The landscape of UK property taxation is shifting dramatically in 2026, and second homeowners face unprecedented financial exposure. With the government's new high-value council tax surcharge targeting properties valued at £2 million or more, precise valuation adjustments have become critical defensive tools. Understanding Valuation Adjustments for 2026 Council Tax Surcharge Risks: Surveyor Strategies for Second Homeowners can mean the difference between paying thousands in unnecessary annual charges or successfully challenging inflated assessments.

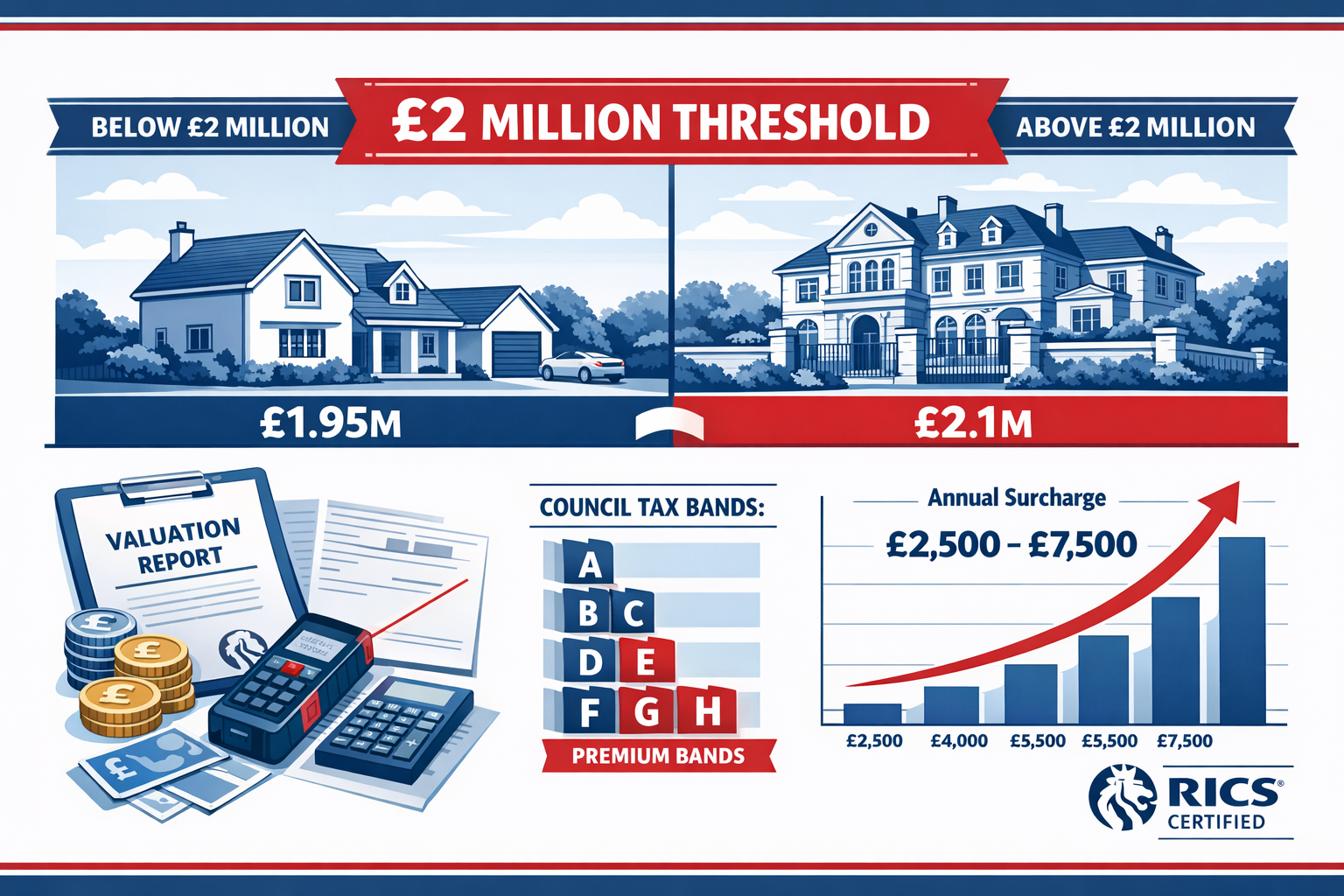

The stakes are substantial: properties crossing the £2 million threshold will incur annual surcharges ranging from £2,500 to £7,500, collected through existing council tax bills starting in April 2028[6]. For second homeowners with properties hovering near this critical valuation point, professional surveyor expertise isn't just advisable—it's essential for protecting asset values and minimizing tax liability.

