Northern England has emerged as a beacon of opportunity for first-time buyers in 2026, with a remarkable shift in market dynamics that hasn't been seen in over a decade. While property prices across the UK have experienced varied trajectories, Northern England's housing market presents a unique advantage: wages are finally outpacing house price increases. This fundamental change creates an unprecedented window for aspiring homeowners to enter the property ladder with greater confidence. Understanding Valuation Techniques for First-Time Buyer Properties in Northern England: Leveraging 2026 Affordability Gains becomes essential for buyers seeking to maximize this opportunity and make informed purchasing decisions in cities like Manchester, Leeds, Liverpool, Sheffield, and Newcastle.

The combination of resilient price growth, improved wage conditions, and buyer-favorable market dynamics demands precise valuation methodologies. First-time buyers must navigate this landscape armed with professional RICS valuation techniques to accurately assess property value and secure their investment for the long term.

Key Takeaways

- Northern England's affordability ratio has improved significantly in 2026, with wage growth outpacing house price increases for the first time since 2014, creating optimal conditions for first-time buyers

- RICS-compliant valuation methods including comparative market analysis, income approach, and cost-based assessments provide accurate property valuations essential for mortgage approval and investment protection

- Location-specific factors such as transport links, regeneration projects, and local employment hubs substantially impact property values across Northern England's diverse housing markets

- Professional chartered surveyors deliver comprehensive valuations that account for regional market nuances, helping first-time buyers avoid overpaying in competitive bidding situations

- Leveraging 2026's market conditions requires combining multiple valuation techniques with local market knowledge to identify genuine value opportunities in the Northern England property landscape

