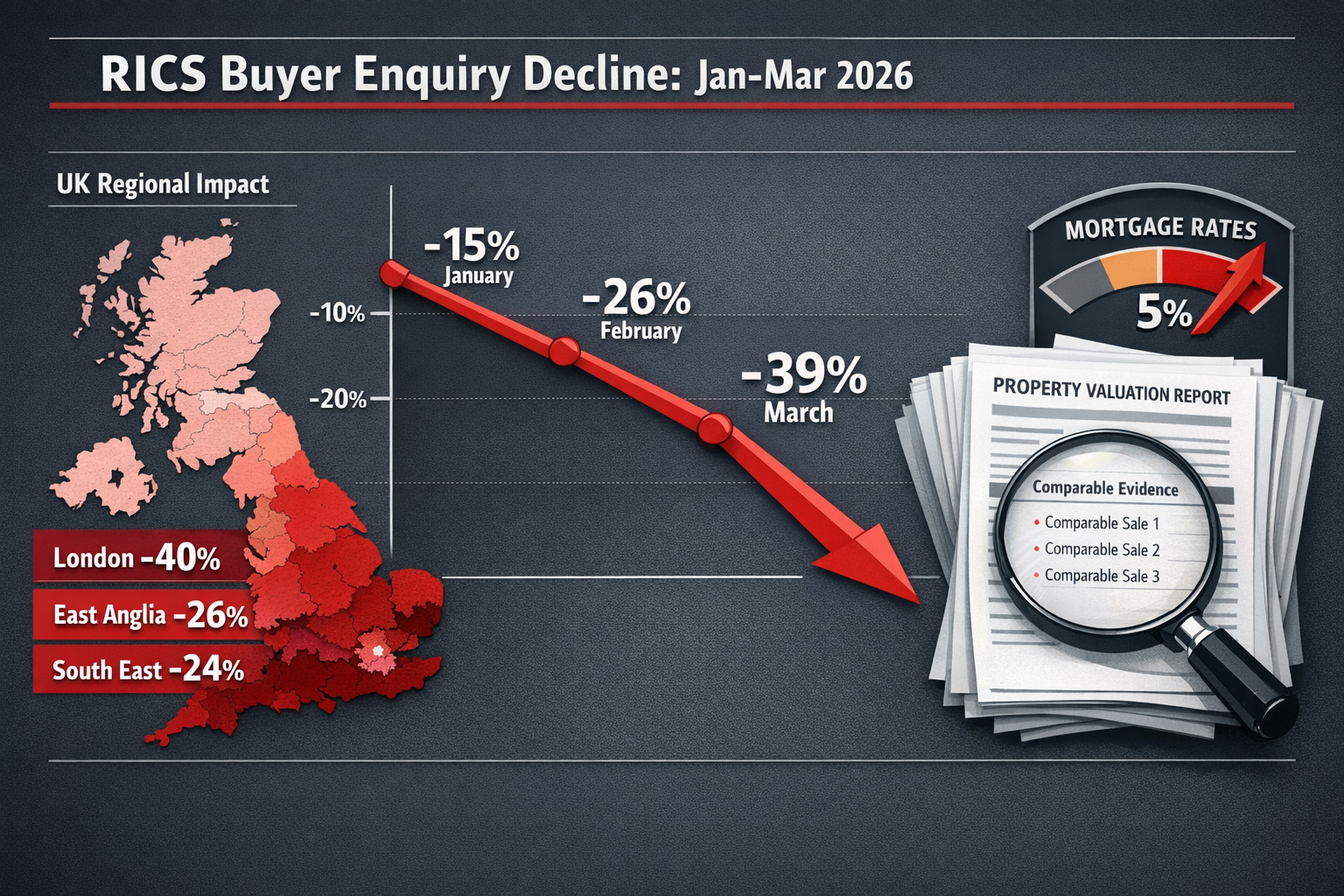

The Royal Institution of Chartered Surveyors (RICS) February 2026 residential market survey revealed a dramatic collapse in buyer interest, with new enquiries plummeting to -26%, down from -15% in January—a trend that accelerated further to -39% by March 2026. This represents the weakest reading since August 2023 and signals fundamental challenges for property valuations across Southern England.[1] For chartered surveyors navigating Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Survey Strategies for Weak Southern Markets, the data demands immediate recalibration of valuation methodologies, particularly when assessing comparable evidence in regions experiencing concentrated downward pressure.

