{"cover":"Professional landscape format (1536×1024) hero image with bold text overlay: 'Valuation Challenges in Spring 2026: RICS February Data Insights for Surveyors' in extra large 70pt white bold sans-serif font with dark semi-transparent overlay box, centered upper-third composition. Background shows a wide-angle view of a UK residential street with Victorian terraced houses in soft spring light, overlaid with a subtle downward-trending graph line in red and a RICS logo watermark. Color palette: deep navy blue, white text, red accent arrows. Magazine cover aesthetic, editorial quality, high contrast, professional property surveying theme.","content":["Detailed landscape format (1536×1024) infographic-style image showing a split UK map with regional heat zones: London and South East in cool blue tones indicating price decline (-40% and -24% net balance labels), Northern Ireland and North West in warm amber tones showing firmer trends. Central panel displays a bar chart with February 2026 buyer enquiry net balance at -26% dropping to -39% in March 2026, with annotated RICS data labels. Clean financial data visualization aesthetic, white background, navy and red color scheme, property surveying context, editorial quality.","Landscape format (1536×1024) close-up aerial overhead shot of a professional RICS-registered surveyor at a large oak desk reviewing printed valuation reports and comparable evidence folders, with a laptop showing declining market trend graphs, a red-stamped 'Material Uncertainty Clause' document visible, a calculator, and sticky notes reading 'Adjust Comps' and 'Review Assumptions'. Warm office lighting, shallow depth of field, professional surveying environment, muted tones with red accent highlights, editorial documentary photography style.","Landscape format (1536×1024) conceptual split-scene image: left half shows a 'For Sale' sign outside a UK terraced house with a padlock symbolizing frozen buyer activity and an empty open house; right half shows a forward-looking calendar marked '12 Months Ahead' with an upward green arrow and positive sentiment icons. Between the two halves, a vertical timeline bar labeled 'Spring 2026' with sentiment indicators transitioning from red caution to amber recovery. Clean editorial illustration style, professional property market theme, navy, green, and red color palette, high contrast."]

