{"cover":"Professional landscape format (1536×1024) hero image with bold text overlay: 'Mortgage Rates & UK Valuations: What Borrowers Must Know in 2026' in extra large 72pt white bold sans-serif font with deep shadow and semi-transparent dark overlay box, centered upper-third composition. Background shows a dramatic wide-angle shot of a UK residential street with Georgian terraced houses, a SOLD sign, and a blurred surveyor holding a clipboard in the foreground. Color palette: deep navy blue, crisp white, gold accent lines. Magazine cover aesthetic, editorial quality, high contrast, cinematic lighting.","content":["Detailed landscape format (1536×1024) editorial infographic-style illustration showing a split-screen composition: left side displays a rising mortgage rate graph with a bold red upward arrow overlaid on a Bank of England building silhouette, right side shows a UK property valuation report with downward-pointing green arrows and percentage figures. Central dividing element is a large percentage symbol. Color scheme: navy, red, white. Clean financial data visualization aesthetic, professional editorial quality, mortgage rate impact on UK property valuations theme.","Detailed landscape format (1536×1024) documentary-style scene showing a RICS-certified surveyor in a high-visibility vest standing inside a UK period property, holding a tablet displaying comparable sales data and LTV ratio charts. The surveyor examines a crack in a wall while a nervous homeowner watches in the background. Warm interior lighting contrasts with data overlays showing down-valuation statistics and lender criteria checklists. Color palette: warm amber, charcoal grey, white text overlays. Editorial quality, realistic property inspection atmosphere.","Detailed landscape format (1536×1024) strategic overhead flat-lay composition on a dark oak desk showing: a UK mortgage application form, a red-stamped DOWN VALUATION notice, a RICS valuation report booklet, a calculator showing LTV percentages, a miniature house model, and scattered coins. A hand holds a pen poised over the application. Soft directional studio lighting with sharp shadows. Color scheme: deep charcoal, cream paper tones, red accent stamps. High-contrast editorial quality, financial planning and borrower strategy theme."]

