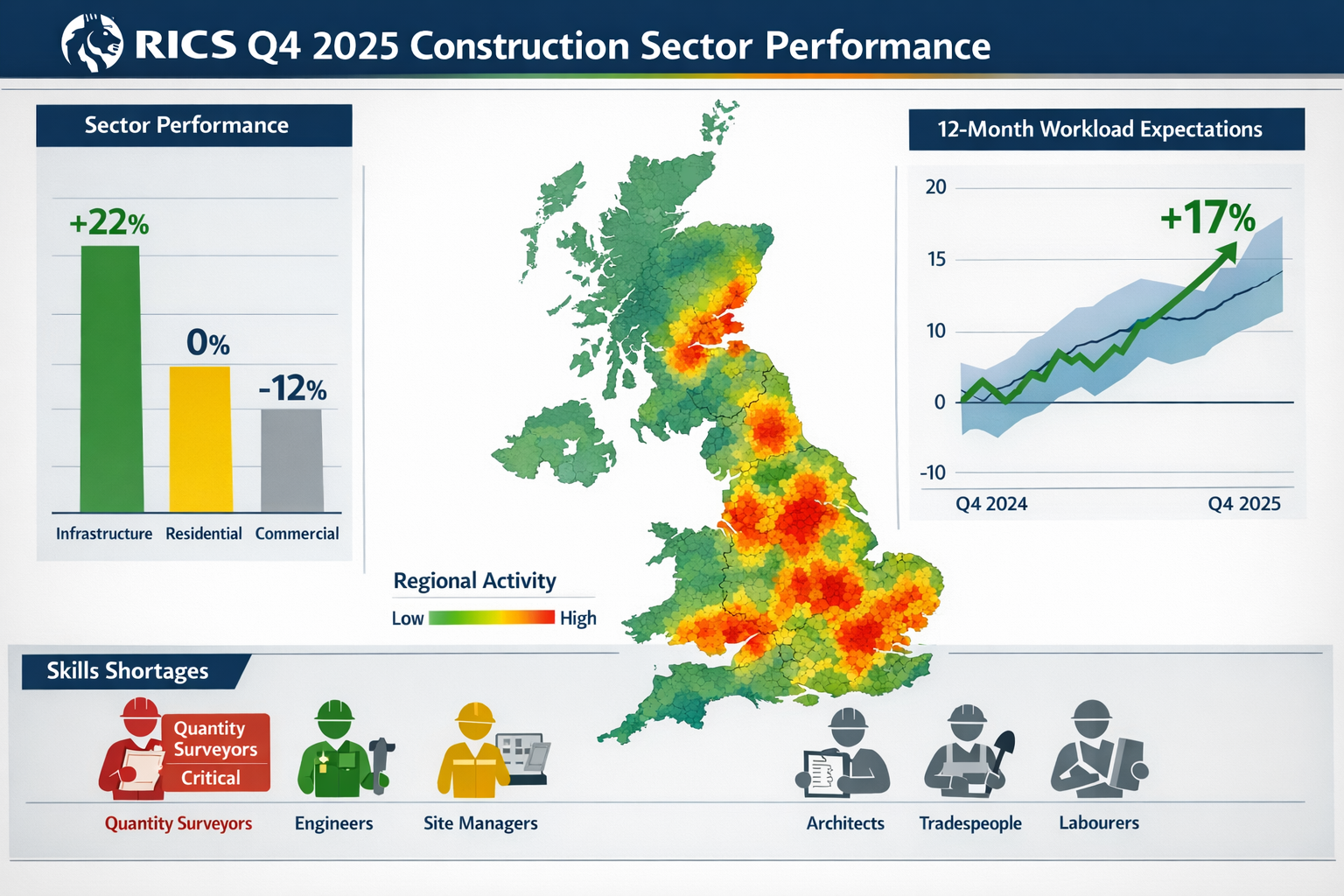

The UK construction industry closed 2025 on a cautious note, with activity remaining broadly flat throughout Q4. Yet beneath this subdued surface, forward-looking indicators from the RICS Q4 2025 Construction Monitor reveal a landscape of emerging opportunities and persistent challenges that will shape building surveys and defect assessment protocols throughout 2026. For chartered surveyors navigating this transitional period, understanding these indicators isn't just about market intelligence—it's about adapting professional methodologies to deliver value in an environment where project volumes remain constrained but expectations for quality and productivity are rising sharply.

As we examine Building Surveys in Subdued Construction Recovery: Forward Indicators from RICS Q4 2025 Monitor for 2026, the data presents a complex picture. While current activity levels disappointed, twelve-month workload expectations jumped to +17%, signaling cautious optimism among industry professionals.[4] This disconnect between present reality and future outlook creates unique challenges for building surveyors, particularly in defect assessment protocols where thoroughness cannot be compromised despite reduced project volumes and ongoing cost pressures.