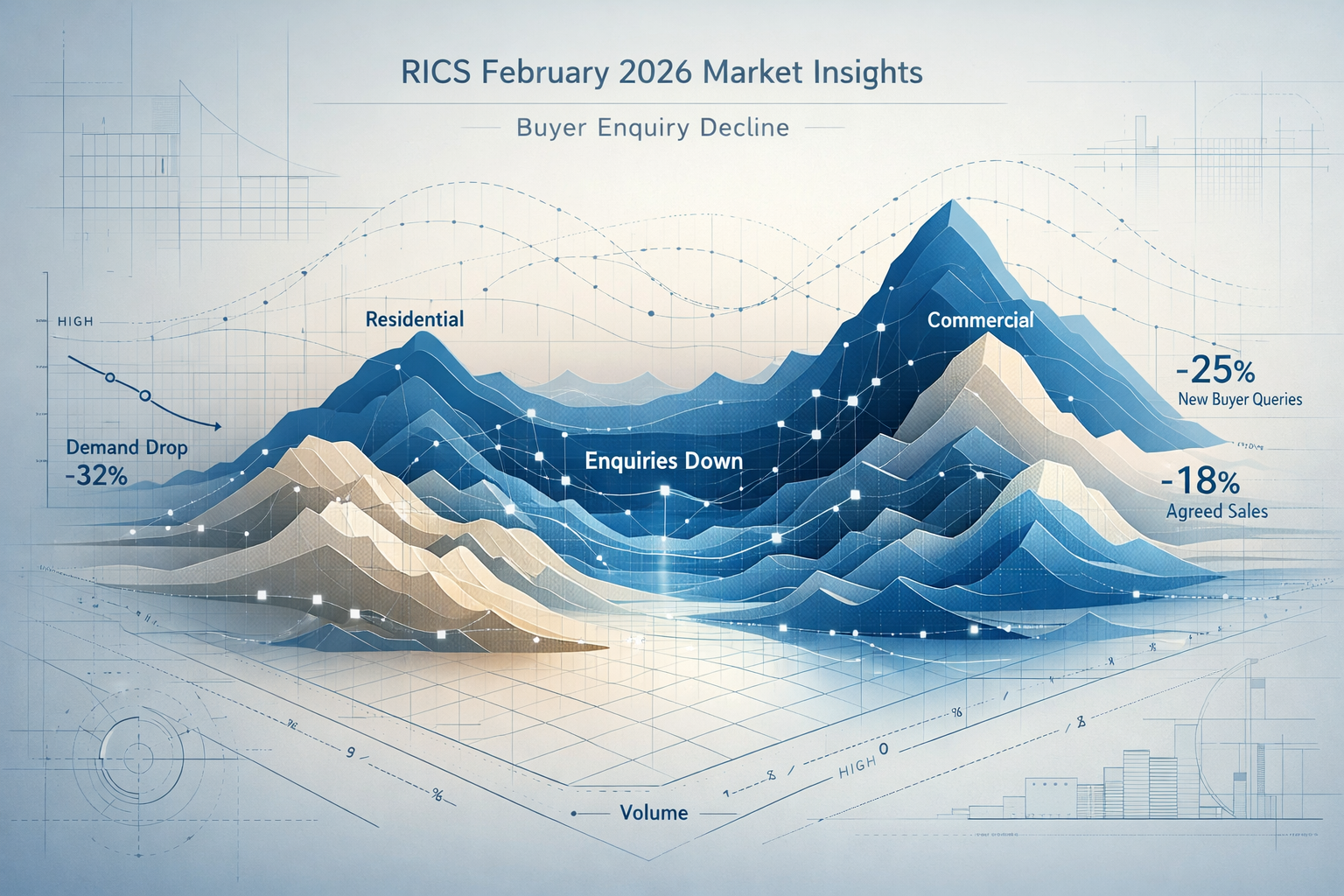

Buyer enquiries collapsed to a net balance of -26% in February 2026 — and then fell even further to -39% in March. For property surveyors, that is not just a headline statistic. It is a direct signal that the comparable evidence underpinning valuations is thinning out fast, and that standard methodologies may no longer be sufficient to produce defensible figures.

The Valuation Challenges in Spring 2026 Market Caution: RICS February Data Insights for Surveyors Adjusting Valuations Amid Buyer Enquiry Decline represent one of the most complex operating environments for RICS-registered valuers since the pandemic era. With near-term price expectations dropping to -18%, regional markets diverging sharply, and geopolitical uncertainty feeding into mortgage rate anxiety, surveyors must now go beyond routine adjustments and implement structured, transparent valuation protocols [1][2].

This article unpacks the RICS February 2026 data in detail, explains what it means for valuation practice, and provides practical guidance for surveyors navigating a cautious spring market.