Understanding Northern England's 2026 Property Market Dynamics

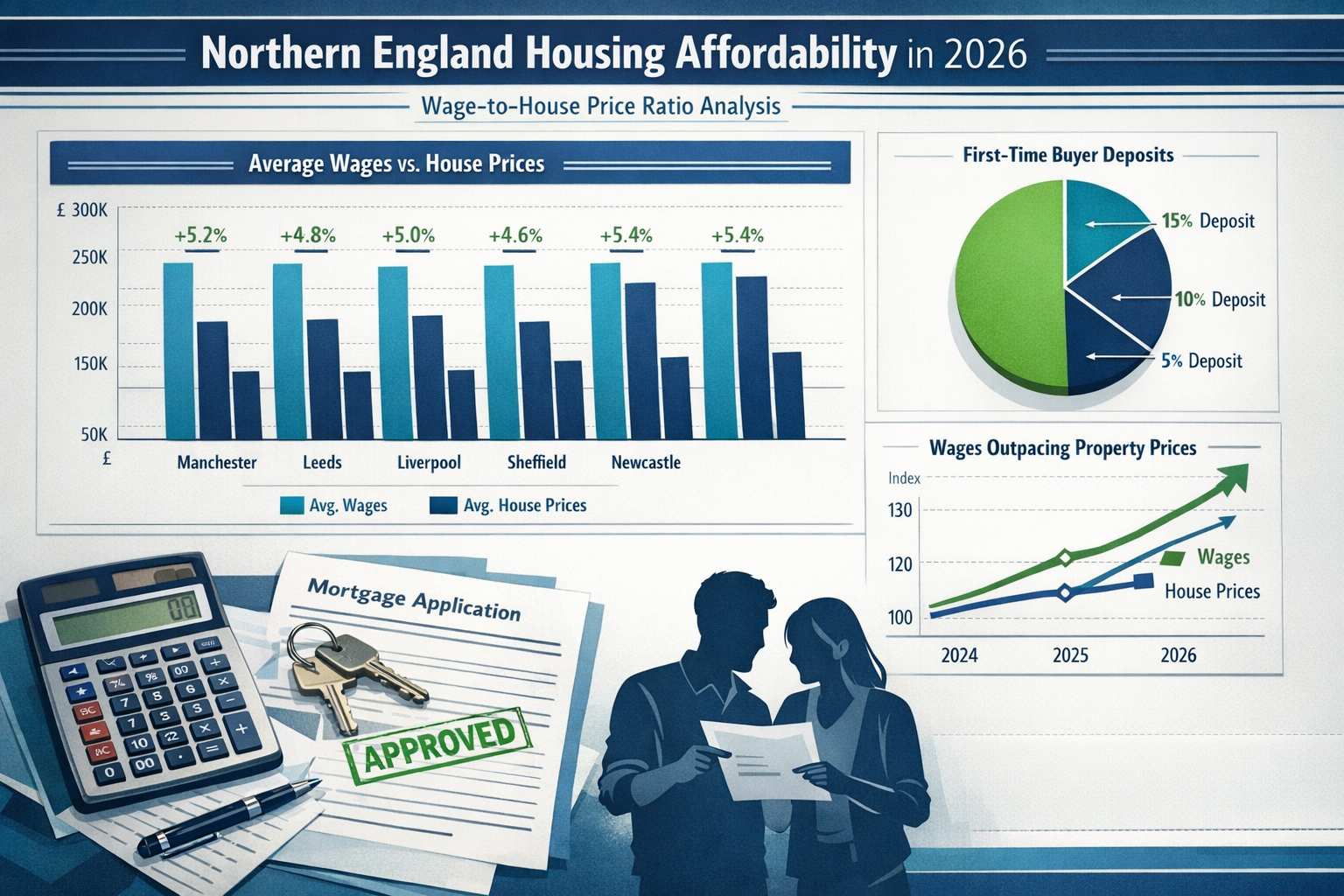

The Northern England property market has undergone significant transformation throughout 2025 and into 2026. Manchester, Leeds, Liverpool, Sheffield, and Newcastle have all experienced steady but modest price growth, typically ranging between 2-4% annually—well below the national inflation rate and significantly lower than wage increases in these regions.

The Wage-to-House-Price Advantage

For the first time in over a decade, average wages in Northern England are growing faster than property prices. This creates a shrinking affordability gap that benefits first-time buyers:

- Average wage growth in Northern England: 4.5-5.2% (2025-2026)

- Average house price growth in Northern England: 2.3-3.8% (2025-2026)

- Affordability ratio improvement: approximately 1.5-2% annually

This mathematical advantage means that first-time buyers who delayed purchases in previous years now face relatively better conditions. A property that required 5.5 times average earnings in 2024 might only require 5.2 times earnings in 2026—a meaningful difference when securing mortgage approval.

Regional Variations Within Northern England

Not all Northern England markets behave identically. Understanding these variations is crucial when applying valuation techniques:

| City/Region | Average First-Time Buyer Property Price | Year-on-Year Growth | Affordability Index |

|---|---|---|---|

| Manchester | £195,000 – £235,000 | 3.2% | Moderate |

| Leeds | £180,000 – £220,000 | 2.8% | Good |

| Liverpool | £165,000 – £200,000 | 2.5% | Excellent |

| Sheffield | £170,000 – £205,000 | 2.3% | Excellent |

| Newcastle | £155,000 – £190,000 | 2.7% | Excellent |

These figures represent typical two-bedroom terraced houses or apartments suitable for first-time buyers. The variations reflect local employment opportunities, transport infrastructure, and regeneration investment.

Core Valuation Techniques for First-Time Buyer Properties in Northern England

Professional property valuation requires systematic methodology rather than guesswork. Understanding factors of valuation helps first-time buyers appreciate how professionals assess property worth in the Northern England context.

