The UK property market has entered a crucial stabilisation phase in early 2026, presenting unique challenges for property valuers and surveyors. With the latest RICS data revealing a Q1 2026 house price net balance of -10%, professionals must navigate a landscape where sentiment is improving yet prices remain under pressure. This delicate market equilibrium demands precision, updated methodologies, and a thorough understanding of regional variations that can significantly impact property valuations.

For chartered surveyors and property professionals, accurately valuing properties under stabilising national prices requires more than traditional approaches. The current market conditions—characterised by constrained supply, evolving regulatory frameworks, and divergent regional performance—necessitate a sophisticated application of RICS-compliant valuation techniques that reflect real-time market dynamics whilst maintaining professional standards.

Key Takeaways

- Market stabilisation at -10% net balance requires valuers to apply rigorous comparable analysis with precise adjustments reflecting current transaction evidence rather than historical trends

- Regional variations significantly impact valuations in Q1 2026, with some areas experiencing growth whilst others face continued price pressure, demanding localised market knowledge

- Updated RICS standards including ESG valuation criteria (effective April 2026) and Basel 3.1 lending guidance must be integrated into all professional valuations [4][3]

- Rental market constraints with enquiries declining to 4.8 per property necessitate careful consideration of investment valuations and yield assessments [2]

- Professional compliance with RICS Red Book standards remains essential for defensible valuations in stabilising market conditions

Understanding the Q1 2026 Market Context for Property Valuations

The Q1 2026 house price net balance of -10% represents a significant moderation from previous quarters, signalling neither dramatic decline nor robust growth. This stabilisation phase creates specific challenges for property valuers who must accurately reflect current market sentiment whilst avoiding over-reliance on outdated comparable evidence.

What Does a -10% Net Balance Actually Mean? 📊

A net balance of -10% indicates that 10% more RICS members reported falling rather than rising house prices during Q1 2026. This metric doesn't represent a 10% price decrease but rather the balance of professional opinion regarding price direction. Understanding this distinction is crucial for accurate valuation work.

Key market characteristics in Q1 2026 include:

- Moderate price pressure rather than sharp corrections

- Improved sentiment compared to 2024-2025 volatility

- Transaction volume stabilisation with buyers and sellers adjusting expectations

- Regional divergence becoming more pronounced across UK markets

- Rental market tightness affecting investment property valuations [2]

