The UK property market stands at a pivotal crossroads in 2026. After years of turbulence marked by rapid price escalations, interest rate shocks, and economic uncertainty, the market is entering a period of price stabilisation that demands a fundamental shift in how property professionals approach valuations. With RICS reporting that 43% of surveyors now anticipate price growth over the coming months—a stark contrast to previous pessimism—the landscape for Valuation Surveys in a Recovering Market: Navigating 2026 Price Stabilisation and Regional Variations has never been more complex or consequential.

Yet beneath this headline optimism lies a more nuanced reality. While national indicators suggest moderation and balance, the Southeast experiences price declines even as Northern markets demonstrate resilience. This regional divergence, coupled with renewed lending activity and improving affordability metrics, creates both opportunities and challenges for property valuers, buyers, and sellers alike. Understanding these dynamics isn't merely academic—it's essential for accurate appraisals, informed decision-making, and successful property transactions in today's recovering market.

Key Takeaways

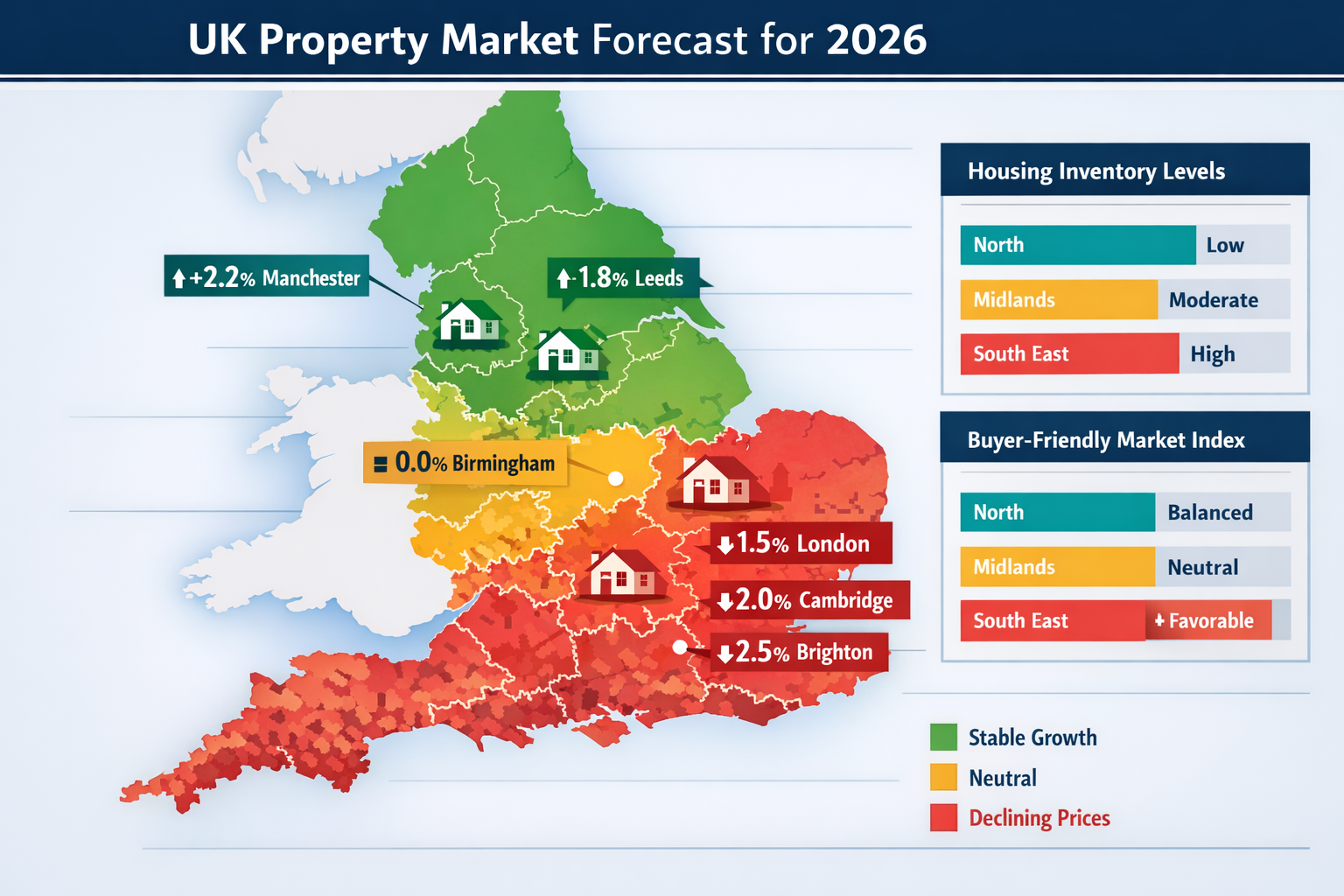

- 📊 National price growth is moderating to approximately 2.2% in 2026, representing a significant cooling from previous years' appreciation rates and marking a shift toward market equilibrium[1]

- 🗺️ Regional variations are intensifying, with Southeast England experiencing price pressures while Northern regions show greater stability, requiring location-specific valuation approaches

- 💰 Affordability is improving for the first time since 2022, with typical mortgage payments falling below 30% of household income as rates stabilize around 6.3%[1]

- 📈 Inventory levels are recovering with an 8.9% increase projected for 2026, though supply remains approximately 12% below pre-2020 averages, influencing valuation parameters[1]

- 🏘️ At least seven major markets have transitioned to buyer-friendly conditions, with this trend expected to expand throughout 2026, fundamentally altering negotiation dynamics[1]

Understanding the 2026 Market Recovery Context

The property market recovery of 2026 represents more than a simple return to pre-pandemic norms. It embodies a fundamental recalibration of expectations, pricing mechanisms, and market dynamics that property valuers must thoroughly comprehend to deliver accurate assessments.

The Moderation of Price Growth