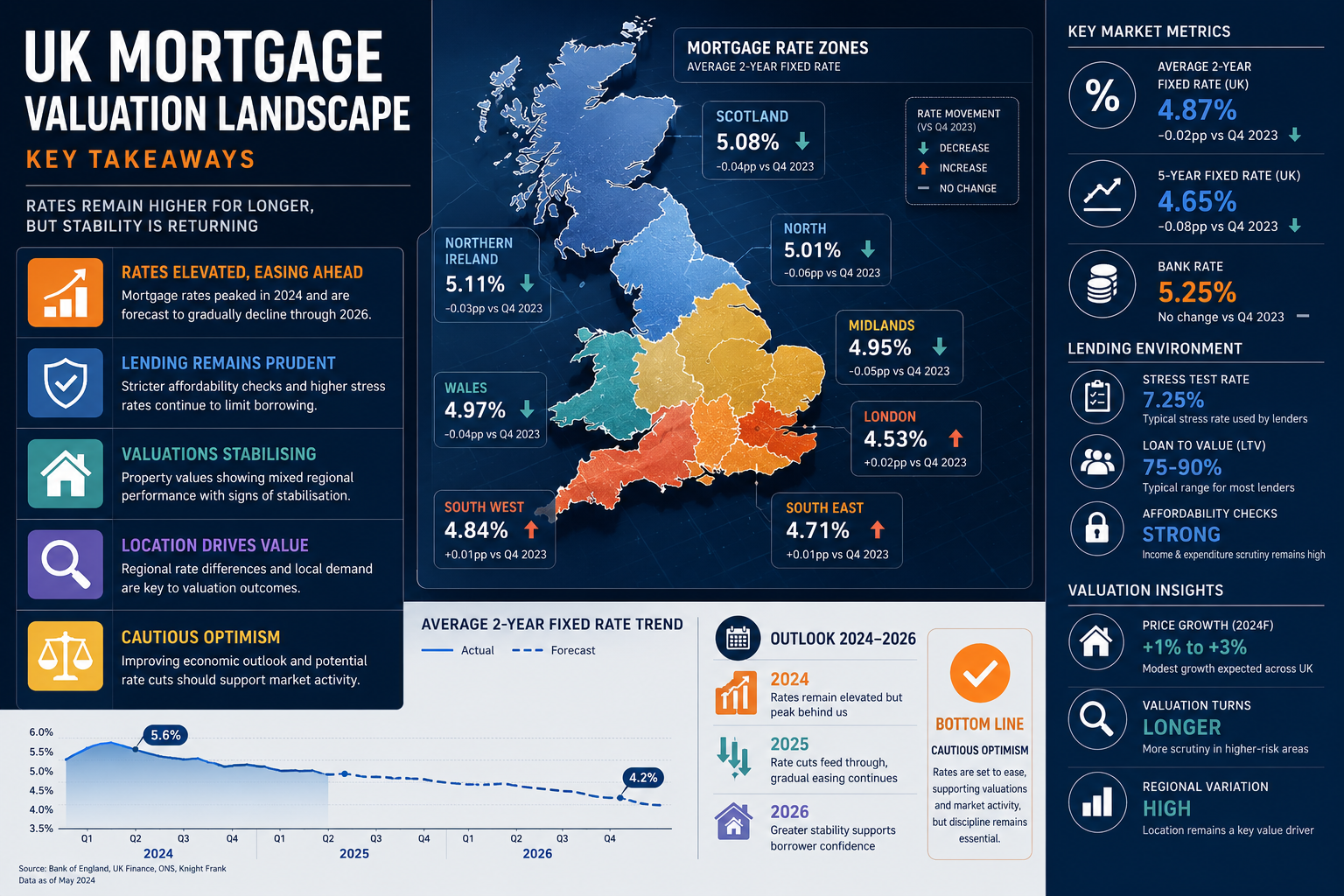

The average two-year fixed mortgage rate climbed from 4.85% in February 2026 to 5.75% by mid-May — a jump of nearly a full percentage point in just three months [1]. For borrowers already stretched by the cost of living, that shift can be the difference between a deal completing and collapsing. Understanding how mortgage rate changes and lending criteria affect UK valuations is no longer just useful knowledge for finance professionals — it is essential for anyone buying, selling, or remortgaging property in 2026.

Key Takeaways 📌

- Rising mortgage rates reduce buyer affordability, shrinking the pool of active purchasers and pushing valuations downward.

- Lenders instruct surveyors using specific criteria, and those criteria tighten when economic conditions are uncertain.

- Down-valuations — where a surveyor values a property below the agreed sale price — are more common when market sentiment is fragile and comparable evidence is limited.

- New regulatory frameworks like Basel 3.1 are reshaping how lenders and valuers approach "prudently conservative" appraisals.

- Buy-to-let and commercial borrowers face additional complexity, with portfolio-level assessments and evolving LTV caps changing what a valuation needs to support.

The Rate-Valuation Connection: Why Borrowing Costs Shape Property Prices

At its core, a property is worth what a willing buyer can pay. When mortgage rates rise, monthly repayments increase, and the maximum purchase price a buyer can afford falls. That reduced affordability directly compresses demand — and where demand falls, so do valuations [5].

The Bank of England held its base rate at 3.75% throughout the start of 2026, with analysts ruling out near-term cuts due to persistent inflation driven by energy and transport costs linked to ongoing geopolitical tensions in the Middle East [1]. Lenders price their fixed-rate products above this base using swap rates, which themselves spiked following global market volatility in early 2026. The result: higher mortgage costs for borrowers, and a more cautious mood across the UK housing market.

💬 Pull Quote: "When rates rise sharply, surveyors do not simply rubber-stamp the agreed sale price. They look at what a buyer can realistically borrow — and the math often tells a different story."

This dynamic matters for valuations because mortgage lenders commission their own valuations — separate from any survey a buyer might arrange — to confirm the property offers adequate security for the loan. If the surveyor concludes the market value is lower than the agreed price, the lender may reduce the loan offer. That is a down-valuation, and it can derail a purchase at the final stage.

Understanding the factors that influence a property valuation helps borrowers anticipate where a surveyor's assessment might diverge from an estate agent's asking price.

How Surveyors Incorporate Lender Guidance, Local Evidence, and Market Expectations

