Fewer than 14% of leasehold flat buyers in England and Wales fully understand how a short lease affects the price they should pay — yet the financial consequences can run into tens of thousands of pounds. This guide on Valuing Properties with Short Leases and Service-Charge Uncertainty: A Practical Guide for Surveyors and Flat Owners breaks down the technical adjustments surveyors must make, explains how to communicate those adjustments clearly to buyers and lenders, and gives flat owners the knowledge they need to protect their investment.

Key Takeaways

- Leases below 80 years trigger "marriage value," sharply increasing the cost of lease extension and reducing the property's open-market value.

- Surveyors use relativity graphs and investment-yield methods to quantify the discount a short lease imposes on a flat's freehold equivalent value.

- Opaque or escalating service charges must be reviewed at the source — not estimated — before a reliable valuation figure can be produced.

- Most mainstream mortgage lenders require a minimum unexpired term of 70–85 years, making short-lease flats difficult to finance and therefore harder to sell.

- A RICS-registered valuer is essential for any flat where the lease is under 80 years or where service-charge accounts are incomplete or disputed.

Why Lease Length Is a Valuation Variable, Not a Side Note

The starting point for Valuing Properties with Short Leases and Service-Charge Uncertainty: A Practical Guide for Surveyors and Flat Owners is understanding that lease length is not a binary pass-or-fail criterion. It is a continuous variable that depresses value in a non-linear way as the term shortens.