National median price growth is projected to moderate to 2.2% in 2026, a substantial deceleration from the 4.5% appreciation witnessed in prior years[1]. This cooling reflects several converging factors: improved inventory availability, stabilizing mortgage rates, and the normalization of pandemic-driven demand spikes. For valuation professionals, this moderation necessitates recalibrating comparable sales analyses and adjusting appreciation assumptions that may have been inflated during the hyper-growth period.

Importantly, despite nominal price gains, real home prices are declining for the second consecutive year when adjusted for inflation[1]. With inflation expected to exceed 3%, the purchasing power embedded in property values is actually contracting. This distinction between nominal and real values becomes critical when conducting valuations for probate or matrimonial settlements, where precise value determination carries legal and financial consequences.

Transaction Volume Recovery

After hitting near 30-year lows in 2025, existing-home sales are projected to climb 1.7% to 4.13 million units in 2026[1]. While this increase appears modest, it represents a meaningful psychological and practical shift. The market is moving away from what realtor.com's chief economist describes as the "4 million home sales floor"—a level that indicated severe market dysfunction[2].

This recovery in transaction volumes directly impacts valuation methodologies. With more sales data available, chartered surveyors can access fresher comparables and more robust market evidence. However, the relatively low absolute volume means that each comparable carries greater weight, and outlier transactions can disproportionately influence valuation conclusions.

Inventory Dynamics and Market Balance

The 8.9% increase in active listings projected for 2026 marks the third consecutive year of inventory gains[1]. Yet despite this recovery, nationwide inventory remains roughly 12% below pre-2020 averages, creating a market that is balanced but not oversupplied. This equilibrium state—neither strongly favoring buyers nor sellers—requires valuers to exercise particular judgment in assessing market conditions and their influence on property values.

For professionals conducting RICS Red Book valuations, understanding local inventory dynamics becomes paramount. A property in a market with rapidly expanding inventory faces different appreciation prospects than one in a supply-constrained area, even if both are experiencing similar current price trends.

Valuation Surveys in a Recovering Market: Regional Variations and Their Impact

Perhaps the most significant challenge facing property valuers in 2026 is the substantial regional variation that persists despite national market stabilization[1]. The UK property market is not monolithic—it comprises dozens of distinct regional and local markets, each with unique supply-demand dynamics, economic drivers, and price trajectories.