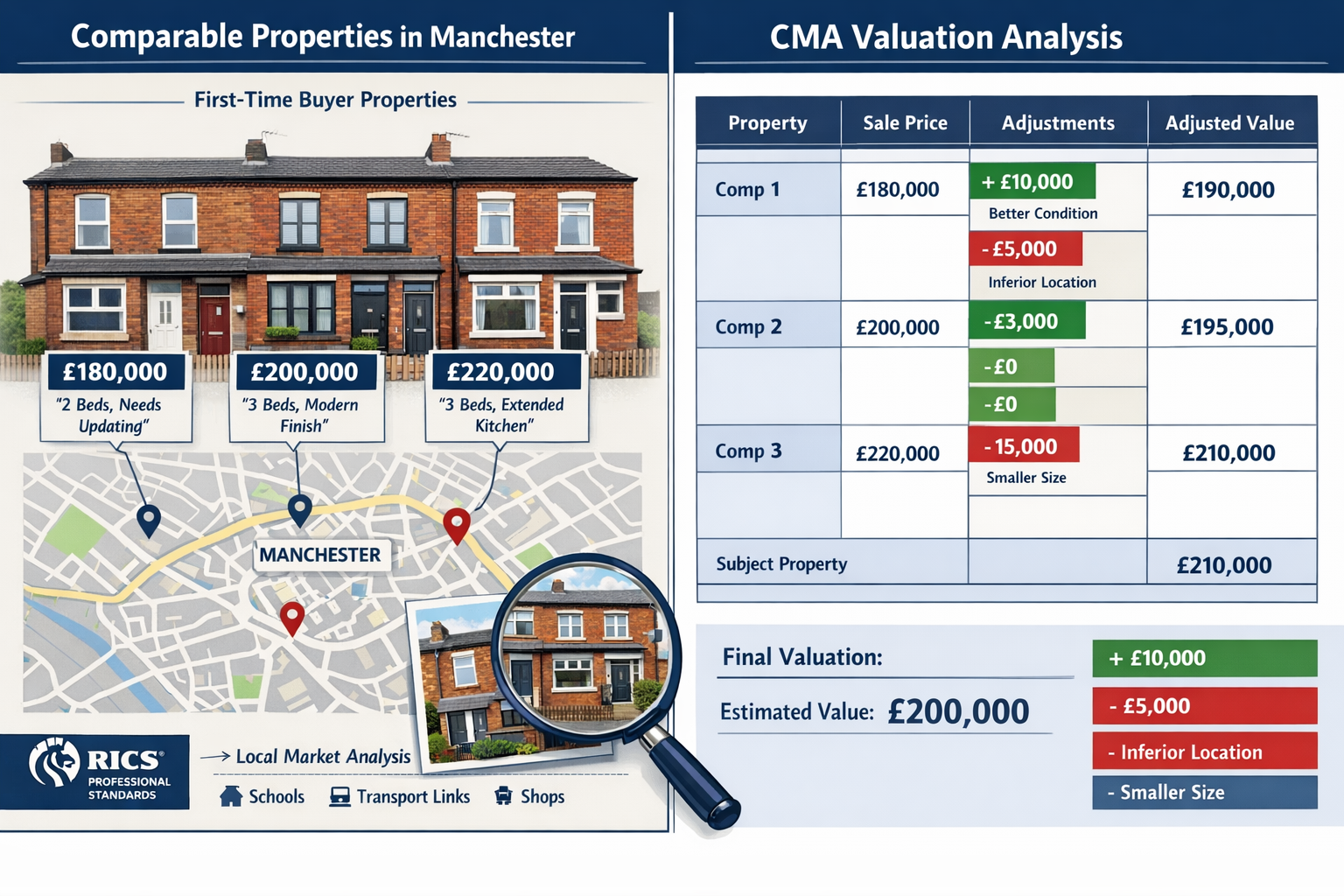

1. Comparative Market Analysis (CMA) Method 🏘️

The Comparative Market Analysis remains the most widely used valuation technique for residential properties in Northern England. This method examines recently sold properties with similar characteristics to establish market value.