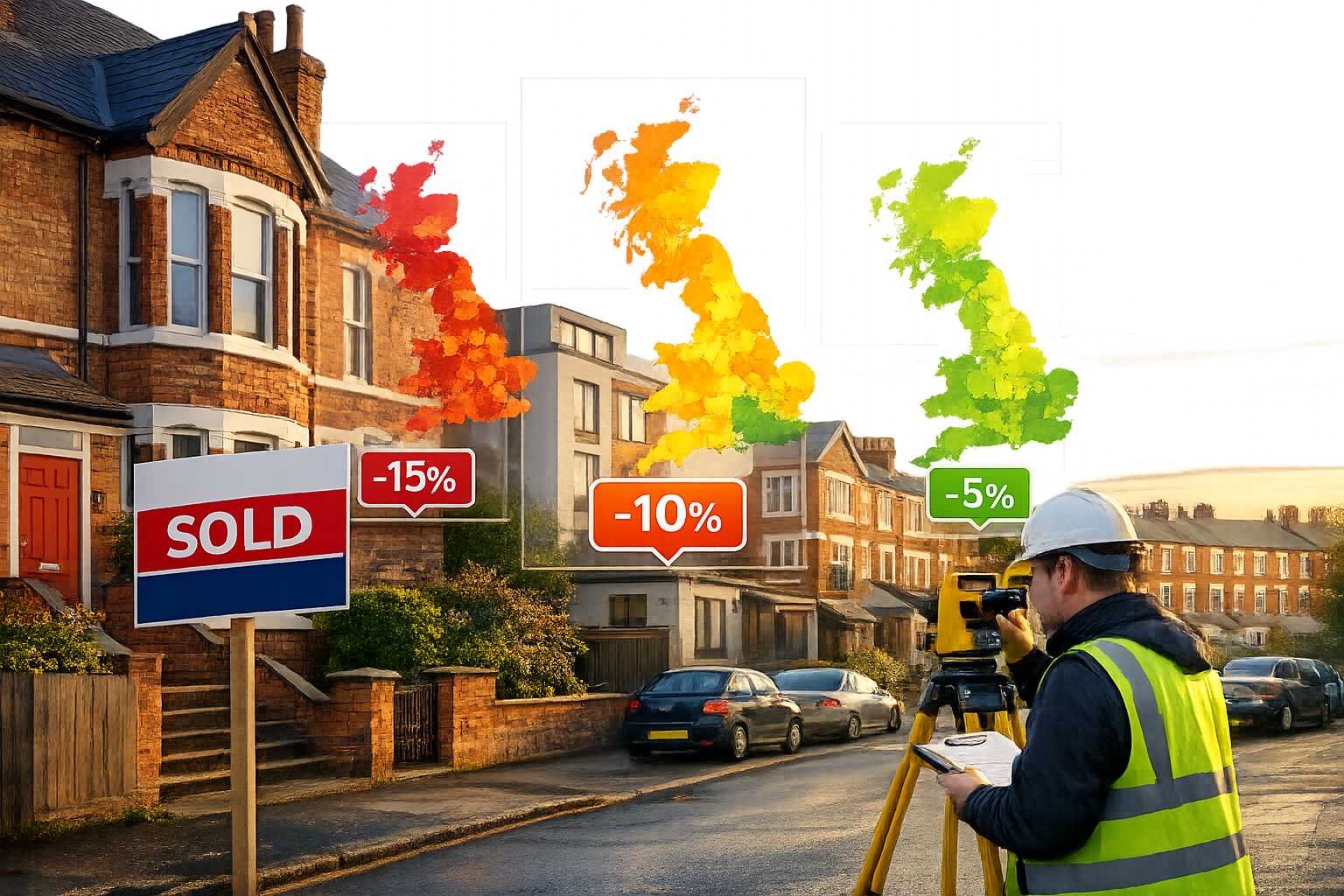

Regional Variations Requiring Localised Valuation Approaches

National statistics mask significant regional performance differences that professional valuers must account for. Some areas continue experiencing price growth whilst others face ongoing adjustments. When conducting RICS building surveys or valuations, understanding local market dynamics becomes paramount.

| Region Type | Typical Q1 2026 Performance | Valuation Considerations |

|---|---|---|

| Prime London | Modest growth (+2% to +5%) | International demand factors, currency impacts |

| Regional Cities | Stabilisation (-5% to 0%) | Employment trends, infrastructure investment |

| Commuter Zones | Mixed performance (-10% to +3%) | Hybrid working patterns, transport links |

| Rural Markets | Sustained demand (0% to +4%) | Lifestyle migration, limited supply |

| Coastal Areas | Variable (-8% to +2%) | Second home demand, local economic factors |

Professional valuers must gather localised comparable evidence rather than relying solely on national indices when assessing properties under these stabilising conditions.