Key Takeaways 📌

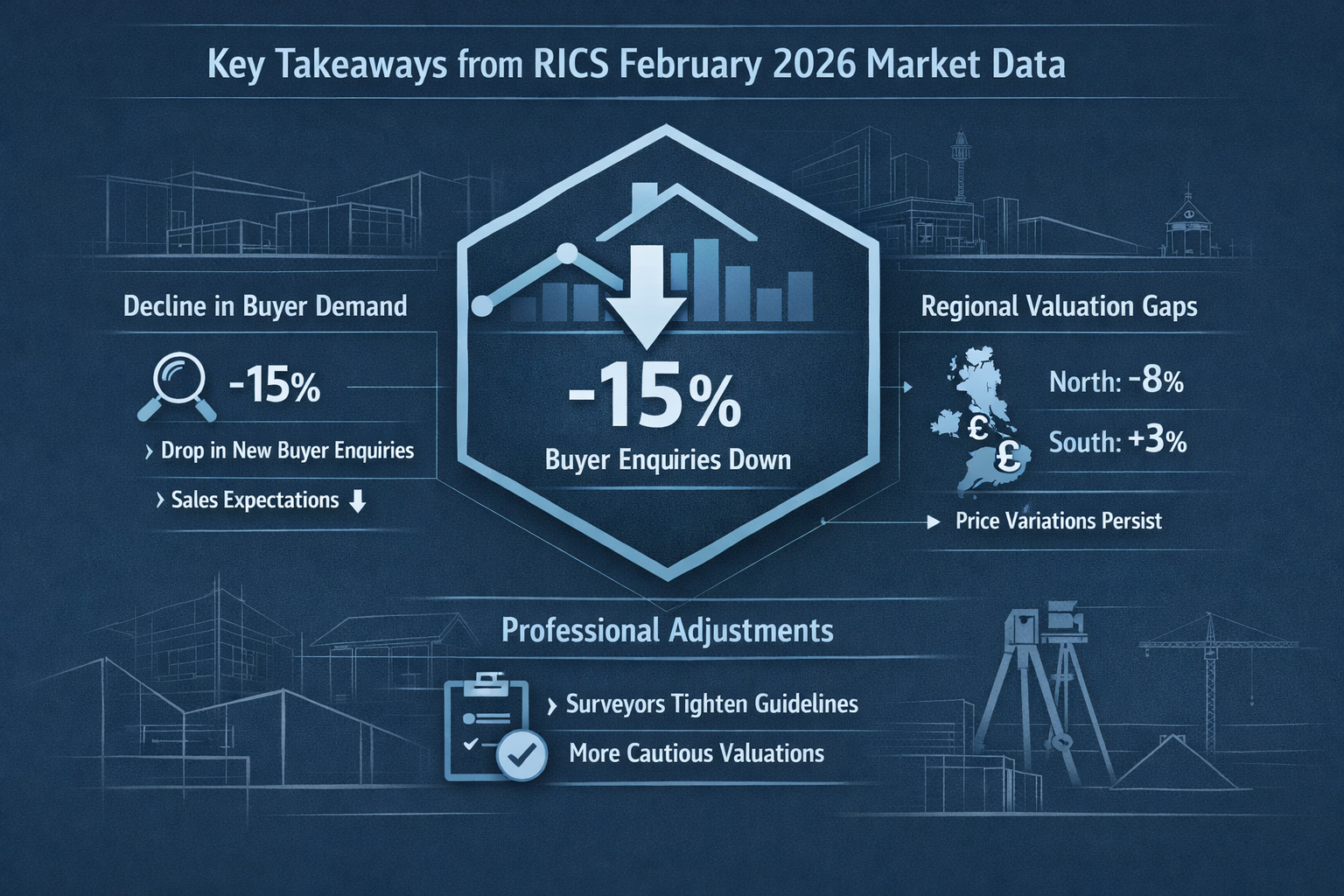

- Buyer enquiries fell to -26% in February 2026, accelerating to -39% in March — reducing the volume of comparable transaction evidence available to valuers [1]

- Regional divergence is extreme: London price balance hit -40%, while Northern Ireland and the North West remain comparatively firm, requiring region-specific valuation protocols [1][3]

- Near-term price expectations dropped to -18%, but the 12-month outlook holds at +33%, creating a bifurcated market that demands careful interpretation [1]

- RICS guidance requires surveyors to implement material uncertainty clauses in volatile conditions — standard caveats are no longer sufficient [4]

- Agreed sales posted -12% and rental landlord instructions remained at -27%, compressing both transaction and investment property comparable evidence [1][3]

Understanding the RICS February 2026 Data: What the Numbers Actually Mean

The Buyer Enquiry Collapse in Context

The drop in new buyer enquiries from -15% in January to -26% in February 2026 is not simply a seasonal blip. It represents a fresh deterioration following what had been a tentative early-year improvement in market activity [1]. The subsequent plunge to -39% in March confirms a trend rather than a one-off reading.

