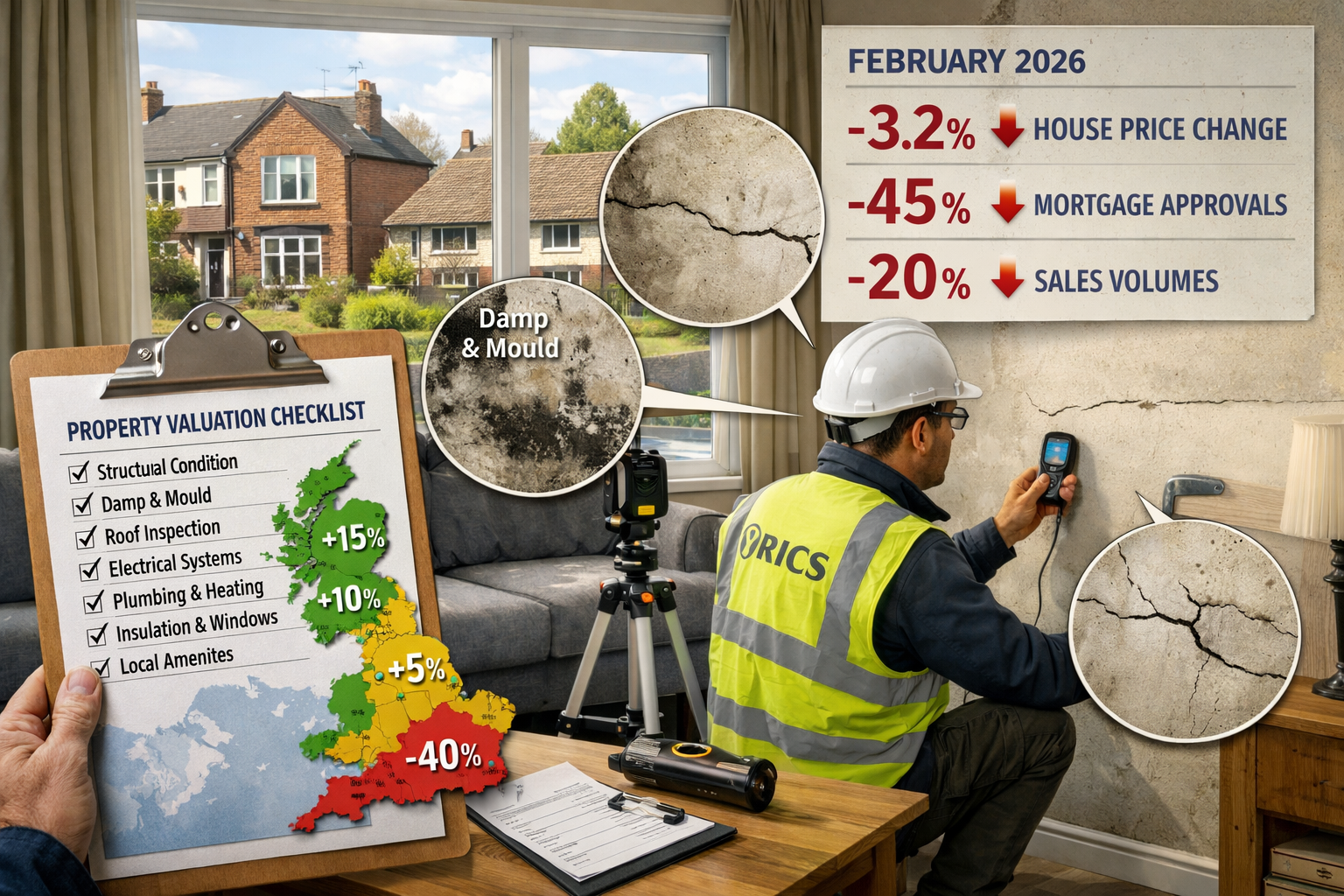

Buyer demand in the UK residential market plummeted to a net balance of -26% in February 2026, marking the sharpest monthly decline since late 2025 and reversing early-year optimism that suggested a spring recovery.[1] This dramatic deterioration, coupled with geopolitical tensions in the Middle East and renewed mortgage rate pressures, has created a complex valuation landscape that demands sophisticated analytical approaches from RICS-accredited surveyors. Understanding Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump has become essential for property professionals navigating this turbulent market environment.