Key steps in CMA for Northern England properties:

- Identify comparable properties within 0.5-1 mile radius

- Select sales from the past 3-6 months to ensure current market conditions

- Adjust for differences in size, condition, features, and location

- Calculate adjusted value based on weighted comparisons

Northern England-specific considerations:

- Terraced housing dominance: Many first-time buyer properties are Victorian or Edwardian terraces requiring specific comparison criteria

- Regeneration impact: Properties near major regeneration projects (Northern Powerhouse initiatives) command premiums

- Transport accessibility: Proximity to Metrolink (Manchester), Leeds rail hub, or other transport nodes significantly affects value

- Period features: Original features in older properties add value when well-maintained

"In Northern England's first-time buyer market, two identical terraced houses can differ by £20,000-£30,000 based solely on street location and proximity to amenities. Proper comparative analysis must account for these micro-location factors." — RICS Chartered Surveyor

2. Income Approach for Investment-Minded First-Time Buyers

While traditionally associated with commercial property, the income approach has relevance for first-time buyers considering properties with rental potential, particularly popular in Northern England's strong rental markets.

This method calculates value based on potential rental income:

Formula: Property Value = Annual Rental Income ÷ Capitalization Rate

For Northern England first-time buyer properties:

- Typical rental yields: 5-7% (higher than Southern England)

- Capitalization rates: 6-8% depending on location and property type

- Rental demand: Strong in university cities (Manchester, Leeds, Sheffield)

Example calculation:

- Two-bedroom terraced house in Leeds

- Monthly rent: £850

- Annual rental income: £10,200

- Capitalization rate: 7%

- Indicated value: £10,200 ÷ 0.07 = £145,714

This technique helps first-time buyers assess whether a property offers good value if they plan to rent out a room or eventually convert to a buy-to-let investment.

3. Cost-Based Valuation Approach

The cost approach estimates value by calculating the cost to rebuild the property plus land value, minus depreciation. While less common for standard residential valuations, it proves valuable for:

- Unique properties without many comparables

- Newly built first-time buyer homes in Northern England developments

- Properties requiring significant renovation

Understanding reinstatement valuation principles helps buyers appreciate the relationship between rebuild costs and market value.

Components of cost-based valuation:

- Land value (varies significantly across Northern England)

- Construction costs (£1,200-£1,800 per square meter for standard builds)

- Professional fees (architects, surveyors, legal)

- Depreciation (age, condition, functional obsolescence)