Key Takeaways

- 📊 UK construction activity remained flat in Q4 2025, but forward workload expectations reached +17%, indicating modest recovery prospects for 2026

- 🏗️ Infrastructure leads sector performance, particularly energy generation and water projects, creating specialized survey demands

- 👷 Critical skills shortages persist, with Quantity Surveyors identified as particularly scarce, impacting project delivery timelines

- 📈 Productivity expectations show significant optimism bias, with a 16-percentage-point gap between reported (+18%) and expected (+34%) improvements

- 🔍 Defect assessment protocols must adapt to low-volume project environments while maintaining rigorous quality standards

Understanding the RICS Q4 2025 Monitor: Current State of UK Construction

The RICS Construction and Infrastructure Market Survey for Q4 2025 provides the most comprehensive snapshot of industry sentiment and activity levels across the United Kingdom. The data reveals an industry in transition—neither growing nor contracting significantly, but poised at an inflection point that will define 2026 outcomes.

Flat Activity Masks Sectoral Divergence

UK construction activity remained broadly flat throughout Q4 2025, representing a continuation of subdued conditions that characterized much of the year.[4] However, this headline figure conceals significant sectoral variation that building surveyors must understand when planning defect assessment approaches and resource allocation.

Infrastructure emerged as the clear outperformer, maintaining positive momentum while other sectors struggled. Within infrastructure, energy generation and distribution projects showed particularly pronounced increases, alongside notable growth in water sector activity.[2] This sectoral strength creates specific demands for RICS commercial building surveys with specialized knowledge of infrastructure-related defects and compliance requirements.

Conversely, residential and commercial sectors remained subdued, with activity levels failing to generate meaningful momentum. For surveyors conducting RICS home surveys, this translates to fewer instructions but potentially more complex assessments as clients seek maximum value from each survey investment.

Regional Performance Variations

Scotland demonstrated particularly interesting dynamics in Q4 2025. The proportion of respondents expecting workloads to rise over the next twelve months reached 24% net balance—a substantial improvement from 12% in Q3 2025.[2] This regional optimism, while encouraging, must be balanced against persistent challenges in profit margins, which remained negative at -6% net balance (improved from -10% in Q3).

For building surveyors operating across UK regions, these variations demand flexible approaches to defect assessment protocols. A chartered building surveyor in Manchester may face different project types and client expectations compared to colleagues in Scotland or the South East, requiring adaptable methodologies while maintaining consistent professional standards.

Forward Indicators from RICS Q4 2025: What Building Surveys Reveal About 2026 Recovery

While current activity levels remained muted, forward-looking indicators from the RICS Q4 2025 Monitor paint a more optimistic picture for 2026. Understanding these indicators helps building surveyors anticipate workload patterns, adjust defect assessment protocols, and position their practices for the modest recovery ahead.

Twelve-Month Workload Expectations Signal Cautious Optimism

The most significant forward indicator from Q4 2025 was the jump in twelve-month workload expectations to +17%.[4] This represents a meaningful improvement in sentiment and suggests that industry participants anticipate conditions will improve through 2026, even if the recovery remains modest rather than robust.

For building surveyors, this forward indicator has several practical implications:

- Increased survey volumes expected in H2 2026, requiring capacity planning and potential recruitment

- Greater emphasis on efficiency as clients seek value while budgets remain constrained

- Enhanced focus on defect prioritization to deliver actionable insights within compressed timelines

- Need for specialized expertise particularly in infrastructure-related assessments

This optimism, however, must be tempered with realism. The construction industry has historically demonstrated optimism bias in forward projections, and the RICS data itself reveals significant gaps between expectations and delivery, particularly around productivity improvements.[3]

Infrastructure Investment Drives Specialized Survey Demand

Infrastructure's position as the strongest performing sector creates specific opportunities and challenges for building surveyors in 2026.[2] Energy generation, distribution networks, and water infrastructure projects require specialized defect assessment protocols that differ significantly from traditional residential or commercial surveys.

Key considerations for infrastructure-related building surveys include:

- Regulatory compliance complexity: Energy and water projects face stringent regulatory frameworks requiring detailed documentation

- Specialized defect categories: Infrastructure-specific issues like thermal bridging in energy facilities or water ingress in treatment plants

- Longer-term performance monitoring: Infrastructure assets require monitoring surveys extending beyond initial completion

- Environmental and sustainability factors: Enhanced focus on energy efficiency and environmental impact assessments

Surveyors positioning themselves for 2026 recovery should consider developing expertise in these specialized areas, potentially through additional training or partnerships with infrastructure specialists.