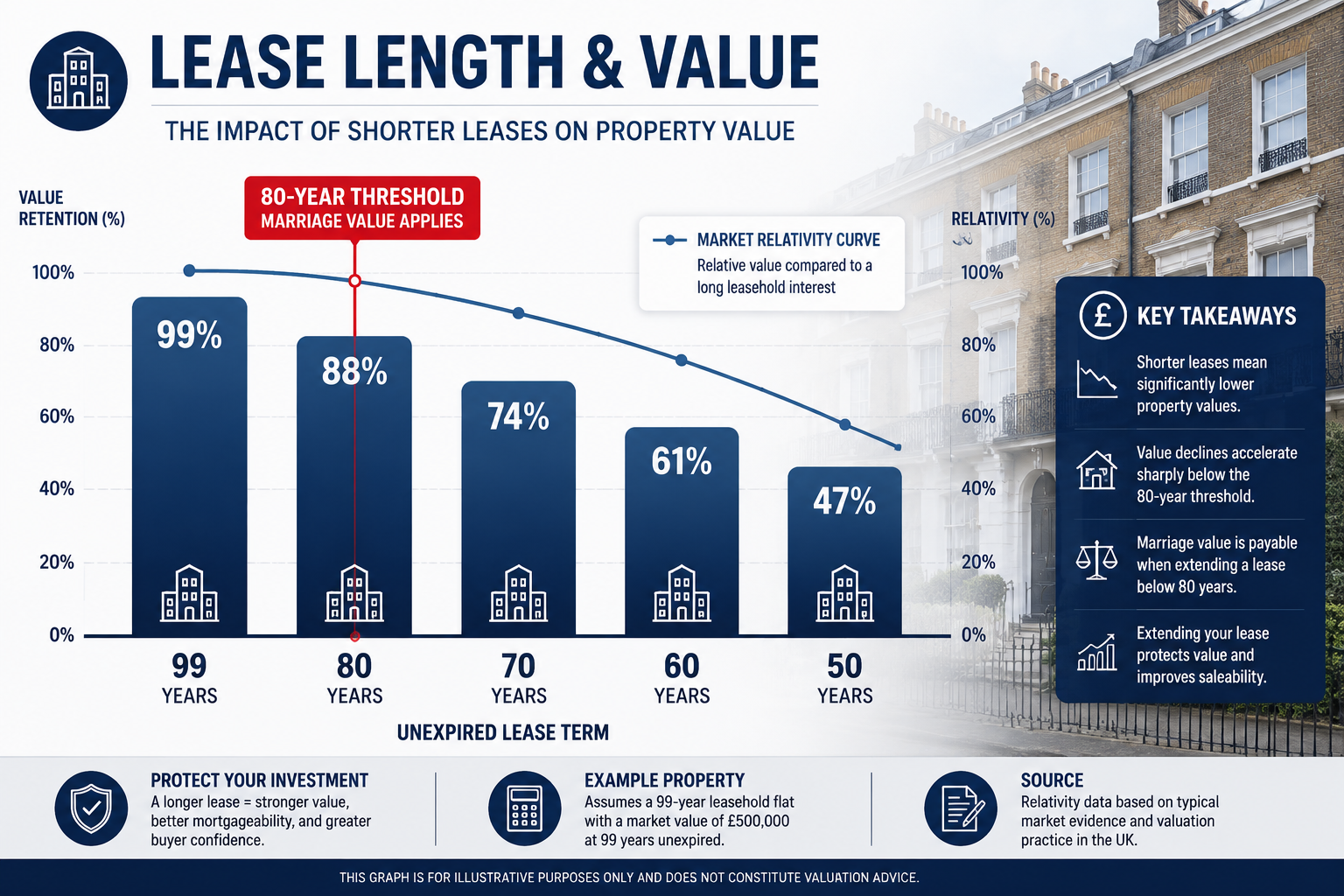

Research shows that a flat with a 70-year lease may retain only around 83% of the value it would command with a 99-year lease [1]. That discount widens dramatically once the term falls below 60 years, and it accelerates again below 50 years. The relationship is not arithmetic — it follows a curve, and surveyors must plot where on that curve a specific property sits.