The market deterioration extends beyond simple demand metrics. Agreed sales posted a net balance of -12% in February before collapsing to -34% in March, while London recorded the steepest regional price decline at -40%.[1][2] These figures create complex valuation challenges for surveyors working in Southern markets, where traditional comparable evidence may no longer reflect current market realities.

Key Takeaways

- Buyer enquiries dropped to -26% in February 2026 and further declined to -39% by March, creating significant downward pressure on property valuations across Southern England

- London experienced a -40% net balance in price sentiment, followed by East Anglia (-26%) and South East (-24%), requiring region-specific valuation adjustment strategies

- Mortgage costs above 5% directly impact affordability calculations and comparable evidence relevance in current market assessments

- Regional divergence widened substantially, with Northern markets maintaining firmer price trends while Southern regions face concentrated weakness

- Surveyors must adapt comparable selection criteria to account for rapid market deterioration and reduced transaction volumes when conducting Red Book valuations

Understanding the February 2026 RICS Data: Market Context and Implications

The February 2026 RICS survey data reveals a market in rapid transition, with multiple indicators pointing toward sustained weakness in Southern property markets. The -26% net balance for new buyer enquiries represents a substantial deterioration from the previous month, but the subsequent March reading of -39% suggests accelerating rather than stabilizing conditions.[2]

Regional Price Divergence: The North-South Split

The geographic distribution of price weakness presents critical challenges for valuation professionals. London's -40% net balance stands in stark contrast to Northern Ireland, Scotland, and the North West of England, which continue reporting firmer price trends.[1] This regional divergence requires surveyors to:

- Adjust comparable evidence timeframes more aggressively in Southern markets

- Apply location-specific market condition adjustments that reflect local demand dynamics

- Consider cross-regional comparable evidence with extreme caution

- Document regional market factors explicitly in valuation reports

For properties in areas served by chartered surveyors in South East London and South West London, the -40% London reading demands particular attention to comparable selection and adjustment factors.

Transaction Volume Collapse and Valuation Evidence

The agreed sales metric deteriorating from -12% in February to -34% in March creates a fundamental challenge for surveyors: reduced transaction volumes limit available comparable evidence.[2] When fewer properties complete, surveyors must:

✅ Extend comparable search periods while applying appropriate time adjustments

✅ Broaden geographic search parameters to capture sufficient evidence

✅ Weight recent transactions more heavily despite smaller sample sizes

✅ Consider withdrawn listings and price reductions as market indicators

The average unsold stock on estate agents' books increased to 47 properties by March 2026, up from approximately 45 at the start of the year, indicating growing inventory challenges particularly in weaker Southern regions.[2]

Mortgage Cost Impact on Affordability

Average fixed mortgage rates climbing back above 5% by March 2026 directly affect property valuations through affordability constraints.[2] Surveyors conducting RICS valuation assessments must consider:

- Reduced buyer purchasing power at higher interest rates

- Increased deposit requirements limiting market participation

- Affordability stress testing by mortgage lenders

- Buyer preference shifts toward lower price points

These factors compress demand at higher price brackets, creating disproportionate downward pressure on premium properties in Southern markets.

Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Practical Survey Methodologies

Implementing appropriate valuation adjustments in response to the February 2026 RICS data requires systematic methodology changes across multiple valuation components. Surveyors must balance Red Book compliance with market reality recognition.