The February 2026 RICS UK Residential Market Survey reveals a market caught between contradictory forces: constrained supply, regional price divergence, and weakening transaction momentum. For surveyors and valuers, these conditions require recalibrated methodologies that account for heightened volatility, shifting buyer psychology, and unprecedented regional variations in price performance.

Key Takeaways

- Buyer demand collapsed to -26% in February 2026, down from -15% in January, driven by geopolitical uncertainty and renewed mortgage rate concerns

- Regional price divergence reached historic levels, with London experiencing -40% net balance while Northern regions maintained relative resilience

- Short-term price expectations deteriorated sharply to -18%, reflecting immediate market caution, though 12-month outlook remains moderately positive at +33%

- Valuation methodologies must incorporate geopolitical risk premiums, enhanced comparable analysis, and regional adjustment factors to maintain accuracy

- RICS Red Book compliance becomes more critical in uncertain markets, requiring rigorous documentation of assumptions and market conditions

Understanding the February 2026 Market Deterioration

The Collapse in Buyer Sentiment

The RICS February 2026 survey data paints a concerning picture of buyer withdrawal from the market. New buyer enquiries fell to a net balance of -26%, representing a significant deterioration from January's -15% reading.[1] This decline reversed the modest improvements observed in late 2025 and early 2026, when mortgage rate reductions had temporarily boosted market participation.

Key demand indicators from February 2026:

| Metric | February 2026 | January 2026 | Change |

|---|---|---|---|

| New Buyer Enquiries | -26% | -15% | ⬇️ 11 points |

| Agreed Sales | -12% | -10% | ⬇️ 2 points |

| Near-term Sales Expectations | -2% | +5% | ⬇️ 7 points |

| 12-month Sales Expectations | +17% | +35% | ⬇️ 18 points |

The weakening in agreed sales to -12% and the softening of near-term expectations to -2% (the weakest reading since November 2025) indicate that the demand slump is translating directly into reduced transaction volumes.[2] When considering RICS home surveys and valuation work, this reduced activity creates challenges for establishing reliable comparable evidence.

Geopolitical Triggers and Economic Headwinds

RICS survey respondents specifically cited Middle East geopolitical escalation, particularly concerning Iran, as a direct contributor to weakened buyer confidence.[1] The mechanism through which geopolitical uncertainty impacts residential valuations operates through multiple channels:

🌍 Energy price volatility → Rising oil costs increase household expenses and inflation expectations

📈 Mortgage rate implications → Central banks maintain higher rates longer to combat inflation pressures

💷 Economic uncertainty premium → Buyers delay major financial commitments during unstable periods

🏠 Wealth effect concerns → Stock market volatility reduces perceived household wealth

For surveyors conducting RICS valuation work, these macroeconomic factors must be explicitly considered when determining market value, particularly when advising clients on purchase decisions or refinancing strategies.

Regional Price Divergence: The North-South Divide Intensifies

Southern England Under Pressure

The February 2026 RICS data reveals the most pronounced regional divergence in recent survey history. London experienced the sharpest downward pressure at a net balance of -40%, followed by East Anglia at -26% and the South East at -24%.[1] This represents a dramatic deterioration in southern market sentiment.

Regional price balance breakdown:

- London: -40% (most negative reading in survey)

- East Anglia: -26%

- South East: -24%

- South West: -15%

- National Average: -12%

The compression in London's 12-month price expectations from +56% to just +7% represents a particularly striking shift in sentiment.[2] For surveyors valuing properties in these regions, this creates significant challenges in comparable selection and adjustment.

