New buyer enquiries plummeted to a net balance of -26% in February 2026, marking the sharpest monthly decline in demand since late 2023 and signaling a dramatic shift in market sentiment that few anticipated at the start of the year.[1] This deterioration in confidence, combined with unprecedented regional divergence—London at -40% while the North West shows +3% growth—presents chartered building surveyors with both challenges and strategic opportunities that will define practice performance throughout 2026.

Understanding Building Survey Market Sentiment in Spring 2026: Interpreting RICS Data on Regional Divergence and Surveyor Confidence has become essential for professionals navigating this increasingly fragmented marketplace. The latest Royal Institution of Chartered Surveyors (RICS) data reveals a market characterized by cautious short-term sentiment, persistent regional disparities, and surprisingly resilient longer-term expectations that suggest the current downturn may be temporary rather than structural.

Key Takeaways

- Buyer demand fell sharply to -26% net balance in February 2026, down from -15% in January, reflecting heightened macroeconomic and geopolitical uncertainty

- London faces severe price pressure at -40% net balance, while northern regions like the North West show resilience with up to 3% annual appreciation

- Near-term sentiment weakened significantly, with price expectations dropping to -18%, yet 12-month outlook remains moderately positive at +33%

- Rental market supply shortage intensifies, with landlord instructions at -27% and rent expectations at +20% for the next quarter

- Surveyor workload implications vary dramatically by region, requiring strategic positioning and service adaptation for building survey professionals

Understanding the RICS Residential Market Survey Framework

The RICS UK Residential Market Survey represents the gold standard for property market intelligence, collecting monthly feedback from chartered surveyors across all UK regions. These professionals—operating at the coalface of residential transactions—provide real-time insights into buyer enquiries, agreed sales, price movements, and market sentiment that often precede official statistics by several months.

Net balance figures form the core metric, calculated by subtracting the percentage of respondents reporting declines from those reporting increases. A reading of -26% for buyer demand, for instance, means 26% more surveyors reported falling enquiries than rising ones—a significant negative indicator.

For building surveyors, this data serves multiple strategic purposes:

- Workload forecasting: Demand indicators predict survey instruction volumes 2-3 months ahead

- Regional positioning: Geographic disparities inform expansion or consolidation decisions

- Service mix optimization: Market conditions influence demand for different survey types

- Pricing strategy: Sentiment data helps calibrate fee structures to market conditions

- Client advisory: Understanding trends enhances value-add consultancy to property buyers

The February 2026 survey captured responses during a period of renewed global uncertainty, with geopolitical tensions and inflation concerns tempering the cautious optimism that characterized January.[4]

Building Survey Market Sentiment in Spring 2026: Key Metrics and Trends

Demand Indicators Show Sharp Deterioration

The -26% net balance for new buyer enquiries in February 2026 represents a substantial deterioration from January's -15%, signaling that whatever green shoots emerged early in the year have been quickly trampled by renewed uncertainty.[1] This marks one of the steepest monthly declines recorded outside of major crisis periods.

Several factors contributed to this demand collapse:

🔴 Rising mortgage rates: Lenders increased rates from 4.24% to 4.51% in mid-March as global instability affected funding costs[4]

🔴 Geopolitical tensions: International conflicts, particularly involving Iran, dampened consumer confidence

🔴 Inflation concerns: Persistent price pressures reduced purchasing power and increased caution

🔴 Economic uncertainty: Mixed signals about growth prospects created wait-and-see attitudes

For RICS chartered building surveyors, falling demand typically translates to reduced instruction volumes with a 6-8 week lag, as initial enquiries convert to formal property viewings and then survey bookings.

Transaction Activity Remains Subdued

Agreed sales posted a net balance of -12% in February 2026, indicating that properties progressing to exchange remain below historical norms.[1] While less severe than the demand collapse, this persistent weakness in completions reflects:

- Buyer hesitancy in committing to purchases

- Mortgage offer delays as lenders tighten criteria

- Chain complications as market velocity slows

- Price negotiation extensions as buyers seek concessions

The gap between enquiries (-26%) and agreed sales (-12%) suggests some resilience in the conversion funnel—buyers who remain active are more committed than the broader pool of potential purchasers who have withdrawn from the market entirely.