Southeast England: Navigating Price Pressures

The Southeast, traditionally the UK's most expensive and volatile region, is experiencing downward price pressure in 2026. Years of rapid appreciation have stretched affordability to breaking points, prompting price corrections even as other regions stabilize or grow. For valuers working in this region, this creates several challenges:

Comparable selection becomes critical. Using sales from six or twelve months ago may overstate current values if prices have declined in the interim. Valuers must weight recent transactions more heavily and adjust older comparables downward to reflect current market realities.

Buyer sentiment shifts. In declining markets, buyers become more cautious and price-sensitive, often seeking concessions or extended negotiation periods. Valuations must account for this psychological dimension, particularly when assessing factors of valuation such as marketability and liquidity.

Oversupply in premium segments. The Southeast's luxury market faces particular pressure as inventory accumulates in higher price brackets. Properties valued above £1 million require especially careful analysis of comparable sales, marketing time expectations, and potential price adjustments.

Northern Resilience: Growth Amid National Stabilisation

In contrast, Northern regions including Manchester, Liverpool, and Leeds demonstrate greater price resilience and, in some cases, continued modest growth. These markets benefit from several advantages:

- Relative affordability compared to Southern counterparts

- Strong regional economies with diverse employment bases

- Infrastructure investment improving connectivity and appeal

- First-time buyer activity sustained by more accessible price points

For valuers operating in these regions, the challenge shifts from managing decline to accurately capturing growth potential without overestimating appreciation. The temptation to extrapolate recent growth trends must be tempered by recognition that national moderation will eventually influence all regional markets.

When conducting help to buy valuations or shared ownership assessments in Northern markets, valuers should consider both current resilience and potential future moderation in their long-term value projections.

Identifying Buyer-Friendly Markets

At least seven major housing markets have already transitioned into buyer-friendly territory as of 2025, with this list expected to expand throughout 2026[1]. In the United States, Indianapolis ranks as the top buyer-friendly market among the 50 largest metros, based on analysis emphasizing cooling momentum with upside appreciation potential[7].

While UK-specific rankings differ, the underlying principle applies: certain markets offer buyers favorable conditions characterized by:

- Inventory levels exceeding historical averages

- Price growth below wage growth, improving affordability

- Reduced competition among buyers

- Greater negotiating leverage for purchasers

For valuation professionals, identifying whether a property sits in a buyer-friendly, seller-friendly, or balanced market fundamentally influences assessment approaches. In buyer-friendly markets, valuations should reflect the reality that sellers may need to accept offers below asking prices, that marketing periods may extend, and that buyers have alternatives.

Valuation Surveys in a Recovering Market: Methodological Adaptations for 2026

The unique characteristics of the 2026 market recovery demand methodological adaptations from property valuers. Traditional approaches must be refined to account for stabilization dynamics, regional variations, and evolving buyer behavior.

Enhanced Comparable Sales Analysis

The comparable sales approach remains the foundation of most residential valuations, but 2026's market conditions require enhanced rigor:

Time adjustments gain importance. In a rapidly changing market, comparables from different time periods require careful adjustment. A sale from three months ago may need modification if market conditions have shifted, particularly in regions experiencing price declines or rapid inventory changes.

Geographic precision matters more. Regional variations mean that comparables must be drawn from increasingly narrow geographic areas. A property in Southeast Manchester may require different comparables than one in Northwest Manchester, even if they're only miles apart, if local market conditions diverge.

Condition and quality weighting intensifies. As buyers become more selective in a balanced market, property condition and quality features carry greater weight in value determination. A property requiring significant updates faces steeper discounts than during seller's markets when buyers competed aggressively for any available inventory.

Incorporating Market Metrics into Valuations

Modern valuation practice increasingly incorporates quantitative market metrics beyond simple comparable sales:

Days on market (DOM) analysis provides insight into property liquidity and pricing accuracy. Properties selling quickly (under 30 days) in a balanced market likely represent good value or desirable features. Those lingering (over 90 days) may be overpriced or face marketability challenges.

List-to-sale price ratios reveal negotiation dynamics. In buyer-friendly markets, these ratios decline as sellers accept offers below asking prices. Valuers should track these ratios for comparable properties to calibrate their assessments realistically.

Inventory absorption rates indicate market velocity and balance. A six-month supply represents equilibrium; lower levels favor sellers, higher levels favor buyers. Understanding local absorption rates helps valuers assess whether current pricing is sustainable or likely to adjust.