Planning and Building Safety Challenges Persist

Despite improved forward expectations, respondents to the RICS Q4 2025 Monitor continued highlighting planning and building safety regime challenges as significant obstacles to workload acceleration.[2] These persistent issues directly impact building survey protocols and defect assessment methodologies.

The building safety regime, substantially reformed following the Grenfell Tower tragedy, continues to evolve with implications for surveyors:

- Enhanced scrutiny of fire safety measures requiring detailed assessment of compartmentation, fire stopping, and means of escape

- Increased documentation requirements for defect reporting and remediation tracking

- Greater liability considerations demanding comprehensive professional indemnity coverage

- Extended assessment timelines as thorough evaluation of safety-critical elements becomes non-negotiable

Building surveyors must integrate these considerations into standard defect assessment protocols, ensuring RICS building surveys meet evolving regulatory expectations while remaining commercially viable in a cost-conscious market.

Defect Assessment Protocols for Surveyors in Low-Volume Project Environments

The subdued construction activity of Q4 2025 and modest recovery expectations for 2026 create a unique operating environment for building surveyors. Lower project volumes don't reduce the need for rigorous defect assessment—if anything, they increase pressure to deliver exceptional value on every instruction. This section outlines adapted protocols that maintain professional standards while acknowledging market realities.

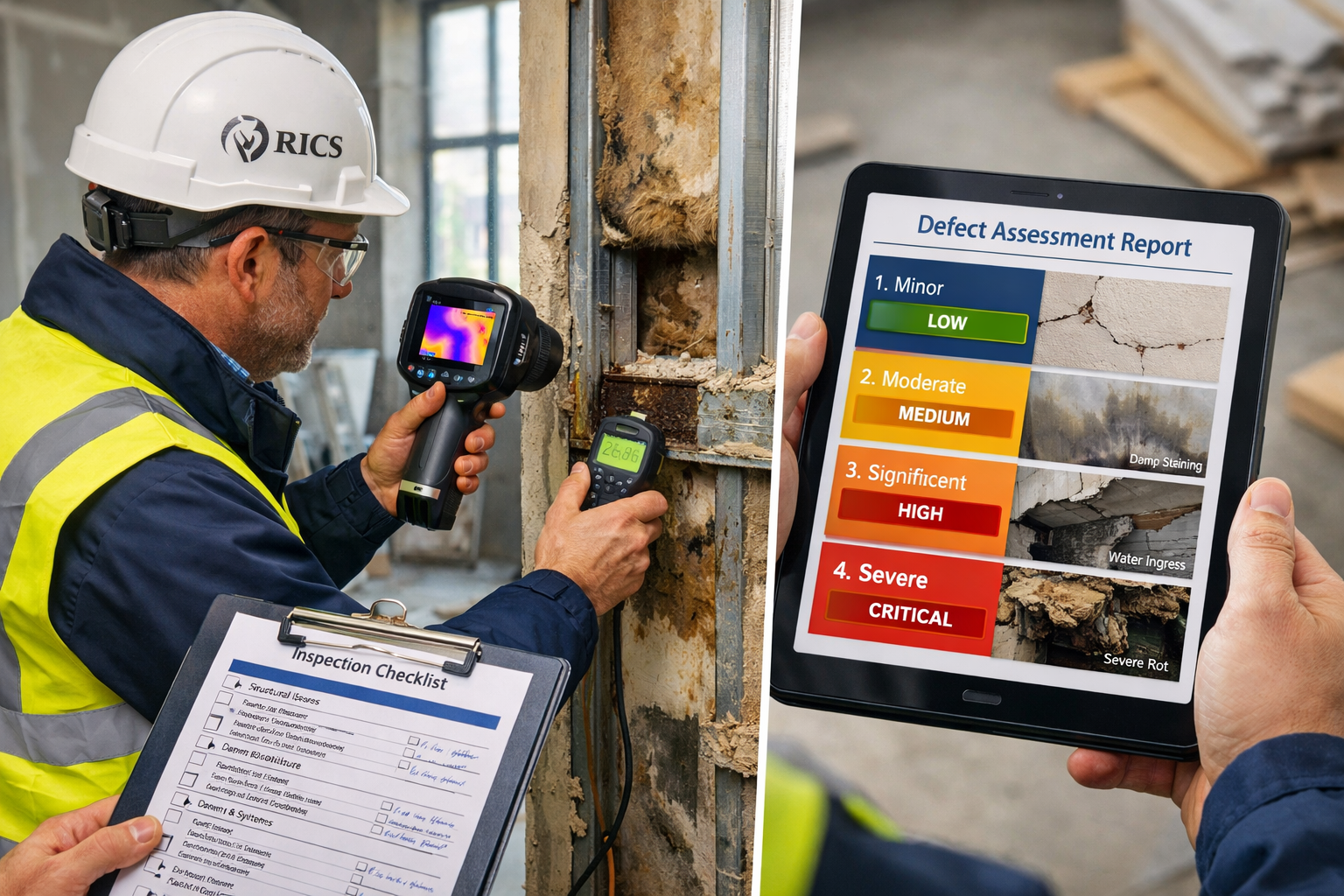

Systematic Defect Categorization in Resource-Constrained Settings

In low-volume environments, efficient defect categorization becomes critical. Surveyors cannot afford to spend excessive time on minor issues while missing critical defects that could impact client decisions. A structured approach helps maintain quality while managing time effectively.

Recommended defect categorization framework:

| Category | Definition | Response Protocol | Documentation Level |

|---|---|---|---|

| Critical | Immediate safety risk or structural integrity concern | Urgent notification, detailed photography, specialist referral | Comprehensive with measurements, multiple images, specialist recommendations |

| Significant | Major defects affecting functionality or requiring substantial repair | Detailed assessment, cost implications, remediation timeline | Detailed with cost estimates, repair specifications |

| Moderate | Defects requiring attention but not immediately critical | Standard documentation, maintenance recommendations | Standard photography and description |

| Minor | Cosmetic or maintenance issues with minimal impact | Brief notation, general guidance | Brief description, single image if relevant |

This framework, adapted from RICS guidance, ensures that surveyors allocate time proportionate to defect severity while maintaining comprehensive coverage. In low-volume periods, the temptation to over-elaborate on minor defects should be resisted in favor of thorough analysis of significant issues.

Technology Integration for Enhanced Efficiency

