The rental housing market in Northern England is experiencing a dramatic transformation in 2026. Co-living developments are reshaping urban landscapes from Manchester to Newcastle, attracting first-time renters and young professionals seeking affordable, community-focused housing alternatives. As traditional rental markets struggle with affordability challenges, Valuation Surveys for Co-Living Spaces in Northern Cities: Capturing 2026 Rental Demand Surge have become essential tools for investors, developers, and financial institutions navigating this rapidly evolving sector.

With the global co-living market valued at $17.33 billion in 2026 and projected to reach $31.06 billion by 2035 [1], Northern cities are positioning themselves as prime locations for this housing revolution. The combination of lower property acquisition costs, strong rental demand from migrating young professionals, and established urban infrastructure creates compelling investment opportunities that require specialized valuation expertise.

Key Takeaways

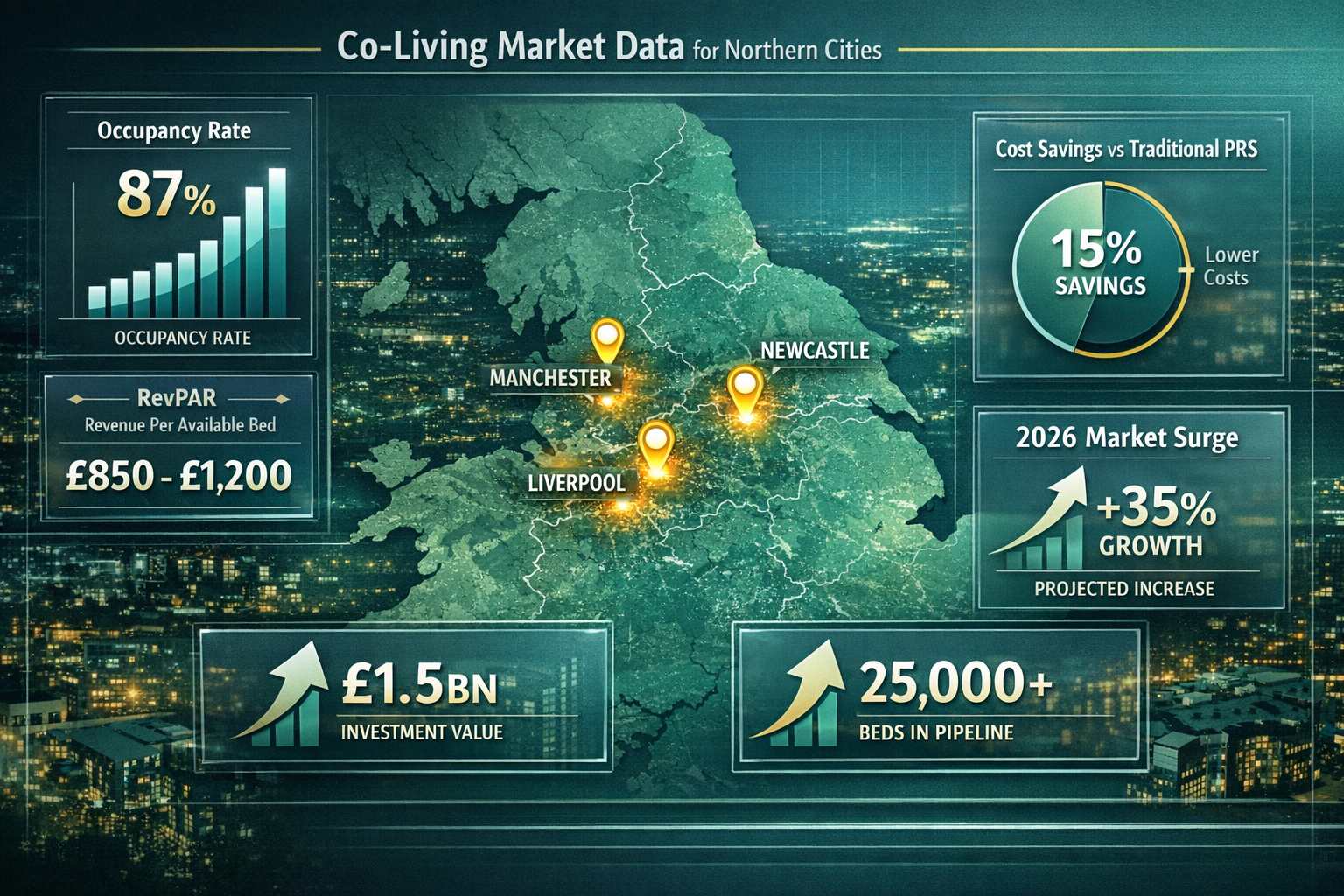

- Co-living properties achieve 87% average occupancy rates with Revenue Per Available Bed (RevPAB) ranging from £850-£1,200 monthly, demonstrating strong financial performance [6]