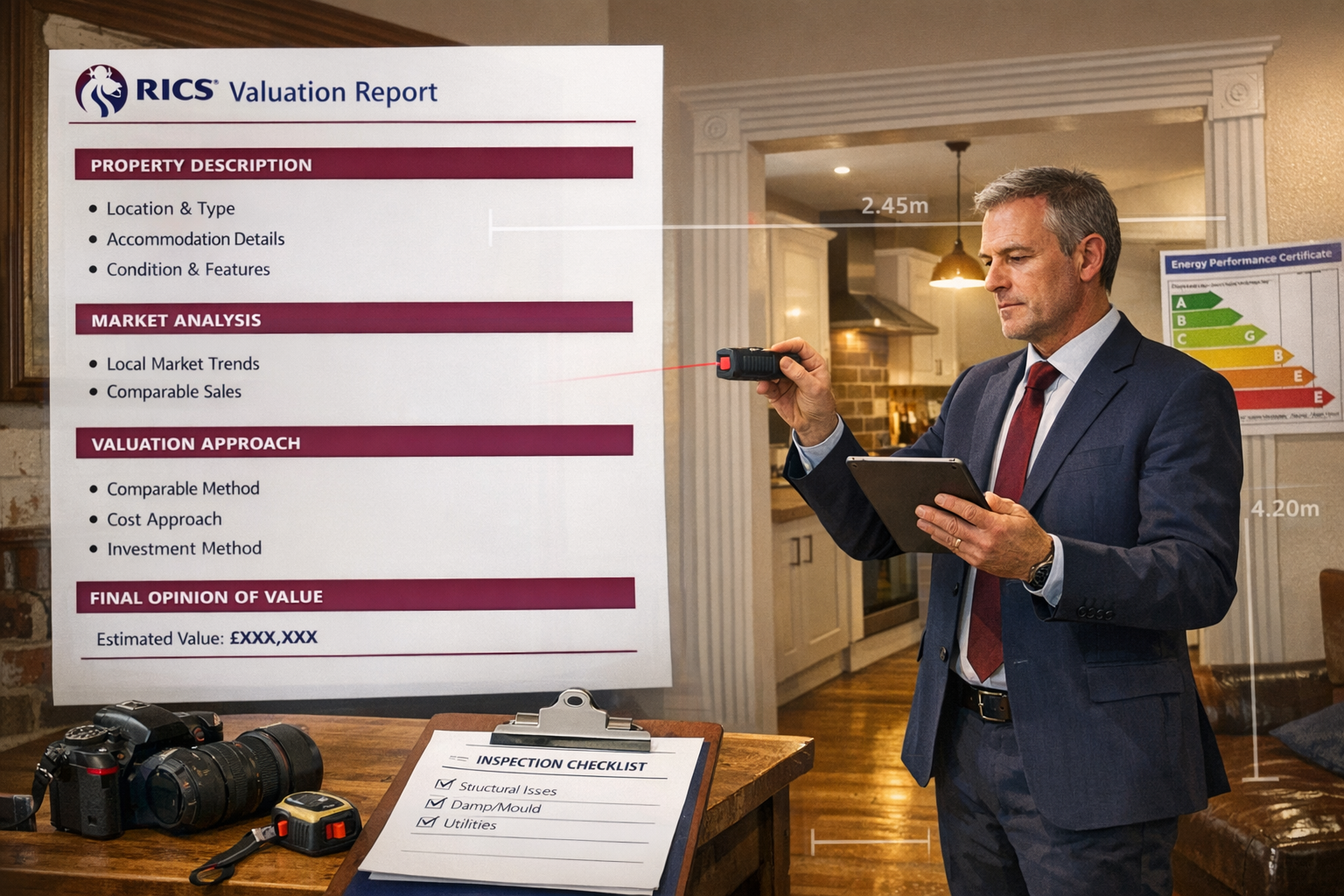

4. RICS Red Book Valuation Standards

For mortgage purposes and professional assurance, RICS Red Book valuations represent the gold standard. These comprehensive assessments follow strict professional guidelines ensuring consistency and reliability.

What RICS valuations include:

- ✅ Detailed property inspection

- ✅ Market analysis and comparable evidence

- ✅ Condition assessment

- ✅ Risk factors identification

- ✅ Formal valuation report

- ✅ Professional indemnity insurance backing

First-time buyers should understand that a mortgage valuation is not the same as a survey. While lenders conduct basic valuations to protect their investment, buyers benefit from comprehensive surveys like a Homebuyer Survey that reveals property condition issues affecting value.

Leveraging 2026 Affordability Gains Through Strategic Valuation

Understanding valuation techniques means little without knowing how to apply them strategically in Northern England's 2026 market conditions. Valuation Techniques for First-Time Buyer Properties in Northern England: Leveraging 2026 Affordability Gains requires combining technical knowledge with market timing and negotiation strategy.

Identifying Undervalued Opportunities

The improved affordability ratio in 2026 creates opportunities to identify properties trading below their true value:

Indicators of undervalued properties:

- 📊 Listed longer than 60 days in current market conditions

- 🏚️ Cosmetic issues that deter less-informed buyers but don't affect structure

- 🗺️ Emerging neighborhoods near confirmed regeneration projects

- 🚉 Transport improvements announced but not yet completed

- 💼 New employment hubs attracting businesses to the area

Strategic approach:

- Obtain professional valuation before making offers

- Compare against asking price to identify negotiation room

- Factor in renovation costs if property needs work

- Consider future value drivers (transport, regeneration, employment)

Negotiation Leverage from Accurate Valuations

Armed with professional valuation evidence, first-time buyers gain substantial negotiation leverage in 2026's buyer-favorable Northern England market.