The RICS Construction Productivity Report 2026 reveals that UK construction professionals rate automation relatively low for productivity impact (only 17% high-impact ratings).[3] However, for building surveyors, selective technology adoption can significantly enhance defect assessment efficiency without requiring major capital investment.

High-value technology applications for building surveys:

- 🔍 Thermal imaging cameras: Rapidly identify moisture ingress, insulation deficiencies, and thermal bridging

- 📱 Mobile survey applications: Streamline data capture, photo annotation, and report generation

- 🚁 Drone surveys: Cost-effective roof and elevation inspection, particularly valuable for roof surveys on complex structures

- 📏 Laser measuring devices: Improve accuracy and speed of dimensional surveys

- 💧 Moisture meters: Provide objective data for damp surveys and water ingress assessment

The key is selecting technologies that genuinely enhance efficiency rather than adopting tools for their novelty value. In subdued market conditions, return on investment becomes paramount, and surveyors should prioritize technologies that reduce assessment time while improving diagnostic accuracy.

Quality Control in Reduced Supervision Environments

Lower project volumes often mean reduced supervision and peer review opportunities. Solo practitioners and small firms must implement robust quality control measures to maintain standards when formal oversight is limited.

Essential quality control protocols:

- Standardized checklists: Ensure consistent coverage across all structural surveys regardless of property type

- Photographic standards: Maintain consistent image quality, annotation, and coverage

- Report templates: Use structured formats ensuring all required elements are addressed

- Peer review partnerships: Establish reciprocal review arrangements with fellow practitioners

- Continuing professional development: Maintain technical knowledge through RICS-accredited training

The RICS Construction Productivity Report 2026 identifies upskilling the workforce as the top-rated productivity intervention, with 47% average high-impact ratings across regions.[3] For individual surveyors, this translates to ongoing investment in professional development even during quiet periods—building capability for the recovery ahead.

Client Communication and Expectation Management

In subdued markets, clients often have heightened expectations for survey deliverables while simultaneously seeking cost reductions. Managing these competing pressures requires clear communication and well-defined scope agreements.

Best practices for client engagement:

- Detailed pre-survey briefings: Clarify exactly what the survey will and won't cover

- Transparent pricing structures: Explain how complexity factors affect fees

- Interim findings communication: Alert clients to critical issues before final report delivery

- Actionable recommendations: Provide clear next steps rather than simply listing defects

- Post-survey support: Offer follow-up consultations to discuss findings and remediation priorities

This approach aligns with the broader need for clear productivity measurement and benchmarking identified in the RICS research. The report notes that one in five UK firms never measure productivity, and no single definition commands even 30% adoption.[3] Surveyors who can clearly articulate their value proposition and demonstrate efficiency gains will be better positioned as recovery accelerates.

Skills Shortages and Their Impact on Building Survey Quality Standards

The RICS Q4 2025 Monitor identifies persistent skills and labour shortages as critical factors undermining project delivery, causing delays and cost overruns.[1] For building surveyors, these shortages create both challenges and opportunities as the industry navigates toward 2026 recovery.

The Quantity Surveyor Shortage Crisis

Among the various skills gaps, the shortage of Quantity Surveyors has been identified as particularly critical.[1] While distinct from building surveyors, this shortage has cascading effects across the construction ecosystem that impact defect assessment and project delivery.

Implications for building surveyors:

- Cost estimation challenges: Clients struggle to obtain accurate remediation cost estimates

- Extended project timelines: Delays in cost planning affect survey scheduling and follow-up work

- Increased collaboration demands: Building surveyors may need to provide preliminary cost guidance

- Opportunity for expanded services: Surveyors with cost estimation capabilities can offer enhanced value

This skills shortage environment reinforces the importance of RICS valuations and cost assessment capabilities within building surveying practices. Firms that can offer integrated services—combining defect assessment with cost implications—will differentiate themselves in the 2026 market.

Maintaining Standards Despite Workforce Constraints

The broader construction skills shortage creates pressure to compromise on quality standards or rush assessments to meet deadlines. Building surveyors must resist these pressures while acknowledging legitimate client concerns about timelines and costs.

Strategies for maintaining standards:

- Realistic timeline commitments: Better to quote longer timelines and deliver early than promise unrealistic turnarounds

- Selective instruction acceptance: Decline instructions that cannot be completed to proper standards

- Transparent capacity communication: Keep clients informed about workload and availability

- Associate networks: Develop relationships with qualified associates for capacity overflow

- Specialization focus: Concentrate on survey types where expertise is strongest rather than accepting all work

The RICS Construction Productivity Report 2026 reveals that UK construction productivity grew by +18% net balance over the past twelve months, with forward expectations rising to +34%.[3] This 16-percentage-point gap suggests significant optimism bias, but also indicates industry recognition that productivity improvements are essential for sustainable recovery.

Productivity Measurement and Benchmarking for Building Survey Practices

One of the most striking findings from the RICS Construction Productivity Report 2026 is the lack of consistent productivity measurement across the construction industry. This measurement gap creates both challenges and opportunities for building surveyors seeking to demonstrate value and improve efficiency.

The Productivity Measurement Gap

The RICS research reveals troubling inconsistencies in how construction firms approach productivity:

- One in five UK firms never measure productivity[3]

- No single productivity definition commands even 30% adoption in any region[3]

- Benchmark usage remains critically low at 5-16%[3]

For building surveyors, this measurement gap represents an opportunity to differentiate through transparent performance metrics and continuous improvement processes. Practices that can demonstrate efficiency gains and quality consistency will be better positioned as competition intensifies during 2026 recovery.

Key Performance Indicators for Building Survey Practices

Developing meaningful KPIs for building survey operations requires balancing efficiency metrics with quality indicators. Pure speed measurements risk incentivizing rushed assessments that miss critical defects.

Recommended KPIs for building survey practices:

- Survey completion time by property type: Track average time for comparable properties

- Report turnaround time: Measure from inspection completion to report delivery

- Client satisfaction scores: Systematic feedback collection and analysis

- Defect identification rate: Track significant defects found per survey type

- Repeat instruction rate: Measure client retention and referral frequency

- Professional development hours: Monitor ongoing capability enhancement

- Technology utilization: Track adoption and effective use of efficiency tools

These metrics should be tracked consistently and reviewed quarterly, with year-over-year comparisons providing insight into practice evolution. The goal isn't simply faster surveys, but rather optimized processes that maintain quality while eliminating waste.

Benchmarking Against Industry Standards

The low benchmark usage identified in the RICS research (5-16%) suggests most construction firms operate without external reference points.[3] Building surveyors can gain competitive advantage by actively seeking benchmark data and comparing performance against industry norms.

Benchmarking approaches:

- RICS guidance documents: Compare practices against published professional standards

- Peer practice groups: Establish informal benchmarking networks with non-competing practices

- Professional body surveys: Participate in RICS and other industry surveys to access aggregated data

- Client feedback analysis: Use satisfaction data to identify performance gaps

- Financial benchmarking: Compare fee structures, profit margins, and overhead ratios

Practices that embrace systematic benchmarking will be better equipped to identify improvement opportunities and demonstrate value to clients during the subdued recovery period.

Regional Variations and Local Market Adaptations for 2026

The RICS Q4 2025 Monitor data reveals significant regional variations in construction activity and forward expectations. Building surveyors must adapt defect assessment protocols and business strategies to local market conditions while maintaining consistent professional standards.