Adjusting for Affordability Improvements

One of 2026's most significant developments is the improvement in housing affordability, with typical mortgage payments falling below 30% of household income for the first time since 2022[1]. This improvement stems from two factors: moderating prices and stabilizing mortgage rates averaging 6.3% in 2026[1].

For valuers, improved affordability has several implications:

Buyer pool expansion. More households can afford properties at current prices, potentially supporting demand and stabilizing values even as appreciation slows.

Financing contingencies. With rates stabilizing rather than rising, financing contingencies become less risky, reducing transaction fall-through rates and supporting valuation confidence.

Investment property calculations. For ATED valuations and investment property assessments, improved affordability affects rental demand projections and capitalization rate selections.

Specialized Valuation Scenarios in the 2026 Market

Beyond standard market value assessments, the 2026 recovery environment creates unique considerations for specialized valuation scenarios that property professionals frequently encounter.

Mortgage Valuations in a Stabilizing Market

Mortgage valuations serve lenders' risk management needs, and the 2026 market presents specific challenges for these assessments. With prices stabilizing but regional variations persisting, mortgage valuers must:

Apply conservative approaches in declining markets. Lenders require valuations that protect their security interests. In Southeast markets experiencing price pressure, valuers should favor lower-end comparable sales and apply cautious adjustments to reflect potential further declines.

Consider loan-to-value (LTV) implications. As affordability improves, buyers may secure financing with lower LTVs, reducing lender risk. However, valuers must still ensure that assessed values reflect genuine market support rather than optimistic projections.

Account for property-specific risks. Issues like subsidence or structural concerns carry heightened significance in balanced markets where buyers have alternatives. Properties with such defects face steeper valuation discounts than during competitive seller's markets.

Probate and Estate Valuations

Probate valuations require particular precision as they determine tax liabilities and estate distributions. The 2026 market's regional variations create specific challenges:

Date-of-death valuation precision. Probate valuations must reflect market conditions on the date of death, which may differ substantially from current conditions if several months have elapsed. In regions experiencing price changes, historical market analysis becomes essential.

Marketability assessments. Estates often require rapid property sales, making marketability a critical valuation factor. In buyer-friendly markets with extended marketing periods, valuations should reflect the potential need for pricing adjustments to achieve timely sales.

Regional market knowledge. Executors and beneficiaries benefit from valuers who understand regional variations and can explain how local market conditions influence estate property values.

Lease Extensions and Freehold Valuations

Lease extension valuations and freehold valuations involve complex calculations affected by market recovery dynamics:

Deferment rates. These rates, which discount future property values to present terms, may require adjustment as market stabilization alters growth expectations. The 2.2% projected appreciation rate[1] provides useful guidance for long-term growth assumptions.

Relativity calculations. The relationship between short-lease and freehold values may shift in recovering markets as buyer preferences and financing availability evolve.

Marriage value assessments. As affordability improves and buyer pools expand, marriage values (the additional value created by combining leasehold and freehold interests) may strengthen, affecting negotiation dynamics in lease extension scenarios.

Commercial Property Valuations: Parallel Recovery Dynamics

While residential markets dominate public attention, commercial real estate experiences its own recovery trajectory in 2026, with implications for valuers operating in this sector.

Investment Activity Rebound

Commercial real estate investment activity is projected to increase 16% in 2026 to $562 billion, nearly matching pre-pandemic annual averages[3]. This recovery reflects:

- Stabilizing interest rates improving investment returns relative to financing costs

- Clearer market direction reducing uncertainty that paralyzed 2024-2025 investment decisions

- Pent-up demand from investors who delayed acquisitions during market turbulence

For commercial property valuers, this activity increase provides richer transaction evidence and clearer market signals, enhancing valuation confidence and accuracy.

Cap Rate Compression

Capitalization rates are expected to compress by 5 to 15 basis points across most property types[3], indicating stronger investor demand and improving property valuations. This compression reflects:

Improved risk perceptions. As economic uncertainty diminishes, investors accept lower returns for perceived stability.

Competitive capital deployment. With $562 billion seeking investment opportunities, competition for quality assets intensifies, driving prices higher and cap rates lower.