RICS-Compliant Valuation Methods for Stabilising Markets

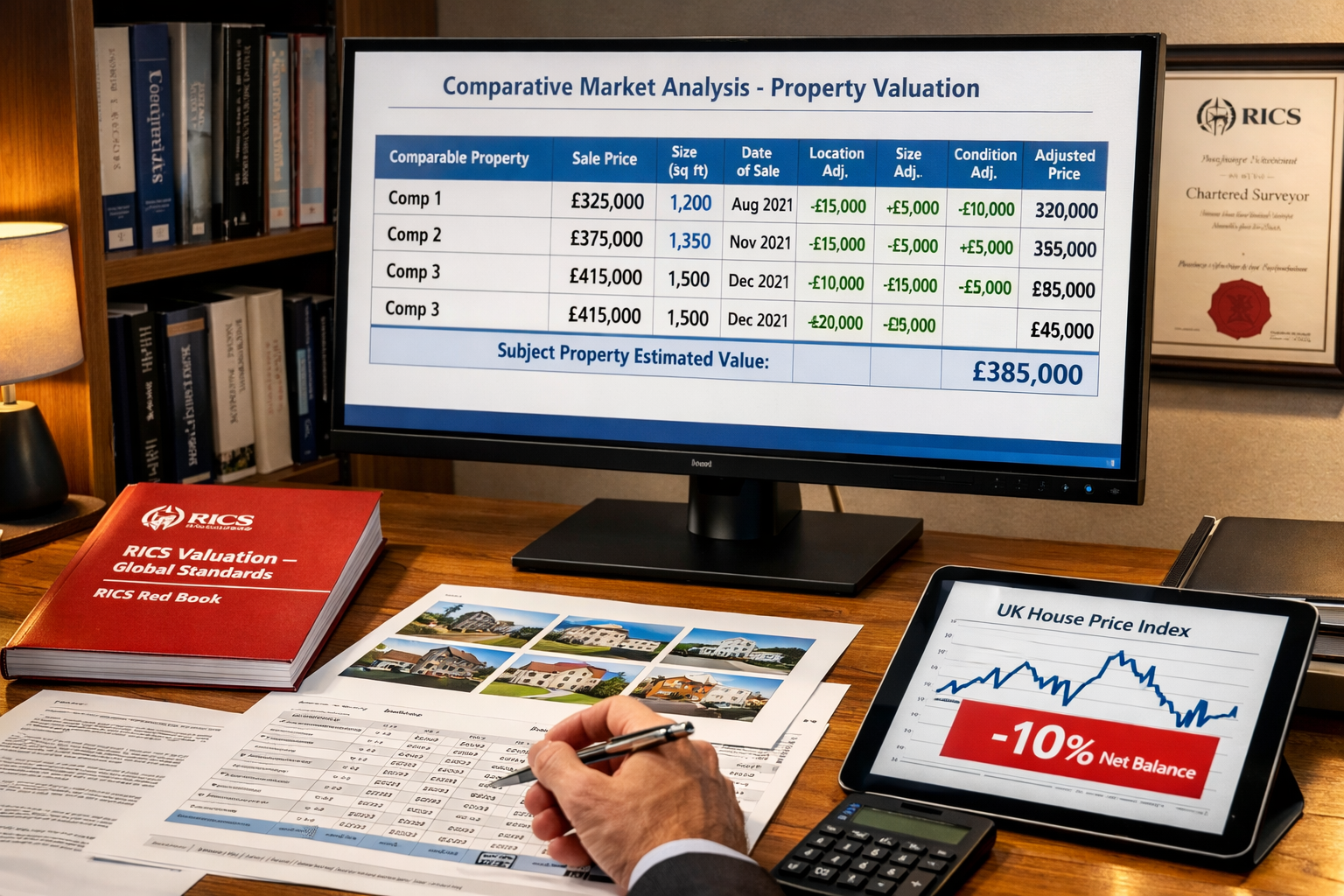

The Royal Institution of Chartered Surveyors provides comprehensive guidance on valuation methodologies, with the comparable method remaining the primary approach for most residential and commercial property assessments [1]. However, applying these methods during market stabilisation requires enhanced rigour and careful adjustment.

The Comparable Method: Enhanced Application in Q1 2026

The comparable method involves analysing recent transactions of similar properties to establish market value. In stabilising markets with a -10% net balance, this approach demands particular attention to:

Transaction recency 🕐 – Comparable evidence from more than 3-6 months ago may not reflect current market conditions. Valuers should prioritise recent transactions and apply appropriate time adjustments where older comparables must be used.

Adjustment precision – Each comparable requires careful adjustment for differences in:

- Location and specific positioning

- Property size, layout, and configuration

- Condition and specification standards

- Market conditions at transaction date

- Buyer motivation and transaction circumstances

Market evidence triangulation – Cross-referencing multiple data sources including Land Registry records, local agent intelligence, and professional networks provides more robust valuation foundations than single-source evidence.

When conducting RICS valuations, professionals should document their comparable selection rationale and adjustment methodology comprehensively to ensure defensibility.

Investment Method for Rental Properties Under Supply Constraints

With rental enquiries declining to 4.8 per property in Q1 2026 [2], the investment method requires careful calibration. This approach capitalises rental income streams using appropriate yields to establish capital value.

