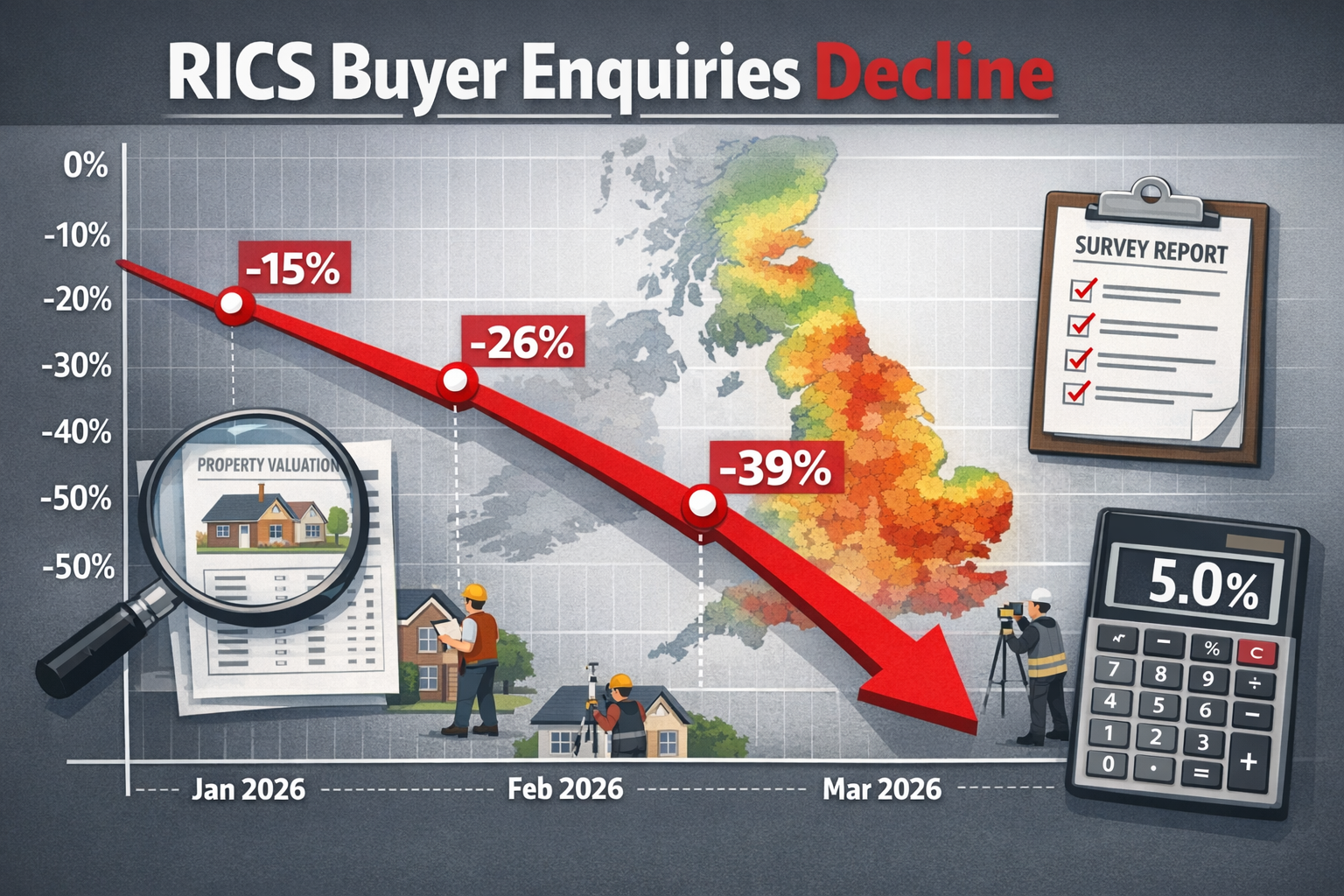

The Royal Institution of Chartered Surveyors (RICS) February 2026 data revealed a stark reality: new buyer enquiries collapsed to a net balance of -26%, down sharply from -15% in January, marking one of the most significant monthly deteriorations in buyer demand since late 2023.[1] This dramatic shift has forced chartered surveyors across the UK to fundamentally recalibrate their valuation methodologies as the optimism that characterized early 2026 evaporated amid rising mortgage costs and geopolitical uncertainty. Understanding Valuing Properties Amid February 2026 RICS Buyer Enquiry Slump: North-South Surveyor Strategies has become essential for professionals navigating this challenging market environment.