Sector-specific dynamics. Industrial and multifamily properties may experience greater compression than office or retail, reflecting divergent demand fundamentals.

When conducting commercial property surveying and valuations, professionals must carefully analyze sector-specific trends and avoid applying blanket assumptions across property types.

Sector Variations in Commercial Recovery

Not all commercial sectors recover uniformly:

Industrial and logistics continue strong performance driven by e-commerce growth and supply chain reconfiguration. Valuations in this sector should reflect sustained demand and limited supply in prime locations.

Multifamily residential benefits from affordability challenges in for-sale markets, supporting rental demand. However, new supply in some markets may pressure rents and cap rates.

Office properties face ongoing uncertainty regarding remote work patterns and space utilization. Valuers must carefully assess building quality, location, and tenant composition, as these factors increasingly differentiate winners from losers.

Retail experiences bifurcation, with experiential and convenience-oriented properties outperforming traditional enclosed malls. Location and tenant mix become critical valuation determinants.

Technology and Data in Modern Valuation Practice

The 2026 market recovery coincides with accelerating technological adoption in property valuation, offering tools that enhance accuracy and efficiency while raising new methodological questions.

Automated Valuation Models (AVMs)

AVMs have evolved significantly, incorporating machine learning algorithms that analyze vast datasets to generate value estimates. In 2026's recovering market, AVMs offer:

Rapid preliminary assessments useful for portfolio valuations, initial lending decisions, or market trend analysis.

Consistent methodology eliminating individual bias and ensuring reproducible results across large property portfolios.

Market trend identification by analyzing thousands of transactions to detect emerging patterns invisible to individual valuers.

However, AVMs face limitations in 2026's regionally varied market:

Regional variation blindness. National or regional models may miss hyper-local market dynamics that significantly influence individual property values.

Unique property challenges. Properties with unusual features, significant defects, or non-standard characteristics often receive inaccurate AVM valuations.

Lag in market turning points. AVMs rely on historical data and may not quickly capture market inflections, particularly problematic in transitioning markets like Southeast England's price declines.

Professional valuers increasingly adopt hybrid approaches, using AVMs for initial assessments while applying professional judgment and local knowledge to refine conclusions, particularly for high-value or complex properties requiring RICS building surveys or Level 3 surveys.

Data Sources and Market Intelligence

Modern valuers access unprecedented data resources:

Multiple Listing Service (MLS) data provides comprehensive sales, listing, and market time information for comparable analysis.

Public records offer deed transfers, mortgage recordings, and property tax assessments useful for verification and trend analysis.

Market analytics platforms aggregate and analyze data, providing inventory trends, price movements, and market velocity metrics.

Economic indicators including employment data, wage growth, and migration patterns help valuers understand demand drivers and long-term value trajectories.

The challenge lies not in data availability but in data interpretation. Valuers must filter signal from noise, identifying which metrics genuinely influence property values versus those that merely correlate with other causal factors.

Regulatory and Professional Standards in Valuation Practice

The 2026 market environment reinforces the importance of adhering to professional standards and regulatory requirements that ensure valuation quality and public trust.

RICS Valuation Standards (Red Book)

The Royal Institution of Chartered Surveyors (RICS) Red Book establishes mandatory standards for valuers operating in the UK and internationally. In 2026's recovering market, several Red Book principles gain particular relevance:

Market value definition. The Red Book defines market value as "the estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

This definition requires valuers to assess current market conditions rather than projecting future appreciation or assuming market recovery. In declining Southeast markets, this means accepting that market value may be below recent sales if current conditions have deteriorated.

Basis of value clarity. The Red Book requires valuers to clearly state the basis of value (market value, investment value, fair value, etc.) and explain any departures from market value. This transparency becomes critical when conducting specialized valuations like right to buy assessments or reinstatement cost valuations.

Assumptions and special assumptions. Valuers must clearly state any assumptions (matters assumed to be true) or special assumptions (assumptions that differ from actual facts) underlying their valuations. In 2026's uncertain market, clearly articulating assumptions about future market direction, planning permissions, or property conditions protects both valuers and clients.