Key considerations for Q1 2026 investment valuations:

- Yield selection must reflect current market expectations rather than historical norms

- Rental value assessments should account for constrained supply potentially supporting rental growth

- Void periods and management costs require realistic assumptions in stabilising markets

- Tenant demand patterns vary significantly by property type and location

- Regulatory changes including energy efficiency requirements impact both rental values and yields

The formula remains straightforward but requires nuanced inputs:

Market Value = Net Annual Rental Income ÷ Market Yield

However, determining accurate rental income and appropriate yields in Q1 2026 conditions demands thorough market research and professional judgement [1].

Residual Method for Development Properties

For development sites and properties requiring substantial refurbishment, the residual method calculates value by deducting development costs and profit from the completed development value. In stabilising markets, this approach requires:

- Conservative end-value assumptions reflecting current market sentiment

- Realistic cost estimates accounting for construction inflation and supply chain factors

- Appropriate developer profit margins for prevailing risk levels

- Accurate timeframe assessments affecting finance costs and market exposure

Professional valuers should consider obtaining specific defect surveys to inform accurate cost assessments for properties requiring significant works.

Applying Updated RICS Standards: ESG and Basel 3.1 Considerations

The regulatory landscape for property valuation has evolved significantly, with two major updates impacting Q1 2026 valuations: the fourth edition of RICS ESG valuation standards (effective 30 April 2026) and updated Basel 3.1 lending valuation guidance.

ESG Integration in Property Valuations

RICS published updated global standards on ESG and sustainability in commercial property valuation, effective from 30 April 2026 [4]. These standards require valuers to systematically consider environmental, social, and governance factors that materially impact property value.

Environmental factors affecting Q1 2026 valuations:

- ⚡ Energy Performance Certificate (EPC) ratings – Properties with poor energy efficiency face potential value discounts and restricted marketability

- 🌡️ Climate risk exposure – Flood risk, overheating potential, and climate adaptation measures influence value

- ♻️ Sustainability features – Renewable energy systems, water efficiency, and sustainable materials can enhance value

- 🏗️ Future-proofing costs – Anticipated regulatory changes requiring retrofitting impact residual value

Social and governance considerations:

- Building safety compliance and cladding issues

- Accessibility standards and inclusive design

- Community impact and local planning considerations

- Corporate governance of property ownership structures

When conducting RICS homebuyer surveys or more detailed Level 3 building surveys, identifying ESG factors that materially affect value has become essential professional practice.

Basel 3.1 Framework and Mortgage Lending Valuations

RICS released updated guidance on bank lending valuations reflecting Basel 3.1 framework changes [3]. This guidance clarifies the relationship between market value, mortgage lending value (MLV), and prudently conservative valuation criteria for secured lending.

Key principles for lending valuations in Q1 2026:

- Market Value remains the foundation – MLV is derived from but distinct from market value

- Sustainability assessment – Long-term value sustainability over economic cycles must be considered

- Conservative adjustments – Prudent assumptions regarding market conditions and property characteristics

- Risk factor identification – Clear documentation of factors that might affect long-term value

For properties requiring Help to Buy valuations or Right to Buy assessments, understanding these lending valuation principles ensures compliance with lender requirements whilst maintaining professional standards.

Practical Valuation Techniques for Q1 2026 Conditions

Beyond theoretical frameworks, practical application of valuation techniques in stabilising markets requires systematic approaches and professional judgement honed through experience and market knowledge.

Comparable Evidence: Sourcing and Adjustment Methodology

Sourcing reliable comparable evidence in Q1 2026:

- HM Land Registry data – Provides transaction prices but with time lag; requires adjustment for market movement

- Local estate agent intelligence – Offers real-time market insights including asking prices, offers, and transaction progress

- Professional networks – Fellow RICS members can provide valuable market intelligence and comparable evidence

- Auction results – Particularly relevant for investment properties and those requiring refurbishment

- New build developments – Useful comparables for modern properties but require adjustment for incentives and market positioning

Systematic adjustment framework:

When adjusting comparable evidence, apply a structured hierarchy:

- Location adjustments (typically ±5-15%) – Account for micro-location differences even within same postcode

- Size adjustments – Apply per square foot/metre analysis with recognition of diminishing returns at larger sizes

- Condition adjustments (±10-25%) – Reflect differences in specification, maintenance, and modernisation

- Time adjustments – Apply monthly market movement rates based on local evidence

- Transaction circumstance adjustments – Account for forced sales, related party transactions, or unusual terms

Documentation of adjustment rationale is essential for professional defensibility, particularly when chartered surveyors conduct valuations.