Key Takeaways

- 🏠 Properties valued at £2 million or more face annual surcharges of £2,500-£7,500 from April 2028, making accurate valuations critical for second homeowners[6]

- 📊 Strategic valuation adjustments can legitimately reduce property assessments through documented evidence of structural defects, market conditions, and location factors

- 🔍 RICS-compliant surveyor strategies provide defensible evidence for challenging inflated valuations and protecting against excessive surcharge liability

- ⏰ Early consultation with chartered surveyors in 2026 allows property owners to prepare comprehensive documentation before the April 2028 implementation

- 💷 The £500 million annual revenue target means local authorities will scrutinize high-value properties intensively, requiring professional valuation support[6]

Understanding the 2026 Council Tax Surcharge Framework

The £2 Million Threshold and Its Implications

Announced in the Autumn Budget 2025, the high-value council tax surcharge represents a fundamental shift in UK property taxation[1]. The policy specifically targets residential properties valued at £2 million or more based on 2026 valuations, creating a sharp dividing line that will significantly impact second homeowners across England.

The surcharge structure operates on a tiered system:

| Property Valuation | Annual Surcharge |

|---|---|

| £2.0m – £3.5m | £2,500 |

| £3.5m – £5.0m | £5,000 |

| £5.0m+ | £7,500 |

Key characteristics of the surcharge include:

- The property owner (not occupier or tenant) bears liability for payment[6]

- Local authorities collect surcharges on behalf of central government through existing council tax bills[1]

- The Office for Budget Responsibility projects approximately £500 million in annual revenue[6]

- A public consultation on implementation details was scheduled for early 2026[8]

For second homeowners, this creates immediate urgency. Properties currently valued between £1.8 million and £2.2 million exist in a critical zone where factors of valuation can determine whether they fall above or below the threshold.

Why Valuation Accuracy Matters for Second Homeowners

Second homeowners face unique vulnerabilities under this regime. Unlike primary residences, second homes often:

- Receive less frequent maintenance and inspection

- Experience market value fluctuations based on location-specific tourism or seasonal demand

- Contain undocumented structural issues that affect true market value

- Face additional local authority premiums already in place for empty or second homes

The combination of existing council tax premiums (which many local authorities already impose on second homes) and the new surcharge creates a compounding tax burden that makes precise valuation critical[2]. A property incorrectly valued at £2.05 million instead of £1.95 million could trigger an unnecessary £2,500 annual charge—£25,000 over a decade.