Negotiation strategies based on valuation:

- Present comparable evidence showing asking price exceeds market value

- Highlight condition issues identified in surveys that affect value

- Reference market conditions showing reduced buyer competition

- Propose fair value based on multiple valuation methods

- Remain prepared to walk away if seller unrealistic about value

Regional Hotspots for First-Time Buyers in 2026

Certain Northern England locations offer exceptional value opportunities when applying proper valuation techniques:

Manchester suburbs:

- Levenshulme, Chorlton, and Didsbury fringes

- Strong transport links and community amenities

- Values: £190,000-£230,000 for two-bedroom properties

Leeds emerging areas:

- Harehills, Armley, and Beeston

- Regeneration investment and improving infrastructure

- Values: £165,000-£200,000 for starter homes

Liverpool regeneration zones:

- Baltic Triangle, Anfield, and Wavertree

- Cultural investment and employment growth

- Values: £155,000-£185,000 for first-time buyer properties

Sheffield opportunity areas:

- Kelham Island, Sharrow, and Hillsborough

- Creative industries and student demand

- Values: £160,000-£195,000 for two-bedroom homes

Newcastle value locations:

- Jesmond fringes, Heaton, and Walker

- University proximity and rental demand

- Values: £145,000-£180,000 for starter properties

Professional Valuation Services: When and Why to Engage Experts

While understanding valuation principles empowers first-time buyers, professional expertise remains invaluable for major purchase decisions. Valuation Techniques for First-Time Buyer Properties in Northern England: Leveraging 2026 Affordability Gains often requires chartered surveyor input to maximize benefits.

Types of Professional Valuations for First-Time Buyers

Different valuation services serve different purposes in the buying process:

1. Mortgage Valuation

- Required by lenders to protect their loan

- Basic assessment of property value

- Does NOT identify defects or condition issues

- Cost: Usually £250-£400 in Northern England

2. RICS Homebuyer Report (Level 2)

- Comprehensive condition assessment

- Market valuation included

- Identifies significant defects

- Cost: Typically £400-£600 for first-time buyer properties

- Recommended for most Northern England purchases

3. RICS Building Survey (Level 3)

- Most detailed inspection available

- Extensive condition analysis

- Recommended for older or unusual properties

- Cost: £600-£1,000+ depending on property size

4. Specialist Valuations

- Freehold valuation for leasehold property purchases

- Help to Buy valuations for government scheme participants

- Reinstatement valuations for insurance purposes

Selecting the Right Surveyor for Northern England Properties

Not all surveyors possess equal expertise in Northern England's specific property types and market conditions.

Selection criteria:

✅ RICS chartered status ensuring professional standards

✅ Local market knowledge of specific Northern England cities

✅ Experience with property type (Victorian terraces, ex-council flats, new builds)

✅ Clear fee structure with no hidden costs

✅ Professional indemnity insurance protecting your interests

✅ Positive client reviews and testimonials

Questions to ask potential surveyors:

- How many valuations have you completed in [specific area]?

- What valuation methodology will you use for this property type?

- How long will the inspection and report take?

- What happens if significant defects are discovered?

- Can you provide recent examples of comparable properties you've valued?

Cost-Benefit Analysis of Professional Valuations

First-time buyers often question whether professional valuation fees represent good value. The mathematics strongly support professional input:

Potential savings from professional valuation:

- Negotiation leverage: £5,000-£15,000 reduction in purchase price

- Defect identification: £10,000-£30,000 in avoided repair costs

- Mortgage confidence: Reduced risk of lender down-valuation

- Investment protection: Assurance of fair market value

Example scenario:

- Property asking price: £210,000

- Professional valuation cost: £550

- Valuation indicates fair value: £197,000

- Negotiated purchase price: £200,000

- Net benefit: £10,000 – £550 = £9,450 saved

This represents a 1,700% return on investment for the valuation fee—compelling evidence for professional input.