- Northern cities offer 15% cost savings compared to traditional Private Rented Sector (PRS) housing plus bills, driving tenant demand and investment interest [5]

- Specialized RICS valuation methodologies must account for shared amenity premiums, hybrid residential-commercial characteristics, and community-focused design elements

- North America holds 35% of global co-living market share at $5.25 billion, while the UK completed 2,500 new units in September 2024, representing 65% year-over-year growth [1]

- Professional valuation surveys incorporating comparable analysis, income capitalization, and development appraisal methods are critical for accurate co-living space assessment

Understanding the Co-Living Market Surge in Northern Cities

The 2026 Market Landscape

The co-living sector has experienced explosive growth across Northern England throughout 2026. Cities like Manchester, Leeds, Liverpool, Sheffield, and Newcastle have emerged as hotspots for co-living development, driven by several converging factors. Young professionals priced out of London and Southern housing markets are migrating northward, seeking affordable living arrangements without sacrificing quality or community connections.

Alternative market estimates place the 2026 global co-living market at $16.3 billion, with projections reaching $35 billion by 2030 [6]. This growth trajectory reflects fundamental shifts in housing preferences, particularly among millennials and Gen Z residents who prioritize flexibility, affordability, and social connectivity over traditional homeownership models.

The UK specifically completed 2,500 new co-living units in September 2024, bringing total operational units to 7,540 with nearly £1 billion invested in developments since 2020 [1]. Northern cities have captured a significant portion of this investment due to their combination of established universities, growing tech sectors, and comparatively affordable development costs.

Why Northern Cities Are Prime Co-Living Markets

Northern England offers unique advantages for co-living development that distinguish these markets from their Southern counterparts:

🏙️ Lower Development Costs: Property acquisition and construction expenses in Northern cities typically run 30-50% below London equivalents, improving development feasibility and investment returns.

👥 Strong Demographic Demand: Major universities in Manchester, Leeds, and Newcastle create steady pipelines of young professionals and postgraduate students seeking community-oriented housing.

🚆 Improved Connectivity: Enhanced rail links through Northern Powerhouse initiatives have strengthened economic connections between Northern cities, supporting professional mobility and rental demand.

💼 Growing Employment Sectors: Technology, digital services, and creative industries are expanding rapidly across Northern cities, attracting exactly the demographic cohorts most interested in co-living arrangements.

🏗️ Regeneration Opportunities: Former industrial areas provide abundant development sites suitable for conversion into modern co-living spaces with character and authenticity.

Defining Co-Living: More Than Shared Housing

Co-living spaces differ fundamentally from traditional house shares or student accommodation. Modern co-living developments feature:

- Private bedroom suites with ensuite bathrooms and individual climate control

- Professionally managed communal spaces including kitchens, lounges, and dining areas

- Premium amenities such as co-working spaces, fitness facilities, and rooftop terraces

- All-inclusive pricing covering utilities, internet, cleaning services, and maintenance

- Community programming with social events, networking opportunities, and skill-sharing workshops

- Flexible lease terms ranging from one month to 12+ months

This hybrid model combines the privacy of traditional apartments with the social benefits and cost efficiencies of shared living, creating a distinct property category that requires specialized valuation approaches.

Valuation Surveys for Co-Living Spaces in Northern Cities: Specialized Assessment Methodologies

RICS Red Book Valuation Standards for Co-Living Properties

Professional valuation surveys for co-living developments must adhere to Royal Institution of Chartered Surveyors (RICS) Red Book standards, which provide the authoritative framework for property valuation in the UK. However, co-living spaces present unique challenges that require adapted methodologies beyond traditional residential valuation approaches.

RICS Red Book valuations for co-living properties must consider:

Hybrid Property Classification: Co-living developments straddle residential and commercial property categories, incorporating elements of both student accommodation and build-to-rent (BTR) developments. Valuers must determine appropriate classification based on operational structure, lease arrangements, and management intensity.

Income Approach Primacy: Unlike traditional residential properties valued primarily through comparable sales, co-living spaces are typically assessed using income capitalization methods that analyze rental income streams, operating expenses, and appropriate yield rates.