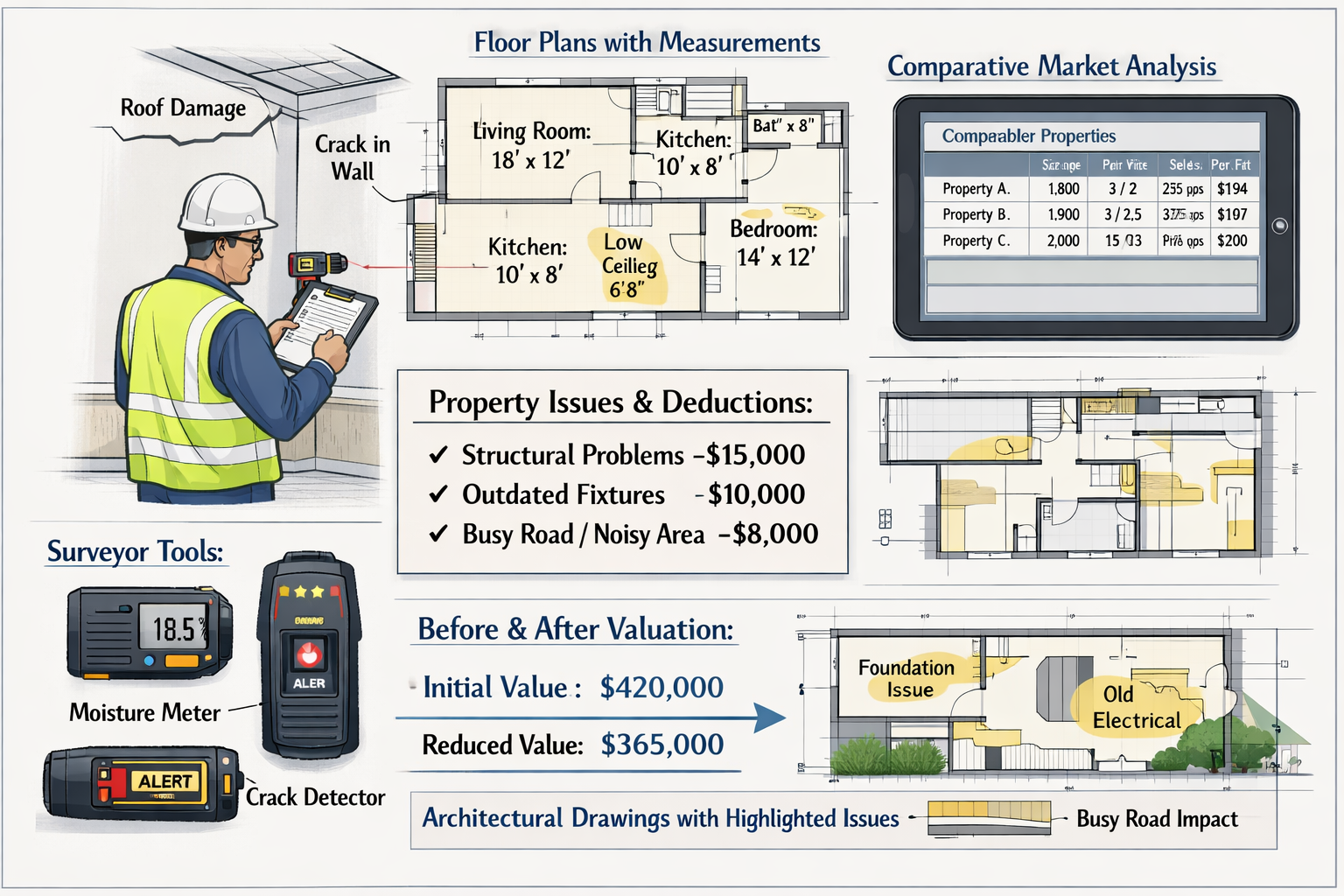

Professional surveyors understand that valuations aren't arbitrary numbers. They represent defensible assessments based on comparable sales, property condition, location factors, and market timing. Strategic engagement with chartered surveyors provides the documentation necessary to challenge inflated assessments.

Valuation Adjustments for 2026 Council Tax Surcharge Risks: Professional Surveyor Methodologies

RICS-Compliant Valuation Approaches

The Royal Institution of Chartered Surveyors (RICS) establishes professional standards that ensure valuations withstand scrutiny from tax authorities. When addressing Valuation Adjustments for 2026 Council Tax Surcharge Risks: Surveyor Strategies for Second Homeowners, RICS-qualified professionals employ several recognized methodologies:

Comparative Method 📊

This approach analyzes recent sales of similar properties in the same area, adjusting for differences in:

- Property size and layout

- Condition and age

- Location advantages or disadvantages

- Market conditions at time of sale

For second homes in premium locations like Hampstead or Richmond, comparable sales data provides the foundation for challenging valuations that don't reflect true market positioning.

Depreciated Replacement Cost

For unique properties without direct comparables, surveyors calculate what it would cost to rebuild the property, then apply depreciation for:

- Physical deterioration

- Functional obsolescence

- Economic obsolescence

Income Capitalization Method

Particularly relevant for second homes with rental income potential, this method values properties based on their income-generating capacity, which may differ significantly from headline market values.

Strategic Deduction Identification

Professional surveyors systematically identify legitimate factors that reduce property valuations. These aren't attempts to manipulate assessments—they're evidence-based adjustments that reflect genuine market realities:

Structural and Condition Factors 🔧

- Documented subsidence or settlement issues (requiring subsidence surveys)

- Roof defects or aging systems (identified through roof surveys)

- Damp or moisture penetration (documented via damp surveys)

- Outdated electrical, plumbing, or heating systems

- Non-standard construction requiring specialist insurance

Location and Environmental Deductions

- Proximity to noise sources (airports, railways, major roads)

- Flood risk zones requiring elevated insurance premiums

- Limited parking or access constraints

- Declining neighborhood characteristics

- Planning restrictions limiting future development

Market Timing Considerations

Property valuations reflect market conditions at specific points in time. The 2026 valuation baseline may not account for:

- Recent market corrections or downturns

- Local oversupply in specific property segments

- Economic uncertainty affecting luxury property demand

- Changes in buyer preferences post-pandemic

A comprehensive building survey provides the detailed documentation necessary to support these adjustments, creating an evidence trail that tax authorities must acknowledge.