Scotland's Improved Outlook

Scotland demonstrated particularly positive forward indicators in Q4 2025, with 24% net balance of respondents expecting workloads to rise over the next year—double the Q3 2025 figure of 12%.[2] This regional optimism creates specific opportunities for surveyors operating in Scottish markets.

However, challenges persist. Profit margin expectations remained negative at -6% net balance in Scotland, though this represents improvement from -10% in Q3.[2] For building surveyors, this suggests increased activity but continued cost pressures requiring efficient operations.

Adaptations for Scottish market conditions:

- Infrastructure focus: Position for energy and water sector opportunities

- Cost-conscious service delivery: Streamline processes without compromising quality

- Local regulatory expertise: Maintain current knowledge of Scottish building standards and regulations

- Partnership development: Build relationships with infrastructure developers and contractors

Regional Specialization Strategies

Different UK regions show varying sector strengths and recovery trajectories. Surveyors can enhance competitiveness by developing regional specializations aligned with local market dynamics.

Regional specialization opportunities:

- London and South East: Commercial redevelopment and residential conversions

- Scotland: Infrastructure and renewable energy projects

- Northern England: Industrial and manufacturing facility assessments

- Wales: Public sector and social housing work

- Midlands: Mixed-use developments and urban regeneration

This regional specialization approach aligns with broader productivity improvement strategies. The RICS Construction Productivity Report 2026 identifies upskilling as the top productivity intervention,[3] and regional specialization represents a form of strategic upskilling that enhances both efficiency and value delivery.

Planning and Regulatory Challenges: Implications for Survey Protocols

The RICS Q4 2025 Monitor consistently identifies planning and building safety regime challenges as significant obstacles to construction activity acceleration.[2] These regulatory complexities directly impact building survey protocols and defect assessment methodologies throughout 2026.

Evolving Building Safety Requirements

The post-Grenfell building safety regime continues to evolve, with implications for how building surveyors approach defect assessment, particularly in multi-occupancy residential buildings and high-rise structures.

Key building safety considerations for 2026:

- Enhanced fire safety assessments: Detailed evaluation of compartmentation, fire doors, and escape routes

- Cladding and external wall systems: Comprehensive assessment of external wall construction and fire performance

- Building safety case compliance: Understanding requirements for higher-risk buildings

- Golden thread documentation: Ensuring survey reports contribute to building information requirements

- Accountability framework awareness: Understanding roles of Principal Designer, Principal Contractor, and Building Safety Manager

Building surveyors conducting commercial building surveys must integrate these considerations into standard protocols, ensuring reports address safety-critical elements with appropriate detail and technical rigor.

Planning System Constraints

Planning delays and constraints continue affecting project viability and timelines. While building surveyors don't directly navigate planning processes, understanding these constraints helps contextualize client needs and project timelines.

Planning-related survey considerations:

- Pre-acquisition due diligence: Enhanced scrutiny of planning compliance and conditions

- Change of use assessments: Detailed evaluation of building suitability for proposed new uses

- Conservation area constraints: Understanding limitations on alterations and extensions

- Listed building considerations: Specialized knowledge of historic building assessment

- Environmental impact factors: Awareness of sustainability and environmental requirements

Surveyors who understand the planning context can provide more valuable advice, helping clients avoid acquisitions with insurmountable planning constraints or identify opportunities where planning approval is likely.

Technology and Innovation in Building Surveys: Preparing for 2026 Recovery

While the RICS Construction Productivity Report 2026 reveals relatively low confidence in automation (17% high-impact ratings in UK),[3] selective technology adoption can significantly enhance building survey efficiency and quality. The key is choosing technologies that address genuine pain points rather than adopting innovations for their novelty value.

High-Impact Technology Investments

Based on current market conditions and forward indicators for 2026, certain technologies offer particularly strong returns for building survey practices:

Thermal imaging technology remains one of the highest-value investments for building surveyors. Modern thermal cameras enable rapid identification of:

- Moisture ingress and water penetration

- Insulation deficiencies and thermal bridging

- Heating system malfunctions

- Air leakage points

- Hidden structural issues

The technology has matured significantly, with professional-grade cameras now available at accessible price points. For practices conducting regular damp surveys or energy efficiency assessments, thermal imaging delivers clear ROI through enhanced diagnostic capability and reduced assessment time.

Drone survey technology offers particular value for roof and elevation inspection, especially on complex or difficult-to-access structures. Benefits include:

- ✅ Enhanced safety by reducing working at height requirements

- ✅ Comprehensive photographic coverage of roof surfaces

- ✅ Detailed elevation inspection without scaffolding or access equipment

- ✅ Rapid data capture reducing on-site time

- ✅ High-resolution imagery for detailed defect analysis

Surveyors offering drone surveys can differentiate their services while improving efficiency and safety outcomes.