The Surveyor's Methodology in a Shifting Market

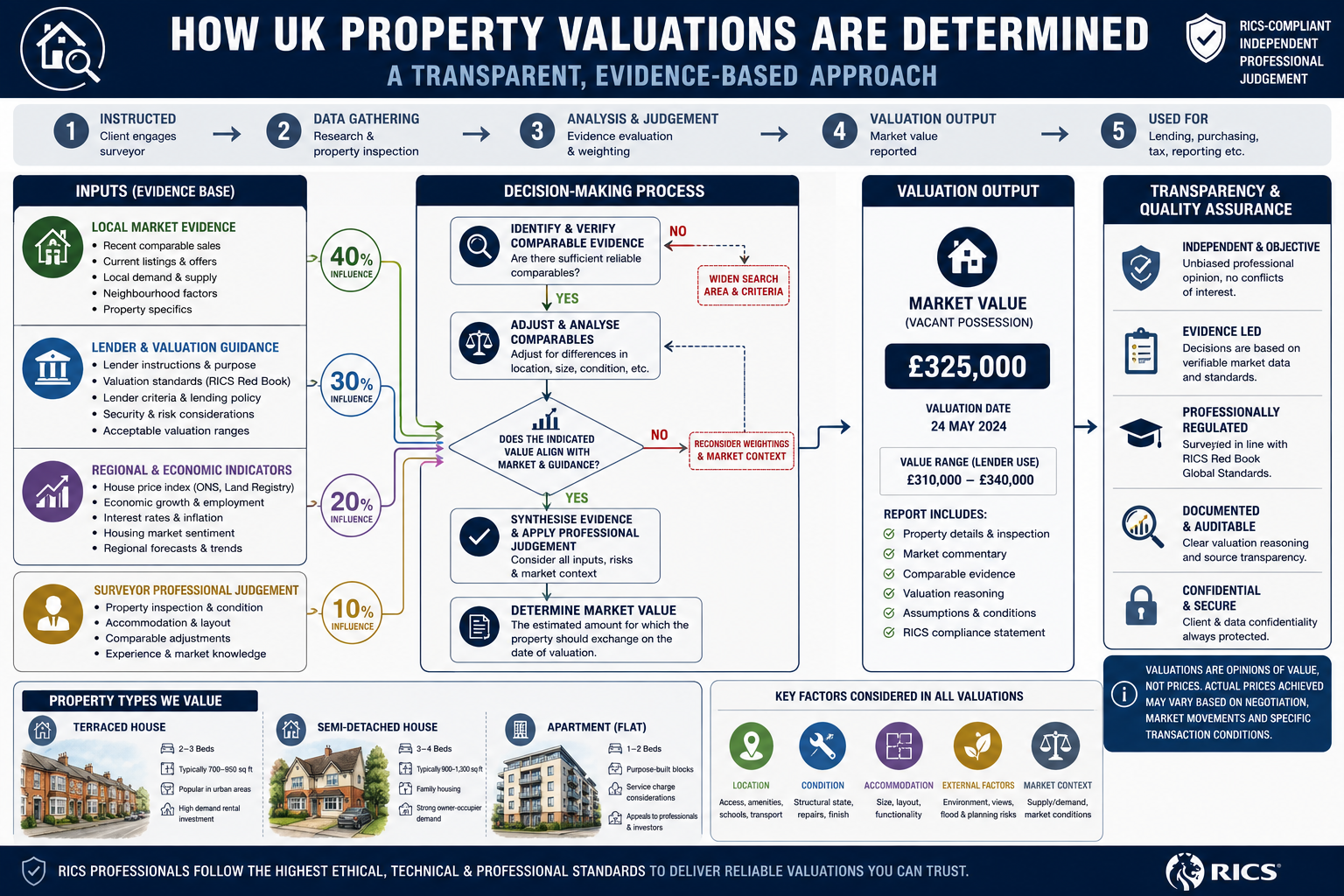

When a lender instructs a surveyor to carry out a mortgage valuation, they do not simply ask for an opinion. They provide a framework of criteria — including acceptable LTV ratios, property types they will and will not lend against, and sometimes specific guidance on how to treat certain markets or property categories.

Surveyors then layer three types of evidence on top of that framework:

| Evidence Type | What It Includes | Why It Matters |

|---|---|---|

| Comparable sales | Recent sold prices for similar properties nearby | Anchors the valuation to real market transactions |

| Local market conditions | Demand levels, time on market, price trends | Indicates whether prices are rising, stable, or falling |

| Future market expectations | Anticipated rate changes, economic outlook | Adjusted cautiously — especially under Basel 3.1 rules |

The third category is where things get complicated. Under proposed Basel 3.1 prudently conservative valuation criteria, valuations used for mortgage lending purposes should exclude speculative expectations of future price increases [4]. In plain terms: a surveyor cannot justify a high valuation on the basis that prices might keep rising. They must ground the figure in current, verifiable evidence.

This is a significant shift. In a rising market, surveyors have historically allowed some forward-looking optimism to inform their figures. In a flat or uncertain market — exactly the conditions seen in parts of the UK in 2026 — that latitude disappears. The RICS Red Book valuation standards underpin this approach, requiring valuers to apply rigorous, evidence-based methodology regardless of what buyers or sellers believe a property is worth.