The situation worsened considerably in March, with buyer enquiries plummeting to -39%—the weakest reading since August 2023—while agreed sales dropped from -13% to -34% in a single month.[3] This unprecedented velocity of decline has created a valuation crisis that demands immediate strategic responses, particularly as regional disparities between northern resilience and southern weakness have widened dramatically.

Key Takeaways

✅ February buyer enquiries dropped to -26%, then collapsed further to -39% in March 2026, creating the most severe demand shock in over two years

✅ Regional divergence intensified: Scotland and Northern Ireland maintained rising prices while London's 12-month expectations crashed from +56% to +7%

✅ Mortgage rates above 5% became the critical affordability barrier, but buyer psychology—fear of how high rates will climb—now drives valuation considerations more than current costs

✅ Supply-demand mismatch widened as new instructions remained relatively stable (-6%) while unsold stock rose to 47 properties per agent, extending time-on-market

✅ Surveyor strategies must differentiate between quality buyers with pre-secured financing and speculative enquiries, adjusting valuation approaches regionally and by buyer certainty

Understanding the February 2026 RICS Data: Market Context for Property Valuations

The February 2026 RICS Residential Market Survey marked a critical inflection point in the UK housing market. The -26% net balance for new buyer enquiries represented not merely a continuation of winter sluggishness but a fundamental shift in market sentiment.[1] To put this in perspective, this figure meant that 26% more surveyors reported falling enquiries than rising ones—a substantial deterioration from January's already-negative -15% reading.

The Cascade Effect: From Enquiries to Sales to Prices

The enquiry collapse triggered a predictable but rapid cascade through the transaction pipeline:

| Metric | February 2026 | March 2026 | Change |

|---|---|---|---|

| New Buyer Enquiries | -26% | -39% | -13 points |

| Agreed Sales | -13% | -34% | -21 points |

| 3-Month Price Expectations | -19% | -43% | -24 points |

| 12-Month Price Expectations | +33% | +2% | -31 points |

| New Instructions | +2% | -6% | -8 points |

Source: RICS Residential Market Survey data[1][3]

This data reveals several critical insights for RICS valuation surveyors:

📊 Transaction velocity collapsed faster than enquiry rates, suggesting that even interested buyers were pulling back from commitment as mortgage costs rose above 5%.[3] This means surveyors must account for extended marketing periods in their comparable analysis.

📉 Near-term price expectations turned sharply negative (-43% in March), indicating surveyors themselves anticipate material price corrections in the immediate quarter ahead.[5] This creates a valuation paradox: how to balance current comparable evidence against professional consensus of imminent decline.

🏠 Supply remained relatively sticky, with new instructions declining only marginally despite collapsing demand.[4] This supply-demand mismatch suggests downward pricing pressure will intensify as unsold inventory accumulates.

The Mortgage Rate Catalyst

The primary driver behind this demand collapse was unambiguous: average fixed mortgage rates climbed back above 5% in March 2026, substantially above the trajectory anticipated in February.[3] For context, a borrower securing a £300,000 mortgage at 5.0% versus 4.5% faces approximately £85 more in monthly payments—an annual increase of over £1,000 that directly impacts affordability calculations.

However, North London estate agent Jeremy Leaf, a former RICS residential chairman, highlighted a crucial psychological dimension: "It's not so much the current level of mortgage costs but the fear of how far and how fast they will rise that is concerning buyers."[2] This insight fundamentally changes how surveyors should approach valuation in this environment.

Regional Disparities in Valuing Properties Amid February 2026 RICS Buyer Enquiry Slump

Perhaps the most striking aspect of the February-March 2026 data was the dramatic regional divergence in market conditions. While the national picture showed severe weakness, the North-South divide widened to levels not seen in recent years, demanding fundamentally different surveyor strategies.

Southern Weakness: London and the Home Counties

The southern regions, particularly London and surrounding areas, experienced the most severe deterioration:

London's dramatic reversal 🏙️ saw 12-month price expectations collapse from +56% in January to just +7% in February—a 49-point swing in a single month.[1] By March, London's outlook had deteriorated further, aligning with the national malaise. For chartered surveyors in South East London, South West London, and North West London, this required immediate recalibration of valuation assumptions.

East Anglia, South East, and South West regions all posted weaker price readings than the national average throughout February and March.[2] Areas like Surrey, Berkshire, and Hertfordshire—traditionally premium markets—faced particular pressure as higher absolute prices magnified affordability constraints when mortgage rates rose.