Digital Report Delivery and Client Portals

Client expectations for digital service delivery continue rising. Modern building survey practices should implement:

- Cloud-based report delivery: Secure, instant access to completed reports

- Interactive report formats: Clickable floor plans, embedded photographs, and video content

- Mobile-optimized viewing: Reports formatted for smartphone and tablet viewing

- Client portal access: Secure platforms where clients can access all documentation

- Digital communication tools: Efficient channels for queries and follow-up discussions

These digital capabilities align with broader productivity improvement goals while meeting evolving client expectations for service delivery in 2026.

Data Analytics and Trend Identification

Building survey practices accumulating substantial historical data can leverage analytics to identify defect patterns, predict maintenance requirements, and provide enhanced value to clients.

Analytics applications for building surveyors:

- Defect frequency analysis: Identify common issues by property type, age, or location

- Cost trend tracking: Monitor how remediation costs evolve over time

- Seasonal pattern recognition: Understand how weather and seasons affect defect presentation

- Property type benchmarking: Compare individual properties against broader datasets

- Predictive maintenance insights: Anticipate future issues based on historical patterns

While sophisticated analytics require investment in data infrastructure, even basic trend analysis can provide valuable insights that differentiate survey services in competitive markets.

Commercial Considerations: Pricing and Service Models for Subdued Recovery

The modest recovery expectations for 2026, combined with persistent cost pressures indicated by negative profit margins in some regions,[2] create challenging commercial dynamics for building survey practices. Sustainable pricing strategies must balance competitive positioning with profitability requirements.

Value-Based Pricing in Cost-Conscious Markets

Traditional time-based pricing models struggle in subdued markets where clients resist fee increases despite rising costs. Value-based pricing offers an alternative approach that aligns fees with client outcomes rather than surveyor inputs.

Value-based pricing principles:

- Outcome focus: Price based on value delivered rather than time spent

- Risk assessment: Higher fees for surveys where significant issues are likely

- Complexity recognition: Adjust pricing for property type, age, and condition

- Expertise premium: Charge appropriately for specialized knowledge and experience

- Service bundling: Offer packages combining multiple services at attractive rates

This approach requires clear communication about what drives pricing and why certain properties command higher fees. Clients who understand the value proposition are more likely to accept appropriate pricing.

Service Diversification Strategies

Relying solely on traditional building surveys creates vulnerability in subdued markets. Diversification into complementary services can stabilize revenue and enhance client value.

Complementary service opportunities:

- Project management: Oversee remediation work identified in surveys

- Monitoring services: Provide ongoing monitoring surveys for structural issues

- Expert witness services: Provide expert witness testimony in construction disputes

- Specialized assessments: Offer subsidence surveys, asbestos surveys, or other niche services

- Reinstatement valuations: Provide reinstatement cost valuations for insurance purposes

Diversification should build on core competencies rather than stretching into unfamiliar territory. The goal is leveraging existing expertise across broader service offerings.

Client Retention and Relationship Development

In low-volume markets, client retention becomes even more critical than new client acquisition. Building long-term relationships generates repeat instructions and referrals that sustain practices through challenging periods.

Client retention strategies:

- Post-survey follow-up: Proactive contact to discuss findings and next steps

- Annual check-ins: Periodic contact with past clients to maintain relationships

- Educational content: Share relevant market insights and property maintenance guidance

- Loyalty recognition: Preferential pricing or priority scheduling for repeat clients

- Referral incentives: Acknowledge and reward clients who provide referrals

These relationship-building activities require time investment but generate substantial long-term value through improved client lifetime value and reduced marketing costs.

Preparing Your Building Survey Practice for 2026: Action Steps

The forward indicators from the RICS Q4 2025 Monitor suggest modest recovery ahead, but success in 2026 will require proactive preparation rather than passive waiting for improved conditions. Building survey practices should implement specific action steps to position for the year ahead.