For surveyors, the practical consequence is stark: fewer buyers in the market means fewer transactions, and fewer transactions mean less comparable evidence. When the pool of recent sales shrinks, valuers face greater difficulty in anchoring their assessments to robust, current market data [2].

💬 "The first quarter of 2026 has challenged property valuers with unprecedented complexity, extending beyond headline statistics to require reassessment of valuation methodologies and comparable evidence analysis." — Nottingham Hill Surveyors [5]

Agreed Sales and Supply: A Stagnant Pipeline

Agreed sales registered a net balance of -12% in February 2026, with near-term sales expectations weakening to -2% — the softest reading since November 2025 [1][3]. Meanwhile, new instructions remained broadly stable at just +2%, indicating that fresh listings are neither rising nor falling in any meaningful way [1].

This combination — weak demand meeting flat supply — creates a market in suspended animation. Surveyors conducting RICS valuations will find that the usual cadence of transactional evidence has slowed considerably, making it harder to justify specific price points with confidence.

Key February 2026 RICS Data Summary:

| Indicator | February 2026 Net Balance | January 2026 Net Balance |

|---|---|---|

| New Buyer Enquiries | -26% | -15% |

| Agreed Sales | -12% | — |

| Near-Term Price Expectations | -18% | -6% |

| 12-Month Price Expectations | +33% | — |

| New Instructions | +2% | — |

| Landlord Instructions | -27% | — |

| Near-Term Sales Expectations | -2% | — |

Source: RICS UK Residential Market Survey, February 2026 [1][3]

Geopolitical Drivers Behind Market Caution

The RICS report identifies geopolitical uncertainty — particularly Middle East conflict escalation — as a key driver of short-term market hesitancy. Rising oil and energy prices have increased the likelihood that mortgage rates will remain elevated for longer, dampening buyer confidence and affordability [1][3].

This macroeconomic backdrop has direct implications for valuation methodology. When external shocks introduce genuine uncertainty about future borrowing costs, surveyors cannot simply rely on recent comparable sales that were agreed under different rate expectations. The conditions that produced those transactions may no longer apply [4].

Regional Divergence and the Valuation Challenges in Spring 2026 Market Caution: RICS February Data Insights for Surveyors Adjusting Valuations Amid Buyer Enquiry Decline