Northern Resilience Continues

In contrast, Northern Ireland, Scotland, and the North West of England continued to report firmer price trends relative to their southern counterparts.[1] This resilience reflects several structural factors:

✅ Affordability advantage – Lower absolute prices maintain buyer participation

✅ Less exposure to international uncertainty – Reduced foreign buyer presence limits volatility

✅ Stronger local employment markets – Regional economic performance remains robust

✅ Less stretched valuations – Price-to-income ratios remain more sustainable

When conducting Manchester valuations or assessments in other northern markets, surveyors must resist the temptation to apply national trends uniformly. Regional analysis requires distinct comparable pools and adjustment factors.

Valuation Strategies Amid RICS February 2026 Residential Survey Challenges

Enhanced Comparable Analysis Techniques

In volatile markets characterized by the conditions revealed in the Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump, traditional comparable analysis requires significant enhancement. Standard three-month comparable windows may no longer provide reliable evidence when market sentiment shifts rapidly.

Recommended comparable selection strategies:

- Narrow the time window – Focus on transactions from the past 4-6 weeks rather than standard 3-6 months

- Increase comparable volume – Use 6-10 comparables rather than 3-5 to identify outliers

- Weight recent evidence more heavily – Apply temporal adjustment factors to older comparables

- Cross-reference with withdrawn listings – Analyze asking prices of properties removed from market

- Include pending sales data – Incorporate agreed sales not yet completed to capture current sentiment

For RICS registered valuers, maintaining detailed records of comparable selection rationale becomes essential for defending valuations in uncertain markets.

Incorporating Geopolitical Risk Adjustments

The February 2026 survey's explicit identification of geopolitical factors as demand suppressors creates a professional obligation for surveyors to address these risks in valuation reports. While geopolitical uncertainty doesn't directly change a property's physical characteristics, it materially affects buyer willingness to transact at specific price points.

Practical approaches for risk incorporation:

📊 Scenario analysis – Provide valuation ranges reflecting different market trajectory assumptions

📝 Enhanced special assumptions – Document market conditions and uncertainty factors explicitly

⚖️ Sensitivity testing – Show how valuation changes with different comparable selections

🔍 Market conditions addendum – Include detailed market commentary beyond standard RICS requirements

When completing Red Book valuations, the RICS Valuation – Global Standards (Red Book) requires valuers to report material uncertainty when market conditions prevent reliable valuation. While February 2026 conditions don't necessarily trigger formal material uncertainty declarations, they demand enhanced disclosure and assumption documentation.

Regional Adjustment Factors

The unprecedented regional divergence revealed in the Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump data necessitates sophisticated regional adjustment methodologies. A London property valuation cannot apply the same market trend assumptions as a Manchester or Edinburgh assessment.

Regional calibration framework:

| Region | Price Trend | Adjustment Approach | Comparable Window |

|---|---|---|---|

| London | -40% | Conservative, recent comparables only | 4 weeks |

| South East | -24% | Cautious, weight recent evidence | 6 weeks |

| East Anglia | -26% | Cautious, narrow selection | 6 weeks |

| National Average | -12% | Moderate, standard approach | 8 weeks |

| North West | Positive | Balanced, broader window acceptable | 10 weeks |

| Scotland | Positive | Balanced, broader window acceptable | 10 weeks |

For surveyors working across multiple regions, maintaining separate comparable databases and regional market intelligence becomes essential for accurate valuation work.

Supply Dynamics and Their Valuation Implications

Constrained New Instructions

Despite weakening demand, new property instructions remained stable at a net balance of +2% in February 2026.[1] This near-neutral reading indicates that fresh listings are neither rising nor falling materially at the national level, creating a supply-demand imbalance that complicates valuation analysis.

When supply remains constrained while demand weakens, the traditional relationship between market activity and price movement becomes less predictable. Properties may take longer to sell, but price reductions may be less severe than demand metrics alone would suggest.

For homebuyer surveys and purchase valuations, this dynamic creates specific considerations:

- Marketing period assumptions must be extended beyond historical norms

- Negotiation leverage shifts toward buyers despite limited inventory

- Price expectations require careful calibration between supply constraints and demand weakness

Rental Market Pressures

The rental sector experienced even more acute supply constraints, with landlord instructions at -27%, representing the lowest point in the survey series.[1] This severe shortage in rental stock creates valuation challenges for buy-to-let investors and those requiring rental value assessments.