The 80-Year Threshold and Marriage Value

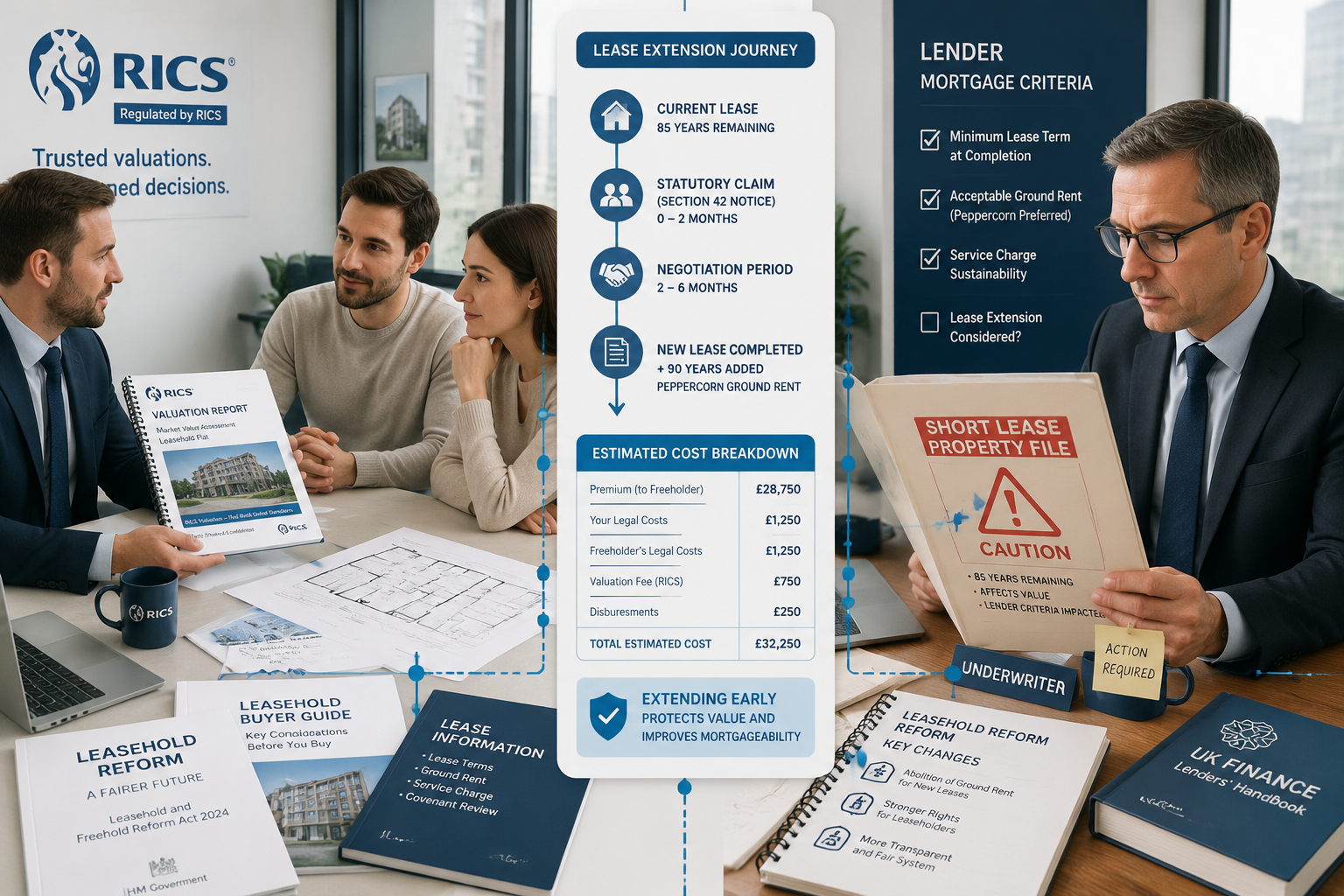

The 80-year mark is the most important boundary in leasehold valuation. When the unexpired term drops below 80 years, marriage value enters the calculation [2]. Marriage value represents the uplift in the combined value of the freehold and leasehold interests that results from merging them through a lease extension. Under the Leasehold Reform, Housing and Urban Development Act 1993, the leaseholder must share 50% of that marriage value with the freeholder when extending.

In practical terms, this means the premium payable for a lease extension can jump by tens of thousands of pounds the moment the lease crosses below the 80-year threshold [2]. A surveyor valuing a flat at, say, 78 years unexpired must factor in not only the current diminution in value but also the elevated cost of the future extension that any informed buyer will seek to negotiate.

"The 80-year threshold is not a cliff edge in the physical sense, but it is a financial cliff edge. A flat at 81 years and a flat at 79 years can differ in extension premium by £20,000 or more, yet look identical to an untrained eye."

Relativity Graphs: The Surveyor's Calibration Tool

Surveyors use relativity graphs to express the percentage of freehold value that a leasehold interest retains at any given unexpired term [8]. Several published graphs exist — produced by bodies including Gerald Eve and the Leasehold Advisory Service — and they do not always agree, which is itself a source of dispute in tribunal proceedings.

The key principle is consistent: as the lease shortens, relativity falls. A flat with 60 years unexpired might have a relativity of around 85–88% depending on the graph used, while a flat at 40 years might fall to 70–75%. The surveyor must select the most appropriate graph for the market in question, document that choice in the report, and explain the resulting adjustment in plain language.

For buyers and lenders unfamiliar with the concept, a simple table in the valuation report can make the adjustment transparent:

| Unexpired Term | Approximate Relativity | Indicative Value Retention |

|---|---|---|

| 99+ years | 100% | Full freehold equivalent |

| 80 years | ~95% | Minor discount |

| 70 years | ~88–90% | Moderate discount |

| 60 years | ~83–86% | Significant discount |

| 50 years | ~75–80% | Substantial discount |

| Below 30 years | Below 65% | Severe discount; specialist methods required |

Note: Figures are indicative. Actual relativity depends on the graph used and local market conditions.

For leases under 30 years, traditional comparable-evidence methods become unreliable. Surveyors increasingly turn to an investment calculation approach, which values the flat based on its potential rental income and net annual yield rather than direct comparable sales [7]. This method must be explained carefully in reports, as lenders and buyers may be unfamiliar with it.

Working with a RICS-registered valuer is strongly recommended in these cases, as the methodology requires professional judgement that goes beyond standard residential valuation.

Decoding Service-Charge Uncertainty in Flat Valuations

Service charges represent the second major layer of complexity in Valuing Properties with Short Leases and Service-Charge Uncertainty: A Practical Guide for Surveyors and Flat Owners. Unlike lease length, which is a fixed number visible on the title register, service charges are dynamic, often opaque, and sometimes contested.