London and the South: Significant Downward Pressure

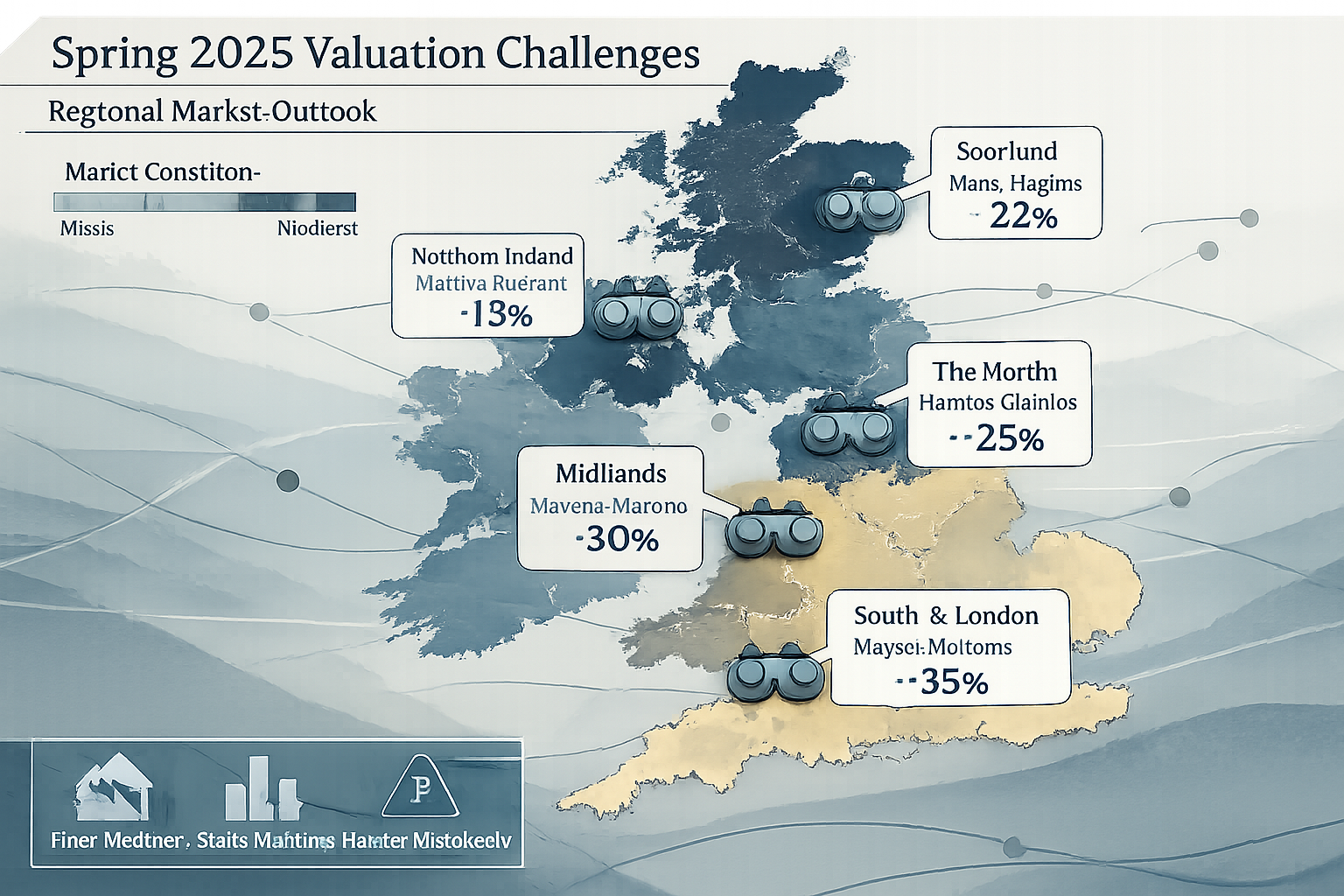

The regional picture emerging from the RICS February 2026 data is one of sharp fragmentation. London recorded a house price net balance of -40% — the most negative reading of any UK region. The South East followed at -24%, and East Anglia registered -26% [1][3].

These are not marginal softening signals. They represent a fundamental repricing dynamic in markets that had previously been supported by strong demand and limited supply. For surveyors working in central London, south west London, or Berkshire, this data demands a recalibration of how comparable evidence is weighted and applied.

Critically, London's 12-month price balance dropped to just +7% — down from +56% in the previous reading [1][3]. This dramatic compression of longer-term optimism suggests that even recovery scenarios must be modelled more conservatively than before.

Northern Markets: Relative Resilience

In contrast, Northern Ireland, Scotland, and the North West are showing firmer trends. This regional resilience reflects a combination of lower absolute price levels, stronger affordability ratios, and less exposure to the mortgage rate sensitivity that is weighing on southern markets [1][3].

For surveyors operating in the North West, this divergence is both an opportunity and a responsibility. The temptation to apply national benchmarks to regional valuations must be resisted. A property in Manchester or Liverpool operates in a fundamentally different market environment from one in Guildford or Hertfordshire right now.

Why Regional Fragmentation Complicates National Benchmarking

The practical challenge for valuers is that national averages mask extreme local variation. When a surveyor is asked to value a property in a region experiencing -40% price pressure, applying a national net balance of -12% would produce a materially misleading result.