Valuation Costs and Client Expectations

Understanding valuation costs and managing client expectations represents an often-overlooked aspect of professional practice. In 2026's complex market, clients increasingly question valuation fees, particularly when values disappoint their expectations.

Professional valuers must clearly communicate:

Scope of work. What the valuation includes (inspection extent, comparable analysis depth, report format) and excludes (structural engineering, environmental assessments, legal advice).

Basis of fees. Whether fees are fixed, hourly, or percentage-based, and what factors influence costs (property complexity, urgency, report requirements).

Value versus cost distinction. Clients must understand that valuation fees reflect professional expertise and liability, not the property value conclusion. A £500,000 property may require the same analytical rigor as a £250,000 property, justifying similar fees despite different values.

Practical Guidance for Property Stakeholders

Different stakeholders—buyers, sellers, investors, and lenders—face distinct challenges and opportunities in navigating Valuation Surveys in a Recovering Market: Navigating 2026 Price Stabilisation and Regional Variations.

For Property Buyers

Commission professional valuations early. Don't rely solely on mortgage valuations, which serve lenders' interests rather than buyers'. An independent RICS valuation provides unbiased assessment of whether asking prices align with market realities.

Understand regional dynamics. Research whether your target market is buyer-friendly, balanced, or seller-friendly. In buyer-friendly markets, negotiate confidently and don't rush decisions. In resilient Northern markets, recognize that competition may persist despite national moderation.

Consider condition carefully. In balanced markets, buyers have leverage to negotiate repairs or price reductions for property defects. Invest in comprehensive building surveys to identify issues before committing, particularly for older properties where specific defect reports may reveal costly problems.

Factor in total ownership costs. With mortgage rates stabilizing around 6.3%[1], financing costs are more predictable. However, also consider maintenance, insurance, and potential repair costs revealed through thorough property surveys.

For Property Sellers

Price realistically from the outset. Overpricing in 2026's balanced market leads to extended marketing periods and eventual price reductions that stigmatize properties. Commission professional valuations to establish defensible asking prices aligned with current market evidence.

Prepare properties thoroughly. With buyers having alternatives, presentation matters. Address obvious defects, enhance curb appeal, and consider pre-listing surveys to identify and remedy issues before they derail negotiations.

Understand your local market position. If selling in Southeast England's declining market, recognize that achieving 2024 or 2025 prices may be unrealistic. If selling in resilient Northern markets, leverage relative strength but avoid overestimating appreciation potential.

Be flexible on terms. In buyer-friendly markets, flexibility on closing dates, included furnishings, or repair credits can differentiate your property and facilitate sales without dramatic price reductions.

For Property Investors

Conduct thorough due diligence. Investment properties require rigorous analysis of income potential, expense projections, and exit strategies. Professional valuations should incorporate investment value assessments, not just market value conclusions.

Diversify geographically. Regional variations create both risks and opportunities. Diversifying across regions—balancing Southeast holdings with Northern properties, for example—hedges against localized market declines.

Monitor market metrics actively. Track inventory levels, absorption rates, and price trends in your investment markets. Early detection of market shifts allows proactive portfolio adjustments.

Consider value-add opportunities. In balanced markets, properties requiring renovation or repositioning may offer better returns than turnkey assets, as competition for distressed properties remains moderate.

For Mortgage Lenders

Enhance valuer instructions. Provide clear guidance on risk tolerance, required comparable recency, and adjustment expectations. In regionally varied markets, ensure valuers understand local conditions rather than applying national assumptions.

Monitor portfolio concentrations. Geographic concentration in declining markets like the Southeast creates portfolio risk. Diversification across regions with different market dynamics reduces exposure to localized downturns.

Adjust LTV policies regionally. Consider implementing region-specific LTV limits reflecting local market conditions. Higher LTVs may be appropriate in stable Northern markets, while conservative LTVs protect against further declines in pressured Southeast markets.

Invest in valuer relationships. Cultivating relationships with competent, local valuers who understand regional market nuances improves valuation quality and reduces risk of overvaluation.

Future Outlook: Beyond 2026

While this article focuses on Valuation Surveys in a Recovering Market: Navigating 2026 Price Stabilisation and Regional Variations, understanding longer-term trajectories helps stakeholders make informed decisions with multi-year implications.