Dealing with Limited Transaction Evidence

Some market segments in Q1 2026 experience reduced transaction volumes, creating challenges for comparable-based valuations. Professional techniques for evidence-constrained situations include:

Expanding geographic search parameters – Carefully extending search areas whilst applying appropriate location adjustments

Temporal extension with robust adjustment – Using older comparables with well-evidenced time adjustments based on local indices

Alternative property type analysis – Analysing related property types (e.g., flats when valuing maisonettes) with appropriate adjustments

Income-based cross-checking – Using investment method calculations to sense-check comparable method conclusions

Professional judgement documentation – Clearly explaining valuation reasoning and evidence limitations in reports

Quality Assurance and Validation Checks

Professional valuers should implement systematic validation procedures:

✅ Sanity check against indices – Compare conclusion against regional house price indices to identify outliers

✅ Price per square foot analysis – Benchmark against typical rates for property type and location

✅ Peer review processes – Internal quality control by senior valuers for complex or high-value instructions

✅ Client expectation management – Discuss preliminary findings before finalising reports where appropriate

✅ Assumptions and limitations documentation – Clearly state any constraints affecting valuation accuracy

Sector-Specific Valuation Considerations for Q1 2026

Different property sectors respond differently to stabilising market conditions, requiring tailored valuation approaches.

Residential Properties: Owner-Occupied vs Investment

Owner-occupied residential valuations focus primarily on comparable evidence, with particular attention to:

- School catchment areas and local amenities

- Property presentation and emotional appeal factors

- Parking and outdoor space (increasingly valued post-pandemic)

- Home working suitability and space configuration

- Energy efficiency and running costs

Residential investment properties require dual consideration:

- Capital value using comparable method

- Investment value using income capitalisation

- Reconciliation of the two approaches

- Tenant security and lease terms

- Management intensity and costs

For properties requiring matrimonial valuations or shared ownership assessments, understanding both owner-occupied and investment perspectives may be necessary.

Commercial Property Valuation in Stabilising Markets

Commercial property valuations face additional complexity in Q1 2026, with the investment method predominating but requiring careful yield and rental value assessment.

Office properties – Hybrid working impacts demand patterns; location quality and specification standards increasingly differentiate values

Retail properties – E-commerce effects continue; prime pitch locations maintain value whilst secondary locations face pressure

Industrial and logistics – Strong fundamentals continue but yield compression may have reached limits

Leisure and hospitality – Recovery patterns vary by subsector; operational performance evidence crucial

Professional valuers conducting commercial building surveys must integrate physical condition assessment with market positioning analysis.

Specialist Valuations: Insurance, Tax, and Statutory Purposes

Certain valuation purposes require specific approaches:

Insurance reinstatement valuations – Focus on rebuilding costs rather than market value; require detailed reinstatement cost assessments independent of market conditions [5]

Capital gains tax valuations – Require retrospective market value assessments; need robust comparable evidence from relevant historical period

Probate valuations – Market value at date of death; must reflect actual market conditions at valuation date regardless of subsequent movements

Compulsory purchase valuations – Statutory compensation basis; requires specialist knowledge of Land Compensation Acts

Each specialist valuation type demands understanding of relevant statutory frameworks and professional standards beyond general market valuation principles.

Technology and Data Analytics in Modern Valuation Practice

Q1 2026 valuation practice increasingly incorporates technological tools whilst maintaining professional judgement as the cornerstone of reliable valuations.

Automated Valuation Models (AVMs): Role and Limitations

AVMs use statistical modelling and property databases to generate valuations algorithmically. Their role in Q1 2026 includes:

Appropriate AVM applications:

- Initial desktop valuations for low-risk lending

- Portfolio valuations for large property holdings

- Market trend analysis and benchmarking

- Quality assurance checks on manual valuations

Critical AVM limitations in stabilising markets:

- Struggle to reflect rapid market changes and sentiment shifts

- Cannot assess property-specific condition and quality factors

- Limited effectiveness for unusual properties or thin markets

- Lack professional judgement on market nuances

Professional RICS valuers should use AVMs as supporting tools rather than replacements for detailed inspection-based valuations, particularly for higher-value or complex properties.