Price Expectations Deteriorate Significantly

Perhaps the most striking shift in Building Survey Market Sentiment in Spring 2026: Interpreting RICS Data on Regional Divergence and Surveyor Confidence concerns near-term price expectations. The net balance collapsed from -6% in January to -18% in February—a 12-percentage-point swing that indicates surveyors anticipate downward price pressure over the coming three months.[1]

At the national level, headline house prices remained broadly flat with a -12% net balance, suggesting stagnation rather than growth or significant decline.[1] This "muddle-through" scenario reflects competing forces:

| Downward Pressures | Upward Supports |

|---|---|

| Weakening demand | Limited supply |

| Affordability constraints | Mortgage rate stabilization hopes |

| Economic uncertainty | Employment resilience |

| Geopolitical risks | Long-term housing shortage |

Despite near-term pessimism, twelve-month price expectations remained moderately positive at +33%, indicating surveyors view current weakness as temporary rather than the start of a sustained downturn.[1] This disconnect between short and medium-term outlooks creates both risk and opportunity for building survey professionals.

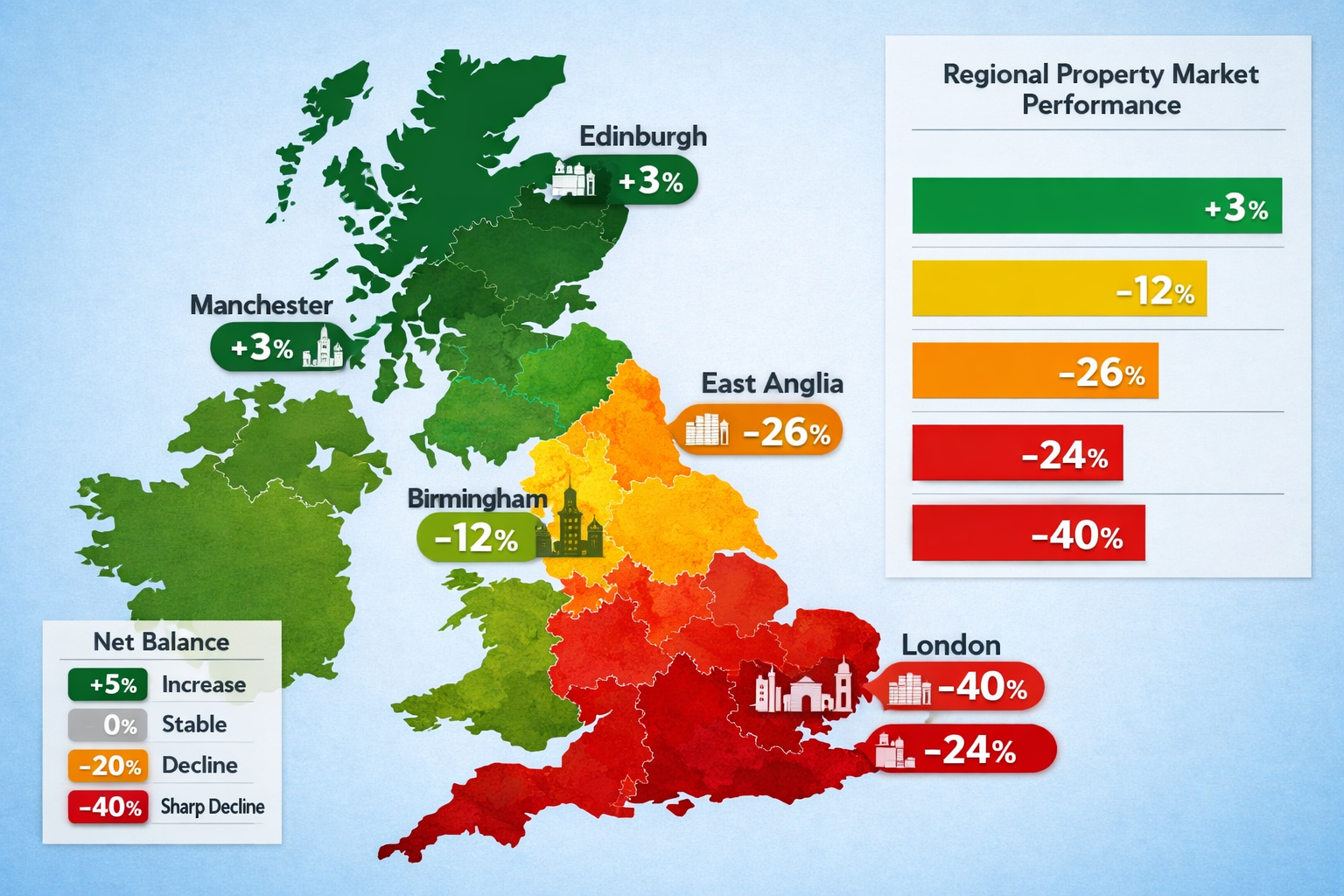

Regional Divergence: The North-South Divide Intensifies

Building Survey Market Sentiment in Spring 2026: London and Southern Weakness

The most dramatic aspect of current market conditions is the unprecedented regional divergence in performance and sentiment. London experienced the most severe downward pressure, with a net balance of -40% in February 2026—a stunning reversal from the +56% twelve-month expectations recorded just weeks earlier.[1]

This London weakness extends across the broader southern market:

- South East: -24% net balance, reflecting affordability challenges and economic uncertainty

- East Anglia: -26% net balance, showing contagion from London weakness

- South West: Moderate negative sentiment as second-home markets cool

Several factors explain southern market vulnerability:

💷 Affordability crisis: Price-to-income ratios in London and the South East remain at historical extremes, limiting buyer pools

💷 Interest rate sensitivity: Higher absolute prices mean mortgage rate increases have larger cash-flow impacts

💷 Economic concentration: Southern markets more exposed to financial services sector volatility

💷 Overseas buyer withdrawal: International uncertainty particularly affects prime London and commuter belt markets

For building surveyors operating in these regions, the implications are significant. Demand for RICS Building Surveys (Level 3) may decline as transaction volumes fall, while buyers who remain active may seek more comprehensive inspections to justify purchases in a falling market.

Northern Resilience Provides Bright Spots

In stark contrast to southern weakness, northern regions continued to demonstrate resilience with firmer price trends. The North West of England showed house price appreciation of up to 3% annually, while Scotland and Northern Ireland maintained positive sentiment.[1][4]

