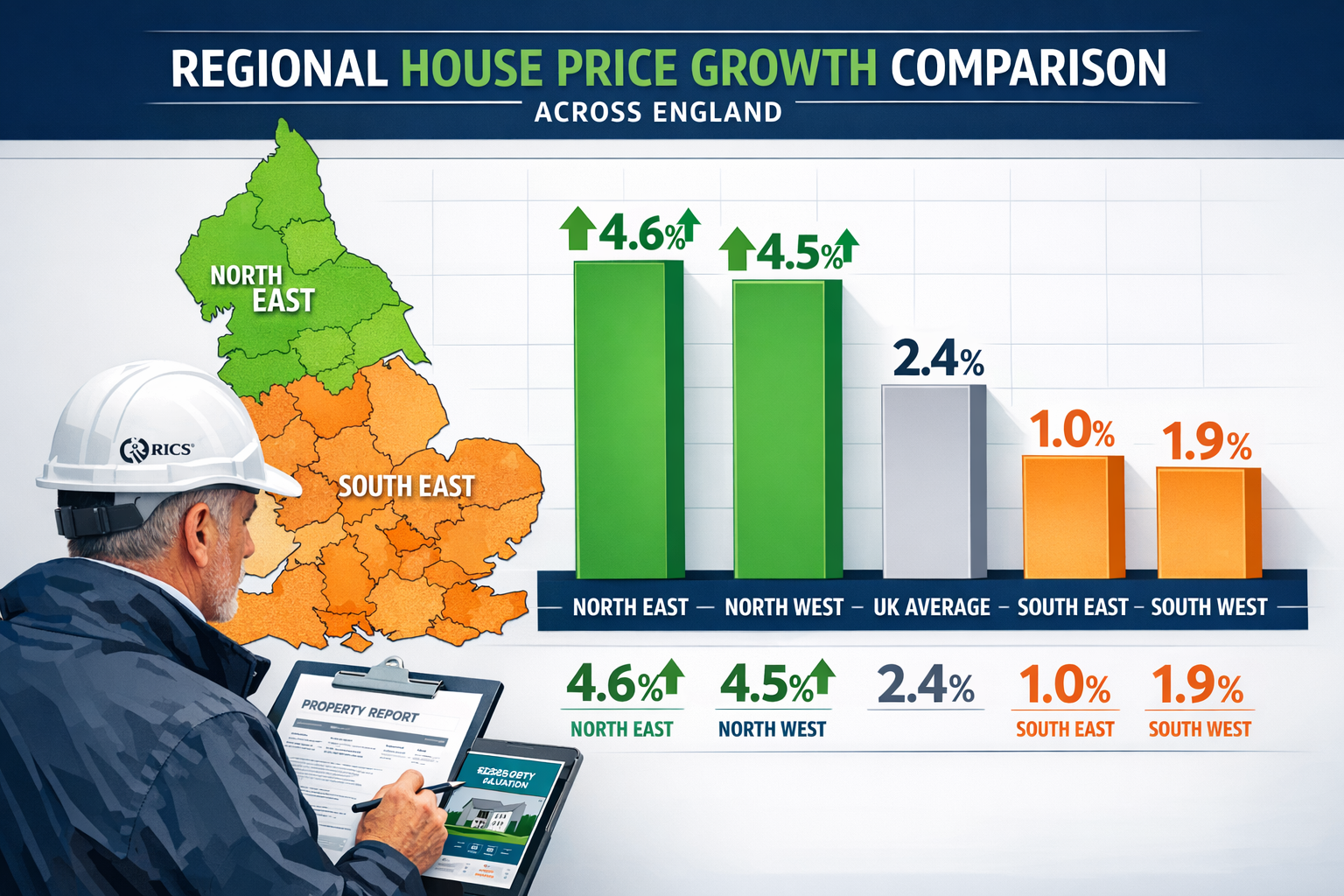

The property market landscape across England has shifted dramatically in 2026, with Northern regions experiencing unprecedented growth while Southern markets struggle to maintain momentum. The North East has achieved 4.6% annual house price inflation, while the North West follows closely with 4.5% growth—both significantly outpacing the UK average of 2.4%.[1][2] Meanwhile, the South East languishes at just 1.0% annual growth, and London's rental market shows the weakest performance in England at 1.1% annually.[1]

Understanding Valuation Strategies for Northern England's 5-7% Price Surge: Outpacing Southern Market Slumps in 2026 has become essential for property professionals, investors, and homeowners navigating this regional divergence. Chartered surveyors must now employ sophisticated tactics to accurately assess properties in these high-growth Northern markets, where traditional valuation methods may no longer capture the full picture of rapidly changing market dynamics.