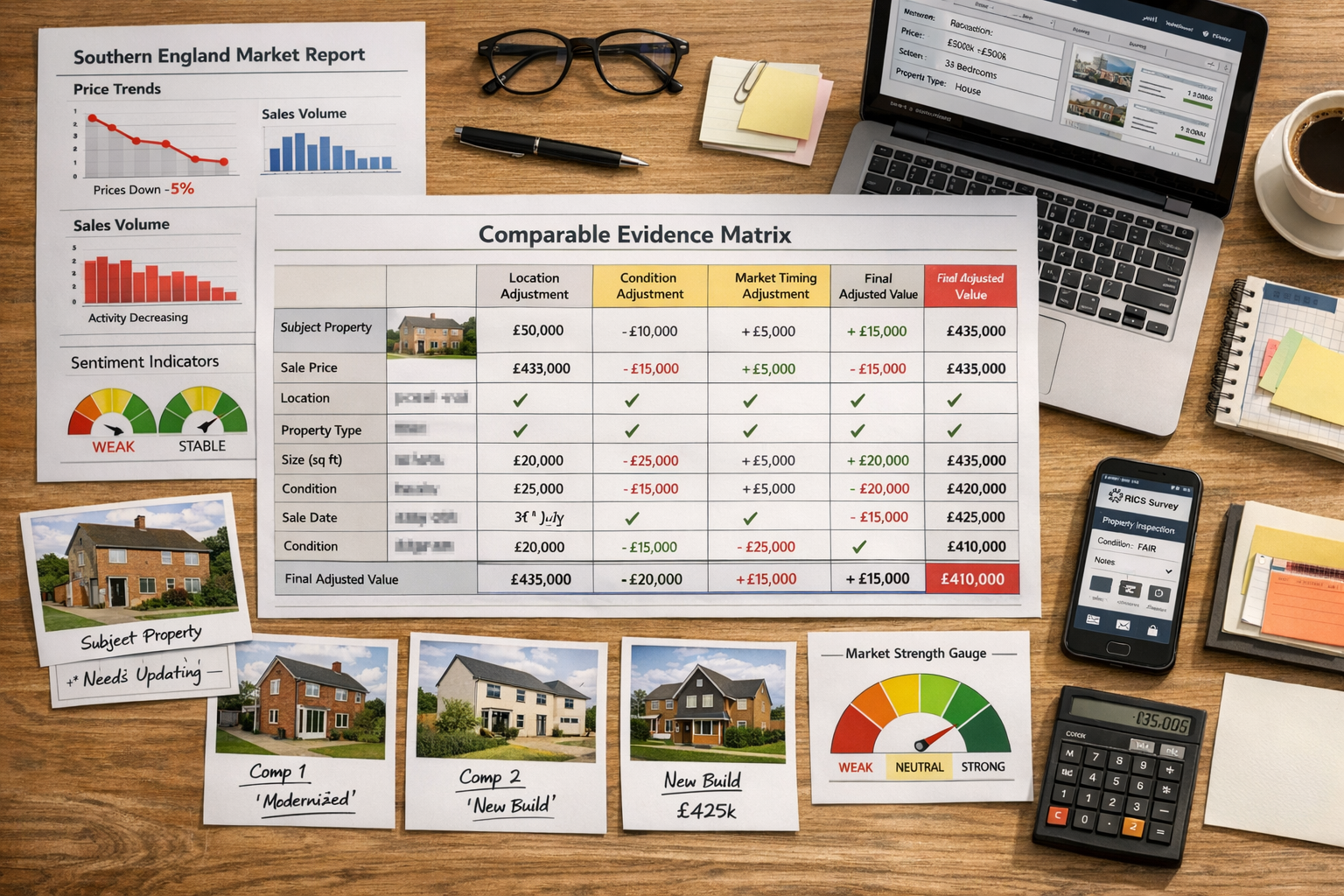

Comparable Evidence Selection in Weak Markets

Traditional comparable selection criteria—typically focusing on transactions within the past 3-6 months—may prove insufficient in rapidly declining markets. The Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Survey Strategies for Weak Southern Markets demand refined approaches:

Temporal Adjustments

| Time Period | Market Condition | Suggested Adjustment Range |

|---|---|---|

| 0-3 months | Rapid decline (-26% to -39% enquiries) | 0% to -2% per month |

| 3-6 months | Pre-decline period | -3% to -5% cumulative |

| 6-12 months | Different market cycle | Use with extreme caution |

Geographic Radius Expansion

When transaction volumes decline, surveyors may need to expand geographic search parameters while applying appropriate location adjustments:

- Primary search radius: 0.5 miles for urban areas, 2 miles for suburban

- Secondary search radius: 1 mile for urban areas, 5 miles for suburban

- Apply location adjustments: -5% to -15% for less desirable micro-locations

For properties requiring RICS building surveys, the physical condition assessment must inform valuation adjustments, particularly when defects may deter buyers in weak demand environments.