Structural Market Changes

Several structural changes may persist beyond 2026:

Remote work normalization continues reshaping location preferences, potentially supporting secondary cities and suburban markets while pressuring central business districts and expensive urban cores.

Climate considerations increasingly influence property values as buyers and investors factor in flood risk, energy efficiency, and climate adaptation costs. Valuers must develop expertise in assessing these factors' value impacts.

Demographic shifts including aging populations and changing household formations affect property type demand, with potential long-term implications for single-family versus multifamily valuations.

Technology Evolution

Valuation technology will continue advancing:

AI and machine learning will enhance AVMs' accuracy and enable more sophisticated market analysis, though professional judgment will remain essential for complex or unique properties.

Blockchain and property records may streamline transaction processes and improve data transparency, benefiting valuers through better information access.

Virtual and augmented reality could enable remote property inspections and enhance valuation report presentations, though physical inspections will remain necessary for comprehensive assessments.

Regulatory Developments

Potential regulatory changes may affect valuation practice:

Enhanced disclosure requirements could mandate more detailed valuation reports, increasing preparation time and costs but improving transparency.

Sustainability reporting may become mandatory, requiring valuers to assess and report on properties' environmental performance and climate risks.

Standardization initiatives could harmonize valuation methodologies across regions or property types, improving consistency but potentially reducing flexibility to address unique circumstances.

Conclusion: Navigating Valuation Excellence in 2026's Recovering Market

The landscape of Valuation Surveys in a Recovering Market: Navigating 2026 Price Stabilisation and Regional Variations presents both challenges and opportunities for property professionals, buyers, sellers, and investors. National price stabilization at 2.2% growth[1], improving affordability with mortgage payments below 30% of income[1], and recovering transaction volumes to 4.13 million units[1] signal a market finding equilibrium after years of turbulence.

Yet this national narrative obscures critical regional variations—Southeast price pressures contrasting with Northern resilience, buyer-friendly markets expanding while others remain balanced, and inventory recovering but remaining 12% below historical norms[1]. These variations demand that valuers, lenders, and property stakeholders adopt location-specific, data-informed approaches rather than relying on national generalizations.

Professional valuation practice in 2026 requires:

✅ Enhanced comparable analysis with careful time adjustments and geographic precision

✅ Integration of market metrics including days on market, inventory levels, and absorption rates

✅ Regional market expertise recognizing that Southeast, Northern, and other markets follow distinct trajectories

✅ Technology adoption leveraging AVMs and data platforms while maintaining professional judgment

✅ Regulatory compliance adhering to RICS Red Book standards and clearly communicating assumptions

✅ Stakeholder communication managing expectations and explaining how market conditions influence values

Actionable Next Steps

For those navigating property transactions or valuations in 2026's recovering market:

-

Engage qualified professionals early. Whether buying, selling, or refinancing, commission chartered surveyors with local market expertise and RICS credentials to ensure accurate, defensible valuations.

-

Research your specific market. National trends provide context, but local conditions determine values. Investigate inventory levels, recent sales, and market velocity in your specific area.

-

Consider comprehensive surveys. Beyond basic valuations, invest in thorough property inspections to identify defects, assess condition, and inform negotiation strategies. Determine which survey you need based on property age, type, and your risk tolerance.

-

Maintain realistic expectations. In stabilizing markets with regional variations, not all properties appreciate equally. Base decisions on current market evidence rather than assumptions about future growth.

-

Monitor market evolution. The 2026 market will continue evolving. Stay informed about inventory trends, interest rate movements, and regional economic developments that influence property values.

The recovering market of 2026 rewards those who combine professional expertise, local knowledge, and data-informed analysis while maintaining realistic expectations about price trajectories and regional variations. By understanding these dynamics and engaging qualified professionals, property stakeholders can navigate this complex landscape successfully, making informed decisions that serve their financial interests and long-term objectives.

References

[1] 2026 National Housing Forecast – https://www.realtor.com/research/2026-national-housing-forecast/

[2] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

[3] Us Real Estate Market Outlook 2026 – https://www.cbre.com/insights/books/us-real-estate-market-outlook-2026

[7] Best Markets Home Buyers 2026 35971 – https://www.zillow.com/research/best-markets-home-buyers-2026-35971/