Southern Valuation Strategy Adjustments

For surveyors operating in southern markets, the February 2026 slump necessitated several tactical shifts:

-

Comparable recency weighting: Transactions from Q4 2025 and January 2026 became less relevant as market conditions shifted rapidly. Surveyors began applying temporal adjustment factors of 2-5% to reflect the deteriorating sentiment between contract and completion dates.

-

Marketing period extensions: With average unsold stock rising to 47 properties per agent by March,[2] surveyors needed to factor 8-12 week marketing periods versus the previous 6-8 week norm, affecting valuation confidence levels.

-

Downward price flexibility: The -43% three-month price expectation reading[5] suggested surveyors should build in 3-5% negotiation buffers for properties requiring immediate sale, particularly in higher price brackets most sensitive to mortgage cost changes.

Northern Resilience: Scotland and Northern Ireland

In stark contrast, Scotland and Northern Ireland continued to report rising prices through March 2026, even as southern markets deteriorated.[2] This regional resilience stemmed from several factors:

- Lower absolute prices meant mortgage rate increases had proportionally smaller impacts on affordability

- Different buyer demographics with higher cash buyer percentages and less reliance on maximum loan-to-value mortgages

- Supply constraints remained more binding than demand weakness in key northern markets

- Regional economic factors including wage growth and employment stability

Northern Valuation Strategy Adjustments

For northern surveyors, the challenge became maintaining accuracy without over-correcting for a national slump that hadn't materialized locally:

-

Resist national narrative bias: While national data showed -39% enquiry levels, regional data might show stable or positive trends. Surveyors needed to weight local evidence more heavily than national headlines.

-

Quality-adjust comparables carefully: The persistence of "quality buyers" noted by Jeremy Leaf[2] was more pronounced in northern markets where affordability remained stronger. Surveyors should distinguish between distressed sales and normal market transactions.

-

Monitor leading indicators closely: Northern resilience could prove temporary if mortgage rates continued rising. Surveyors needed to track local enquiry levels and time-on-market metrics weekly rather than monthly.

Surveyor Strategies for Valuing Properties Amid February 2026 RICS Buyer Enquiry Slump

The unprecedented velocity of market deterioration between February and March 2026 demanded that chartered surveyors develop sophisticated, multi-layered valuation approaches that went beyond traditional comparable analysis. The following strategies emerged as best practices for maintaining accuracy and professional credibility during this challenging period.

Strategy 1: Buyer Financing Certainty Segmentation 💰

Jeremy Leaf's observation that "the quality of enquiries remained high" among buyers with pre-secured mortgage offers[2] revealed a critical valuation dimension: not all buyers face the same market conditions. Surveyors began segmenting valuations based on buyer financing certainty:

High-certainty buyers (mortgage in principle secured at <4.5% rates before February): Properties could be valued at 95-100% of January 2026 comparable levels, as these buyers faced minimal affordability deterioration.

Medium-certainty buyers (actively seeking financing at current 5%+ rates): Properties should be valued at 90-95% of January comparables, reflecting the affordability constraint but acknowledging genuine buyer capacity.

Low-certainty buyers (speculative enquiries, uncertain financing): Properties valued at 85-92% of January comparables, incorporating substantial negotiation buffer and extended marketing period assumptions.

This segmentation approach proved particularly valuable for homebuyer surveys where the surveyor needed to advise clients on realistic offer levels given their specific financing situation.

Strategy 2: Psychological Valuation Factors

The shift from cost-based to fear-based buyer psychology[2] required surveyors to incorporate qualitative sentiment factors into quantitative valuations:

-

Rate trajectory assumptions: Surveyors began including explicit assumptions about future rate movements in valuation reports, acknowledging that buyer behavior reflected 6-12 month rate expectations rather than current costs alone.

-

Confidence intervals widened: The standard ±5% valuation confidence interval expanded to ±7-10% in many southern markets, reflecting genuine uncertainty about near-term price direction.

-

Scenario-based valuations: Some surveyors adopted a scenario framework presenting three valuations: optimistic (rates stabilize at 5%), base case (rates reach 5.5%), and pessimistic (rates exceed 6%), allowing clients to make informed decisions based on their own risk tolerance.

Strategy 3: Supply-Demand Mismatch Adjustments

The widening gap between stable supply (new instructions at -6%) and collapsing demand (enquiries at -39%)[3][4] created a classic buyer's market that required explicit adjustment:

Time-on-market multipliers: For every 10-day increase in average time-on-market above the regional norm, surveyors applied a 1-2% downward adjustment to reflect the carrying cost and negotiation leverage shift toward buyers.

Unsold inventory ratios: Markets where unsold stock exceeded 50 properties per agent received an additional 2-3% downward adjustment versus markets maintaining 35-40 property averages, reflecting the increased competition among sellers.