Technology and Data in Modern Property Valuation

The valuation landscape has evolved significantly with technology integration, particularly relevant for tech-savvy first-time buyers in 2026.

Digital Valuation Tools and Limitations

Automated Valuation Models (AVMs) use algorithms and property data to estimate values:

Advantages:

- ⚡ Instant results

- 💰 Low or no cost

- 📊 Large data sets analyzed

Limitations:

- ❌ Cannot assess property condition

- ❌ Miss unique features or defects

- ❌ Less accurate for unusual properties

- ❌ Don't account for micro-location factors

- ❌ Not accepted by mortgage lenders

Verdict: AVMs provide useful starting points but cannot replace professional valuations for purchase decisions.

Data Sources for Informed Valuation

First-time buyers can access various data sources to inform their understanding:

- Land Registry Price Paid Data: Historical sales information

- Rightmove and Zoopla: Current market listings and sold prices

- Local authority planning portals: Regeneration and development plans

- ONS regional statistics: Employment, wages, and demographic data

- Transport authority announcements: Infrastructure improvements

Combining these sources with professional valuation creates comprehensive market understanding.

Common Valuation Pitfalls for First-Time Buyers

Even with improved 2026 affordability conditions, first-time buyers can make costly valuation mistakes.

Pitfall #1: Emotional Over-Valuation 💔

The problem: Falling in love with a property and ignoring valuation evidence.

The solution: Maintain objectivity by:

- Setting maximum price limits before viewing

- Bringing a trusted friend or family member

- Always obtaining independent professional valuation

- Remembering other properties exist

Pitfall #2: Ignoring Location-Specific Factors

The problem: Applying general valuation principles without considering Northern England specifics.

The solution: Account for:

- Flood risk in certain Northern England areas

- Former industrial land contamination issues

- Mining subsidence in former coal regions

- Leasehold ground rents on certain developments

- Right to buy properties with restrictive covenants

Pitfall #3: Confusing Asking Price with Market Value

The problem: Assuming sellers' asking prices reflect true market value.

The solution: Recognize that:

- Asking prices often include negotiation buffer

- Sellers may lack accurate market knowledge

- Properties priced too high sit unsold longer

- Professional valuation reveals true worth

Pitfall #4: Neglecting Future Value Drivers

The problem: Focusing only on current value without considering appreciation potential.

The solution: Evaluate:

- 🚇 Planned transport improvements

- 🏢 Employment hub developments

- 🎓 University expansion plans

- 🏗️ Regeneration project timelines

- 🌳 Green space and amenity improvements

Pitfall #5: Skipping Professional Surveys

The problem: Relying solely on mortgage valuation to assess property.

The solution: Always commission appropriate survey level:

- New builds: Snagging survey minimum

- Standard properties: Homebuyer Report (Level 2)

- Older properties: Building Survey (Level 3)

- Specific concerns: Specialist surveys (damp, structural, etc.)

Maximizing Your Investment: Beyond Initial Valuation

Understanding valuation doesn't end at purchase—first-time buyers should consider long-term value protection and enhancement.

Value-Adding Improvements for Northern England Properties

Strategic improvements can significantly increase property value:

High-return improvements:

- Kitchen modernization: 5-10% value increase (£9,000-£18,000 on £180,000 property)

- Bathroom renovation: 4-6% value increase

- Loft conversion: 10-15% value increase (where suitable)

- Energy efficiency: Growing importance in 2026 market

- Garden landscaping: 3-5% value increase

Cost-effective enhancements:

- Fresh paint and decoration

- Improved storage solutions

- Modern lighting fixtures

- Kerb appeal improvements

- Smart home technology integration

Protecting Your Investment Through Regular Valuations

When to obtain updated valuations:

- Remortgage time (typically every 2-5 years)

- Before major renovations to assess potential return

- Considering home equity release

- Insurance policy renewals

- Marital/partnership property settlements

Regular valuations help first-time buyers understand their equity position and make informed financial decisions.