Surveyors should consider the following regional adjustment framework:

- 🔴 High caution zones (London, South East, East Anglia): Apply material uncertainty clauses; weight recent comparables heavily; consider downward adjustments to listings-based evidence

- 🟡 Moderate caution zones (East Midlands, West Midlands, South West): Standard enhanced protocols; verify comparable currency carefully

- 🟢 Firmer zones (North West, Scotland, Northern Ireland): Standard methodology with heightened awareness of national sentiment spillover

Understanding the full range of factors of valuation becomes especially important when regional conditions diverge this sharply from the national picture.

Adjusting Valuation Methodologies: Professional Protocols for the Valuation Challenges in Spring 2026 Market Caution: RICS February Data Insights for Surveyors Adjusting Valuations Amid Buyer Enquiry Decline

When Standard Caveats Are No Longer Enough

RICS guidance is explicit on this point: in extreme or highly uncertain market conditions, it is "too simplistic merely to include a standard caveat" [4]. Surveyors must implement enhanced protocols that reflect the genuine difficulty of the task — not simply add a boilerplate disclaimer to an otherwise unchanged report.

The precedent for this approach was established during the COVID-19 pandemic, when RICS introduced material uncertainty clauses as a formal mechanism for communicating valuation risk. The February 2026 data suggests that conditions now warrant a similar response, particularly in the most affected regions [4][2].

Implementing Material Uncertainty Clauses

A material uncertainty clause is not an admission of failure. It is a professional and transparent acknowledgement that market conditions have created a wider-than-usual range of plausible values. Key elements of a robust clause include:

- Explicit identification of the uncertainty source — e.g., declining buyer enquiries, geopolitical factors, mortgage rate volatility

- Quantification of the evidence gap — how many comparables were available, how recent they were, and what adjustments were made

- Statement of the assumptions applied — including any special assumptions about market normalisation

- Clear communication of the valuation range — not just a single figure, but a defensible range with stated confidence levels

For surveyors handling valuation for capital gains tax or shared ownership valuations, where precision is legally significant, these clauses take on additional importance.

Adjusting Comparable Evidence in a Thin Market

When transaction volumes fall — as they have in early 2026 — surveyors face a choice between using older comparables (which may not reflect current conditions) or using fewer, more recent ones (which may not be statistically robust). Neither option is ideal. The professional response is to:

- Extend the search radius for comparables while applying explicit time and location adjustments

- Weight active listings and withdrawn properties as secondary evidence of market sentiment

- Cross-reference against RICS survey data as a corroborating macro indicator — precisely the role that the February 2026 data can play [2]

- Document the methodology transparently so that any future challenge can be addressed with a clear audit trail

This approach is particularly relevant for freehold valuations and commercial property valuations, where comparable evidence is already more limited than in the residential sector.

The Bifurcated Market Problem: Near-Term vs. 12-Month Outlook

One of the most technically demanding aspects of the current environment is the disconnect between short-term and long-term market sentiment. Near-term price expectations sit at -18%, yet the 12-month outlook remains at +33% [1]. This gap creates a genuine methodological question: which timeframe should a valuation reflect?

The answer depends on the purpose of the valuation:

| Valuation Purpose | Appropriate Timeframe Weighting |

|---|---|

| Mortgage security | Current market value; near-term bias |

| Capital gains tax | Date of disposal; current conditions |

| Investment appraisal | Longer-term income and capital growth |

| Right to Buy | Current open market value |

| Shared ownership staircasing | Current market conditions |

Surveyors should make this weighting decision explicit in their reports, citing the RICS data as supporting evidence for the chosen approach [2][3].

Rental Market Adjustments: A Separate Challenge

The rental market presents its own valuation complexity. Landlord instructions remained firmly negative at -27% in February 2026, signalling an ongoing shortage of rental stock [1][3]. Despite this constraint, +20% of survey participants expect rents to rise over the coming three months [1].