Shared Amenity Valuation: Communal facilities represent significant capital investment but generate value indirectly through enhanced rental rates and occupancy performance rather than direct revenue. Valuers must quantify these premiums through market analysis and comparable property performance.

Operational Considerations: Management intensity, service provision costs, and community programming expenses significantly impact net operating income and must be accurately reflected in valuation models.

The Three-Pillar Valuation Approach

Professional chartered surveyors typically employ a three-pillar methodology when conducting Valuation Surveys for Co-Living Spaces in Northern Cities: Capturing 2026 Rental Demand Surge:

1. Comparable Method Analysis

This approach examines recent transactions of similar co-living properties within the target market and comparable Northern cities. Key metrics include:

- Price per bed for completed sales

- Revenue Per Available Bed (RevPAB) ranging from £850-£1,200 monthly [6]

- Occupancy rates averaging 87% for stabilized properties [6]

- Amenity premiums for properties with superior communal facilities

- Location adjustments for proximity to transport, employment centers, and universities

The comparable method provides market-based validation but requires sufficient transaction data, which can be limited in emerging co-living markets across Northern cities.

2. Income Capitalization Approach

This methodology calculates property value based on projected income streams:

Gross Rental Income = (Number of Beds × RevPAB × Occupancy Rate × 12 months)

Net Operating Income (NOI) = Gross Rental Income – Operating Expenses

Property Value = NOI ÷ Capitalization Rate

Operating expenses for co-living properties typically include:

- Property management fees (10-15% of gross income)

- Utilities and internet provision

- Cleaning and maintenance services

- Community programming costs

- Insurance and property taxes

- Reserve funds for capital improvements

Capitalization rates for co-living properties in Northern cities currently range from 5.5% to 7.5%, depending on property quality, location, and operational track record [3].

3. Development Appraisal Method

For new or proposed co-living developments, valuers employ residual valuation techniques:

Development Value = Completed Property Value – (Development Costs + Developer's Profit + Finance Costs)

This approach requires detailed analysis of:

- Construction costs specific to co-living design requirements

- Planning and professional fees

- Marketing and lease-up costs

- Development timeline and associated finance costs

- Appropriate developer's profit margin (typically 15-20% for co-living projects)

Unique Valuation Factors for Northern Co-Living Properties

Several factors distinguish Valuation Surveys for Co-Living Spaces in Northern Cities: Capturing 2026 Rental Demand Surge from standard residential assessments:

Affordability Premium: Co-living apartments deliver approximately 15% savings compared to PRS plus bills [5], with average co-living costs calculated at £336 for one-bedroom units. This affordability advantage drives demand but must be balanced against operational cost requirements in valuation models.

Rapid Lease-Up Performance: Living by Scape in Guildford achieved full occupancy in just 7 weeks with 113 beds fully let and average tenancy lengths of 11 months [5]. Similar performance metrics in Northern cities demonstrate strong market demand that supports premium valuations.

Community Value Quantification: The social and networking aspects of co-living create intangible value that manifests through extended tenancy lengths, reduced vacancy periods, and tenant willingness to pay premiums. Valuers must translate these qualitative benefits into quantitative adjustments.

Flexible Use Potential: Many co-living developments can adapt to changing market conditions, potentially converting to traditional BTR, student accommodation, or even hotel use. This flexibility provides downside protection that may justify yield compression.

Market Data and Performance Metrics Driving Valuation Surveys for Co-Living Spaces in Northern Cities

2026 Occupancy and Revenue Performance

Stabilized co-living properties across Northern cities are demonstrating exceptional operational performance in 2026. Average occupancy rates of 87% [6] significantly exceed traditional rental housing benchmarks, reflecting strong tenant demand and effective property management.

Revenue Per Available Bed (RevPAB) metrics provide critical valuation inputs:

| Market Tier | Monthly RevPAB | Annual Revenue per Bed |

|---|---|---|

| Premium (City Centers) | £1,100-£1,200 | £13,200-£14,400 |

| Standard (Urban Core) | £950-£1,100 | £11,400-£13,200 |

| Value (Peripheral Areas) | £850-£950 | £10,200-£11,400 |

These figures demonstrate the strong revenue-generating capacity of co-living developments, particularly when compared to traditional rental properties on a per-square-foot basis. Co-living units typically range from 150-250 square feet for private bedrooms, achieving revenue densities that often exceed conventional studio apartments.