Rental market implications:

🏘️ Yield compression – Rental values may hold firm while capital values soften, affecting investment valuations

📉 Landlord exit continues – Regulatory pressures and tax changes drive further supply reduction

📈 Tenant demand remains strong – Rental market fundamentals remain tighter than sales market

💼 Investment strategy shifts – Valuation approaches must reflect changing investor motivations

When conducting valuations for shared ownership properties or right to buy assessments, understanding these rental market dynamics becomes particularly important for determining fair market value.

Price Expectations and Forward-Looking Valuation Approaches

Short-Term Pessimism vs. Medium-Term Optimism

The February 2026 RICS survey reveals a striking dichotomy in price expectations. Short-term expectations deteriorated sharply to -18% from -6% in January, reflecting immediate caution following geopolitical escalation.[2] However, 12-month expectations remained moderately positive at +33%, though down from +43% previously.[2]

This divergence suggests market participants expect current uncertainty to prove temporary, with more normal conditions returning later in 2026. For valuers, this creates a professional dilemma: should valuations reflect current distressed sentiment or incorporate expectations of recovery?

RICS Red Book guidance on market expectations:

The Red Book requires valuations to reflect market conditions as of the valuation date, not anticipated future conditions. However, market value inherently incorporates the expectations of typical market participants. When those participants demonstrate clear forward-looking optimism (as evidenced by the +33% 12-month expectation), this sentiment forms part of the current market psychology.

Balancing Current Evidence with Market Psychology

Practical approaches for incorporating expectation data into valuations include:

- Primary reliance on current comparables – Base valuation on actual transaction evidence

- Secondary consideration of sentiment – Use expectation data to inform comparable adjustment decisions

- Explicit documentation – Clearly state how forward expectations influenced professional judgment

- Scenario sensitivity – Provide alternative valuations under different market trajectory assumptions

For building surveys that include valuation elements, maintaining clear separation between physical condition assessment and market value opinion becomes particularly important in uncertain markets.

Practical Implementation for RICS Surveyors

Documentation and Reporting Standards

In markets characterized by the conditions revealed in Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump, documentation standards must exceed typical requirements. Every assumption, comparable selection decision, and adjustment factor requires explicit justification.

Enhanced documentation checklist:

✅ Market conditions summary – Include RICS survey data and regional statistics

✅ Comparable selection rationale – Explain why specific comparables were chosen or rejected

✅ Adjustment factor justification – Document basis for all location, condition, and timing adjustments

✅ Uncertainty disclosure – Identify factors that could materially affect valuation accuracy

✅ Assumption limitations – Clearly state what the valuation assumes about future market conditions

✅ Alternative scenarios – Consider providing valuation ranges or sensitivity analysis

When completing valuation for probate or capital gains tax purposes, this enhanced documentation protects both the surveyor and the client from future disputes arising from market volatility.

Client Communication Strategies

Effective communication becomes paramount when market conditions create valuation uncertainty. Clients often struggle to understand why valuations may differ from their expectations or why properties take longer to sell than anticipated.

Key communication principles:

💬 Proactive education – Explain market conditions before presenting valuation conclusions

📊 Data-driven explanations – Use RICS survey statistics to contextualize individual property assessments

🎯 Realistic expectations – Clearly communicate likely marketing periods and negotiation dynamics

⚠️ Risk transparency – Honestly discuss factors that could affect valuation accuracy

🔄 Regular updates – In fast-moving markets, offer to review valuations if conditions change materially

For clients considering comparing different types of survey, explaining how market conditions affect valuation accuracy helps them make informed decisions about survey level selection.

Professional Competence and Continuing Development

The market conditions revealed in the February 2026 RICS survey demand that surveyors maintain current knowledge of macroeconomic factors, geopolitical developments, and regional market variations. Traditional property-focused expertise must expand to encompass broader economic literacy.