Market Condition Adjustments: Quantifying the Slump

The RICS data provides specific quantitative indicators that can inform market condition adjustments:

📊 Buyer Enquiry Adjustment Factor

February -26% reading suggests applying a -3% to -5% market condition adjustment compared to pre-slump valuations, with March's -39% reading justifying -5% to -8% adjustments.

📊 Regional Weighting Factors

- London: -40% price balance = -6% to -9% adjustment

- East Anglia: -26% price balance = -4% to -6% adjustment

- South East: -24% price balance = -3% to -5% adjustment

These adjustments should be applied to comparable evidence from stronger market periods to reflect current market realities. Surveyors working in areas like Guildford, Esher, and Oxfordshire must carefully calibrate these factors to local conditions.

Price Expectation Integration

The sharp deterioration in short-term price expectations—falling to -43% for the next three months in March 2026 compared to -18% in February—provides forward-looking valuation context.[2] While Red Book valuations reflect current market value rather than future predictions, surveyors should:

- Document market sentiment in valuation reports

- Highlight uncertainty ranges more explicitly

- Consider shorter validity periods for valuation certificates

- Recommend revaluation triggers for pending transactions

Supply-Demand Imbalance Considerations

New instructions remained subdued, posting +2% in February and declining to -6% in March, suggesting limited new supply entering the market.[1][2] This creates a complex dynamic:

Downward Pressure Factors:

- Collapsed buyer demand (-39% enquiries)

- Rising mortgage costs (>5%)

- Negative price expectations (-43%)

Stabilizing Factors:

- Limited new supply (-6% instructions)

- Constrained inventory growth

- Reduced forced selling pressure

Surveyors must weigh these competing factors when determining valuation adjustments, recognizing that supply constraints may moderate price declines despite weak demand.

Survey Strategies for Weak Southern Markets: Regional Implementation

Implementing effective Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Survey Strategies for Weak Southern Markets requires region-specific approaches that recognize local market dynamics while maintaining Red Book compliance.

London Market: Navigating the -40% Price Balance

London's dramatic -40% net balance in February 2026, combined with the 12-month price outlook collapsing to +7% from +56% in the previous survey, demands the most aggressive valuation adjustments.[1] Surveyors conducting assessments for properties in areas like Camden, Chelsea, Hammersmith, and Fulham should consider:

Micro-Market Analysis

London's diversity requires postcode-level assessment rather than city-wide generalizations. Prime central London may experience different dynamics than outer boroughs.

Property Type Differentiation

- Flats/apartments: More vulnerable to demand collapse due to affordability constraints

- Houses with gardens: Relatively stronger demand retention

- New-build developments: Facing particular pressure from reduced investor activity

Comparable Evidence Hierarchy

- Completed transactions within 0-2 months (apply minimal adjustment)

- Agreed sales pending completion (apply -2% to -4% adjustment)

- Asking price reductions (indicative evidence only)

- Transactions from 3-6 months ago (apply -5% to -8% adjustment)

South East Corridor: Commuter Belt Challenges

The South East's -24% price balance reflects specific challenges in commuter-dependent markets where mortgage affordability constraints hit hardest.[1] Properties in Battersea, Putney, Twickenham, Chiswick, and Barnes require particular attention to:

Transport Link Premiums

Traditional location premiums for proximity to rail links may compress as hybrid working reduces commuting frequency and mortgage stress limits buyer budgets.

Price Point Sensitivity

Properties priced £500,000-£750,000 face maximum affordability pressure at 5%+ mortgage rates, requiring more substantial adjustments than lower or higher price brackets.

New-Build vs. Resale Dynamics

New-build premiums may erode faster in weak markets as buyers prioritize value and established locations over modern specifications.

East Anglia and Secondary Southern Markets

East Anglia's -26% price balance positions it between London and the broader South East, requiring calibrated approaches for markets like Hemel Hempstead, Harpenden, and Leatherhead.[1]

Market Depth Considerations

Secondary markets typically have thinner transaction volumes, making comparable evidence selection more challenging during demand slumps.

Local Economic Factors

Employment concentration, major employer stability, and demographic trends significantly influence local market resilience during broader downturns.