Data Sources and Market Intelligence Platforms

Modern valuation practice leverages multiple data sources:

- Land Registry Price Paid Data – Comprehensive transaction records with time lag

- EPC databases – Energy efficiency information affecting value

- Planning portals – Development potential and constraints

- Flood risk databases – Environmental risk assessment

- Demographic and economic data – Market demand drivers

- Commercial property databases – Rental and yield evidence

Integrating diverse data sources with site-specific inspection findings produces robust valuations reflecting Q1 2026 market realities.

Professional Standards and Risk Management

Maintaining professional standards whilst managing risk remains paramount for RICS members conducting valuations in stabilising markets.

RICS Red Book Compliance Essentials

The RICS Valuation – Global Standards (Red Book) establishes mandatory requirements for all RICS members undertaking valuation services. Key compliance requirements include:

📋 Terms of engagement – Written confirmation of instruction scope, basis of value, assumptions, and limitations

🎯 Basis of value – Clear identification (typically Market Value, Market Rent, or specialist bases)

🔍 Inspection requirements – Appropriate inspection level for valuation purpose and property type

📊 Valuation approach – Documented methodology and reasoning

⚠️ Assumptions and special assumptions – Clear statement of any departures from standard assumptions

📝 Report format – Compliance with minimum content requirements

When professionals provide RICS Red Book valuations, adherence to these standards ensures professional credibility and reduces liability risk.

Professional Indemnity Insurance Considerations

Valuation work carries inherent professional liability risks, particularly in changing markets. Risk management strategies include:

- Maintaining adequate professional indemnity insurance coverage

- Clear documentation of valuation reasoning and evidence

- Appropriate limitation of liability clauses in terms of engagement

- Regular CPD to maintain technical competence

- Quality assurance procedures and peer review

- Prompt notification to insurers of potential claims

The stabilising market conditions of Q1 2026, with a -10% net balance, create particular risks where valuations might be challenged if market conditions subsequently deteriorate or improve significantly.

Continuing Professional Development for Market Conditions

RICS members must maintain competence through ongoing professional development. Relevant CPD topics for Q1 2026 include:

- Updated ESG valuation standards and application

- Basel 3.1 lending valuation requirements

- Regional market dynamics and performance drivers

- Technology tools and data analytics in valuation

- Legal and regulatory updates affecting property values

Engaging with professional surveying resources and industry publications helps maintain current market knowledge essential for accurate valuations.

Case Study Applications: Valuing Properties Under Stabilising Conditions

Practical examples illustrate how RICS techniques apply to real-world Q1 2026 valuation scenarios.

Case Study 1: Semi-Detached Family Home in Commuter Location

Property: 3-bedroom semi-detached house, commuter town 30 miles from major city

Context: Local market showing -8% net balance, hybrid working affecting demand patterns

Valuation approach:

- Comparable analysis – Identified 5 transactions within 6 months, ranging £285,000-£310,000

- Adjustment process:

- Location adjustments for specific street desirability (±3-5%)

- Size adjustments (subject property 1,250 sq ft vs comparables 1,150-1,350 sq ft)

- Condition adjustments (subject property recently updated kitchen/bathroom, +£8,000)

- Time adjustments applying -1% monthly market movement

- Supporting evidence – Local agent intelligence confirming asking price reductions of 5-8% typical

- Validation – Price per square foot £240-£250 consistent with local norms

Concluded value: £298,000 (mid-range of adjusted comparables, reflecting stabilising but slightly negative market sentiment)

Case Study 2: Buy-to-Let Apartment with Rental Income

Property: 2-bedroom apartment, regional city centre, tenanted at £950 pcm

Context: Rental demand strong (4.8 enquiries per property [2]), capital values stabilising

Dual valuation approach:

Comparable method:

- Recent sales of similar apartments: £165,000-£180,000

- Adjusted for floor level, parking, condition

- Comparable method indication: £172,000

Investment method:

- Annual rental income: £11,400

- Deduct management (10%): £1,140

- Net income: £10,260

- Market yield for similar properties: 6.0%

- Investment method calculation: £10,260 ÷ 0.06 = £171,000

Reconciliation: Both methods align closely, providing confidence in valuation range £171,000-£172,000. Concluded value £172,000 reflecting strong rental fundamentals supporting capital value despite broader market stabilisation.