Recommended professional development areas:

📚 Macroeconomic analysis – Understanding interest rate policy, inflation dynamics, and economic cycles

🌍 Geopolitical awareness – Monitoring international developments that affect UK market sentiment

📈 Regional market intelligence – Maintaining detailed knowledge of local market conditions

💻 Data analytics skills – Using statistical tools to analyze comparable evidence and identify trends

📖 Red Book updates – Staying current with RICS guidance on valuation in uncertain markets

Chartered surveyors who invest in these competencies will be better positioned to provide accurate, defensible valuations throughout market cycles.

Strategic Considerations for Different Property Types

Prime vs. Secondary Markets

The February 2026 RICS data's revelation of severe London price pressure (net balance of -40%) disproportionately affects prime central London markets, where international buyer participation and geopolitical sensitivity are highest.[1] Secondary markets in outer London and commuter zones face different dynamics.

Prime market valuation considerations:

- International buyer withdrawal – Geopolitical uncertainty particularly affects foreign investment

- Currency volatility – Exchange rate movements create additional valuation complexity

- Luxury segment sensitivity – High-value discretionary purchases face greatest demand elasticity

- Comparable scarcity – Reduced transaction volumes make reliable comparable evidence harder to obtain

Leasehold vs. Freehold Implications

Market uncertainty affects leasehold properties differently than freehold equivalents, particularly when considering lease extension valuations or enfranchisement scenarios. Weakening capital values may create opportunities for leaseholders to negotiate more favorable terms.

Leasehold-specific considerations:

🏢 Ground rent capitalization rates – Uncertainty may increase required yields

📅 Deferment rates – Market volatility affects assumptions about future value growth

⚖️ Relativity curves – Short lease discounts may widen in uncertain markets

💰 Marriage value calculations – Weakening freeholder expectations may reduce premiums

For surveyors conducting help to buy valuations or shared ownership assessments, understanding how government schemes interact with market uncertainty becomes essential for accurate valuation work.

New Build vs. Resale Properties

The RICS survey data doesn't distinguish between new build and resale markets, but these segments typically respond differently to demand shocks. New build properties often face greater price rigidity due to developer business models and construction cost floors.

New build valuation challenges:

- Incentive packages – Developers offer substantial incentives that complicate comparable analysis

- Help to Buy distortions – Government schemes create artificial demand support

- Construction cost floors – Developers resist price reductions below build cost

- Comparable selection difficulties – Mixing new build and resale comparables requires careful adjustment

Risk Management and Professional Liability

Valuation Accuracy in Volatile Markets

The conditions described in Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump create heightened professional liability exposure for surveyors. When market sentiment shifts rapidly, valuations can quickly appear inaccurate, even when they were reasonable based on available evidence at the valuation date.

Risk mitigation strategies:

🛡️ Robust assumption documentation – Clearly state all assumptions and their rationale

📸 Comprehensive evidence retention – Maintain detailed records of comparable research

⏰ Valuation date emphasis – Explicitly note that valuations reflect conditions as of specific date

📋 Scope limitation clarity – Clearly define what the valuation does and doesn't cover

🔍 Quality assurance processes – Implement internal review procedures for all valuation work

When to Consider Material Uncertainty Declarations

The RICS Valuation – Global Standards (Red Book) provides for material uncertainty declarations when market conditions prevent reliable valuation. While the February 2026 market conditions are challenging, they don't automatically trigger material uncertainty requirements.

Material uncertainty considerations:

A material uncertainty declaration is appropriate when:

- Transaction evidence is absent or unreliable – Insufficient comparables exist for confident valuation

- Market conditions are unprecedented – No historical precedent exists for current circumstances

- Valuation confidence is materially reduced – Professional judgment cannot overcome evidence limitations

The February 2026 conditions, while difficult, still provide sufficient transaction evidence in most regions to support reliable valuations without formal material uncertainty declarations. However, individual property circumstances may warrant such declarations.