This northern strength reflects distinct market dynamics:

✅ Relative affordability: Lower absolute prices maintain accessibility for first-time buyers

✅ Economic diversification: Broader employment base reduces vulnerability to single-sector shocks

✅ Infrastructure investment: Transport and regeneration projects support demand

✅ Migration patterns: Internal UK migration from expensive southern markets

✅ Rental yield advantage: Better returns attract buy-to-let investors

For surveyors in these regions, the outlook remains more positive. Steady transaction activity supports consistent workload, while price growth may increase demand for valuation services alongside traditional building surveys. Chartered surveyors operating across multiple regions can leverage this divergence by reallocating resources toward stronger markets.

Regional Strategy Implications for Surveyors

The north-south divide creates strategic imperatives for building survey practices:

For London and southern practices:

- Diversify service offerings beyond residential surveys

- Develop expertise in commercial building surveys as alternative revenue

- Enhance value-add services like defect analysis and remediation guidance

- Consider geographic expansion into resilient northern markets

- Focus on high-value, complex properties where surveys remain essential

For northern practices:

- Capitalize on relative market strength with capacity expansion

- Develop relationships with volume conveyancers and estate agents

- Maintain competitive pricing to capture market share

- Build expertise in first-time buyer properties and new-build snagging

- Prepare for potential southern competitor entry as they seek growth

Supply Dynamics and the Rental Market Squeeze

Sales Market Supply Stabilizes

New instructions to sell remained broadly stable at +2% net balance in February 2026, suggesting the market is experiencing neither a flood of new stock nor a severe shortage.[1] This stability contrasts with the demand collapse, creating a supply-demand imbalance that explains downward price pressure.

Several factors contribute to vendor hesitancy:

- Loss aversion: Sellers reluctant to accept lower prices than recent peak valuations

- Mortgage lock-in: Low fixed rates from 2020-2021 discourage moves

- Economic uncertainty: Vendors postpone discretionary moves until conditions improve

- Chain dependency: Difficulty finding onward purchases delays listings

For building surveyors, stable supply means the pool of properties requiring inspection remains adequate, but falling demand reduces the conversion rate from listing to survey instruction.

Rental Market Faces Acute Supply Crisis

The rental sector presents a starkly different picture. Landlord instructions remained firmly negative at -27%, indicating an ongoing exodus of rental stock from the market.[1] Simultaneously, tenant demand remains robust, creating severe supply shortages in most regions.