This comprehensive guide explores the professional surveyor tactics, RICS-compliant methodologies, and data-driven approaches necessary to navigate the complex valuation landscape emerging across England's divided property market.

Key Takeaways

✅ Northern regions dominate growth: The North East (4.6%) and North West (4.5%) lead England in house price appreciation, nearly doubling the national average of 2.4%.[1][2]

✅ Southern markets underperform: The South East records only 1.0% growth with monthly declines, while London experiences the weakest rental inflation at just 1.1% annually.[1]

✅ RICS valuation methods require regional adaptation: Surveyors must adjust comparable analysis, affordability assessments, and market trend projections to account for significant regional divergences.

✅ Affordability drives Northern demand: Lower property prices in Northern England, combined with returning buyer confidence and anticipated interest rate cuts, fuel sustained growth momentum.[2]

✅ Professional valuation expertise is critical: Accurate property assessments in high-growth Northern markets require specialized knowledge of factors of valuation and regional market dynamics.

Understanding the Regional Divide: Northern Growth vs Southern Stagnation

The Numbers Behind Northern England's Remarkable Performance

The North East has emerged as England's strongest performing region, achieving 4.6% annual house price inflation to December 2025—nearly double the UK average.[1] Some monthly comparison data suggests even more dramatic growth, with figures reaching 6.8%, indicating volatile but consistently strong performance.[5]

The North West maintains equally impressive momentum with 4.5% annual growth and 0.9% monthly increases in recent periods.[2][5] This sustained performance reflects what Peter Graham, head of real estate and construction for the North at RSM UK, describes as "remarkable resilience" driven by strong affordability compared to southern regions and returning buyer confidence for 2026.[2]

| Region | Annual Growth (%) | Monthly Change (%) | Average Price |

|---|---|---|---|

| North East | 4.6% | +0.9% | £185,000 |

| North West | 4.5% | +0.9% | £238,000 |

| UK Average | 2.4% | -0.7% | £270,000 |

| South East | 1.0% | -0.8% | £385,000 |

| South West | 1.9% | -0.4% | £325,000 |

Southern England's Market Challenges

In stark contrast, Southern regions struggle to maintain growth momentum. The South East recorded only 1.0% annual growth with a -0.8% monthly decline, while the South West showed marginally better performance at 1.9% annual growth but still experienced monthly declines.[5]

London faces particular challenges, with private rent inflation at just 1.1% annually—the lowest rate in England—indicating significantly weakened demand in the capital.[1] This represents a dramatic reversal from historical patterns where London and the South East typically led national property price appreciation.

"Slowing annual growth of house prices signals ongoing affordability pressures and cautious buyer sentiment, though modest price adjustments may benefit some purchasers." — Nathan Emerson, Chief Executive of Propertymark[6]

The Rental Market Tells the Same Story

The rental market mirrors these regional divergences. The North East leads England with 8.0% annual private rent inflation to January 2026, reflecting strong demand pressures in the region.[1] Meanwhile, London's 1.1% rental growth represents the weakest performance nationally, suggesting fundamental shifts in housing demand patterns.

Even Wales outperforms with 5.8% annual private rent growth to January 2026, reaching an average monthly rent of £826.[1] This sustained growth across Northern England and Wales contrasts sharply with Southern stagnation, creating unprecedented challenges for property valuers attempting to apply consistent methodologies across regions.