Professional Indemnity Insurance Considerations

Surveyors should review their professional indemnity insurance coverage to ensure it adequately addresses valuation work in uncertain markets. Key considerations include:

- Adequate coverage limits – Ensure limits reflect current market values and potential claims

- Retroactive coverage – Verify protection for valuations conducted in previous policy periods

- Claims notification procedures – Understand when to notify insurers of potential issues

- Coverage exclusions – Review exclusions that might apply to geopolitical or market uncertainty scenarios

Looking Forward: Market Recovery Indicators

Monitoring Key Metrics

For surveyors navigating the conditions revealed in the Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump, establishing a framework for monitoring market recovery becomes essential for adjusting valuation approaches as conditions evolve.

Critical indicators to track:

📊 RICS new buyer enquiries – Return to positive territory signals demand recovery

📈 Mortgage approval volumes – Leading indicator of transaction activity

💷 Mortgage rate trends – Sustained rate reductions support buyer confidence

🌍 Geopolitical developments – Resolution of Middle East tensions removes uncertainty premium

🏠 Regional price balance convergence – Narrowing North-South gap indicates market stabilization

Scenario Planning for Different Recovery Paths

Professional valuers should develop contingency approaches for different market trajectory scenarios:

Optimistic scenario – Geopolitical tensions ease, mortgage rates fall, demand recovers by Q3 2026

- Valuation approach: Gradually extend comparable windows, reduce uncertainty premiums

- Communication strategy: Emphasize forward-looking market optimism

Base case scenario – Uncertainty persists through 2026, gradual improvement into 2027

- Valuation approach: Maintain conservative comparable selection, continue enhanced documentation

- Communication strategy: Emphasize long-term market fundamentals

Pessimistic scenario – Geopolitical situation deteriorates, recession emerges, prolonged market weakness

- Valuation approach: Consider material uncertainty declarations, provide valuation ranges

- Communication strategy: Emphasize risk transparency, recommend delayed transactions where appropriate

Conclusion

The Valuation Strategies Amid RICS February 2026 Residential Survey: Responding to Geopolitical Uncertainty and Buyer Sentiment Slump reveal a UK residential market facing significant headwinds. The collapse in buyer demand to -26%, coupled with unprecedented regional price divergence and geopolitical uncertainty, creates complex challenges for RICS-accredited surveyors and valuers.[1][2]

Accurate property valuation in these conditions demands enhanced methodologies that go beyond traditional approaches. Surveyors must narrow comparable selection windows, increase evidence volumes, incorporate regional adjustment factors, and provide comprehensive documentation of assumptions and market conditions. The dramatic North-South divide—with London experiencing -40% price pressure while northern regions maintain resilience—requires distinct regional approaches rather than uniform national methodologies.[1]

Professional excellence in uncertain markets requires several critical actions:

Immediate action steps for surveyors:

- Review and update comparable databases – Ensure evidence reflects current market conditions

- Enhance documentation standards – Exceed minimum RICS requirements for assumption disclosure

- Implement regional calibration – Develop distinct approaches for different UK markets

- Strengthen client communication – Proactively educate clients about market uncertainty

- Monitor recovery indicators – Track RICS survey data and macroeconomic developments

- Review professional insurance – Ensure adequate coverage for current market conditions

- Invest in continuing development – Expand macroeconomic and geopolitical knowledge

The moderate optimism reflected in 12-month price expectations (+33%) suggests market participants believe current challenges will prove temporary.[2] However, professional valuers cannot rely on optimistic forecasts—they must base valuations on current evidence while transparently documenting the uncertain environment.

For property owners, buyers, and investors, engaging qualified RICS surveyors who understand these complex market dynamics becomes more important than ever. Accurate valuations in uncertain times require not just technical competence but also sophisticated understanding of macroeconomic forces, regional variations, and geopolitical risk factors.

The February 2026 RICS survey serves as a critical reminder that property markets don't operate in isolation from broader economic and political developments. Surveyors who adapt their methodologies to reflect this reality—while maintaining rigorous professional standards—will provide the most valuable service to clients navigating these challenging conditions.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[4] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets