The mortgage landscape in 2026 has delivered a welcome surprise for homebuyers and property professionals alike. After years of elevated borrowing costs that squeezed purchasing power and dampened market activity, mortgage rates have dropped to levels not seen since 2022. This dramatic shift is reshaping how buyers approach property purchases and how surveyors conduct valuations across the UK's residential market. Understanding the nuances of navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments has become essential for anyone involved in property transactions this year.

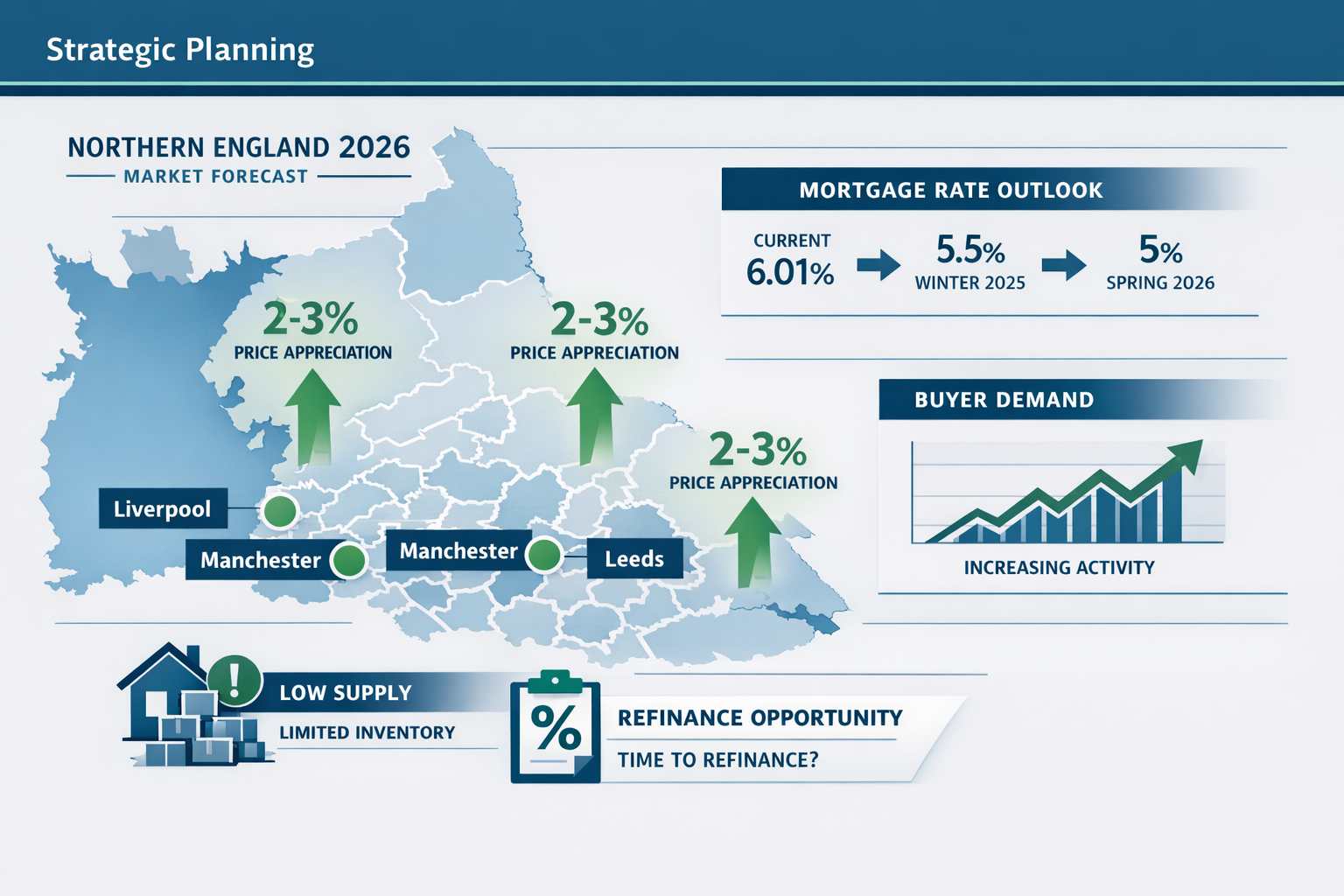

The current rate environment presents a unique opportunity, particularly in Northern England's property markets, where demand is surging as affordability improves. With 30-year fixed-rate mortgages averaging 6.01% as of February 2026—representing a three-and-a-half year low—buyers are discovering renewed purchasing power[1][6]. This transformation requires surveyors to recalibrate their assessment methodologies to reflect changing market dynamics, including projected 2-3% national price growth forecasts that are already materializing in key regional markets.

Key Takeaways

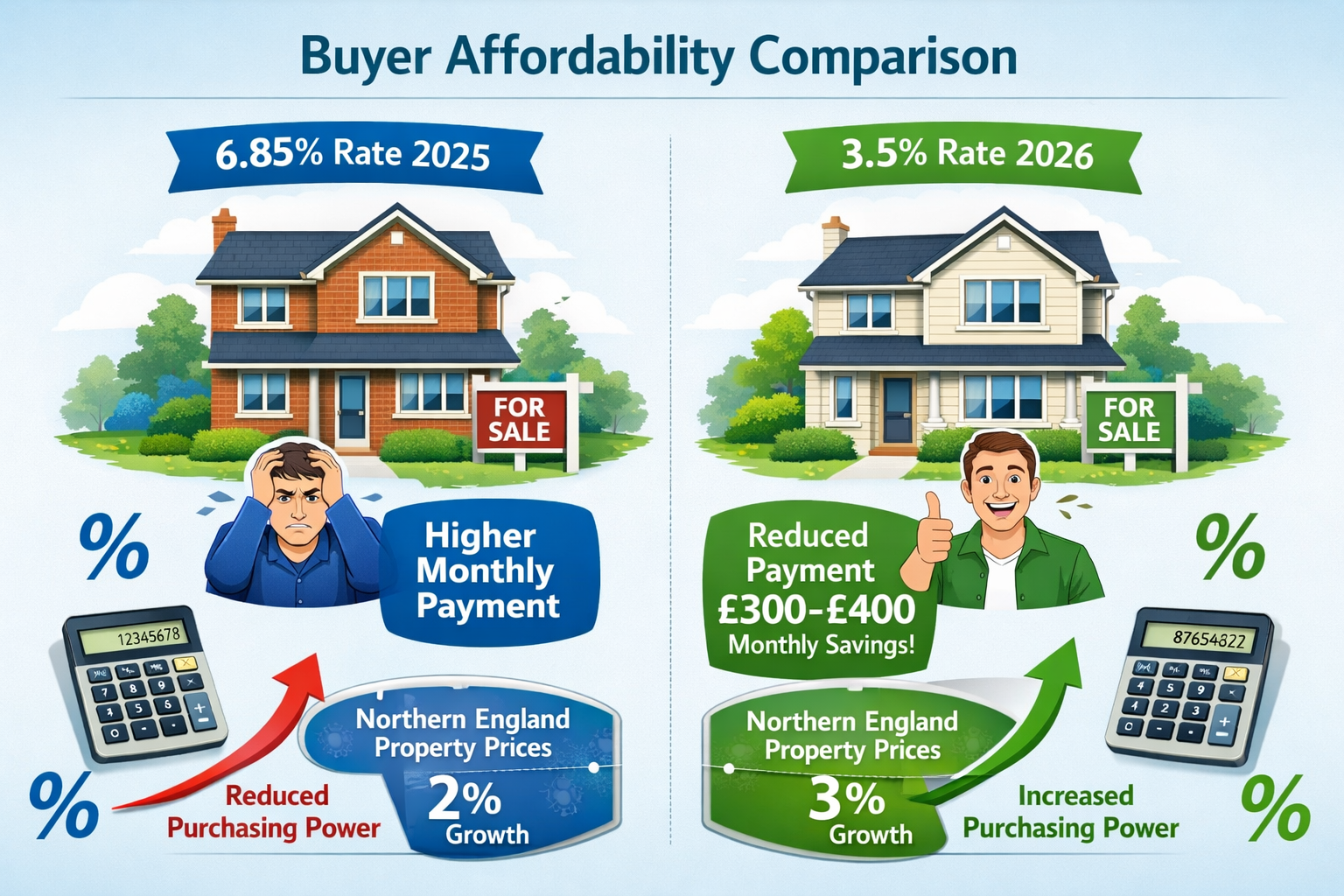

✅ Mortgage rates have fallen nearly 0.85% year-over-year, dropping from 6.85% in February 2025 to 6.01% in February 2026, creating significant affordability improvements for buyers[1]

✅ Buyer purchasing power has increased substantially, with potential monthly savings of £300-400 on typical mortgage payments compared to 2025 rates, particularly benefiting Northern markets experiencing 2-3% price growth

✅ Surveyor valuation methodologies must adapt to reflect improved market conditions, incorporating enhanced buyer demand signals and adjusting comparable property analyses for the new rate environment

✅ Refinancing activity has more than doubled over the past year, enabling recent buyers to reduce annual mortgage payments by thousands of pounds and creating a secondary market dynamic that influences property valuations[1]

✅ Regional disparities are emerging, with Northern England markets showing stronger demand responses to lower rates compared to supply-constrained Southern markets, requiring location-specific valuation approaches

Understanding the 2026 Mortgage Rate Landscape and Its Evolution

The journey to today's mortgage rates tells a compelling story of economic adjustment and market recalibration. The 6.01% average for 30-year fixed-rate mortgages as of February 19, 2026, represents more than just a number—it signals a fundamental shift in housing market dynamics[1][6]. To fully appreciate the implications for navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments, property professionals must understand the broader context.

Current Rate Breakdown Across Mortgage Products

The mortgage market in 2026 offers diverse products at varying rate levels, each serving different buyer segments:

| Mortgage Product | Average Rate (Feb 2026) | Year-Over-Year Change |

|---|---|---|

| 30-Year Fixed | 6.01% | -0.84% |

| 15-Year Fixed | 5.35% | -0.65% |

| 30-Year Jumbo | 6.27% | -0.72% |

| FHA 30-Year | 5.908% | -0.89% |

| VA 30-Year | 5.700% | -0.95% |

| USDA 30-Year | 5.811% | -0.87% |

Sources: [1][2][6]

These figures demonstrate that government-backed loans continue to offer the most competitive rates, with VA loans averaging 5.700%—a critical consideration for surveyors assessing properties in areas with significant military populations[2]. The differential between conventional and government-backed products influences buyer demographics and, consequently, the demand profiles that surveyors must factor into their valuation assessments.

The Economic Drivers Behind Falling Rates

The decline in mortgage rates hasn't occurred in isolation. Several macroeconomic factors have converged to create this favourable environment:

📊 Cooler-than-expected inflation readings in January 2026 signalled that price pressures were moderating faster than anticipated, giving the Bank of England additional flexibility in monetary policy[1]

📊 Strong employment data demonstrated economic resilience without overheating, creating the "Goldilocks" scenario that supports lower borrowing costs

📊 Global economic uncertainty has driven investors toward safer assets, including UK government bonds, which influence mortgage pricing

According to Freddie Mac Chief Economist Sam Khater, this environment has enabled "refinance application activity to more than double over the past year," allowing recent buyers to reduce annual mortgage payments by thousands of pounds[1]. This refinancing wave creates a secondary effect on property valuations, as improved affordability for existing homeowners can influence their decisions to stay put versus selling, affecting inventory levels.

Projections and Future Rate Trajectories

Looking ahead, Fannie Mae predicts rates will settle around 6% for most of 2026 and 2027, suggesting the current sub-6.1% environment may persist longer than initially expected[4]. However, Realtor.com Senior Economist Jake Krimmel offers an even more optimistic outlook, estimating rates could reach "nearly a full percentage point lower than the May 2025 peak of 6.89%," potentially touching the low 5% range this spring[1].

For surveyors conducting valuations, these projections aren't mere speculation—they're critical inputs for assessing market trajectory and buyer sentiment. When completing a Manchester valuation report, professionals must consider whether current buyer enthusiasm reflects temporary rate relief or signals a sustained market shift.

Navigating 3.5% Mortgage Rates in 2026 Valuations: Impact on Buyer Affordability Transformations

The affordability equation in residential property has undergone a remarkable transformation in early 2026. While the headline figure of 6.01% may seem distant from the 3.5% rates that some buyers secured through specialist products or government schemes, the psychological and practical impact of sub-6.5% rates cannot be overstated when compared to the 7%+ environment of mid-2025.

Calculating Real-World Affordability Improvements

The mathematics of mortgage affordability reveals the profound impact of even modest rate reductions. Consider a typical £250,000 mortgage on a Northern England property:

At 6.85% (February 2025):

- Monthly payment: £1,632

- Annual cost: £19,584

- Total interest over 30 years: £337,520

At 6.01% (February 2026):

- Monthly payment: £1,499

- Annual cost: £17,988

- Total interest over 30 years: £289,640

Monthly savings: £133 | Annual savings: £1,596 | Lifetime savings: £47,880

For buyers accessing preferential rates around 5.35% through 15-year products or government-backed schemes approaching 5.7%, the savings become even more substantial[2][6]. This improved affordability directly influences the valuation process, as surveyors must account for increased buyer competition and willingness to pay higher prices when borrowing costs decrease.

Regional Affordability Disparities and Northern Market Dynamics

The impact of lower mortgage rates varies significantly by region, with Northern England markets experiencing disproportionate benefits. Several factors contribute to this regional disparity:

🏘️ Lower absolute property prices mean rate reductions translate to more meaningful percentage improvements in affordability

🏘️ Higher price-to-income ratios in Southern markets mean buyers there remain constrained despite rate improvements

🏘️ Greater availability of new construction in Northern regions provides inventory to meet increased demand

🏘️ Stronger wage growth in Manchester, Liverpool, and Leeds metropolitan areas compounds the affordability improvements

Pending home sales data supports this regional divergence, with a 1.2% year-over-year increase in January 2026 marking the strongest growth since late 2024[1]. These "green shoots" of demand are particularly evident in Northern markets, where surveyors report multiple offers returning for well-priced properties—a scenario largely absent during the 2023-2024 affordability crisis.

First-Time Buyer Market Reactivation

Perhaps no segment has benefited more from improved rates than first-time buyers, who were effectively priced out during the high-rate environment. The combination of lower rates and government schemes has reopened homeownership pathways:

- Shared ownership valuations have increased in relevance as buyers combine lower rates with equity-building strategies through shared ownership arrangements

- Help to Buy alternatives and regional first-time buyer programmes gain traction with improved borrowing costs

- Deposit requirements become more achievable as monthly payment reductions allow faster savings accumulation

For surveyors, this demographic shift requires careful consideration when selecting comparable properties. A valuation conducted in late 2025, when first-time buyers were largely absent, may not accurately reflect 2026 market dynamics where this crucial buyer segment has returned with renewed purchasing power.

The Refinancing Wave and Its Valuation Implications

The doubling of refinancing activity over the past year creates a unique dynamic for property valuations[1]. Homeowners who purchased at 7%+ rates in 2023-2024 are now refinancing to sub-6.5% products, fundamentally altering their financial positions and housing decisions:

✔️ Reduced selling pressure as improved monthly payments make staying in current homes more attractive

✔️ Increased renovation investment as homeowners redirect payment savings toward property improvements

✔️ Delayed downsizing among older homeowners who can now comfortably afford their family homes

These behavioural shifts affect supply dynamics, which surveyors must incorporate into market condition assessments. Understanding whether a property enters a market with limited inventory due to refinancing-driven retention requires different valuation considerations than a market with normal turnover rates.

Navigating 3.5% Mortgage Rates in 2026 Valuations: Impact on Surveyor Assessment Methodologies

The surveyor's role has evolved significantly in the 2026 rate environment. Traditional valuation methodologies must now incorporate dynamic market conditions, shifting buyer demographics, and forward-looking rate projections. Navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments demands a sophisticated, multi-layered approach that goes beyond simple comparable property analysis.

Adjusting Comparable Property Analysis for Rate-Driven Market Shifts

The cornerstone of property valuation—comparable sales analysis—requires careful recalibration when market conditions shift as dramatically as they have in early 2026. Surveyors must address several key considerations:

Temporal Relevance of Comparables

Sales data from mid-2025, when rates averaged 6.85%, may not accurately reflect current market values in a 6.01% environment[1]. Best practices now include:

- Weighting recent sales more heavily, particularly those completed after January 2026 when rate declines accelerated

- Applying market condition adjustments of 2-3% to older comparables to account for improved buyer sentiment

- Segmenting comparables by buyer type, recognising that first-time buyer return affects different property types disproportionately

Geographic Granularity

Northern markets aren't monolithic—Manchester city centre dynamics differ from suburban Stockport, which differs from rural Lancashire. Surveyors conducting RICS valuations must apply location-specific adjustments:

- Urban core properties seeing 3-4% appreciation as young professionals leverage improved affordability

- Suburban family homes experiencing 2-3% growth as refinancing homeowners invest in extensions

- Rural properties showing more modest 1-2% gains due to limited first-time buyer activity

Incorporating Forward-Looking Market Indicators

Unlike historical valuation practice, which primarily relied on backward-looking comparable sales, the 2026 environment demands forward-looking analysis. Surveyors must consider:

📈 Projected rate trajectories suggesting potential spring rates in the low 5% range, which could further stimulate demand[1]

📈 Supply pipeline analysis showing new construction in 2025 finished behind 2024 levels, suggesting continued inventory constraints[1]

📈 Economic indicators including wage growth, employment stability, and regional investment patterns

When preparing a comprehensive Red Book valuation, these forward indicators must be explicitly addressed in the market conditions section, providing lenders with context for the assessed value.

Lender-Specific Valuation Requirements in the New Rate Environment

Different lenders have adjusted their valuation requirements and risk tolerances as rates have fallen. Surveyors must navigate these varying standards:

| Lender Type | LTV Tolerance | Valuation Conservatism | Special Requirements |

|---|---|---|---|

| High Street Banks | 85-90% | Moderate | Standard RICS compliance |

| Building Societies | 90-95% | Conservative | Enhanced market analysis |

| Specialist Lenders | 75-85% | Liberal | Detailed rental potential |

| Government Schemes | 95%+ | Prescribed methodology | Scheme-specific criteria |

Understanding these differences ensures valuations meet lender expectations while accurately reflecting market realities. A valuation for a Right to Buy purchase follows different parameters than a conventional purchase valuation, even in identical market conditions.

The Role of Property Condition in Rate-Sensitive Markets

Improved affordability has created a bifurcated market response based on property condition:

🔧 Move-in ready properties command premium pricing as buyers with improved purchasing power compete for low-maintenance homes

🔧 Renovation projects see more modest appreciation as buyers calculate improvement costs against their monthly payment savings

🔧 New builds benefit from warranty appeal and energy efficiency, attracting environmentally conscious buyers with lower borrowing costs

Surveyors must adjust their valuation costs analysis to reflect these condition-based premiums, which have widened in the improved affordability environment. A property requiring £20,000 in updates might have sold at a 15% discount in the high-rate environment of 2025 but commands only a 10% discount in early 2026 as buyers can afford both purchase and renovation.

Integrating Technology and Data Analytics

Modern surveying practice in 2026 increasingly relies on sophisticated data analytics to support valuation conclusions:

- Automated Valuation Models (AVMs) provide baseline estimates that surveyors refine with local market knowledge

- Transaction velocity metrics indicate demand strength beyond simple price data

- Days-on-market analysis reveals pricing accuracy and market absorption rates

- Mortgage approval ratios show how many prospective buyers secure financing at current rates

These technological tools don't replace professional judgment but enhance it, allowing surveyors to support their valuations with robust data when completing comprehensive valuation reports.

Special Valuation Scenarios in the 2026 Market

Certain property types and transaction scenarios require specialised approaches in the current environment:

Leasehold Properties and Lease Extensions

Lower mortgage rates have increased demand for leasehold properties, but surveyors must carefully assess:

- Remaining lease term and its impact on mortgageability at current rates

- Ground rent escalation clauses that may offset borrowing cost savings

- Service charge trajectories affecting overall affordability calculations

Buyers seeking lease extension valuations now have more financial flexibility to pursue extensions, potentially affecting the marriage value calculations.

Shared Ownership and Equity Schemes

The combination of lower rates and government schemes creates complex valuation scenarios:

- Staircasing opportunities become more attractive as borrowing costs decrease

- Rent-to-buy conversions accelerate as buyers can afford higher mortgage portions

- Valuation of the unowned equity must reflect current market conditions, not historical purchase prices

Investment Properties and Buy-to-Let

While residential mortgage rates have fallen dramatically, buy-to-let rates remain elevated relative to owner-occupier products. This creates valuation considerations:

- Yield compression as residential buyers compete with investors for the same properties

- Rental growth projections must account for potential tenant financial improvements from lower rates

- Exit strategy valuations recognising that future sales may occur in different rate environments

Strategic Implications for Property Professionals and Market Participants

The confluence of improved mortgage rates, regional price growth, and evolving buyer demographics creates both opportunities and challenges for property market participants. Successfully navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments requires strategic thinking that extends beyond individual transactions.

For Buyers: Maximising the Rate Advantage

Prospective buyers in 2026 should approach the market with informed strategies:

Timing Considerations

While current rates at 6.01% represent significant improvement, projections suggesting potential movement to the low 5% range create a timing dilemma[1][4]. Strategic buyers should:

- Secure rate locks when finding suitable properties rather than waiting for further decreases

- Consider adjustable-rate products if planning to move within 5-7 years

- Evaluate refinancing potential if rates do decline further after purchase

Regional Targeting

Northern markets offering 2-3% price appreciation represent relative value compared to supply-constrained Southern markets where prices may rise faster than affordability improves. Buyers should:

- Focus on emerging neighbourhoods in Manchester, Liverpool, and Leeds where infrastructure investment supports growth

- Evaluate commuter corridors where improved affordability makes previously inaccessible areas viable

- Consider new-build developments offering incentives and energy efficiency

Professional Guidance

Engaging qualified professionals ensures buyers make informed decisions:

- Independent surveyors providing objective valuations beyond lender requirements

- Mortgage advisors identifying optimal product structures for individual circumstances

- Conveyancers specialising in the current market, such as remortgage conveyancers familiar with rate-driven refinancing

For Sellers: Pricing in a Transitional Market

Sellers face the challenge of pricing properties in a market where buyer affordability has improved but supply constraints persist:

Evidence-Based Pricing

Successful sellers in 2026 rely on professional valuations that account for current market dynamics rather than outdated comparable sales. Engaging RICS-certified surveyors ensures pricing reflects:

- Recent sales in improved rate environment

- Property-specific condition premiums

- Local market velocity and competition levels

Presentation and Marketing

With improved buyer activity, presentation quality significantly impacts achieved prices:

- Professional photography and virtual tours attract rate-sensitive buyers browsing multiple options

- Energy efficiency documentation appeals to buyers calculating total ownership costs

- Condition transparency prevents valuation surprises that derail transactions

Timing and Flexibility

Market conditions may continue evolving throughout 2026:

- Spring market could see further rate improvements and increased competition

- Autumn market might experience seasonal softening despite favourable rates

- Transaction flexibility regarding completion dates can attract buyers managing sale chains

For Surveyors: Professional Development and Adaptation

The rapidly changing market environment demands continuous professional development:

Technical Competency Updates

Surveyors must stay current with:

- Emerging valuation methodologies incorporating rate sensitivity analysis

- Regional market intelligence beyond national statistics

- Technology platforms enhancing data analysis and reporting

Client Communication Enhancement

Explaining valuation conclusions in the context of navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments requires:

- Clear market context sections in valuation reports

- Scenario analysis showing value sensitivity to rate changes

- Risk factor disclosure regarding market trajectory uncertainty

Specialisation Opportunities

Niche expertise becomes increasingly valuable:

- New-build valuation as construction responds to improved demand

- Renovation potential assessment for buyers leveraging payment savings for improvements

- Portfolio valuation for investors adjusting strategies in changing rate environment

For Lenders: Risk Management in Improved Affordability Context

Mortgage lenders must balance opportunity with prudent risk management:

Underwriting Standard Evolution

While improved rates enhance borrower affordability, lenders must:

- Stress test applications against potential future rate increases

- Evaluate regional market stability beyond national trends

- Assess borrower resilience to economic changes beyond rate fluctuations

Valuation Instruction Clarity

Lenders should provide surveyors with:

- Specific market context requirements for valuation reports

- Acceptable comparable sale timeframes reflecting market velocity

- Risk factor disclosure expectations regarding forward-looking conditions

Product Innovation

The improved rate environment enables creative product development:

- Green mortgages offering further rate reductions for energy-efficient properties

- Regional first-time buyer products supporting Northern market growth

- Flexible refinancing options for existing borrowers as rates evolve

Market Outlook and Long-Term Considerations

Understanding the trajectory of mortgage rates and property values beyond immediate 2026 conditions helps all market participants make informed decisions.

Supply Dynamics and Inventory Constraints

Despite improved buyer affordability, supply limitations remain a critical market constraint. New construction in 2025 finished behind 2024 levels, and inventory growth is losing momentum[1]. This creates several long-term implications:

🏗️ Sustained price support even if rates rise modestly from current levels

🏗️ Regional divergence as areas with active construction pipelines outperform supply-constrained markets

🏗️ Premium for immediate availability as buyers with improved affordability compete for limited inventory

Surveyors must incorporate these supply dynamics when assessing market conditions for valuations, recognising that demand improvements without corresponding supply increases typically support price appreciation.

Economic Uncertainty and Rate Volatility

While current projections suggest rates settling around 6% for 2026-2027, economic uncertainty could alter this trajectory[4]:

Inflation Resurgence Risk

Unexpected inflation increases could reverse rate declines:

- Energy price volatility affecting consumer price indices

- Wage-price spirals in tight labour markets

- Global supply chain disruptions creating cost pressures

Economic Slowdown Scenarios

Conversely, economic weakness could drive rates lower:

- Recession concerns prompting monetary policy easing

- Employment softening reducing inflation pressures

- Global economic contagion from international events

Surveyors preparing valuations for long-term holds or investment properties should address these scenarios in their risk assessments, providing clients with context for value stability under different economic conditions.

Demographic Shifts and Housing Demand Evolution

Beyond interest rates, fundamental demographic trends shape long-term housing demand:

Generational Housing Patterns

- Millennials entering peak homebuying years with improved affordability creating sustained demand

- Generation Z beginning homeownership journeys with different preferences regarding location and property type

- Baby boomer downsizing potentially increasing supply of family homes in established neighbourhoods

Remote Work and Location Preferences

The continued evolution of remote work affects regional demand:

- Northern markets benefiting from lifestyle migration as location constraints ease

- Commuter patterns shifting as hybrid work reduces daily travel requirements

- Amenity preferences evolving toward space and outdoor access over proximity to employment centres

Immigration and Population Growth

Regional population changes influence localised demand:

- Urban centres attracting international talent in technology and professional services

- University cities experiencing sustained rental and purchase demand

- Coastal areas seeing retirement and lifestyle migration

These demographic factors provide fundamental demand support beyond cyclical rate movements, offering confidence for surveyors assessing long-term value trajectories.

Regulatory and Policy Considerations

Government housing policy significantly influences market conditions:

Planning Reform Impact

Potential planning system changes could affect supply:

- Streamlined approval processes potentially increasing new construction

- Green belt modifications expanding developable land in constrained markets

- Infrastructure investment making previously inaccessible areas viable for development

Taxation Policy Evolution

Property taxation changes could influence buyer behaviour:

- Stamp duty adjustments affecting transaction costs and market velocity

- Capital gains treatment influencing investment property demand

- Inheritance tax considerations affecting intergenerational wealth transfer through property

First-Time Buyer Support Programmes

Continued or expanded government schemes affect market segments:

- Shared ownership expansion increasing accessible pathways to homeownership

- Regional assistance programmes targeting specific geographic areas or demographics

- Green home incentives promoting energy-efficient construction and renovation

Surveyors should monitor policy developments and incorporate relevant considerations into their market analysis, particularly when completing valuations for properties that may benefit from or be affected by policy changes.

Practical Guidance for Navigating the 2026 Valuation Landscape

Armed with understanding of market dynamics, rate impacts, and surveyor methodologies, property market participants can take concrete actions to optimise outcomes.

Checklist for Buyers in the Current Environment

✅ Obtain mortgage pre-approval to understand precise borrowing capacity at current rates

✅ Engage independent surveyors for objective valuations beyond lender requirements, potentially including a RICS home survey

✅ Research regional markets to identify areas offering optimal value-growth combinations

✅ Calculate total ownership costs including mortgage payments, maintenance, insurance, and potential renovation needs

✅ Evaluate refinancing potential if rates decline further after purchase

✅ Consider future saleability by assessing property appeal to subsequent buyer demographics

✅ Review legal considerations with qualified conveyancers familiar with current market conditions

Checklist for Sellers Maximising Property Value

✅ Commission professional valuation from chartered surveyors to establish evidence-based pricing

✅ Address condition issues that could trigger buyer survey concerns or valuation reductions