For surveyors valuing investment properties, this creates a situation where rental income assumptions may need to be revised upward even as capital values face downward pressure. The yield implications are significant and must be modelled carefully, particularly for Help to Buy valuations where affordability calculations depend on accurate current market rents.

Practical Steps for Surveyors in Spring 2026

A Checklist for Defensible Valuations in a Cautious Market ✅

Given the complexity of the current environment, the following checklist provides a structured approach for surveyors:

- Review RICS February 2026 data for the specific region of the subject property before commencing the valuation

- Identify the applicable regional sentiment band (high caution, moderate caution, or firmer zone)

- Assess comparable evidence currency — flag any comparables older than three months as requiring explicit adjustment

- Consider whether a material uncertainty clause is warranted based on local market conditions

- Document the rationale for all adjustments in the valuation report with reference to supporting data sources

- Distinguish between current market value and 12-month forward value in the report narrative

- Apply rental market adjustments separately for investment properties, reflecting the landlord instruction shortage

- Peer review the report where possible before issue, particularly for high-value or legally sensitive instructions

The Role of RICS Data as a Valuation Anchor

One of the most valuable aspects of the RICS monthly survey is that it provides real-time, surveyor-reported data rather than lagged transaction statistics. In a market where buyer enquiries are falling sharply, the RICS net balance figures can serve as a contemporaneous anchor for valuation adjustments — providing the kind of current-conditions evidence that transaction databases cannot yet supply [2][5].

This is particularly important for surveyors who need to justify a downward adjustment from a recent comparable that was agreed under more buoyant conditions. The RICS data provides a transparent, authoritative basis for that adjustment [2].

Conclusion: Navigating Spring 2026 With Precision and Transparency

The Valuation Challenges in Spring 2026 Market Caution: RICS February Data Insights for Surveyors Adjusting Valuations Amid Buyer Enquiry Decline are real, significant, and demanding of a professional response that goes beyond routine practice. The data is clear: buyer enquiries have collapsed, near-term price expectations have turned sharply negative, and regional markets are diverging in ways that make national benchmarking unreliable [1][3].

Yet the 12-month outlook remains positive, and the market is not in freefall. What it requires is precision, transparency, and methodological rigour from every RICS-registered valuer working in it.

Actionable Next Steps for Surveyors:

- Download and review the full RICS February 2026 UK Residential Market Survey before completing any valuation instruction in the current quarter

- Implement material uncertainty clauses for all valuations in high-caution regions, particularly London, the South East, and East Anglia

- Extend comparable evidence searches and document all adjustments with explicit reference to current market conditions

- Distinguish near-term and 12-month valuation scenarios clearly in reports, particularly for investment and mortgage security purposes

- Consult RICS professional guidance on real estate valuation in extreme conditions to ensure compliance with enhanced protocol requirements [4]

- Engage with clients proactively to explain why valuations may differ from recent listing prices or automated model outputs — the RICS data provides the professional basis for that conversation [5]

The surveyors who navigate this period most effectively will be those who treat the current data not as an obstacle, but as a professional tool — using it to produce valuations that are both accurate and defensible in a market that rewards neither complacency nor panic.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Valuation Challenges In Uncertain Markets Using Rics February 2026 Data To Adjust Valuations Amid Geopolitical Volatility And Interest Rate Concerns – https://nottinghillsurveyors.com/blog/valuation-challenges-in-uncertain-markets-using-rics-february-2026-data-to-adjust-valuations-amid-geopolitical-volatility-and-interest-rate-concerns

[3] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Real Estate Valuation Extreme Conditions – https://ww3.rics.org/uk/en/journals/property-journal/real-estate-valuation-extreme-conditions.html

[5] Navigating Uncertainty In Spring 2026 Valuations How Rics Real Time Surveyor Data Outperforms Automated Valuation Models – https://nottinghillsurveyors.com/blog/navigating-uncertainty-in-spring-2026-valuations-how-rics-real-time-surveyor-data-outperforms-automated-valuation-models