What Makes Service Charges a Valuation Risk

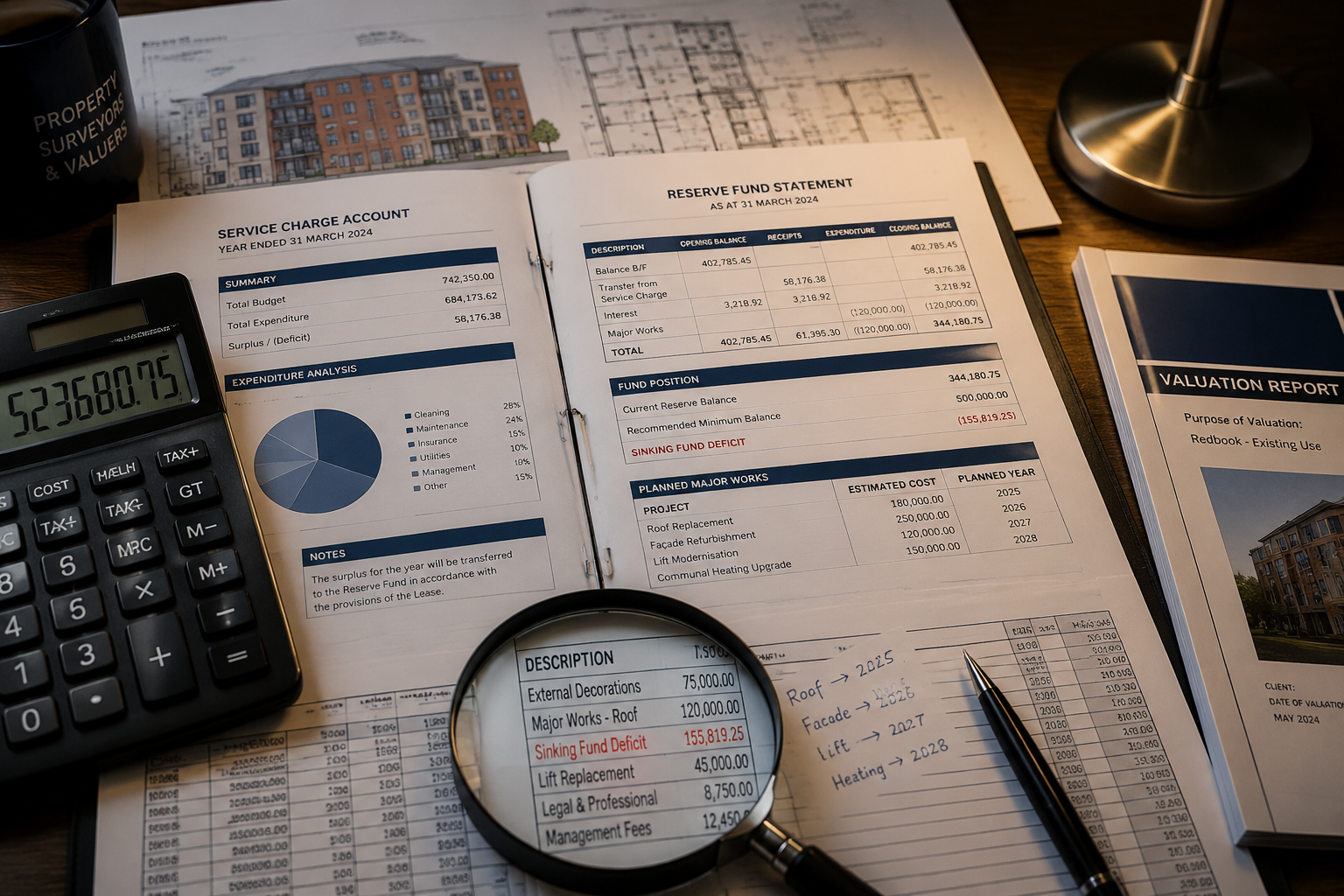

A service charge is the leaseholder's contribution to the running costs of the building — maintenance, insurance, management fees, and major works. The problem is that these costs can be unpredictable. Buildings with deferred maintenance, ageing roofs, or failing cladding systems can generate sudden demands for large sums that no buyer has budgeted for.