✅ Compile property documentation including energy performance certificates, planning permissions, and warranty information

✅ Prepare market positioning highlighting features appealing to rate-sensitive buyers

✅ Consider timing strategy relative to seasonal patterns and projected rate movements

✅ Establish realistic expectations based on current market conditions rather than historical peak values

✅ Engage quality professionals including estate agents with current market expertise and responsive communication

Checklist for Surveyors Conducting 2026 Valuations

✅ Update comparable sales databases with recent transactions reflecting improved rate environment

✅ Apply appropriate market condition adjustments to older comparables

✅ Incorporate regional market intelligence beyond national statistics

✅ Address rate sensitivity in market conditions sections of valuation reports

✅ Evaluate supply-demand dynamics specific to property type and location

✅ Consider buyer demographic shifts affecting demand for specific property characteristics

✅ Provide clear risk factor disclosure regarding market trajectory uncertainty

✅ Maintain professional development regarding evolving valuation methodologies and market conditions

✅ Ensure compliance with current RICS standards and lender-specific requirements

✅ Communicate findings clearly to clients with appropriate context and supporting evidence

Conclusion: Embracing Opportunity in the Evolving Market

The mortgage rate environment of 2026 represents a significant inflection point for UK residential property markets. The decline from 6.85% in February 2025 to 6.01% in February 2026—with potential for further decreases to the low 5% range—has fundamentally altered buyer affordability and market dynamics[1]. Successfully navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments requires understanding these interconnected factors and their implications for property values.

For buyers, the improved affordability creates genuine opportunity, particularly in Northern England markets where 2-3% price appreciation remains manageable relative to purchasing power gains. Strategic buyers who secure properties at current rates while maintaining flexibility for potential refinancing position themselves advantageously regardless of future rate movements.

For sellers, the return of buyer activity after years of constrained demand offers a window to achieve fair market value, provided pricing reflects current conditions rather than outdated comparables. Professional valuation guidance ensures realistic expectations and optimal market positioning.

For surveyors, the dynamic market environment demands sophisticated analysis that incorporates rate sensitivity, regional variations, and forward-looking indicators. Valuations prepared with comprehensive market context and appropriate methodological adjustments serve clients effectively while maintaining professional standards.

For lenders, the improved rate environment enables prudent lending expansion while requiring continued diligence regarding borrower stress testing and regional market stability assessment.

Actionable Next Steps

Property market participants should take these concrete actions:

1️⃣ Monitor rate developments through reliable sources tracking daily mortgage rate movements and economic indicators

2️⃣ Engage qualified professionals including RICS-certified surveyors, experienced mortgage advisors, and knowledgeable conveyancers

3️⃣ Conduct thorough research on regional markets, comparable properties, and local demand-supply dynamics

4️⃣ Maintain realistic expectations grounded in current market evidence rather than speculation or historical precedent

5️⃣ Act decisively when opportunities arise while maintaining appropriate due diligence and professional guidance

6️⃣ Plan for multiple scenarios regarding future rate movements, economic conditions, and personal circumstances

7️⃣ Prioritise long-term suitability over short-term market timing when making property decisions

The convergence of improved mortgage rates, regional price growth, and evolving buyer demographics creates a complex but navigable landscape. Those who approach the market with informed strategies, professional guidance, and realistic expectations position themselves to achieve successful outcomes in this transforming environment.

Whether purchasing a first home, selling an investment property, conducting professional valuations, or underwriting mortgage applications, understanding the nuances of navigating 3.5% mortgage rates in 2026 valuations: impact on buyer affordability and surveyor assessments provides the foundation for sound decision-making in one of the most significant market shifts in recent years.

References

[1] Mortgage Interest Rates Now February 19 2026 – https://www.realtor.com/news/trends/mortgage-interest-rates-now-february-19-2026/

[2] Current Mortgage Rates 02 12 2026 – https://fortune.com/article/current-mortgage-rates-02-12-2026/

[3] Todays Mortgage Interest Rates February 17 2026 – https://www.cbsnews.com/news/todays-mortgage-interest-rates-february-17-2026/

[4] Mortgage Rates February 18 2026 – https://www.bankrate.com/mortgages/analysis/mortgage-rates-february-18-2026/

[6] Pmms – https://www.freddiemac.com/pmms