RICS-Compliant Valuation Strategies for Northern England's 5-7% Price Surge: Outpacing Southern Market Slumps in 2026

Adapting Comparable Sales Analysis for High-Growth Markets

Traditional comparable sales analysis—the cornerstone of property valuation—requires significant adaptation in Northern England's rapidly appreciating markets. RICS Red Book standards mandate that valuers use recent comparable transactions, but in markets experiencing 5-7% annual growth, even sales from six months ago may undervalue current market conditions.

Professional surveyors must:

📊 Adjust time-based comparables: Apply monthly appreciation rates to older comparables, using the documented 0.9% monthly growth in the North West and similar figures for the North East.[2][5]

📊 Weight recent transactions heavily: Prioritize comparables from the most recent 3-month period, as older sales may not reflect current market momentum.

📊 Consider asking price trends: Rightmove data showing the largest January increase in asking prices in more than two decades signals renewed market momentum that completed sales data may not yet capture.[2]

📊 Account for seasonal variations: January 2026 data suggests stronger-than-typical winter market activity, requiring adjustments to seasonal comparison models.

Understanding factors of valuation becomes particularly crucial when standard comparable analysis may lag behind rapid market changes. Chartered surveyors must incorporate forward-looking indicators alongside historical transaction data.

Incorporating Affordability Metrics into Valuation Models

The affordability advantage driving Northern England's growth must be quantified within professional valuations. Properties in the North West average £238,000 compared to £385,000 in the South East—a difference of £147,000 that fundamentally alters buyer demand dynamics.[1]

Key affordability considerations include:

💰 Income-to-price ratios: Northern regions maintain healthier ratios (typically 4-5x average earnings) compared to Southern regions (often 8-10x or higher).

💰 First-time buyer accessibility: Lower absolute prices enable deposit accumulation and mortgage qualification for demographics priced out of Southern markets.

💰 Rental yield comparisons: Higher rental yields in Northern markets (often 5-7%) versus Southern markets (typically 3-4%) attract investor demand.

💰 Mortgage affordability stress tests: Properties priced at £238,000 (North West average) versus £385,000 (South East average) pass affordability tests for significantly broader buyer pools.

When conducting RICS Help to Buy valuations, surveyors must recognize that government-backed schemes have disproportionate impact in affordable Northern markets, potentially driving additional demand pressure beyond historical norms.

Regional Market Trend Analysis and Forecasting

Valuation Strategies for Northern England's 5-7% Price Surge: Outpacing Southern Market Slumps in 2026 require sophisticated market trend analysis that recognizes persistent regional divergence. Paula Higgins, CEO of HomeOwners Alliance, forecasts UK house prices will rise approximately 2% in 2026, with the current north-south divide expected to persist and potentially widen.[5]

Professional trend analysis must incorporate:

📈 Interest rate impact modeling: Bank of England rate cuts expected throughout 2026, with UK inflation dropping to 3% in January 2026, will disproportionately benefit Northern markets where affordability is already stronger.[2][5]

📈 Regional employment trends: Economic development in Northern cities, particularly Manchester, Liverpool, and Newcastle, supports sustained housing demand.

📈 Infrastructure investment: Transport improvements and regeneration projects in Northern England create localized appreciation hotspots requiring granular market knowledge.

📈 Migration patterns: Net migration from Southern to Northern regions, driven by remote work flexibility and cost-of-living considerations, supports demand fundamentals.

Chartered surveyors conducting structural surveys in Northern England must recognize that property condition assessments directly impact valuation in competitive markets where buyers have multiple options.

Specialized Valuation Approaches for Different Property Types

Different property types within Northern England's high-growth markets require tailored valuation approaches:

Victorian and Edwardian Terraced Housing

These properties dominate Northern England's housing stock and represent the primary growth segment. Valuation considerations include:

- Renovation potential: Many Northern terraced properties offer significant value-add opportunities through modernization

- Period features: Original architectural details command premiums in gentrifying areas

- Energy efficiency: Properties with modern insulation and heating systems achieve higher valuations

- Street-by-street variation: Values can vary significantly within short distances based on regeneration status

Modern New-Build Developments

New construction in Northern cities attracts first-time buyers and investors. Key valuation factors:

- Developer reputation: Established builders command price premiums

- Help to Buy eligibility: Properties qualifying for government schemes achieve higher demand

- Service charges and management: Ongoing costs significantly impact investment valuations

- Completion timelines: Off-plan valuations must account for market movement during construction

Commercial-to-Residential Conversions

Urban regeneration drives conversions in Manchester, Liverpool, and Leeds. Valuation complexities include:

- Planning restrictions: Permitted development rights versus full planning permission affect future value

- Build quality variations: Conversion standards vary significantly between developers

- Management company structures: Ongoing governance impacts long-term value retention

When performing commercial property surveying, professionals must recognize how commercial-to-residential conversion trends affect both commercial and residential market dynamics.

Technology-Enhanced Valuation Methodologies

Modern valuation in high-growth Northern markets increasingly incorporates technology-driven approaches:

🖥️ Automated Valuation Models (AVMs): While useful for initial assessments, AVMs often lag in rapidly appreciating markets and require professional override adjustments.

🖥️ Geographic Information Systems (GIS): Mapping tools identify micro-market variations within broader regional trends, particularly valuable in urban regeneration areas.

🖥️ Big data analytics: Transaction databases, rental listings, and economic indicators provide real-time market intelligence beyond traditional comparable sales.

🖥️ Digital property inspection tools: Laser measuring devices, thermal imaging, and drone photography enhance inspection accuracy and documentation.

However, technology complements rather than replaces professional judgment. RICS-qualified surveyors must interpret technological outputs within the context of local market knowledge, property-specific factors, and professional standards.

Practical Implementation: Conducting Accurate Valuations in Northern England's Dynamic Market

Pre-Valuation Research and Market Intelligence Gathering

Successful Valuation Strategies for Northern England's 5-7% Price Surge: Outpacing Southern Market Slumps in 2026 begin with comprehensive pre-valuation research:

Step 1: Regional Market Analysis

- Review ONS house price indices for specific Northern regions

- Analyze Land Registry transaction data for the relevant postcode sector

- Examine rental market trends and yields

- Assess local economic indicators (employment, wages, development)

Step 2: Micro-Market Assessment

- Identify street-level price variations within the broader area

- Research recent planning applications and approvals

- Evaluate infrastructure projects affecting accessibility and desirability

- Assess school catchment areas and local amenities

Step 3: Property-Specific Investigation

- Obtain EPC certificates and building regulations compliance documentation

- Review any previous survey reports or valuation documents

- Investigate property history (extensions, renovations, planning issues)

- Identify any lease complications or lease extension valuation requirements

Step 4: Comparable Transaction Research

- Compile minimum 6-8 comparable sales from the past 3-6 months

- Adjust for time differences using documented monthly appreciation rates

- Identify and document key differences (size, condition, location specifics)

- Consider both completed sales and current asking prices for market direction

On-Site Inspection Protocols for High-Growth Markets

Physical property inspection remains fundamental to accurate valuation, regardless of market conditions. In Northern England's appreciating markets, inspection thoroughness directly impacts valuation accuracy:

External Inspection Focus Areas:

🏠 Structural condition: Victorian and Edwardian properties require particular attention to foundations, damp-proofing, and roof condition

🏠 External improvements: Recent renovations (windows, doors, rendering, roofing) add significant value in competitive markets

🏠 Boundary definitions: Clear property boundaries and any encroachments affect valuations

🏠 Parking and access: Off-street parking commands substantial premiums in urban Northern markets

Internal Inspection Priorities:

🏠 Modernization extent: Kitchen and bathroom quality significantly impact valuations in competitive buyer markets

🏠 Space configuration: Open-plan living arrangements and bedroom counts affect buyer appeal

🏠 Energy efficiency: Modern heating systems, insulation, and double glazing increasingly influence valuations

🏠 Condition versus potential: Distinguish between properties requiring cosmetic updates versus structural work

Surveyors should consider recommending damp surveys when moisture issues are suspected, as these significantly impact both valuation and buyer willingness to proceed.