The key risk factors surveyors should investigate include:

- Reserve fund (sinking fund) balance: A low or zero balance means future major works will be funded by special levies rather than accumulated reserves. This is a direct financial liability for the incoming buyer.

- Planned or ongoing major works: Section 20 consultation notices, scaffold on the building, or correspondence about cladding remediation all signal imminent expenditure.

- Ground rent escalation clauses: Leases with ground rent that doubles every ten or fifteen years can render a property unmortgageable and unsellable [4]. Surveyors must identify and report these terms explicitly.

- Management quality: Poor management companies often produce incomplete accounts, making it impossible to assess the building's financial health without further enquiries.

Surveyors should always request at least three years of service charge accounts, the most recent reserve fund statement, and any Section 20 notices before forming a view on value [3]. If these documents are unavailable, the valuation report must state that fact prominently and reflect the uncertainty in the figure produced.

Quantifying the Service-Charge Discount

There is no universal formula for the service-charge discount, but a structured approach is possible:

- Establish the "clean" comparable value — what the flat would be worth with a long lease and normal service charges.

- Identify the specific service-charge risk — quantify the likely shortfall in the reserve fund or the estimated cost of known major works.

- Apply a market-derived adjustment — based on evidence of how similar risks have affected prices in comparable transactions.

- Document the reasoning — the report must show the logic, not just the number.

For buyers, this process is most useful when supported by a RICS building survey that assesses the physical condition of the building independently of the service-charge accounts. A building in poor condition with a low reserve fund represents a compounded risk that should produce a compounded discount.

Ground Rent: The Hidden Multiplier

Ground rent terms deserve special attention. Leases with escalating ground rent clauses — particularly those that double every ten years — have attracted intense scrutiny from lenders and regulators [4]. A flat with a ground rent starting at £250 per year but doubling every decade will reach £8,000 per year within 50 years. Many lenders will not lend against such terms at any lease length.

Surveyors must identify the ground rent review mechanism from the lease itself, not from the seller's solicitor's summary. The valuation report should state the current ground rent, the review frequency, the review mechanism (fixed increase, RPI-linked, or doubling), and an opinion on whether the terms are likely to affect mortgageability.

Exploring collective enfranchisement — where leaseholders collectively purchase the freehold — may be relevant where onerous ground rent terms affect multiple flats in the same building. This option can resolve both the ground rent problem and the short-lease problem simultaneously, though it requires the cooperation of qualifying leaseholders.

Writing Valuation Reports That Buyers and Lenders Can Actually Use

The technical skill of adjusting for lease length and service-charge risk is only half the job. The other half is communicating those adjustments in a way that a buyer, a mortgage underwriter, or a solicitor can understand and act upon. This is where many valuation reports fall short.

Structuring the Short-Lease Adjustment

A well-structured report on a short-lease flat should contain the following elements:

- Unexpired term stated clearly — not buried in the property description but highlighted as a material fact.

- Relativity graph identified — state which graph was used and why.

- Marriage value calculation — if applicable, show the estimated premium for extension and how it affects the open-market value.

- Comparable evidence — cite transactions involving similar lease lengths, not just similar properties with long leases.

- Adjusted figure with explanation — the final value should be accompanied by a sentence explaining the quantum of the short-lease discount.

For lenders in particular, the report should also address minimum lease term requirements. Most mainstream lenders require an unexpired term of at least 70–85 years at the point of application, and many require the lease to have at least 70 years remaining at the end of the mortgage term [6]. If the subject property does not meet these criteria, the report should say so directly.

Communicating Service-Charge Risk

Service-charge uncertainty should be presented as a range of potential outcomes rather than a single figure. Where the reserve fund is deficient, the report should estimate the likely shortfall and state what that means in per-flat terms. Where major works are imminent, the estimated cost and the leaseholder's likely share should be stated.