This supply-demand imbalance drives expectations that rents will rise significantly, with +20% of survey participants expecting increases over the coming three months.[1] Several policy and economic factors explain landlord withdrawal:

- Tax treatment changes: Reduced mortgage interest relief and capital gains tax increases

- Regulatory burden: Enhanced energy efficiency requirements and tenant protections

- Licensing costs: Selective and additional licensing schemes in many areas

- Market exit opportunity: Strong sales prices encourage portfolio liquidation

For building surveyors, the rental crisis creates opportunities in several areas:

- Portfolio disposal surveys: Landlords exiting require valuations and condition assessments

- Energy efficiency assessments: Regulatory compliance drives demand for specialized surveys

- Buy-to-let purchase surveys: Remaining investors seek thorough due diligence

- Disrepair and dilapidations: Tenant disputes increase as stock quality declines

Interpreting Surveyor Confidence: Short-Term Caution Meets Long-Term Optimism

The Confidence Paradox in Building Survey Market Sentiment Spring 2026

One of the most intriguing aspects of current Building Survey Market Sentiment in Spring 2026: Interpreting RICS Data on Regional Divergence and Surveyor Confidence is the disconnect between near-term pessimism and medium-term optimism.

While near-term price expectations fell to -18%, twelve-month price expectations remained at +33%—indicating surveyors believe current weakness will prove temporary.[1] Similarly, despite subdued current activity, +17% of professionals expected sales volumes to rise over the next 12 months.[1]

This confidence paradox reflects several considerations:

🔍 Cyclical perspective: Experienced surveyors recognize temporary demand shocks versus structural decline

🔍 Fundamental shortage: UK housing undersupply remains acute, supporting medium-term prices

🔍 Rate expectations: Anticipation that mortgage rates will stabilize or decline as inflation moderates

🔍 Pent-up demand: Buyers postponing purchases represent future transaction pipeline

🔍 Economic resilience: Employment remains robust despite growth challenges

For building survey professionals, this dual outlook suggests:

- Near-term caution: Manage costs and maintain financial resilience through weak months

- Medium-term positioning: Invest in capacity and capability for anticipated recovery

- Service innovation: Develop offerings that address current market conditions

- Client relationship focus: Maintain engagement during quiet periods to capture recovery demand

Workload Implications for Chartered Building Surveyors

The RICS data has direct implications for survey instruction volumes and practice management. Historical correlations suggest:

Demand-to-instruction lag: New buyer enquiries typically convert to survey instructions within 6-8 weeks, meaning the February demand collapse (-26%) will impact April-May workload.[1]

Regional variation: Northern practices may see continued steady instructions, while southern firms face 15-25% volume declines.

Survey type mix: Buyers remaining active in weak markets often opt for more comprehensive RICS Home Surveys to reduce purchase risk.

Price sensitivity: Downward price pressure may increase buyer negotiation leverage, with surveys identifying defects becoming key negotiation tools.

Completion rates: The gap between agreed sales (-12%) and enquiries (-26%) suggests higher conversion rates among committed buyers, potentially improving survey-to-completion ratios.[1]

Practices should model scenarios based on regional exposure and service mix, with southern-focused firms potentially facing 20-30% workload reductions while northern practices maintain 90-100% of normal volumes.

Strategic Positioning for Building Survey Practices in 2026

Service Diversification Strategies

The current market environment rewards practices that can adapt service offerings to changing conditions:

Expand beyond residential surveys:

- Commercial building surveys provide alternative revenue as businesses adapt premises

- Dilapidations surveys serve commercial lease market

- Structural surveys address defect investigation demand

Develop specialized residential services:

- Subsidence surveys for properties with movement concerns

- Damp surveys addressing moisture issues in older stock

- Drone surveys for comprehensive roof and elevation inspection

Value-add consultancy:

- Renovation cost guidance for buyers planning improvements

- Energy efficiency assessments supporting retrofit planning

- Defect prioritization helping buyers make informed offers

Geographic Expansion Considerations

Regional divergence creates opportunities for strategic geographic expansion:

Southern practices expanding north:

- Leverage brand reputation and expertise in resilient markets

- Partner with local firms for market knowledge and presence

- Focus on higher-value properties where southern expertise commands premium

Northern practices consolidating position:

- Invest in capacity to serve growing local demand

- Develop relationships with volume conveyancers and lenders

- Build market share while southern competitors focus elsewhere

Multi-regional practices optimizing allocation:

- Shift surveyor resources toward stronger markets temporarily

- Develop flexible working arrangements enabling geographic mobility

- Use regional variation to smooth overall practice workload

Technology and Efficiency Investment

Weak markets create opportunities to invest in efficiency improvements that position practices for recovery:

- Digital survey platforms: Streamline report production and client communication

- Drone and thermal imaging: Enhance survey quality while reducing time on-site

- Client portals: Improve service experience and differentiation

- Data analytics: Better understand local market trends and pricing opportunities

- Marketing automation: Maintain client relationships during quiet periods

Macroeconomic Context: Understanding the Drivers Behind Spring 2026 Sentiment

Interest Rate and Inflation Dynamics

The sharp deterioration in sentiment between January and February 2026 reflects renewed concerns about inflation and interest rates. Mortgage rates increased from 4.24% to 4.51% in mid-March as lenders responded to global instability and funding cost increases.[4]

This rate volatility creates several challenges:

- Affordability impact: Higher rates reduce maximum borrowing capacity

- Buyer psychology: Rate uncertainty encourages postponement of purchase decisions

- Fixed rate expiry: Homeowners facing refinancing at higher rates reduce discretionary spending

- Investment returns: Higher risk-free rates make property less attractive relative to alternatives

For building surveyors, rate movements create indirect effects through transaction volume impacts, while also affecting practice financing costs and investment decisions.

Geopolitical Uncertainty and Consumer Confidence

International tensions, particularly conflicts involving Iran and broader Middle East instability, contributed significantly to the confidence collapse in early 2026.[4] Geopolitical shocks affect property markets through multiple channels:

- Energy prices: Conflict risk premiums increase heating and transport costs

- Economic growth: Trade disruptions and uncertainty reduce GDP expectations

- Financial markets: Stock market volatility affects wealth perceptions

- Migration patterns: International instability influences buyer and tenant demand

While geopolitical factors lie beyond surveyor control, understanding these drivers helps contextualize market movements and advise clients appropriately.

Employment and Income Resilience

Despite demand weakness, employment has remained relatively robust through early 2026, providing underlying support for the market. This employment resilience explains why twelve-month expectations remain positive despite near-term challenges—surveyors recognize that income stability eventually translates to housing demand.

Key employment considerations include:

- Regional variation: Northern labor markets showing particular strength

- Sector shifts: Technology and green economy jobs growing while traditional sectors decline

- Wage growth: Nominal increases supporting affordability despite rate rises

- Job security perceptions: Confidence in employment stability affects purchase decisions

Practical Implications for Property Buyers and Homeowners

Buyer Strategy in the Current Environment

For property buyers navigating the spring 2026 market, the RICS data suggests several strategic considerations:

Timing decisions:

- Near-term price pressure may create opportunities for patient buyers

- Regional variation means timing considerations differ significantly by location

- Mortgage rate uncertainty argues for securing agreements in principle early

Negotiation leverage:

- Weak demand conditions favor buyers in price negotiations

- Comprehensive building surveys provide valuable negotiation ammunition

- Vendors facing reduced enquiries may accept lower offers

Survey importance:

- Market uncertainty increases value of thorough property inspection

- Identifying defects becomes more critical when future price growth uncertain

- Choosing the right survey type matches inspection depth to risk tolerance

Regional considerations:

- Northern markets offer better value and growth prospects

- Southern buyers may benefit from waiting for further price adjustment

- Cross-regional comparison reveals significant value disparities

Homeowner Considerations

For existing homeowners, current market conditions present different challenges:

Selling decisions:

- Weak demand argues for postponing discretionary moves if possible

- Properties requiring significant work may struggle to attract buyers

- Realistic pricing essential in current environment

Improvement investments:

- Weak market reduces urgency for pre-sale improvements

- Focus on essential maintenance rather than value-add renovations

- Energy efficiency improvements may become regulatory requirements

Refinancing planning:

- Fixed rate expiry timing critical given rate volatility

- Consider longer-term fixes to reduce future uncertainty

- Assess affordability at higher rates before committing to moves

Future Outlook: What the Data Suggests for the Rest of 2026

Base Case Scenario: Gradual Recovery

The most likely scenario suggested by Building Survey Market Sentiment in Spring 2026: Interpreting RICS Data on Regional Divergence and Surveyor Confidence involves:

Q2 2026 (April-June):

- Continued weak demand as February's -26% enquiry collapse flows through

- Transaction volumes 10-15% below 2025 levels

- Prices broadly flat nationally with regional variation

- Survey workload down 15-20% in southern markets, stable in north

Q3 2026 (July-September):

- Gradual demand recovery as rate uncertainty reduces

- Traditional autumn market activity provides seasonal boost

- Prices stabilize with modest growth in northern regions

- Survey instructions recover to 90-95% of normal levels

Q4 2026 (October-December):

- Continued recovery momentum into year-end

- Twelve-month positive expectations (+33%) begin materializing[1]

- Regional divergence persists but southern markets stabilize

- Survey workload approaches normal seasonal patterns

This base case assumes no major additional economic shocks and gradual moderation in inflation and interest rates.

Upside Scenario: Faster Recovery

A more optimistic scenario could develop if:

- Inflation falls faster than expected, enabling rate cuts

- Geopolitical tensions ease, restoring consumer confidence

- Government introduces targeted housing market support

- Pent-up demand releases rapidly once uncertainty reduces

In this scenario, the twelve-month expectations of +33% for prices and +17% for sales volumes could prove conservative, with recovery accelerating through summer 2026.[1]

Downside Scenario: Extended Weakness

Conversely, conditions could deteriorate further if:

- Interest rates rise further in response to persistent inflation

- Economic recession reduces employment and income security

- Geopolitical situation worsens significantly

- Financial market stress creates credit availability issues

This downside case would see the near-term pessimism (-18% price expectations) extending beyond three months, with potential for modest price declines nationally and more significant falls in southern markets.[1]

Conclusion

Building Survey Market Sentiment in Spring 2026: Interpreting RICS Data on Regional Divergence and Surveyor Confidence reveals a property market at an inflection point. The sharp deterioration in buyer demand to -26% and near-term price expectations to -18% signals genuine short-term challenges, while the persistence of positive twelve-month outlooks (+33% for prices, +17% for sales) suggests surveyors view current weakness as temporary rather than structural.[1]

The most striking feature of the current environment is unprecedented regional divergence. London's -40% price pressure contrasts starkly with the North West's +3% annual appreciation, creating fundamentally different operating environments for building survey practices across the country.[1][4] This divergence demands strategic responses tailored to regional exposure and market positioning.

For chartered building surveyors and property professionals, the data suggests several clear action steps:

Immediate Actions (Next 30 Days)

✅ Model workload scenarios based on regional exposure and historical demand-to-instruction conversion lags

✅ Review cost structures to ensure financial resilience through anticipated quiet period in Q2 2026

✅ Strengthen client relationships with conveyancers, estate agents, and lenders to maintain instruction flow

✅ Assess service mix and identify opportunities for diversification beyond standard residential surveys

Medium-Term Positioning (Next 3-6 Months)

✅ Invest in efficiency improvements during quieter periods to enhance competitiveness for recovery

✅ Develop specialized capabilities in areas like energy efficiency, subsidence, and defect analysis

✅ Consider geographic expansion or resource reallocation to capitalize on regional variation

✅ Enhance digital presence and marketing to capture recovering demand as confidence returns

Strategic Planning (Next 6-12 Months)

✅ Prepare for recovery by maintaining capacity and capability despite near-term weakness

✅ Build resilience through service diversification and geographic spread

✅ Monitor RICS data monthly to identify inflection points and adjust strategy accordingly

✅ Position for long-term trends including rental market evolution, sustainability requirements, and demographic shifts

The spring 2026 market presents genuine challenges, but the underlying fundamentals—housing shortage, employment resilience, and medium-term confidence—suggest current weakness will prove temporary. Practices that maintain strategic perspective, adapt to regional conditions, and invest in capability during the downturn will be best positioned to capitalize on the recovery that surveyor confidence suggests will materialize through the second half of 2026.

For property buyers and homeowners, the message is equally clear: weak sentiment creates opportunities for patient buyers with thorough due diligence, while sellers should approach the market with realistic expectations and strong professional advice. The importance of comprehensive building surveys from qualified RICS professionals increases in uncertain markets, providing the detailed property intelligence needed to make confident decisions despite broader market volatility.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] Uk Residential Property Market Update Spring 2026 – https://www.vailwilliams.com/uk-residential-property-market-update-spring-2026/