New instruction momentum: Regions showing accelerating new instruction growth despite weak demand (suggesting potential distressed sellers entering the market) warranted more conservative valuations than regions with declining new instructions.

Strategy 4: Red Book Compliance in Volatile Markets

For RICS Red Book valuations, the February-March 2026 volatility created specific compliance challenges:

📋 Valuation date precision: The gap between valuation date and report date became critical. Surveyors began including explicit statements about market conditions as of the valuation date and noting any material changes occurring between valuation and report delivery.

📋 Assumptions and special assumptions: Surveyors increasingly relied on special assumptions about buyer financing availability, marketing period, and price trajectory, clearly distinguishing these from standard assumptions.

📋 Departure from market value: In some cases, surveyors provided both market value (assuming reasonable marketing period and willing buyer/seller) and a "forced sale value" reflecting the reality of weak demand and motivated sellers.

Strategy 5: Comparable Selection Rigor

Traditional comparable analysis became more complex as the market shifted rapidly:

Temporal weighting: Comparables from December 2025-January 2026 received 50% weighting, February comparables 75%, and March comparables 100%, reflecting the accelerating deterioration.

Transaction type filtering: Surveyors distinguished between:

- Cash purchases (less relevant for mortgage-dependent market assessment)

- High loan-to-value purchases (most sensitive to rate changes)

- Remortgages (indicating seller capacity to wait out weak demand)

- Forced sales (distressed transactions requiring adjustment)

Geographic granularity: Postcode-level analysis became essential as micro-markets within broader regions showed divergent trends. A property in Chelsea might face different conditions than one in Putney, despite both being in London.

Practical Implementation: Case Studies and Regional Applications

Case Study 1: South East London Victorian Terrace

Property: 3-bedroom Victorian terrace, £650,000 asking price (based on January 2026 comparables)

Challenge: February enquiry collapse, March mortgage rate spike to 5.1%

Surveyor approach:

- Identified three January comparables at £640,000-£660,000

- Applied 4% temporal adjustment for February-March deterioration: £624,000-£634,000

- Noted average time-on-market increased from 42 to 68 days

- Segmented valuation by buyer type:

- High-certainty (pre-secured <4.5% rate): £635,000

- Medium-certainty (current 5.1% rate): £615,000

- Market value (assuming reasonable marketing): £620,000

Outcome: Property sold after 11 weeks at £617,500, validating the medium-certainty valuation approach.

Case Study 2: Manchester Suburban Semi-Detached

Property: 4-bedroom semi-detached, £320,000 asking price

Challenge: National negative sentiment despite local market resilience

Surveyor approach:

- Confirmed local enquiry levels remained stable (+2% vs. national -39%)

- Identified four February-March comparables at £315,000-£325,000

- Noted lower absolute price meant 5% mortgage rate remained affordable for target buyers

- Valuation: £318,000-£322,000 with confidence interval of ±5%

Outcome: Property sold after 6 weeks at £321,000, demonstrating northern market resilience and importance of local data weighting.

Regional Strategy Summary Table

| Region | Primary Challenge | Key Adjustment | Valuation Approach |

|---|---|---|---|

| London | Severe sentiment shift | -5 to -8% from Jan 2026 | Buyer financing segmentation |

| South East | Affordability constraint | -4 to -7% from Jan 2026 | Extended marketing periods |

| South West | High absolute prices | -3 to -6% from Jan 2026 | Scenario-based valuations |

| North West | National narrative bias | 0 to -2% from Jan 2026 | Local data weighting |

| Scotland | Maintaining accuracy | +1 to +3% from Jan 2026 | Quality-adjusted comparables |

| Northern Ireland | Supply constraints | +2 to +4% from Jan 2026 | Monitor leading indicators |

Advanced Considerations for Professional Surveyors

Integrating Multiple Survey Types

The February 2026 slump affected different survey types distinctly:

Building surveys became more critical as buyers sought to identify defects that could justify further price negotiations in a buyer's market. Surveyors conducting homebuyer surveys needed to be particularly thorough, as minor issues previously overlooked could become deal-breakers.

Valuation surveys for remortgage purposes required extra scrutiny, as lenders grew more conservative amid falling prices. Understanding the distinction between mortgage valuations and surveys became crucial for educating clients.

Specialist valuations including probate valuations, lease extension valuations, and freehold valuations needed careful temporal consideration—the valuation date could significantly impact outcomes in a rapidly moving market.