Documentation Standards for Challenge Preparation

Successful valuation challenges require meticulous documentation. Professional surveyors prepare comprehensive reports that include:

- Detailed property inspection findings with photographic evidence

- Comparable sales analysis with adjustment justifications

- Condition reports highlighting defects and required remediation costs

- Market analysis demonstrating local pricing trends

- Professional opinions on appropriate valuation ranges

This documentation serves dual purposes: it supports immediate valuation discussions with local authorities and provides appeal evidence if disputes escalate. The investment in professional survey pricing typically represents a fraction of potential multi-year surcharge savings.

Implementing Valuation Adjustments for 2026 Council Tax Surcharge Risks: Surveyor Strategies for Second Homeowners

Pre-Implementation Action Timeline

With the surcharge taking effect in April 2028, second homeowners have a strategic window to prepare. The optimal action timeline includes:

2026: Assessment and Documentation Phase

- Commission comprehensive property surveys from RICS-qualified surveyors

- Document all structural defects, maintenance issues, and condition concerns

- Gather comparable sales data for similar properties

- Review existing council tax banding for accuracy

- Identify potential grounds for valuation challenges

Early 2027: Consultation Engagement

- Participate in government consultations on implementation details[8]

- Submit evidence-based representations regarding property-specific circumstances

- Engage with local authority valuation officers proactively

- Consider pre-emptive valuation reviews before official assessments

Late 2027: Challenge Preparation

- Finalize comprehensive valuation reports

- Prepare formal challenge documentation

- Review appeal procedures and timelines

- Consider strategic property improvements that might affect valuations

Strategic Renovation and Improvement Timing

Property improvements create complex valuation dynamics. While renovations typically increase property values, strategic timing can influence surcharge liability:

Deferring Value-Adding Improvements

Second homeowners near the £2 million threshold might strategically defer:

- Luxury kitchen or bathroom renovations

- Extensions or additional square footage

- High-end finishes or premium fixtures

- Landscape improvements that enhance curb appeal

Prioritizing Value-Neutral Maintenance

Essential maintenance that preserves value without adding premium features:

- Addressing structural defects that reduce current valuations

- Updating aging systems to standard (not luxury) specifications

- Resolving damp, drainage, or weatherproofing issues

- Maintaining existing features rather than upgrading

Professional Insight: "The difference between maintaining a property at its current standard and improving it to premium specifications can easily represent £200,000-£300,000 in valuation terms—potentially the difference between surcharge liability and exemption." — RICS Chartered Surveyor

Working with Specialized Valuation Professionals

Not all surveyors possess equal expertise in tax-related valuations. Second homeowners should specifically seek professionals with:

Relevant Qualifications and Experience

- RICS chartered status with valuation specialization

- Experience with council tax banding challenges

- Knowledge of local property markets in relevant areas

- Track record of successful valuation appeals

Comprehensive Service Offerings

Professional firms offering integrated services provide strategic advantages:

- Initial homebuyer surveys for baseline documentation

- Specialized freehold valuations for ownership structures

- Expert witness reports for formal appeals

- Ongoing monitoring and reassessment services

For second homes in different regions, engaging local specialists familiar with area-specific market dynamics proves invaluable. Properties in Hertfordshire, Fulham, or Clapham each present unique valuation considerations that local chartered surveyors understand intimately.

Alternative Ownership Structures and Their Valuation Implications

Some second homeowners explore ownership restructuring to manage surcharge exposure. While tax advice should come from qualified accountants and solicitors, surveyors play critical roles in valuing properties under different ownership scenarios:

Corporate Ownership Considerations

Properties held through corporate structures may face different valuation approaches, though the surcharge specifically targets residential properties regardless of ownership structure. Professional valuations help assess:

- Whether corporate ownership affects market value perceptions

- How rental income potential influences valuations under different structures

- Documentation requirements for properties with complex ownership

Shared Ownership and Fractional Interests

For properties with multiple owners, valuation becomes more nuanced:

- How do fractional interests affect overall property valuation?

- What documentation proves individual ownership percentages?

- How do surveyors assess properties with complex ownership arrangements?

Trust and Estate Planning Implications

Properties held in trust require specialized valuation approaches that consider:

- Beneficial ownership versus legal title

- Restrictions on use or disposal affecting market value

- Estate planning objectives influencing valuation timing

These complex scenarios demand coordination between surveyors, tax advisors, and legal professionals to ensure valuations align with overall strategic objectives.