Cross-Border Comparable Evidence

When local transaction volumes prove insufficient, surveyors may need to reference comparable evidence from adjacent regions while applying appropriate location adjustments.

Valuation Report Documentation Standards

Regardless of location, surveyors must enhance documentation standards when applying Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Survey Strategies for Weak Southern Markets:

Market Context Section

Explicitly reference RICS survey data, regional price balances, and buyer enquiry trends affecting the subject property's market.

Comparable Evidence Justification

Document why specific comparables were selected, what adjustments were applied, and how market condition factors were quantified.

Uncertainty Disclosure

Acknowledge market volatility, limited transaction volumes, or other factors that increase valuation uncertainty.

Validity Period Limitations

Consider recommending shorter validity periods (e.g., 60 days rather than 90 days) given rapid market deterioration.

For specialized valuations such as matrimonial valuations, probate valuations, or capital gains tax assessments, these documentation standards become even more critical to support valuation conclusions in potentially contentious situations.

Advanced Adjustment Techniques for Challenging Market Conditions

Beyond basic comparable adjustments, surveyors can employ sophisticated techniques to navigate the February 2026 RICS buyer enquiry slump:

Statistical Regression Analysis

When sufficient transaction data exists, regression analysis can quantify the relationship between market indicators and realized sale prices:

- Time-series regression: Measure price decline rates across monthly cohorts

- Multi-variable analysis: Isolate the impact of property characteristics from market timing

- Regional coefficient modeling: Quantify geographic premium/discount factors

Bracketing and Sensitivity Analysis

Given market uncertainty, bracketing valuations within explicit ranges provides transparency:

Example Bracketing Approach:

- Upper bound: Comparable evidence with minimal market condition adjustment (+0% to -2%)

- Central estimate: Moderate adjustment reflecting RICS data (-4% to -6%)

- Lower bound: Aggressive adjustment anticipating further deterioration (-8% to -10%)

Mortgage Valuation vs. Market Valuation Divergence

Understanding the difference between mortgage valuations and surveys becomes critical in weak markets. Lenders may apply additional caution factors beyond surveyor market value assessments, creating potential transaction complications.

Reinstatement Cost Considerations

For insurance purposes, reinstatement build cost valuations remain independent of market value fluctuations, but surveyors should clearly distinguish between these valuation bases in reports to avoid client confusion.

Professional Standards and Red Book Compliance

The Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Survey Strategies for Weak Southern Markets must maintain strict adherence to RICS Red Book standards:

VPS 3: Valuation Reports

Reports must clearly state:

- Valuation date and market conditions as of that date

- Basis of value (typically Market Value per VPS 4)

- Assumptions and special assumptions applied

- Extent of investigations and information relied upon

Market Value Definition Compliance

Market Value requires assessment of "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

In the context of -26% buyer enquiries and -34% agreed sales, surveyors must carefully consider:

- What constitutes "proper marketing" in a severely weakened market?

- How do rapidly changing conditions affect the "valuation date" snapshot?

- What evidence demonstrates "willing buyer" behavior when enquiries collapse?

Professional Indemnity Considerations

Valuation adjustments in volatile markets increase professional liability exposure. Surveyors should:

✓ Maintain comprehensive file documentation supporting all adjustment decisions

✓ Seek peer review for complex or high-value assessments

✓ Ensure adequate professional indemnity insurance coverage

✓ Consider excluding specific high-risk instruction types if insufficient expertise exists

Client Communication Strategies During Market Downturns

Effective communication becomes paramount when delivering valuations that reflect significant downward adjustments:

Managing Vendor Expectations

Property owners often resist accepting lower valuations, particularly when recent comparable evidence suggested higher values. Surveyors should:

- Present RICS data context to demonstrate market-wide trends rather than property-specific issues

- Explain adjustment methodology transparently to build credibility

- Distinguish between market value and desired value clearly

- Recommend realistic pricing strategies aligned with current market realities

Supporting Buyer Decision-Making

For buyers commissioning homebuyer surveys or Level 3 building surveys, valuation context helps inform purchase decisions:

- Highlight negotiation opportunities created by weak demand

- Explain mortgage valuation risks that may affect financing

- Identify properties likely to experience further value pressure versus those with resilience factors

- Recommend transaction timing considerations based on market trajectory

Lender Communication

Mortgage lenders rely on surveyor valuations for lending decisions. Clear communication should address:

- Market condition factors affecting valuation certainty

- Comparable evidence limitations due to reduced transaction volumes

- Regional market divergence requiring location-specific assessment

- Validity period recommendations appropriate to market volatility

Future Market Outlook and Valuation Strategy Adaptation

While the February 2026 RICS data paints a challenging picture, surveyors must maintain forward-looking perspectives to serve clients effectively.