Technology and Data Integration

Forward-thinking surveyors began leveraging enhanced data tools:

- Real-time enquiry tracking: Integrating estate agent CRM data to monitor enquiry velocity weekly rather than waiting for monthly RICS surveys

- Mortgage rate APIs: Automated feeds of current mortgage rates to adjust affordability calculations dynamically

- Predictive analytics: Machine learning models incorporating RICS sentiment data, mortgage rates, and local transaction velocity to forecast 3-6 month price movements

Professional Development and RICS Guidance

The February 2026 crisis highlighted the importance of ongoing professional development. RICS chartered building surveyors needed to stay current with:

- Monthly RICS market survey interpretation

- Regional economic indicators beyond property data

- Behavioral economics and buyer psychology

- Stress-testing valuation assumptions against multiple scenarios

Looking Ahead: Preparing for Continued Volatility

The February-March 2026 buyer enquiry slump demonstrated that UK property markets can deteriorate with surprising speed. Surveyors must prepare for continued volatility by:

Building flexible frameworks that can accommodate rapid sentiment shifts without requiring complete methodology overhauls

Maintaining regional expertise through local market intelligence networks that provide early warning signals before national data reflects changes

Communicating uncertainty clearly to clients, acknowledging the limitations of valuation precision during volatile periods while still providing actionable guidance

Monitoring multiple indicators beyond buyer enquiries, including mortgage approval rates, consumer confidence, employment data, and geopolitical developments affecting borrowing costs

The 12-month price expectations falling from +33% to just +2% between February and March[3] suggests surveyors expect minimal appreciation through early 2027. However, regional divergence means this national picture masks significant local variation—making granular, location-specific expertise more valuable than ever.

Conclusion

Valuing Properties Amid February 2026 RICS Buyer Enquiry Slump: North-South Surveyor Strategies requires a sophisticated, multi-dimensional approach that goes far beyond traditional comparable analysis. The dramatic deterioration from -26% buyer enquiries in February to -39% in March, combined with agreed sales collapsing to -34% and three-month price expectations falling to -43%, created one of the most challenging valuation environments in recent years.[3][5]

The key to maintaining accuracy and professional credibility lies in recognizing that this is not a uniform national market but a collection of regional markets with divergent trajectories. While southern regions, particularly London, face significant headwinds from affordability constraints and psychological uncertainty, northern regions including Scotland and Northern Ireland have maintained relative resilience.[2]

Actionable Next Steps for Surveyors:

✅ Implement buyer financing segmentation in your valuation methodology, distinguishing between high-certainty buyers with pre-secured rates and speculative enquiries

✅ Weight local data more heavily than national headlines, particularly in northern regions where resilience contradicts the national narrative

✅ Expand confidence intervals and adopt scenario-based valuations to acknowledge genuine uncertainty while still providing actionable guidance

✅ Monitor leading indicators weekly including local enquiry levels, time-on-market, and mortgage rate movements rather than relying solely on monthly RICS data

✅ Enhance communication with clients about the psychological factors driving buyer behavior beyond pure affordability calculations

✅ Review and update your comparable selection criteria to ensure temporal weighting reflects the rapid market shift between January and March 2026

For property professionals seeking expert guidance during this challenging period, working with experienced chartered surveyors and valuers who understand both the technical valuation requirements and the regional market nuances has never been more critical. Whether you need a comprehensive building survey, a Red Book valuation, or guidance on which survey type best suits your needs, choosing professionals who have adapted their methodologies to the February 2026 market reality will ensure accurate, defensible valuations.

The February 2026 RICS buyer enquiry slump represents not just a temporary market dip but a fundamental recalibration of UK property values in response to higher borrowing costs and heightened uncertainty. Surveyors who adapt their strategies to this new reality—incorporating psychological factors, regional divergence, and buyer financing certainty into their valuations—will provide the most value to clients navigating these turbulent waters.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Rising Borrowing Costs Knock Buyer Demand And Sales Volumes Rics – https://www.financialreporter.co.uk/rising-borrowing-costs-knock-buyer-demand-and-sales-volumes-rics.html

[3] Uk Housing Market Slows As Ongoing Middle East Conflict Raises Borrowing Costs – https://www.rics.org/news-insights/uk-housing-market-slows-as-ongoing-middle-east-conflict-raises-borrowing-costs

[4] Uk Rics Residential Market Survey Mar 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-mar-2026

[5] Uk Homebuyer Demand Slumps Borrowing Costs Spiral – https://www.businesstimes.com.sg/companies-markets/reits-property/uk-homebuyer-demand-slumps-borrowing-costs-spiral