Risk Mitigation and Long-Term Planning Strategies

Portfolio Diversification for Multiple Property Owners

Second homeowners with multiple properties face compounded surcharge risks. Strategic portfolio management includes:

Geographic Diversification

Spreading property holdings across different markets reduces concentration risk:

- Properties in lower-value markets provide surcharge-exempt holdings

- Regional diversification protects against localized market fluctuations

- Different property types (coastal, rural, urban) respond differently to market conditions

Value Distribution Strategies

Rather than concentrating wealth in single high-value properties, some owners consider:

- Holding multiple properties below the £2 million threshold

- Balancing one high-value property with several lower-value investments

- Strategic sales and reinvestment to optimize portfolio structure

Ongoing Monitoring and Reassessment

Property valuations aren't static. Market conditions, property conditions, and regulatory frameworks evolve continuously. Effective long-term strategies include:

Annual Valuation Reviews

Regular professional assessments identify:

- Market value trends affecting surcharge liability

- Emerging maintenance issues reducing property values

- Opportunities for strategic improvements or deferrals

- Changes in comparable sales data

Market Intelligence Monitoring

Staying informed about:

- Local property market trends and pricing dynamics

- Regulatory changes affecting property taxation

- Economic factors influencing luxury property demand

- Planning and development affecting neighborhood values

Relationship Building with Valuation Officers

Proactive, professional engagement with local authority valuation officers creates:

- Understanding of specific documentation requirements

- Opportunities for informal discussions before formal challenges

- Credibility when presenting evidence-based valuation arguments

- Smoother resolution processes if disputes arise

Insurance and Financial Planning Considerations

The surcharge creates additional financial planning requirements:

Budgeting for Surcharge Liability

Even with successful valuation strategies, some properties will incur surcharges. Prudent planning includes:

- Incorporating potential surcharge costs into property ownership budgets

- Establishing reserves for tax liabilities

- Reviewing rental income strategies to offset surcharge costs

- Considering whether surcharge liability affects overall property investment returns

Insurance Valuation Alignment

Interestingly, insurance valuations serve different purposes than market valuations. Properties require insurance reinstatement valuations that reflect rebuilding costs rather than market values. This creates potential misalignments:

- A property might have a £2.5 million market value but £3 million reinstatement cost

- Insurance valuations don't determine surcharge liability

- However, significant disparities might trigger questions from authorities

Coordinating different valuation purposes with professional surveyors ensures consistency and defensibility across all property-related financial planning.

Conclusion

Valuation Adjustments for 2026 Council Tax Surcharge Risks: Surveyor Strategies for Second Homeowners represent essential defensive tools in the evolving UK property tax landscape. With surcharges of £2,500-£7,500 annually affecting properties valued at £2 million or more from April 2028, the financial stakes demand professional surveyor engagement[6].

Strategic approaches include:

✅ Early engagement with RICS-qualified chartered surveyors to establish baseline valuations

✅ Comprehensive documentation of structural defects, market conditions, and location factors that legitimately reduce property values

✅ Strategic timing of improvements and maintenance to manage valuation trajectories

✅ Professional challenge preparation with evidence-based valuation reports that withstand authority scrutiny

✅ Ongoing monitoring and reassessment to adapt to changing market conditions and regulatory frameworks

The £500 million annual revenue target means local authorities will scrutinize high-value properties intensively[6]. Second homeowners who proactively engage professional surveyors gain significant advantages: defensible valuations, documented evidence for challenges, and strategic insights that minimize unnecessary tax exposure.

Next Steps for Second Homeowners

- Commission a comprehensive property survey from qualified professionals to establish current condition and market value

- Review comparable sales data in your property's area to understand valuation benchmarks

- Document all defects and condition issues that might justify valuation adjustments

- Engage with the 2026 consultation process to represent your interests in implementation details

- Develop a long-term strategy coordinating surveyor expertise with tax and legal advice

The window for effective preparation is now. Properties near the £2 million threshold require immediate attention, while all high-value second homes benefit from professional valuation strategies that protect against excessive surcharge liability. By implementing the surveyor strategies outlined in this guide, second homeowners can navigate the 2026 council tax surcharge framework with confidence and minimize financial exposure through legitimate, evidence-based valuation adjustments.

References

[1] Council Tax – https://obr.uk/forecasts-in-depth/tax-by-tax-spend-by-spend/council-tax/

[2] How To Deal With 2026 Council Tax Bill Increases And Arrears – https://www.charles-stanley.co.uk/insights/commentary/how-to-deal-with-2026-council-tax-bill-increases-and-arrears

[6] New Property Tax – https://hoa.org.uk/news/new-property-tax/

[8] How Will The High Value Council Tax Surcharge Work – https://www.ross-brooke.co.uk/how-will-the-high-value-council-tax-surcharge-work/