Adjusting Valuations for Market Momentum and Buyer Sentiment

In rapidly appreciating markets, buyer sentiment and market momentum become valuation factors requiring professional judgment:

Positive Momentum Indicators:

- Multiple offers on comparable properties

- Properties selling above asking prices

- Reduced time on market (days to sale under offer)

- High viewing-to-offer conversion rates

- Strong attendance at open houses and viewings

Negative Sentiment Signals:

- Increasing inventory levels

- Price reductions on comparable listings

- Extended marketing periods

- Vendor concessions (including fixtures, legal fees)

- Seasonal slowdowns exceeding historical norms

The January 2026 asking price surge—the largest January increase in more than two decades—suggests strong positive momentum entering 2026.[2] Professional valuers must determine whether this represents sustainable demand or temporary optimism requiring cautious interpretation.

Documentation and Reporting Standards

RICS Red Book compliance requires comprehensive documentation supporting valuation conclusions. In high-growth Northern markets, enhanced documentation protects both valuer and client:

Essential Documentation Components:

📋 Market context section: Detailed analysis of regional trends, including specific reference to North East and North West growth rates versus national averages

📋 Comparable evidence: Minimum six comparables with detailed adjustment explanations, including time-based appreciation calculations

📋 Assumptions and limitations: Clear statement of valuation basis, inspection limitations, and market condition assumptions

📋 Supporting data: Photographs, floor plans, EPC certificates, and any specialist reports informing the valuation

📋 Market outlook commentary: Professional assessment of likely short-term market direction based on current indicators

When conducting Help to Buy valuations, additional documentation requirements apply, including specific confirmation of scheme eligibility and purchase price reasonableness.

Quality Assurance and Peer Review Processes

Given the significant regional divergence between Northern and Southern markets, internal quality assurance becomes particularly important:

Recommended QA Processes:

✓ Peer review of comparables: Second surveyor verification of comparable selection and adjustments

✓ Regional expertise consultation: Input from surveyors with specific Northern England market knowledge

✓ Trend analysis comparison: Valuation results compared against documented regional appreciation rates

✓ Client expectation management: Clear communication about market conditions and valuation basis

✓ Post-completion monitoring: Tracking actual sale prices versus valuations to refine future assessments

Professional indemnity insurance considerations also require enhanced diligence in rapidly changing markets, where valuation accuracy directly impacts lender security and buyer financial exposure.

Strategic Considerations for Different Stakeholder Groups

Valuation Strategies for Mortgage Lenders

Mortgage lenders face particular challenges in Northern England's high-growth markets, where rapid appreciation affects loan-to-value ratios and security assessments:

Lender-Specific Valuation Priorities:

🏦 Conservative growth assumptions: While markets show 5-7% growth, lenders typically require valuations based on sustainable long-term trends rather than short-term momentum

🏦 Downside risk assessment: Consideration of potential market corrections and regional economic vulnerabilities

🏦 Property liquidity evaluation: Assessment of likely sale timeline and buyer pool depth in event of repossession

🏦 Comparable weighting: Preference for completed sales over asking prices to avoid over-valuation based on optimistic listings

Understanding whether a mortgage valuation is the same as a survey helps both lenders and borrowers set appropriate expectations for valuation scope and purpose.

Interest Rate Sensitivity Modeling:

With Bank of England rate cuts expected throughout 2026, lenders must model how changing mortgage costs affect property affordability and demand. A 0.5% rate reduction on a £200,000 mortgage saves approximately £60 monthly, potentially expanding the buyer pool and supporting continued price appreciation.[2]

Investor-Focused Valuation Approaches

Property investors require different valuation emphasis than owner-occupiers, particularly in Northern England's strong rental markets:

Investment Valuation Components:

💼 Rental yield analysis: North East rental inflation at 8.0% annually creates compelling income opportunities[1]

💼 Capital appreciation projections: 5-7% annual growth combined with strong rental yields offers attractive total returns

💼 Tenant demand assessment: Employment trends, student populations, and demographic shifts affecting rental demand

💼 Operating expense evaluation: Management costs, maintenance requirements, and void periods impacting net yields

💼 Exit strategy considerations: Likely future buyer pool and resale potential

Comparative Regional Analysis:

Investors increasingly compare Northern England opportunities against Southern alternatives:

| Metric | North West | South East | Investor Advantage |

|---|---|---|---|

| Average Price | £238,000 | £385,000 | North: Lower entry cost |

| Annual Growth | 4.5% | 1.0% | North: Higher appreciation |

| Rental Yield | 5-7% | 3-4% | North: Better income |

| Total Return | 9-12% | 4-5% | North: Superior combined return |

When conducting freehold valuation for investment properties, surveyors must incorporate both income and capital appreciation components to provide comprehensive investment analysis.

First-Time Buyer Considerations

First-time buyers represent a significant portion of Northern England's market growth, driven by superior affordability:

First-Time Buyer Valuation Factors:

🏡 Absolute price accessibility: Properties under £250,000 qualify for reduced stamp duty and improved mortgage terms

🏡 Future family needs: Valuation of growth potential (loft conversions, extensions) affects long-term suitability

🏡 Commuting patterns: Transport links to employment centers significantly impact desirability and value

🏡 Neighborhood trajectory: Areas undergoing regeneration offer appreciation potential but carry execution risk

🏡 Shared ownership and Help to Buy: Government scheme eligibility affects effective affordability and market access

Affordability Stress Testing:

Professional valuers should consider whether first-time buyer clients can sustain mortgage payments if interest rates rise from current levels, despite expected 2026 rate cuts. A property affordable at 4% mortgage rates may become challenging at 5-6%, affecting both purchase decision and long-term value sustainability.

Developer and Builder Valuation Requirements

Property developers require specialized valuation approaches for land acquisition, development appraisal, and sales pricing:

Development Valuation Considerations:

🏗️ Residual land value calculations: Working backward from projected sale prices to determine viable land acquisition costs

🏗️ Phased release pricing: Multi-phase developments must account for market appreciation during construction and sales periods

🏗️ Specification impact: Build quality and specification choices significantly affect achievable prices in competitive markets

🏗️ Planning gain and Section 106: Affordable housing requirements and infrastructure contributions affecting development viability

🏗️ Market absorption rates: Realistic assessment of sales velocity in local market conditions

In Northern England's strong markets, developers benefit from rising prices during construction periods, but must avoid over-optimistic projections that compromise development viability if market conditions moderate.

Navigating Regulatory and Professional Standards

RICS Red Book Compliance in Regional Markets

The RICS Valuation – Global Standards (Red Book) provides the framework for professional valuation practice, but application requires regional market understanding:

Key Red Book Requirements:

📘 Basis of value clarity: Market value, investment value, or other basis must be explicitly stated and appropriate for purpose

📘 Assumptions and special assumptions: Any departures from standard assumptions (e.g., assuming completion of renovations) must be clearly documented

📘 Inspection and investigation: Appropriate inspection level for valuation purpose and property type

📘 Comparable evidence: Sufficient market evidence to support valuation conclusions

📘 Independence and objectivity: Freedom from conflicts of interest and objective professional judgment

Regional Application Challenges:

In markets experiencing 5-7% annual growth significantly above national averages, valuers must carefully document the market evidence supporting valuations that may appear optimistic compared to broader UK trends. Clear explanation of regional divergence protects both valuer and client.

Professional surveyors should reference valuers registered with the RICS to ensure compliance with current professional standards and continuing professional development requirements.

Managing Professional Liability in Volatile Markets

Professional indemnity insurance and liability management require particular attention in rapidly appreciating markets:

Risk Management Strategies:

⚖️ Conservative comparable selection: When market evidence is mixed, favor conservative comparables over optimistic outliers

⚖️ Clear limitation of scope: Document any inspection limitations or information unavailability affecting valuation confidence

⚖️ Market condition caveats: Explicitly state that valuations reflect market conditions at inspection date and may change rapidly

⚖️ Appropriate valuation ranges: Consider providing valuation ranges rather than single-point figures in uncertain markets

⚖️ Regular market monitoring: Stay current with regional trends through continuing professional development and market research

Negligence Claims and Market Changes:

Valuations that appear inaccurate due to subsequent market changes do not automatically constitute negligence. Professional liability depends on whether the valuation was reasonable based on information available at the time, using appropriate methodology and professional skill.

Data Protection and Client Confidentiality

Valuation work involves sensitive financial and personal information requiring strict data protection compliance:

GDPR Compliance Requirements:

🔒 Lawful basis for processing: Legitimate interest or contractual necessity for valuation data collection

🔒 Data minimization: Collect only information necessary for valuation purpose

🔒 Secure storage and transmission: Encrypted digital files and secure physical document storage

🔒 Retention policies: Clear data retention schedules and secure disposal procedures

🔒 Client access rights: Procedures for clients to access, correct, or request deletion of personal data

Comparable Evidence and Privacy:

When using comparable sales evidence, valuers must ensure that property-specific information from previous clients is not disclosed without consent, while still providing sufficient detail to support valuation conclusions.

Future Outlook: Sustaining Valuation Accuracy as Markets Evolve

Anticipated Market Developments Through 2026

Valuation Strategies for Northern England's 5-7% Price Surge: Outpacing Southern Market Slumps in 2026 must account for likely market evolution throughout the year:

Expected Positive Factors:

📈 Interest rate reductions: Bank of England rate cuts expected throughout 2026 will improve mortgage affordability[2][5]

📈 Inflation normalization: UK inflation dropping to 3% in January 2026 with further falls anticipated in April supports economic stability[2]

📈 Sustained affordability advantage: Northern England's price differential versus Southern regions remains substantial and compelling

📈 Infrastructure investment: Continued Northern Powerhouse and leveling-up initiatives support economic development

📈 Remote work flexibility: Ongoing work-from-home arrangements enable location flexibility favoring affordable regions

Potential Headwinds:

📉 Economic uncertainty: Global economic conditions and UK-specific challenges may affect buyer confidence

📉 Affordability limits: Even in Northern markets, rapid price growth eventually constrains buyer pools

📉 Policy changes: Potential modifications to stamp duty, Help to Buy, or mortgage regulations

📉 Regional economic performance: Northern growth depends on sustained employment and wage growth

📉 Market correction risk: Rapid appreciation sometimes precedes price corrections as markets overshoot fundamentals

Adapting Valuation Methodologies for Changing Conditions

Professional valuers must continuously adapt methodologies as markets evolve:

Ongoing Professional Development:

🎓 Regional market expertise: Regular analysis of Northern England transaction data and trends

🎓 Economic indicator monitoring: Tracking employment, wages, migration, and development activity

🎓 Regulatory updates: Staying current with RICS guidance and regulatory changes

🎓 Technology adoption: Incorporating new valuation tools and data sources appropriately

🎓 Peer learning: Engaging with professional networks to share market intelligence and best practices

Methodology Refinement:

As markets mature and data accumulates, valuation methodologies should be refined based on actual performance versus projections. Tracking valuation accuracy over time enables continuous improvement and enhanced professional judgment.

Building Resilient Valuation Practices

Long-term success in property valuation requires building practices that perform accurately across varying market conditions:

Resilience Strategies:

💪 Diversified expertise: Capability across multiple property types, valuation purposes, and geographic areas

💪 Robust quality assurance: Systematic peer review and validation processes

💪 Strong professional networks: Relationships with other surveyors, estate agents, and market participants providing market intelligence

💪 Technology integration: Balanced use of technology to enhance rather than replace professional judgment

💪 Client education: Clear communication helping clients understand valuation basis, limitations, and market context

💪 Ethical practice: Unwavering commitment to independence, objectivity, and professional standards regardless of client pressure

The current regional divergence—with Northern England significantly outpacing Southern markets—represents both opportunity and challenge for valuation professionals. Those who develop deep regional expertise, maintain rigorous professional standards, and adapt methodologies to changing conditions will provide the greatest value to clients and maintain the strongest professional reputations.