A short summary table is often more useful than a paragraph of prose:

| Risk Factor | Status | Estimated Financial Impact |

|---|---|---|

| Reserve fund balance | Low (£12,000 against £80,000 benchmark) | Potential special levy of £5,000–£8,000 per flat |

| Roof condition | Deteriorating; replacement likely within 5 years | £3,000–£5,000 per flat |

| Ground rent | Doubling clause; currently £300/year | Mortgageability risk; affects buyer pool |

| Cladding | EWS1 form not available | Significant uncertainty; lender restriction likely |

This format allows a lender's underwriter to assess the risk quickly and gives a buyer a clear picture of the financial commitments they are taking on.

When to Recommend Further Action

Valuation reports on short-lease or high-service-charge properties should routinely recommend:

- Instructing a solicitor to review the full lease before exchange, not just the title summary.

- Obtaining a RICS HomeBuyer Survey or Level 3 Building Survey if the physical condition of the building has not been independently assessed.

- Requesting a formal service charge budget and reserve fund statement from the managing agent.

- Seeking specialist leasehold advice on the cost of extension before committing to a purchase price.

For buyers in specific locations — whether purchasing a flat in central London, Surrey, or South East London — local market knowledge matters. Relativity and service-charge norms vary by area, and a surveyor with regional experience will produce a more accurate and defensible report.

It is also worth noting that, as of 2026, no transformative leasehold reform legislation has been enacted that changes the fundamental valuation methodology for short leases [6]. Surveyors should therefore continue to apply established RICS guidance and tribunal-tested approaches while monitoring legislative developments.

For those considering a Red Book valuation — the formal RICS standard required for mortgage, legal, and tax purposes — it is essential that the valuer has demonstrable experience with leasehold properties and can justify every adjustment made.

Conclusion

Valuing Properties with Short Leases and Service-Charge Uncertainty: A Practical Guide for Surveyors and Flat Owners is ultimately about translating complexity into clarity. A short lease is not just a number on a document — it is a financial liability that compounds over time, affects mortgageability, and shapes the buyer pool. Service-charge uncertainty is not just an administrative inconvenience — it can represent tens of thousands of pounds in future obligations that a buyer unknowingly inherits.

Actionable next steps for surveyors:

- Always identify the unexpired term and marriage value threshold before selecting comparable evidence.

- State the relativity graph used and justify the choice in the report.

- Request three years of service charge accounts and a current reserve fund statement as standard.

- Present service-charge risks in a table format that lenders and buyers can act on.

Actionable next steps for flat owners and buyers:

- If the lease is under 85 years, obtain a specialist leasehold valuation before agreeing a price.

- Ask the seller's solicitor for all service charge accounts, reserve fund balances, and Section 20 notices before exchange.

- Investigate lease extension or collective enfranchisement options early — the cost rises as the lease shortens.

- Work only with a RICS-registered valuer who has specific leasehold experience.

The complexity of short-lease and service-charge valuation is real, but it is manageable with the right professional guidance and a disciplined, transparent approach to reporting.

References

[1] Lease Length And Property Value Chart – https://sell-short-lease-flat.co.uk/guides/lease-length-and-property-value-chart/?utm_source=openai

[2] What Is A Short Lease – https://sell-short-lease-flat.co.uk/guides/what-is-a-short-lease/?utm_source=openai

[3] Building Surveying For Pre Purchase Flats Leasehold Risks Service Charge Clues And Hidden Defects Buyers Miss – https://www.canterburysurveyors.com/blog/building-surveying-for-pre-purchase-flats-leasehold-risks-service-charge-clues-and-hidden-defects-buyers-miss/?utm_source=openai

[4] Short Lease London Flats Sell Fast Or Extend – https://www.quickhousebuyer.co.uk/short-lease-london-flats-sell-fast-or-extend/?utm_source=openai

[5] Professional Valuation – https://www.lease-advice.org/lease-extension/flats/valuation/professional-valuation/?utm_source=openai

[6] Short Leases Long Chains – https://extension.lease/short-leases-long-chains/?utm_source=openai

[7] Lease Valuation Methods And Examples – https://www.perryhill.co.uk/news/lease-valuation-methods-and-examples/?utm_source=openai

[8] Selling Property With Short Lease – https://getpine.co.uk/guides/selling-property-with-short-lease?utm_source=openai