Why Down-Valuations Cluster in Flat Markets 📉

Mortgage brokers have flagged a notable increase in down-valuations, particularly across London and the South East, with some properties being valued as much as 10% below the agreed sale price [3]. This is not random. Down-valuations cluster in specific conditions:

- Thin comparable evidence — when few similar properties have sold recently, surveyors have less data to support a high figure

- Motivated sellers and optimistic buyers — agreed prices can drift above true market value when a seller is in a hurry or a buyer is emotionally attached

- Lender caution — when lenders tighten their criteria, surveyors instructed by those lenders apply a more conservative lens

- Flat sentiment — even when prices are not falling, a market where activity is subdued gives surveyors little reason to stretch their figures

For buyers, understanding this mechanism is critical. A professional RICS valuation commissioned independently — before agreeing a purchase price — can provide a realistic benchmark and reduce the risk of a lender's valuation coming in lower than expected.

Lending Criteria Changes in 2026: What Borrowers Are Facing

New-Build Properties and LTV Caps

One of the most significant lending criteria changes in 2026 came from specialist lenders updating how they treat new-build properties. RAW Capital Partners, for example, revised its approach to lend on current market value for new-build homes at a maximum LTV of 65%, removing the previous practice of deducting a "new-build premium" from the valuation [2]. This matters because new-build properties have historically attracted a premium — sometimes 10–15% above equivalent second-hand stock — that lenders were reluctant to fully recognise.

For buyers of new-build homes, the practical implication is straightforward: the deposit required may be larger than expected if the lender's valuation does not match the developer's asking price. Borrowers considering shared ownership valuations or Help to Buy schemes should be especially alert to how lender criteria interact with scheme-specific valuation rules.

Commercial and Buy-to-Let: A More Complex Picture

Commercial lending criteria have also evolved. InterBay updated its commercial and semi-commercial lending parameters in early 2026, offering up to 75% LTV based on market value and removing minimum lease period requirements for income-producing properties [6]. While this increases flexibility for some borrowers, it also means valuations must now support a wider range of scenarios — and surveyors are expected to assess income sustainability more rigorously.

For buy-to-let landlords, the challenge is even more layered. Lenders now assess portfolio-level risk rather than individual properties in isolation, considering total borrowing, aggregate LTV, and rental income coverage across the entire portfolio [7]. A single property that looks fine on its own may create problems when assessed alongside other mortgaged assets. This has made remortgaging more complex and has increased the importance of getting accurate, up-to-date valuations across the whole portfolio.

💬 Pull Quote: "A buy-to-let borrower with five properties is no longer assessed on one deal at a time. The whole portfolio is under the microscope — and so is every valuation underpinning it."

In the commercial real estate sector, lower valuations combined with higher interest rates are creating pressure on both loan-to-value ratios and interest cover ratios [9]. Borrowers who secured commercial loans when rates were lower and values were higher may find themselves in breach of loan covenants when properties are revalued — a risk that makes professional, independent valuations more important than ever.

Key Lending Criteria Changes at a Glance 🔍

- ✅ New-build LTV capped at 65% by some specialist lenders (RAW Capital Partners)

- ✅ Commercial LTV up to 75% with relaxed lease requirements (InterBay)

- ✅ Portfolio-level assessment now standard for buy-to-let borrowers

- ✅ Basel 3.1 pushing for "prudently conservative" valuations that exclude speculative price growth

- ✅ Swap rate volatility feeding directly into fixed-rate mortgage pricing

What Borrowers Should Do: Practical Steps to Protect Your Position

Before Agreeing a Purchase Price

The single most effective thing a buyer can do is commission an independent valuation before exchanging contracts. This gives a realistic view of what a lender's surveyor is likely to conclude — and avoids the costly scenario of a down-valuation emerging only after solicitor fees have been paid.

A Manchester property valuation or equivalent regional assessment from a RICS-registered firm provides a defensible, evidence-based figure that can inform negotiation with the seller.

Understanding the Difference Between a Mortgage Valuation and a Survey

Many borrowers confuse the lender's mortgage valuation with a full structural survey. They are not the same thing:

- A mortgage valuation is brief, completed for the lender's benefit, and confirms only that the property is adequate security for the loan amount

- A RICS Home Survey or building survey is far more detailed, identifies defects, and is commissioned for the buyer's benefit

Getting both is advisable, particularly for older properties or those with visible defects. A RICS building survey can reveal structural issues that — if flagged in a mortgage valuation — might cause the lender to reduce the loan offer or add conditions.

If a Down-Valuation Occurs

Down-valuations are not the end of a transaction. Borrowers have several options:

- Challenge the valuation — provide comparable sales evidence to the lender and request a review

- Renegotiate with the seller — use the down-valuation as leverage to reduce the agreed price

- Increase the deposit — bridge the gap between the lender's valuation and the agreed price with additional funds

- Switch lenders — a different lender may instruct a different surveyor who reaches a different conclusion

The valuation costs involved in commissioning an independent second opinion are often modest relative to the sums at stake in a property transaction — and can be decisive in resolving a dispute.