Monitoring Key Indicators

Surveyors should track:

📈 Monthly RICS survey releases for trend continuation or reversal signals

📈 Mortgage rate movements as primary demand drivers

📈 Regional transaction volume data to assess comparable evidence availability

📈 Government policy announcements affecting housing market fundamentals

Scenario Planning for Valuation Strategies

Given uncertainty, surveyors should develop contingency approaches:

Scenario 1: Continued Deterioration

If buyer enquiries decline further beyond -39%, more aggressive adjustments (-10% to -15%) may become necessary, particularly in Southern markets.

Scenario 2: Stabilization

If mortgage rates stabilize or decline, demand may recover, reducing the need for substantial market condition adjustments.

Scenario 3: Regional Divergence Acceleration

If Northern markets continue strengthening while Southern markets weaken further, cross-regional comparable evidence becomes increasingly problematic.

Professional Development Priorities

Surveyors should prioritize:

- Advanced statistical analysis training for quantifying market adjustments

- Regional market specialization to develop deep local expertise

- Red Book update monitoring for guidance on volatile market valuations

- Peer networking to share adjustment methodologies and market intelligence

Conclusion

The Valuation Adjustments for February 2026 RICS Buyer Enquiry Slump: Survey Strategies for Weak Southern Markets present significant professional challenges for chartered surveyors. With buyer enquiries collapsing to -26% in February and accelerating to -39% by March, combined with London's -40% price balance and agreed sales deteriorating to -34%, surveyors must fundamentally recalibrate valuation methodologies to reflect market realities.[1][2]

The key strategic adjustments include:

🔑 Applying market condition adjustments of -3% to -8% depending on regional severity and property characteristics

🔑 Expanding comparable evidence search parameters while applying appropriate temporal and location adjustments

🔑 Documenting valuation uncertainty explicitly given reduced transaction volumes and rapid market changes

🔑 Differentiating regional strategies recognizing the -40% London balance versus firmer Northern markets

🔑 Maintaining Red Book compliance while adapting to unprecedented market conditions

For property owners, buyers, and lenders navigating these challenging conditions, engaging qualified RICS valuers with demonstrated expertise in weak market assessments becomes essential. The February 2026 data demands sophisticated analytical approaches that balance professional standards with market reality recognition.

Actionable Next Steps

For Property Owners:

- Commission updated valuations if existing assessments predate the February 2026 market shift

- Adjust pricing expectations based on current RICS data and regional factors

- Consider comprehensive building surveys to identify value-preservation opportunities through property improvements

For Buyers:

- Leverage weak demand conditions to negotiate favorable purchase terms

- Ensure mortgage valuations reflect current market realities to avoid financing complications

- Request detailed comparable evidence documentation to verify valuation conclusions

For Surveyors:

- Review and update internal valuation adjustment protocols to reflect February 2026 RICS data

- Enhance documentation standards for market condition adjustments

- Develop region-specific expertise for Southern markets experiencing concentrated weakness

- Consider which survey type best serves clients in current market conditions

The February 2026 RICS buyer enquiry slump represents a defining moment for property valuation practice in Southern England. Surveyors who adapt methodologies systematically while maintaining professional standards will provide the greatest value to clients navigating these uncertain market conditions. As mortgage costs remain above 5% and short-term price expectations sit at -43%, the coming months will test valuation professionals' ability to balance analytical rigor with practical market assessment—skills that define excellence in chartered surveying practice.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Rising Borrowing Costs Knock Buyer Demand And Sales Volumes Rics – https://www.financialreporter.co.uk/rising-borrowing-costs-knock-buyer-demand-and-sales-volumes-rics.html

[3] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026