Regional Market Variations Across Northern Cities

While Northern England presents unified advantages for co-living development, individual city markets exhibit distinct characteristics that impact valuation approaches:

Manchester: As the largest Northern market, Manchester leads in co-living supply with multiple established operators. Competition drives quality standards higher while maintaining strong occupancy. Typical RevPAB ranges £1,000-£1,200 in central locations.

Leeds: Strong financial services and professional services sectors create ideal tenant demographics. The city's compact city center supports walkability, a key co-living amenity. RevPAB typically ranges £900-£1,100.

Liverpool: Lower development costs and growing cultural appeal attract value-focused co-living operators. University populations provide stable demand. RevPAB ranges £850-£1,000.

Newcastle: Strong student populations from multiple universities create natural co-living demand. Regeneration initiatives in city center areas provide development opportunities. RevPAB ranges £850-£1,050.

Sheffield: Emerging market with limited existing supply but strong university presence. Development opportunities remain abundant. RevPAB ranges £800-£950.

Professional valuation reports must incorporate these regional variations when assessing co-living properties across Northern cities.

Investment Yield Analysis and Market Comparisons

The Newmark Valuation & Advisory 2026 North American Market Survey indicates that commercial real estate markets entered 2026 with greater pricing clarity and improved capital market functionality [3]. Similar trends are evident in UK co-living markets, where increased transaction activity provides better valuation benchmarks.

Co-living properties in Northern cities currently trade at yields that reflect their hybrid residential-commercial nature:

- Core stabilized assets: 5.5-6.5% net initial yields

- Value-add opportunities: 6.5-7.5% net initial yields

- Development projects: 7.5%+ targeted development yields

These yields compare favorably to alternative investment opportunities:

- Traditional BTR developments: 4.5-5.5% yields

- Student accommodation: 5.0-6.0% yields

- Commercial offices: 6.0-8.0% yields (depending on quality and location)

The yield premium for co-living reflects both higher operational intensity and the sector's relative newness, which creates perceived risk among some investors. As the asset class matures and performance track records lengthen, yield compression is anticipated.

Demographic Drivers and Tenant Demand Analysis

Understanding tenant demographics is essential for accurate valuation surveys. Primary co-living tenant segments in Northern cities include:

🎓 Young Professionals (25-35 years): 45-50% of tenant base

- Relocated for career opportunities

- Seek networking and social connections

- Value convenience and all-inclusive pricing

- Average tenancy: 8-12 months

👨💼 Early Career Professionals (22-25 years): 25-30% of tenant base

- First jobs after university graduation

- Price-sensitive but quality-conscious

- Appreciate community programming

- Average tenancy: 6-9 months

🌍 International Professionals: 15-20% of tenant base

- Temporary work assignments or relocations

- Require fully furnished, move-in-ready accommodation

- Value flexibility and community support

- Average tenancy: 3-6 months

📚 Postgraduate Students: 10-15% of tenant base

- Older than traditional student accommodation residents

- Seek quiet study environments with social opportunities

- Budget-conscious with stable income sources

- Average tenancy: 9-12 months

This demographic diversity provides operational stability and reduces vacancy risk, factors that professional valuers must incorporate into income projections and risk assessments.

Strategic Considerations for Investors and Developers

Site Selection and Development Feasibility

Successful co-living developments in Northern cities share common location characteristics that significantly impact valuation outcomes:

Transport Connectivity: Properties within 10-minute walks of major transport hubs command 15-20% rental premiums and achieve faster lease-up periods.

Employment Proximity: Locations near business districts, tech hubs, or major employers reduce commute times, a primary tenant priority.

Retail and Leisure Access: Walkable neighborhoods with cafes, restaurants, and entertainment options enhance lifestyle appeal.

Safety and Neighborhood Quality: Well-maintained areas with low crime rates support premium positioning and tenant retention.

Development Site Characteristics: Former office buildings, hotels, or industrial structures often provide cost-effective conversion opportunities compared to ground-up construction.

When conducting building surveys for potential co-living conversions, structural suitability, services capacity, and planning permission viability must be thoroughly assessed.

Planning and Regulatory Considerations

Co-living developments face unique planning challenges that impact development feasibility and timeline:

Use Class Classification: Co-living may fall under C3 (residential), C4 (HMO), or sui generis classifications depending on design and operation, affecting planning requirements.

Space Standards: Some local authorities apply minimum room size standards that may exceed typical co-living bedroom dimensions (150-250 sq ft).

Affordable Housing Requirements: Section 106 obligations may apply, though their application to co-living remains inconsistent across Northern local authorities.

Parking Requirements: Many co-living developments successfully argue for reduced parking provision given target demographics and urban locations.

HMO Licensing: Properties with specific occupancy structures may require Houses in Multiple Occupation licenses, adding regulatory complexity.

Professional valuers must account for planning risk and timeline implications when assessing development projects. Properties with secured planning permission command significant premiums over those requiring applications.

Financing and Investment Structures

The financing landscape for co-living developments has matured significantly, though challenges remain:

Senior Debt Availability: Mainstream lenders increasingly provide development and term financing for co-living projects, typically at 55-65% loan-to-value ratios for experienced developers.

Specialist Lenders: Alternative lenders and debt funds offer higher leverage (65-75% LTV) at premium pricing for developers with strong track records.

Equity Requirements: Development projects typically require 35-45% equity contributions, with investors seeking 15-20% IRR targets.

Forward Funding: Some institutional investors provide forward funding structures, acquiring properties upon completion at predetermined yields.

REIT and Fund Structures: Co-living assets are increasingly held within Real Estate Investment Trusts and specialist funds, providing liquidity and scale advantages.

Commercial property valuations for financing purposes must meet lender requirements and incorporate appropriate risk adjustments for development stage, operator experience, and market positioning.

Operational Excellence and Value Enhancement

Co-living properties require professional management that significantly exceeds traditional landlord responsibilities:

Community Management: Dedicated community managers organize events, facilitate connections, and maintain positive living environments.

Maintenance Responsiveness: Rapid response to maintenance issues maintains tenant satisfaction and supports premium pricing.

Technology Integration: Digital platforms for booking, payments, service requests, and community engagement enhance operational efficiency.

Flexible Service Packages: Tiered service offerings allow tenants to customize experiences while optimizing revenue per bed.

Tenant Retention Programs: Loyalty incentives, renewal discounts, and referral bonuses reduce turnover costs and vacancy periods.

Properties demonstrating operational excellence through high tenant satisfaction scores, extended tenancy lengths, and strong renewal rates justify premium valuations through reduced risk profiles and enhanced income stability.

Risk Factors and Mitigation Strategies

Professional Valuation Surveys for Co-Living Spaces in Northern Cities: Capturing 2026 Rental Demand Surge must address sector-specific risks:

⚠️ Market Saturation Risk: Rapid supply growth could exceed demand in specific Northern markets. Valuers should assess development pipelines and absorption rates.

⚠️ Economic Sensitivity: Co-living tenants typically represent early-career demographics vulnerable to economic downturns. Stress testing income projections against recession scenarios is prudent.

⚠️ Operational Complexity: Higher management intensity creates execution risk. Operator experience and track record significantly impact value.

⚠️ Regulatory Evolution: Planning policies and licensing requirements may tighten, affecting development feasibility and existing property operations.

⚠️ Exit Liquidity: Co-living remains a relatively niche asset class with limited buyer pools compared to traditional residential investments.

Mitigation strategies include:

- Conservative underwriting assumptions (80-85% stabilized occupancy vs. 87% market average)

- Flexible design allowing alternative uses if market conditions deteriorate

- Partnership with experienced operators with proven track records

- Diversification across multiple Northern city markets

- Maintaining strong unit economics that provide cushion against revenue pressures

Future Outlook: Co-Living Market Trajectory Through 2030

Growth Projections and Market Evolution

The co-living sector's growth trajectory remains robust through the remainder of the decade. With the global market projected to reach $31.06 billion by 2035 at a 7.5% CAGR [1], Northern cities are positioned to capture significant portions of this expansion.

Several trends will shape market evolution:

🏗️ Institutionalization: Increased participation by institutional investors will drive professionalization, standardization, and scale economies.

🌐 Brand Consolidation: Leading operators will expand across multiple Northern cities, creating recognized brands that command premium valuations.

🔧 Product Innovation: Second and third-generation co-living developments will incorporate lessons learned, optimizing layouts, amenities, and service offerings.

📊 Data-Driven Operations: Advanced analytics will enable dynamic pricing, targeted marketing, and optimized community programming.

🤝 Partnership Models: Collaborations between developers, operators, and institutional investors will create efficient development and operational structures.

Implications for Valuation Methodologies

As the co-living sector matures, valuation approaches will continue evolving:

Enhanced Comparable Data: Growing transaction volumes will provide robust comparable evidence, reducing reliance on income-based methodologies.

Standardized Metrics: Industry-wide adoption of consistent performance metrics (RevPAB, occupancy, operating expense ratios) will improve valuation accuracy.

Risk Adjustment Refinement: Extended performance track records will enable more precise risk assessment and appropriate yield determination.

ESG Integration: Environmental, social, and governance factors will increasingly influence valuations as investors prioritize sustainability and social impact.

Technology Valuation: Digital platforms, data assets, and technology infrastructure will become explicit valuation components rather than implicit operational factors.

Professional valuers specializing in co-living properties must stay current with these evolving methodologies to provide accurate, defensible valuations that meet RICS standards.

Sustainability and Social Impact Considerations

Co-living developments align with broader sustainability objectives that increasingly influence property valuations:

Resource Efficiency: Shared amenities reduce per-capita resource consumption compared to traditional housing.

Urban Density: Co-living supports higher-density development that reduces urban sprawl and transportation emissions.

Community Building: Social connectivity and community programming address isolation challenges in modern urban living.

Affordable Housing: Cost savings versus traditional rentals improve housing accessibility for young professionals.

Adaptive Reuse: Conversion of underutilized buildings reduces embodied carbon compared to new construction.

These sustainability attributes create positive externalities that may justify valuation premiums as ESG considerations become increasingly central to investment decision-making.

Conclusion

Valuation Surveys for Co-Living Spaces in Northern Cities: Capturing 2026 Rental Demand Surge represent a specialized discipline requiring expertise in residential valuation, commercial property analysis, and operational assessment. As co-living developments continue transforming Northern England's rental landscape, accurate valuation becomes increasingly critical for investors, developers, lenders, and operators navigating this dynamic sector.

The compelling fundamentals driving co-living growth—87% occupancy rates, £850-£1,200 monthly RevPAB, and 15% cost savings versus traditional rentals—demonstrate the sector's strong value proposition for both tenants and investors. Northern cities' combination of affordable development costs, strong demographic demand, and improving connectivity positions these markets for continued expansion through the remainder of the decade.

Professional valuers must employ sophisticated methodologies that account for co-living's unique characteristics: hybrid property classification, shared amenity premiums, operational intensity, and community value creation. The three-pillar approach combining comparable analysis, income capitalization, and development appraisal provides comprehensive valuation frameworks when executed by experienced chartered surveyors familiar with co-living sector dynamics.

Actionable Next Steps

For investors and developers considering co-living opportunities in Northern cities:

- Engage RICS-qualified valuers with specific co-living experience to conduct comprehensive property assessments

- Conduct thorough market analysis of target Northern cities, examining demographic trends, competitive supply, and absorption rates

- Develop detailed financial models incorporating conservative occupancy assumptions, realistic operating expenses, and appropriate yield expectations

- Secure experienced operators with proven track records managing co-living properties successfully

- Prioritize locations with strong transport connectivity, employment proximity, and lifestyle amenities

- Obtain professional surveys including building surveys and structural assessments for conversion opportunities

- Navigate planning processes proactively, engaging local authorities early to address regulatory requirements

For lenders and financial institutions:

- Develop co-living underwriting expertise recognizing sector-specific characteristics and risk factors

- Require comprehensive valuations from qualified professionals with co-living sector knowledge

- Monitor portfolio performance through standardized metrics enabling comparative analysis

- Consider forward funding structures for experienced developers with strong business plans

The co-living sector's continued maturation presents significant opportunities for stakeholders who approach investments with appropriate due diligence, professional expertise, and realistic expectations. As Northern cities capture growing portions of the UK's £1 billion co-living investment pipeline, accurate valuation surveys will remain essential tools for informed decision-making and successful project execution.

The rental demand surge of 2026 is not a temporary phenomenon but rather reflects fundamental shifts in housing preferences, affordability challenges, and lifestyle priorities among younger demographics. Co-living spaces that deliver genuine community value, operational excellence, and cost advantages will continue thriving, rewarding investors and developers who recognize this sector's transformative potential.

References

[1] Co Living Market 117296 – https://www.businessresearchinsights.com/market-reports/co-living-market-117296

[3] 2026 Valuation Advisory North American Market Survey – https://www.nmrk.com/insights/market-report/2026-valuation-advisory-north-american-market-survey

[5] Co Living In An Ever Changing Market Where Do The Hurdles And Opportunities Lie For The Sector – https://www.cushmanwakefield.com/en/united-kingdom/insights/co-living-in-an-ever-changing-market-where-do-the-hurdles-and-opportunities-lie-for-the-sector

[6] Coliving Statistics – https://everythingcoliving.com/coliving-statistics