survey for additional peace of mind.

Professional Indemnity and Liability Considerations

Upfront assessments commissioned by sellers but relied upon by buyers create novel liability considerations that require careful professional indemnity insurance review. Key issues include:

- Duty of care: Clarifying to whom the surveyor owes professional duties

- Limitation of liability: Establishing clear caps and exclusions in engagement terms

- Reliance statements: Documenting which parties may rely on the assessment

- Update protocols: Defining circumstances requiring valuation revalidation

Surveyors should work with their professional indemnity insurers to ensure coverage adequately addresses these reformed market dynamics. RICS guidance on liability management will likely evolve as implementation details become clearer.

Specialisation Opportunities

The reformed market creates opportunities for surveyors to develop specialised expertise in niche areas:

- New-build snagging: Comprehensive snagging reports for developers marketing new properties

- Heritage properties: Specialist assessments for listed buildings and conservation areas

- Leasehold assessments: Evaluating shared ownership and leasehold properties

- Commercial conversions: Assessing residential conversions from commercial buildings

- Sustainability ratings: EPC assessments and energy efficiency recommendations

Developing recognised expertise in these areas can differentiate practices in an increasingly competitive market and command premium fees for specialist knowledge.

Challenges and Considerations

While the proposed reforms offer significant opportunities, they also present substantial challenges that the industry must address for successful implementation.

Capacity Constraints and Workforce Shortages

The surveying profession faces a demographic challenge with an ageing workforce and insufficient new entrants to replace retiring professionals. If reforms dramatically increase demand for upfront assessments, capacity constraints could manifest as:

- Extended wait times for survey appointments

- Upward fee pressure potentially pricing out some sellers

- Quality compromises as practices stretch resources

- Geographic disparities with rural areas particularly underserved

RICS's workforce development initiatives aim to address these constraints, but building professional capacity takes years, not months. This is why the institution has requested a 24-month minimum implementation period.[5]

Cost Allocation and Market Acceptance

A fundamental question remains: who pays for upfront assessments? If sellers bear the cost, there's concern that:

- Some sellers may delay listing properties to avoid upfront costs

- Lower-value properties may face proportionally higher assessment costs

- Sellers may pressure surveyors for favourable valuations

- Properties requiring multiple surveys (after fall-throughs) create duplicated costs

Alternative models include:

- Buyer reimbursement: Successful buyers reimburse sellers for assessment costs

- Shared costs: Sellers and buyers split assessment fees

- Packaged fees: Conveyancers bundle assessment costs into overall transaction fees

Market acceptance of upfront assessments will depend heavily on how cost allocation is structured and whether participants perceive value from earlier information availability.

Valuation Disputes and Renegotiation

Even with upfront assessments, valuation disputes may still arise when:

- Market conditions change between assessment and offer

- Buyers commission additional surveys revealing new issues

- Mortgage lenders' valuations differ from upfront assessments

- Sellers disagree with condition ratings or repair cost estimates

The reformed process may reduce but not eliminate these disputes. Clear protocols for handling valuation differences and updating assessments will be essential. Understanding valuation costs and the factors influencing them helps all parties maintain realistic expectations.

Integration with Conveyancing Process

Successful reform implementation requires seamless integration between upfront assessments and the broader conveyancing process. This includes:

- Digital platforms enabling easy survey sharing between parties

- Standardised data formats for integration with property portals

- Clear protocols for updating legal documentation based on survey findings

- Coordination between surveyors, conveyancers, and mortgage lenders

Technology infrastructure development will be critical to achieving this integration, requiring investment from multiple industry stakeholders beyond just surveying practices.

Conclusion

The proposed Valuation Surveys for Upfront Property Condition Assessments: RICS Playbook Under 2026 Homebuying Reforms represents a watershed moment for the UK property market and surveying profession. While implementation timelines remain uncertain as government reviews consultation feedback, the direction of travel is clear: property transactions are moving toward greater transparency, earlier information provision, and reduced fall-through rates.

For chartered surveyors, this transformation creates both significant opportunities and substantial challenges. Practices that proactively invest in capacity building, technology infrastructure, and professional development will be best positioned to capitalise on increased demand for upfront assessments. Those that maintain high professional standards, embrace RICS guidance, and develop sophisticated valuation adjustment techniques for volatile markets will build competitive advantages in the reformed landscape.

The market context of 2026—characterised by regional divergence, modest price growth, and recovering lending volumes—demands careful calibration of valuation methodologies and transparent communication of market assumptions. Surveyors must balance technical rigour with accessibility, producing reports that serve multiple audiences while maintaining Red Book compliance and managing professional liability.

Actionable Next Steps

For surveying practices:

- Review capacity and capability: Assess current workforce capacity and identify gaps that need addressing before reforms take effect

- Invest in technology: Implement digital survey platforms, inspection tools, and data analytics capabilities

- Engage with RICS guidance: Participate in consultations and stay current with evolving professional standards

- Develop standardised processes: Create templates and workflows for upfront assessments that can scale efficiently

- Strengthen professional indemnity coverage: Review insurance policies with brokers to ensure adequate protection for reformed market dynamics

For property professionals:

- Educate clients proactively: Begin conversations with sellers and buyers about potential reform impacts

- Build collaborative networks: Strengthen relationships between surveyors, conveyancers, and mortgage brokers

- Monitor market developments: Stay informed about government announcements and implementation timelines

- Trial upfront assessments: Consider voluntarily offering upfront surveys on selected properties to test market response

For homebuyers and sellers:

- Understand survey options: Learn about different types of surveys and their appropriate applications

- Budget for assessments: Factor survey costs into property transaction planning

- Choose qualified professionals: Work with RICS-registered valuers who understand reformed market requirements

- Request clarity: Ask surveyors about their experience with upfront assessments and reporting standards

The journey toward reformed homebuying in the UK is underway, even if the destination timeline remains unclear. By understanding the RICS playbook, embracing professional standards, and preparing proactively for structural market changes, surveyors and property professionals can help ensure that reforms deliver their intended benefits: faster transactions, fewer fall-throughs, and more informed decision-making for all market participants.

References

[1] Surveying In 2026 Reform Recovery And Renewed Demand – https://www.lrg.co.uk/news-and-insights/surveying-in-2026-reform-recovery-and-renewed-demand/

[2] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[3] Homebuying Process Reforms 2026 Impact On Early Building Surveys And Valuation Timing – https://nottinghillsurveyors.com/blog/homebuying-process-reforms-2026-impact-on-early-building-surveys-and-valuation-timing

[4] Uk Rics Residential Market Survey Mar 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-mar-2026

[5] Home Buying And Selling Reform Hub – https://www.rics.org/news-insights/current-topics-campaigns/home-buying-and-selling-reform-hub

[6] Valuation Adjustments For March 2026 Rics Survey Navigating Softer House Prices And Middle East Conflict Impacts – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-march-2026-rics-survey-navigating-softer-house-prices-and-middle-east-conflict-impacts