Conclusion: Mastering Valuation in England's Divergent Property Markets

The Valuation Strategies for Northern England's 5-7% Price Surge: Outpacing Southern Market Slumps in 2026 require sophisticated professional approaches that recognize fundamental regional divergence in England's property markets. The North East's 4.6% annual growth and North West's 4.5% appreciation—both substantially exceeding the UK average of 2.4% and dramatically outpacing the South East's 1.0%—represent more than temporary fluctuations.[1][2]

These regional differences reflect structural market changes driven by affordability differentials, economic development patterns, demographic shifts, and evolving work arrangements. Professional valuers must adapt methodologies to capture these dynamics accurately, moving beyond simple comparable analysis to incorporate affordability metrics, market momentum assessment, and forward-looking trend analysis.

Key Professional Imperatives

For Chartered Surveyors:

- Develop deep regional market expertise specific to Northern England's dynamics

- Enhance comparable analysis with time-based adjustments reflecting documented monthly appreciation

- Incorporate affordability metrics and buyer pool analysis into valuation frameworks

- Maintain rigorous RICS Red Book compliance with enhanced documentation in volatile markets

- Invest in continuing professional development focused on regional market intelligence

For Property Professionals:

- Recognize that national averages obscure significant regional variations requiring localized expertise

- Understand that factors of valuation vary substantially between high-growth Northern and stagnant Southern markets

- Engage RICS-qualified surveyors with specific Northern England experience for critical valuations

- Consider both current market conditions and likely evolution when making property decisions

- Utilize appropriate survey types—from RICS building surveys to specialist assessments—based on property type and transaction purpose

For Market Participants:

- Recognize Northern England's affordability advantage as a sustainable driver of demand

- Understand that anticipated interest rate cuts will disproportionately benefit affordable Northern markets

- Consider regional diversification strategies to capitalize on varying growth rates

- Monitor economic indicators and infrastructure development supporting Northern growth

- Maintain realistic expectations about market sustainability and potential correction risks

Actionable Next Steps

Immediate Actions:

-

Engage qualified professionals: Contact chartered surveyors with specific Northern England expertise for accurate property valuations

-

Conduct comprehensive research: Analyze recent transaction data for specific postcode sectors rather than relying on regional averages

-

Assess affordability dynamics: Calculate income-to-price ratios and mortgage affordability for target properties and buyer demographics

-

Review comparable evidence: Ensure valuations incorporate recent transactions with appropriate time-based adjustments

-

Consider specialist assessments: Obtain specific defect reports or subsidence surveys where property-specific issues may affect valuations

Medium-Term Strategies:

-

Monitor market evolution: Track monthly house price indices and rental market data to identify trend changes

-

Build professional networks: Develop relationships with estate agents, mortgage brokers, and other market participants providing market intelligence

-

Enhance market knowledge: Participate in professional development focused on regional market analysis and valuation methodology

-

Review valuation accuracy: Compare valuations against subsequent sale prices to refine professional judgment

-

Stay regulatory current: Monitor RICS guidance updates and regulatory changes affecting valuation practice

Long-Term Positioning:

-

Develop regional specialization: Build recognized expertise in Northern England property markets

-

Invest in technology: Adopt appropriate valuation tools and data analytics enhancing professional capabilities

-

Maintain professional standards: Uphold RICS Red Book compliance and ethical practice regardless of market pressures

-

Contribute to industry knowledge: Share market insights through professional publications and peer networks

-

Adapt to market changes: Continuously refine methodologies based on market performance and emerging trends

The unprecedented regional divergence characterizing England's 2026 property market creates both opportunities and challenges. Northern England's strong performance—driven by fundamental affordability advantages and supported by anticipated interest rate reductions—appears sustainable in the near term. However, professional valuers must balance recognition of genuine market strength against the risks of over-optimism and potential corrections.

Success in this environment requires technical excellence, regional expertise, professional integrity, and continuous adaptation. Those who master these elements will provide invaluable service to clients navigating England's complex and divergent property markets, while maintaining the professional standards that protect both practitioners and the public they serve.

The property valuation profession faces a defining period as regional markets diverge more dramatically than at any time in recent decades. By embracing sophisticated valuation strategies, maintaining rigorous professional standards, and developing deep regional market expertise, chartered surveyors can navigate this complexity successfully—delivering accurate, defensible valuations that serve clients and support well-functioning property markets across all regions of England.