The UK property market has entered an unprecedented era of regional divergence in 2026. While London house prices have fallen 1.7% in the 12 months to January 2026—marking the sixth consecutive month of annual decline—Scotland, Wales, and Northern England are experiencing robust growth that is reshaping the national property landscape.[1] This dramatic shift in Regional Valuation Divergences in 2026: Building Survey Strategies for Scotland, Wales, and Northern England vs London Laggards demands that chartered surveyors develop sophisticated, region-specific approaches to property assessment and client communication.

The traditional hierarchy of UK property markets has been turned on its head. Surveyors who continue to apply London-centric valuation methodologies to regional properties risk significantly undervaluing assets in high-growth areas while potentially overestimating recovery prospects in the capital. Understanding these divergences isn't merely academic—it directly impacts investment decisions, lending criteria, and portfolio strategies worth billions of pounds.

Key Takeaways

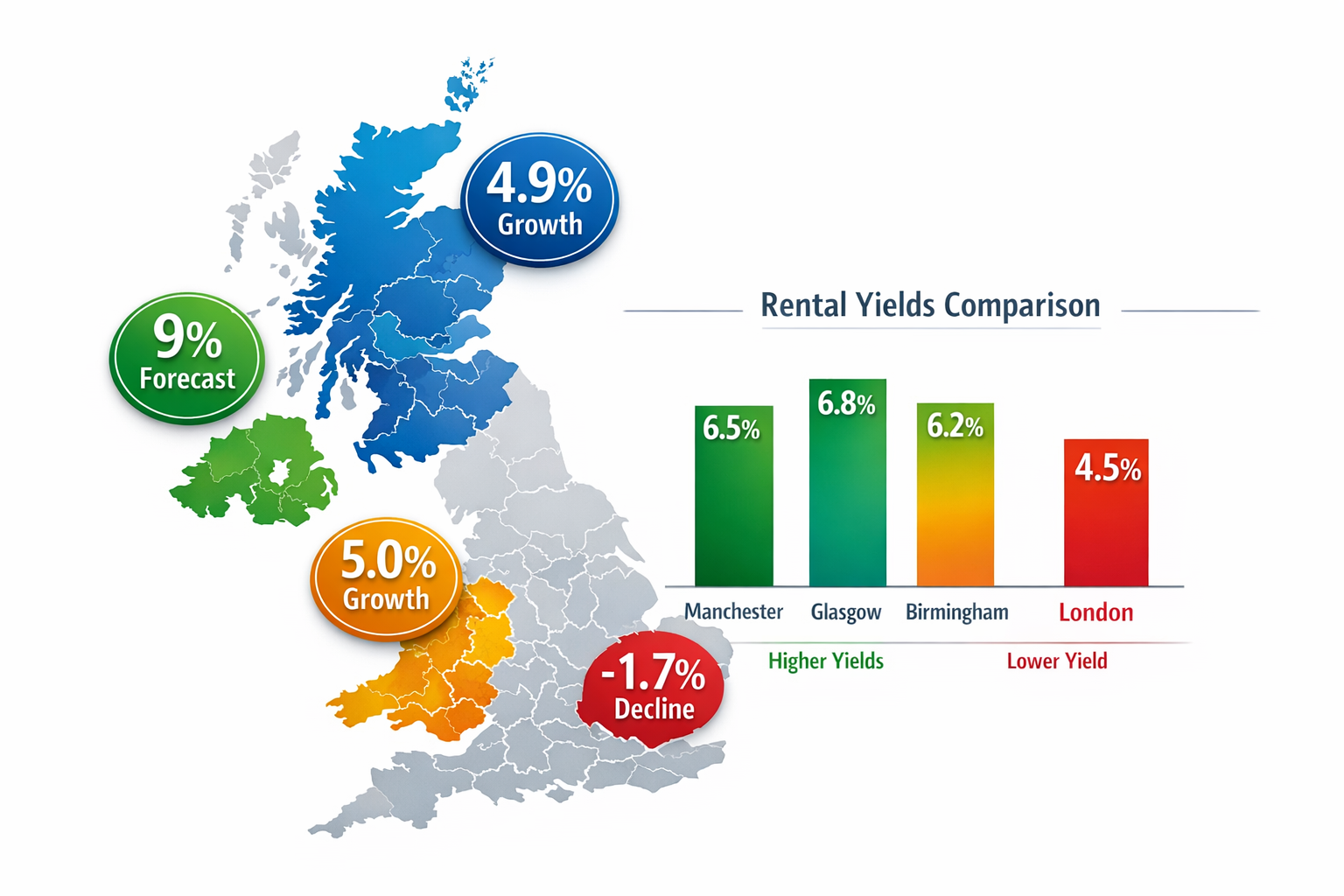

- 🏴 Scotland and Wales lead the market with annual growth rates of 4.9% and 5.0% respectively, while London declined 1.7% in the year to January 2026[1][4]

- 📈 Northern regions forecast 20-25% cumulative growth over five years, with the North West expected to achieve 9% growth from 2026-2028 alone[1]

- 💰 Rental yield advantages are substantial: Manchester (6.5%), Glasgow (6.8%), and Birmingham (6.2%) significantly outperform London's 4.5% yield[1]

- 🔍 Surveyors must adapt valuation methodologies to account for structural drivers including affordability advantages, infrastructure investment, and remote work migration patterns

- 📊 Investment capital is shifting toward regional portfolios as London-concentrated strategies offer lower yields and weaker growth prospects through 2031[3]

Understanding the 2026 Regional Valuation Divergences

The Scale of Market Separation

The current market presents the most significant regional performance gap in modern UK property history. London's 1.7% annual decline through January 2026 contrasts starkly with Scotland's 4.9% growth and Wales's 5.0% growth—a spread of nearly 7 percentage points between the strongest and weakest performers.[1][4]

This isn't a temporary blip. The Office for Budget Responsibility projects the average UK house price will rise from approximately £260,000 in 2024 to just under £305,000 by 2030, with growth averaging approximately 2.5% annually from 2026 onwards.[1] However, this national average masks profound regional variations that surveyors must understand when conducting building surveys across different markets.

Northern England's Exceptional Performance

The North West is forecast to achieve 9% growth from 2026-2028, while Yorkshire & Humber and the Midlands are expected to deliver 8% growth over the same period.[1] These figures significantly outpace London's modest 5% forecast for the same timeframe.

Over a five-year horizon, northern regions are projected to achieve 20-25% cumulative growth according to Savills projections.[1] This represents not just a cyclical advantage but a structural realignment of the UK property market that reflects fundamental economic and demographic shifts.

| Region | 12-Month Growth (to Jan 2026) | Forecast 2026-2028 | 5-Year Projection |

|---|---|---|---|

| Scotland | +4.9% | 8-9% | 20-25% |

| Wales | +5.0% | 8-9% | 20-25% |

| North West | +3.8% | 9% | 20-25% |

| Yorkshire & Humber | +3.5% | 8% | 20-25% |

| London | -1.7% | 5% | 12-15% |

The London Lag: Understanding the Capital's Weakness

London is forecast for only "moderate recovery" through 2026-2031 from its weaker starting point.[1] Several factors explain this underperformance:

Affordability constraints remain severe in the South East and London, limiting growth relative to lower-cost northern regions.[1] The average London property requires income multiples that have priced out large segments of potential buyers, creating demand suppression that doesn't exist in regional markets.

Remote work patterns have permanently altered location preferences. The flexibility to work from home has reduced the premium buyers are willing to pay for proximity to London offices, redistributing demand to more affordable regions with superior quality of life metrics.

Investment capital reallocation is underway. Within the UK industrial sector, investment conviction is skewed toward regional portfolios rather than London-concentrated ones, as London rents trade at nearly double Midlands levels yet at much lower yields.[3] This pattern extends across residential markets as well.

Regional Valuation Divergences in 2026: Developing Survey Strategies for High-Growth Markets

Adapting Comparable Selection Methodology

Traditional valuation approaches that rely heavily on comparable sales must be recalibrated for high-growth regional markets. When annual growth rates exceed 4-5%, comparables from even six months prior may significantly undervalue current market conditions.

Time adjustments become critical. Surveyors working in Scotland, Wales, and Northern England should apply monthly adjustment factors to older comparables to reflect ongoing appreciation. A property sold nine months ago in Manchester's high-growth submarkets may require a 3-4% upward adjustment to reflect current values accurately.

Geographic granularity matters more than ever. Within regions showing strong aggregate growth, specific postcodes and neighborhoods may be experiencing divergent trajectories based on local factors such as:

- Proximity to new transport infrastructure

- Urban regeneration initiatives

- School catchment areas

- Remote work desirability factors

- Local employment growth

When conducting factors of valuation assessments, surveyors must consider these micro-market dynamics rather than applying broad regional adjustments.

Incorporating Rental Yield Analysis

The rental yield divergence reveals fundamental investment opportunity differences across regions. Regional rental yields demonstrate substantial advantages:

- Manchester: 6.5%

- Glasgow: 6.8%

- Birmingham: 6.2%

- Leeds: 6.4%

- London: 4.5%[1]

These yield differentials have profound implications for valuation approaches, particularly for investment properties and portfolio assessments. A property generating £1,500 monthly rent in Manchester may be valued more favorably relative to its rental income than a London property generating £2,500 monthly rent due to the superior yield compression in regional markets.

Surveyors should incorporate yield-based valuation cross-checks alongside traditional comparable methods, particularly when assessing buy-to-let properties or multi-unit residential investments. The valuation of commercial property principles that emphasize income capitalization rates apply increasingly to residential investment properties in yield-focused markets.

Structural Driver Assessment

The Regional Valuation Divergences in 2026: Building Survey Strategies for Scotland, Wales, and Northern England vs London Laggards phenomenon is driven by structural factors that surveyors must incorporate into medium-term value projections:

Infrastructure investment is concentrated in northern regions. Major transport projects, including HS2 connections, Northern Powerhouse Rail initiatives, and urban transit expansions, are creating accessibility improvements that support long-term value appreciation in specific corridors.

Affordability advantages create sustained demand. With average property prices in northern regions typically 40-60% below London levels, these markets attract first-time buyers, young families, and relocating professionals who are permanently priced out of southern markets.

Remote work migration continues. The flexibility to work remotely has enabled professionals to relocate from expensive southern markets to affordable northern cities without sacrificing career opportunities or income levels. This demographic shift supports sustained demand growth in recipient regions.

Urban regeneration initiatives are transforming city centers across Scotland, Wales, and Northern England. Public and private investment in mixed-use developments, cultural amenities, and residential conversions of commercial buildings is enhancing urban living appeal and supporting property values.

When conducting comprehensive RICS valuations, these structural factors should inform the surveyor's assessment of future value trajectory and market positioning.

Building Survey Strategies for London and Underperforming Markets

Tempering Client Expectations

Surveyors working in London and the South East face the challenging task of communicating realistic value projections to clients accustomed to decades of outperformance. The sixth consecutive month of annual decline represents a psychological shift that requires careful client management.[1]

Transparent market context is essential. Clients purchasing or refinancing London properties need to understand that the modest 5% growth forecast for 2026-2028 represents a significant departure from historical norms.[1] This doesn't necessarily indicate a poor investment decision, but it does require adjusted return expectations.

Long-term structural support remains in place despite near-term weakness. London benefits from global capital flows, international buyer demand, limited supply in prime areas, and its status as a world financial center. These factors provide a floor beneath values and support eventual recovery, even if the timeline extends beyond initial expectations.

Identifying Value Pockets Within Weak Markets

Not all London submarkets are experiencing uniform weakness. Surveyors should identify and communicate opportunities in:

Emerging neighborhoods with improving transport links or regeneration activity may outperform the broader London market. Areas benefiting from Crossrail access, new Underground extensions, or major redevelopment schemes may show resilience despite citywide weakness.

Property types with specific demand drivers such as family homes near outstanding schools or properties suitable for multi-generational living may maintain value better than generic flats in oversupplied areas.

Chartered surveyors working across North West London, North London, South West London, South East London, and East London should develop granular knowledge of these micro-market variations.

Risk Assessment and Defect Implications

In markets experiencing price pressure, the financial impact of building defects becomes more significant. A structural issue that might represent 2-3% of value in a rising market could represent 5-7% in a stagnant or declining market due to reduced buyer appetite for properties requiring work.

Surveyors conducting building surveys in London should:

- Provide detailed cost estimates for remedial works with realistic assumptions about contractor availability and pricing

- Assess marketability impact of defects, recognizing that buyers in weak markets have more choice and less tolerance for problems

- Consider timing implications for necessary works, as delays in addressing issues may result in further value erosion in declining markets

The comparing different types of survey decision becomes more critical in weak markets, as comprehensive assessments provide greater protection against overpaying for properties with hidden issues.

Strategic Implications for Different Property Stakeholders

For Property Investors and Portfolio Managers

The Regional Valuation Divergences in 2026: Building Survey Strategies for Scotland, Wales, and Northern England vs London Laggards dynamic creates clear strategic implications for investment capital allocation.

Yield-focused investors should prioritize regional markets offering 6-7% gross yields compared to London's 4.5%.[1] The superior income generation provides both cash flow advantages and downside protection during market volatility.

Growth-focused investors should recognize that the 20-25% cumulative growth projections for northern regions over five years substantially exceed London's 12-15% forecast.[1] Capital appreciation potential has shifted decisively away from traditional prime London markets.

Diversified portfolios should rebalance toward regional exposure. UK real estate investment trusts demonstrate significantly better value positioning in regional markets, with lower leverage and greater embedded rental reversion compared to London-heavy portfolios.[3]

For Lenders and Mortgage Providers

Lending criteria should reflect regional divergences in both risk assessment and loan-to-value ratios. Properties in high-growth regional markets may justify more aggressive LTV ratios given positive momentum and affordability factors supporting sustained demand.

Conversely, London properties may warrant more conservative approaches given the extended period of price weakness and uncertain recovery timeline. Stress testing should incorporate region-specific scenarios rather than applying uniform national assumptions.

For Homeowners and Buyers

Regional buyers should act with confidence but not complacency. Strong growth projections support purchase decisions in Scotland, Wales, and Northern England, but individual property selection remains critical. Not all properties in strong markets will perform equally—location, condition, and specific features still determine individual outcomes.

London buyers should focus on long-term value rather than near-term appreciation expectations. Properties purchased in 2026 should be evaluated primarily on use value, location desirability, and long-term structural factors rather than expectations of rapid price growth.

Relocation decisions from London to regional markets should incorporate comprehensive financial analysis. The combination of lower purchase prices, superior rental yields, and stronger growth prospects creates compelling financial cases for many households, but individual circumstances vary significantly.

For Surveyors and Valuation Professionals

Professional development should prioritize regional market expertise. Surveyors who develop deep knowledge of specific regional markets—understanding local planning policies, infrastructure projects, demographic trends, and micro-market dynamics—will deliver superior value to clients navigating these divergent markets.

Continuing professional development should include:

- Regional economic development initiatives and their property market implications

- Infrastructure project timelines and catchment area impacts

- Remote work demographic patterns and location preference shifts

- Regional planning policy changes affecting supply and development potential

- Comparative valuation methodologies for markets experiencing different growth trajectories

Understanding why to choose an RICS chartered building surveyor becomes even more important as market complexity increases and regional expertise becomes a differentiating factor.

Medium-Term Outlook and Surveyor Preparation

The Recovery and Normalization Narrative

Over the next five years, the market is characterized as a recovery-and-normalization story rather than a boom cycle.[1] Modest near-term growth is forecast to be followed by firmer gains as borrowing conditions ease and the structural undersupply of housing reasserts itself.[1]

This gradual recovery trajectory has important implications for valuation practice:

Conservative near-term projections remain appropriate. Despite positive momentum in regional markets, surveyors should avoid extrapolating recent growth rates indefinitely. Market cycles persist, and current regional outperformance may moderate as London eventually stabilizes and recovers.

Structural undersupply supports medium-term confidence. Despite interest rate volatility and affordability constraints limiting short-term price growth, structural housing shortages, demographic demand, and investment inflows support long-term appreciation—particularly in undersupplied northern and midland markets.[1]

Monitoring Key Indicators

Surveyors should track several indicators to adjust regional strategies as market conditions evolve:

📊 Regional transaction volumes indicate demand strength beyond price movements

📊 Time on market metrics reveal buyer urgency and market momentum shifts

📊 Rental market tightness signals underlying housing demand and future price pressure

📊 Planning approval rates affect future supply and medium-term value trajectories

📊 Infrastructure project progress impacts specific corridor and neighborhood valuations

📊 Remote work policy changes at major employers influence location demand patterns

Regular monitoring of these indicators enables surveyors to adjust valuation approaches proactively rather than reactively as market conditions shift.

Conclusion

The Regional Valuation Divergences in 2026: Building Survey Strategies for Scotland, Wales, and Northern England vs London Laggards represent a fundamental restructuring of the UK property market hierarchy. Scotland and Wales are leading with growth rates near 5%, Northern England is forecast for 20-25% cumulative appreciation over five years, while London experiences its sixth consecutive month of annual decline and faces only modest recovery prospects through 2031.[1][4]

For chartered surveyors, these divergences demand sophisticated, region-specific approaches to property valuation and client communication. Traditional London-centric methodologies no longer serve clients well in regional markets experiencing structural outperformance driven by affordability advantages, infrastructure investment, and demographic shifts.

Actionable next steps for surveyors:

- Develop regional specialization in high-growth markets through dedicated market research, local networking, and transaction analysis

- Adjust comparable selection methodologies to account for rapid appreciation in regional markets and apply appropriate time adjustments

- Incorporate rental yield analysis as a valuation cross-check, particularly for investment properties in yield-advantaged regional markets

- Communicate market context transparently to clients in both outperforming and underperforming regions, managing expectations appropriately

- Monitor structural drivers including infrastructure projects, planning policies, and demographic trends that will shape medium-term regional performance

- Invest in continuing professional development focused on regional market dynamics, comparative valuation techniques, and evolving best practices

The surveyors who adapt most effectively to these regional divergences—developing deep market expertise, adjusting methodologies appropriately, and communicating insights clearly to clients—will deliver superior value and build competitive advantages in an increasingly complex and regionally differentiated property market.

The UK property market of 2026 rewards regional expertise over historical assumptions. Surveyors who recognize and respond to this new reality will guide clients to better decisions and more successful outcomes across Scotland, Wales, Northern England, and even within the pockets of opportunity that exist in London's challenging market environment.

References

[1] Uk Real Estate Market 2026 2040 – https://auditconsultinggroup.co.uk/blog/uk-real-estate-market-2026-2040/

[2] Valuation Divergence North Vs South Uk House Prices In 2026 And Surveyor Adjustment Techniques – https://nottinghillsurveyors.com/blog/valuation-divergence-north-vs-south-uk-house-prices-in-2026-and-surveyor-adjustment-techniques

[3] 2026 Global Reits Outlook Regional Divergence And Sector Opportunities – https://www.centersquare.com/insights/2026-global-reits-outlook-regional-divergence-and-sector-opportunities/

[4] Valuation Strategies For The 2026 Uk Housing Recovery Regional Price Divergence And Surveyor Tactics – https://nottinghillsurveyors.com/blog/valuation-strategies-for-the-2026-uk-housing-recovery-regional-price-divergence-and-surveyor-tactics