Regional Case Studies: Successful First-Time Buyer Valuations

Real examples demonstrate how proper valuation techniques create successful outcomes in Northern England's 2026 market.

Case Study 1: Manchester Terraced House Negotiation

Property: Two-bedroom Victorian terrace, Levenshulme

Asking price: £215,000

Professional valuation: £198,000

Valuation findings:

- Comparable sales: £192,000-£205,000

- Required: New boiler (£3,000), damp treatment (£2,500)

- Location: Good transport links, improving area

Outcome: Buyer negotiated to £200,000, saved £15,000, used savings for immediate repairs.

Case Study 2: Leeds New Build Assessment

Property: Two-bedroom apartment, Holbeck Urban Village

Asking price: £185,000

Professional valuation: £182,000

Valuation findings:

- Developer premium included in price

- Comparable resales: £175,000-£183,000

- Leasehold with £250 annual ground rent

- Service charges: £1,200 annually

Outcome: Buyer negotiated to £180,000, factored ongoing costs into affordability calculations.

Case Study 3: Liverpool Regeneration Opportunity

Property: Three-bedroom terrace, Anfield

Asking price: £165,000

Professional valuation: £170,000

Valuation findings:

- Recent regeneration investment nearby

- New Everton FC stadium development planned

- Property condition: Good, recently renovated

- Comparable sales trending upward

Outcome: Buyer purchased at asking price, recognizing undervaluation and future appreciation potential.

Conclusion: Empowering First-Time Buyers Through Valuation Knowledge

The Northern England property market in 2026 presents a remarkable opportunity for first-time buyers, with wages outpacing house prices and creating genuine affordability improvements. However, capitalizing on these favorable conditions requires more than simply entering the market—it demands sophisticated understanding of Valuation Techniques for First-Time Buyer Properties in Northern England: Leveraging 2026 Affordability Gains.

Professional valuation methodologies—including comparative market analysis, income approaches, cost-based assessments, and RICS Red Book standards—provide the foundation for informed purchasing decisions. These techniques, when properly applied to Northern England's specific market characteristics, help buyers identify genuine value, negotiate effectively, and protect their investment for the long term.

The key advantages of 2026's Northern England market include:

- Improved affordability ratios with wage growth exceeding property price increases

- Buyer-favorable negotiating conditions in most locations

- Strong rental yields for investment-minded purchasers

- Regeneration projects creating future value appreciation

- Diverse property stock offering options across price points

Actionable Next Steps for First-Time Buyers

To maximize the opportunities available in Northern England's 2026 property market:

- Research your target location thoroughly using Land Registry data, local market reports, and regeneration plans

- Obtain mortgage agreement in principle to understand your budget and strengthen negotiating position

- Engage RICS chartered surveyors for professional valuations on properties you're seriously considering

- Commission appropriate surveys beyond basic mortgage valuations to identify condition issues

- Use valuation evidence strategically in negotiations to achieve fair purchase prices

- Consider future value drivers including transport, employment, and regeneration factors

- Budget for improvements that will enhance value and enjoyment of your property

- Build relationships with local professionals including surveyors, conveyancers, and mortgage advisors

The combination of favorable market conditions and professional valuation expertise creates an unprecedented opportunity for Northern England's first-time buyers in 2026. By understanding and applying proper valuation techniques, buyers can confidently navigate the property market, secure fair value, and establish a strong foundation for their homeownership journey.

The improved affordability gains of 2026 won't last indefinitely—economic cycles ensure that market conditions constantly evolve. First-time buyers who act decisively, armed with professional valuation knowledge and expert support, position themselves to benefit from this favorable window and build long-term wealth through property ownership in Northern England's resilient housing markets.