Case Study 3: Period Property Requiring Modernisation

Property: Victorian terraced house, conservation area, requiring comprehensive updating

Context: Prime location with limited supply, but renovation costs affecting value

Residual valuation approach:

- Completed value assessment – Comparable evidence for fully renovated similar properties: £425,000-£450,000

- Renovation cost estimate:

- Full refurbishment specification: £85,000

- Professional fees (12%): £10,200

- Contingency (10%): £9,500

- Total development costs: £104,700

- Developer profit allowance – 15% of completed value: £65,000

- Residual calculation: £435,000 – £104,700 – £65,000 = £265,300

Market testing – Comparable evidence for similar unrenovated properties: £255,000-£275,000, supporting residual calculation

Concluded value: £265,000 (rounded), reflecting development potential whilst accounting for costs and risks in current market

Conclusion: Navigating Valuation Excellence in Q1 2026

Valuing properties under stabilising national prices with a Q1 2026 house price net balance of -10% demands professional excellence, technical rigour, and nuanced market understanding. The current market environment—characterised by moderate price pressure, improving sentiment, and significant regional variation—requires valuers to apply RICS-compliant methodologies with enhanced precision and careful judgement.

Key principles for valuation success in Q1 2026:

🎯 Prioritise recent, relevant comparable evidence and apply systematic adjustments reflecting current market dynamics rather than historical trends

🌍 Recognise regional variations that make national statistics insufficient for accurate local valuations

📚 Integrate updated regulatory requirements including ESG standards (effective April 2026) and Basel 3.1 lending guidance into all professional valuations

🔍 Maintain rigorous inspection standards combined with comprehensive market research to inform robust valuation conclusions

📊 Leverage technology and data analytics as supporting tools whilst preserving professional judgement as the foundation of reliable valuations

⚖️ Ensure Red Book compliance and maintain comprehensive documentation to support valuation reasoning and manage professional risk

Actionable Next Steps for Property Professionals

For surveyors and valuers operating in Q1 2026 market conditions:

- Update technical knowledge on ESG valuation standards and Basel 3.1 requirements through targeted CPD

- Strengthen local market intelligence by cultivating relationships with estate agents, fellow professionals, and market participants

- Review comparable evidence protocols to ensure recency and relevance in stabilising market conditions

- Enhance documentation practices to clearly explain valuation reasoning and evidence in professional reports

- Consider specialist surveys such as building surveys or specific defect assessments where property condition materially affects value

- Engage with professional resources and industry guidance to maintain best practice standards

The stabilising market conditions of Q1 2026 present both challenges and opportunities for property valuation professionals. By applying RICS techniques with precision, maintaining professional standards, and exercising informed judgement, chartered surveyors can deliver valuations that accurately reflect market realities whilst serving client needs and upholding public confidence in the profession.

Whether conducting valuations for purchase, lending, taxation, or other purposes, the fundamental principles remain constant: thorough investigation, robust evidence, systematic analysis, and clear communication. In navigating the nuanced landscape of stabilising national prices, these principles—combined with updated technical knowledge and professional integrity—ensure valuation excellence that serves the property market and wider economy effectively.

References

[1] Apc 5 Valuation Methods – https://ww3.rics.org/uk/en/journals/property-journal/apc-5-valuation-methods.html

[2] Lettings Tenant Demand Uptick Valuation Surveys For Constrained Rental Supply In Q1 2026 – https://nottinghillsurveyors.com/blog/lettings-tenant-demand-uptick-valuation-surveys-for-constrained-rental-supply-in-q1-2026

[3] Rics Updates Global Guidance On Bank Lending Valuations With Two Key Publications – https://www.rics.org/news-insights/rics-updates-global-guidance-on-bank-lending-valuations-with-two-key-publications

[4] Rics Publishes Updated Global Standard Esg Sustainability Commercial Property Valuation – https://www.rics.org/news-insights/rics-publishes-updated-global-standard-esg-sustainability-commercial-property-valuation

[5] Valuation Techniques For Stabilising National House Prices Rics January 2026 Survey Insights For Surveyors – https://nottinghillsurveyors.com/blog/valuation-techniques-for-stabilising-national-house-prices-rics-january-2026-survey-insights-for-surveyors