For Remortgaging Borrowers

Those remortgaging — particularly on buy-to-let or commercial properties — should prepare for a more rigorous process in 2026. Ensuring properties are well-maintained, that rental income is documented, and that the portfolio's overall LTV is within acceptable bounds will all strengthen the position when a lender's surveyor visits. Working with a remortgage conveyancer who understands current lender criteria can also smooth the process considerably.

The Bigger Picture: Regulation, Sentiment, and the Road Ahead

The convergence of higher mortgage rates, tighter lending criteria, and incoming regulatory changes like Basel 3.1 is reshaping the UK property market in ways that are not always visible at street level. Valuers are under more pressure than at any point in recent years to justify their figures with hard evidence — and lenders are less willing to stretch criteria to make deals work.

For borrowers, this environment demands greater preparation and financial literacy. The days of assuming that an agreed sale price will automatically be supported by a lender's valuation are over — at least while rates remain elevated and market sentiment is only gradually recovering.

Market value, as a concept, has always reflected what a willing buyer will pay and a willing seller will accept under normal conditions [10]. When those conditions are distorted by rate shocks, geopolitical uncertainty, or regulatory change, the gap between asking prices and lender-supported values widens. That gap is where down-valuations live — and understanding it is the first step to navigating it successfully.

Conclusion: Actionable Next Steps for Borrowers in 2026

Understanding how mortgage rate changes and lending criteria affect UK valuations is not a passive exercise — it requires active preparation. Here is what borrowers should do right now:

- Commission an independent RICS valuation before agreeing a purchase price, especially in markets where recent comparable sales are sparse

- Check lender-specific LTV criteria for the property type being purchased — new-build, commercial, and shared ownership all carry different rules

- Review portfolio-level exposure if remortgaging a buy-to-let portfolio, and ensure rental income documentation is current

- Do not confuse a mortgage valuation with a structural survey — get both for full protection

- Challenge down-valuations with evidence — a well-prepared comparable sales pack can overturn a conservative assessment

- Monitor rate movements — even a 0.5% change in mortgage rates can shift the maximum affordable purchase price by thousands of pounds

The property market in 2026 rewards the prepared. Borrowers who understand the mechanics of valuation — and the pressures that lenders and surveyors are operating under — are far better placed to protect their transactions and their financial interests.

References

[1] Latest UK Mortgage Rates – https://moneyweek.com/personal-finance/mortgages/latest-UK-mortgage-rates?utm_source=openai

[2] Raw Capital Partners Updates New Build Lending Criteria – https://theintermediary.co.uk/2026/03/raw-capital-partners-updates-new-build-lending-criteria/?utm_source=openai

[3] Mortgage Lenders House Buying Surveyor Down Valuing – https://www.theguardian.com/money/2025/nov/22/mortgage-lenders-house-buying-surveyor-down-valuing?utm_source=openai

[4] Basel 3.1 Prudently Conservative Valuation Criteria – https://ww3.rics.org/uk/en/journals/property-journal/basel-3-1-prudently-conservative-valuation-criteria.html?utm_source=openai

[5] How Are Rising Mortgage Rates Affecting The UK Housing Market – https://kalkine.co.uk/news/premium/how-are-rising-mortgage-rates-affecting-the-uk-housing-market?utm_source=openai

[6] InterBay Enhances Commercial Criteria To Increase Flexibility For Brokers – https://theintermediary.co.uk/2026/03/interbay-enhances-commercial-criteria-to-increase-flexibility-for-brokers/?utm_source=openai

[7] Why Remortgaging A Buy To Let Portfolio Is Harder Than Expected In 2026 – https://www.willowprivatefinance.co.uk/why-remortgaging-a-buy-to-let-portfolio-is-harder-than-expected-in-2026?utm_source=openai

[8] Valuation Adjustments For Mortgage Rate Changes How 2026 Rate Cuts Impact Building Survey Recommendations – https://wimbledonsurveyors.com/valuation-adjustments-for-mortgage-rate-changes-how-2026-rate-cuts-impact-building-survey-recommendations/?utm_source=openai

[9] Financing Headwinds For Commercial Real Estate – https://www.grantthornton.co.uk/insights/financing-headwinds-for-commercial-real-estate/?utm_source=openai

[10] Market Value – https://www.finbri.co.uk/glossary/real-estate/property-transactions/valuations/market-value?utm_source=openai