Immediate Actions (Q1 2026)

Capability assessment and gap analysis:

- Review current service offerings against anticipated market demand

- Identify skills gaps requiring training or recruitment

- Evaluate technology infrastructure and identify upgrade needs

- Assess capacity constraints and develop expansion plans

Market positioning refinement:

- Clarify target client segments and property types

- Develop specialized expertise in high-growth sectors (infrastructure, energy)

- Update marketing materials to reflect current capabilities

- Strengthen digital presence and online visibility

Operational efficiency improvements:

- Implement systematic productivity measurement

- Standardize processes and documentation

- Adopt high-value technologies (thermal imaging, drones)

- Establish quality control protocols

Medium-Term Actions (H1 2026)

Professional development investment:

- Complete RICS-accredited training in specialized areas

- Develop infrastructure and energy sector expertise

- Enhance understanding of evolving building safety regulations

- Build cost estimation and valuation capabilities

Strategic partnerships:

- Establish relationships with infrastructure developers

- Build referral networks with complementary professionals

- Develop associate arrangements for capacity management

- Join industry groups and professional networks

Service expansion:

- Launch new specialized survey offerings

- Develop monitoring survey capabilities

- Create bundled service packages

- Implement value-added client services

Long-Term Strategic Positioning (2026 and Beyond)

Data and analytics infrastructure:

- Implement systematic data capture and storage

- Develop analytics capabilities for trend identification

- Build historical databases for benchmarking

- Create predictive maintenance models

Thought leadership development:

- Publish insights on market trends and technical topics

- Speak at industry events and conferences

- Contribute to professional publications

- Build reputation as market authority

Business model evolution:

- Transition toward value-based pricing

- Develop recurring revenue streams

- Create scalable service delivery models

- Build practice value for eventual succession or sale

Conclusion: Navigating Building Surveys Through Subdued Recovery

The RICS Q4 2025 Construction Monitor presents a nuanced picture of the UK construction industry—subdued current activity balanced against cautiously optimistic forward indicators for 2026. For building surveyors, this transitional period demands both resilience and adaptability, maintaining rigorous defect assessment protocols while acknowledging market realities of constrained volumes and persistent cost pressures.

The forward indicators are encouraging: twelve-month workload expectations at +17%, infrastructure sector strength, and regional improvements particularly in Scotland all suggest modest recovery ahead.[2][4] However, significant challenges persist—skills shortages, planning constraints, negative profit margins, and productivity measurement gaps that undermine industry efficiency.[1][3]

Building surveyors who will thrive through this subdued recovery period share common characteristics:

✅ Systematic defect assessment protocols that maintain quality regardless of market conditions

✅ Strategic technology adoption focused on genuine efficiency gains rather than novelty

✅ Specialized expertise aligned with high-growth sectors like infrastructure and energy

✅ Transparent productivity measurement demonstrating value and continuous improvement

✅ Flexible service models that adapt to regional variations and client needs

✅ Long-term relationship focus prioritizing client retention over transaction volume

The disconnect between current activity levels and future expectations—what the RICS research identifies as optimism bias—serves as both warning and opportunity. Practices that prepare systematically for recovery while maintaining realistic expectations will be better positioned than those who either ignore forward indicators or over-commit based on optimistic projections.

As we progress through 2026, the construction industry's trajectory will depend significantly on how effectively it addresses persistent challenges: skills shortages, productivity measurement gaps, planning constraints, and building safety compliance. Building surveyors play a critical role in this ecosystem, providing the quality assurance and defect identification that underpins successful project delivery.

The path forward requires balancing competing demands—efficiency without compromising thoroughness, specialization without excessive narrowness, technology adoption without losing professional judgment, and commercial sustainability without sacrificing quality standards. Those who navigate this balance effectively will emerge from the subdued recovery period stronger, more capable, and better positioned for long-term success.

Next Steps for Building Survey Professionals

- Review your current defect assessment protocols against the frameworks outlined in this article

- Identify one high-value technology investment that addresses genuine pain points in your practice

- Develop specialized expertise in infrastructure, energy, or other high-growth sectors

- Implement systematic productivity measurement to track efficiency and demonstrate value

- Strengthen client relationships through proactive communication and value-added services

- Invest in professional development particularly in building safety and regulatory compliance

- Join professional networks to access benchmarking data and market intelligence

The modest recovery ahead won't transform market conditions overnight, but it offers opportunities for well-prepared practices to strengthen their position and build sustainable competitive advantages. By understanding the forward indicators from the RICS Q4 2025 Monitor and adapting accordingly, building surveyors can navigate this transitional period successfully while maintaining the professional standards that define quality RICS building surveys.

References

[1] UK construction activity increase this year, says RICS prediction – https://www.pbctoday.co.uk/news/hr-skills-news/uk-construction-activity-increase-this-year-says-rics-prediction/148101/

[2] Construction Outlook Improves For 2026 After Subdued End To Year – https://www.scottishfinancialnews.com/articles/construction-outlook-improves-for-2026-after-subdued-end-to-year

[3] RICS Construction Productivity Report 2026 – https://www.rics.org/news-insights/rics-construction-productivity-report-2026

[4] RICS Reports UK Construction Activity Remained Subdued In Q4 2025 – https://www.lexisnexis.co.uk/legal/news/rics-reports-uk-construction-activity-remained-subdued-in-q4-2025