The regional office market is experiencing a seismic shift. As Birmingham celebrates record-breaking rental growth of 20% and Manchester races toward the £50 per square foot benchmark, property valuers face an unprecedented challenge: accurately capturing the value of premium office spaces in an era where artificial intelligence infrastructure and technology-enabled workspaces command significant rental premiums. Valuation Surveys for Core City Office Properties 2026: Capturing AI-Driven Rental Growth in Manchester and Birmingham requires sophisticated methodologies that account for both traditional metrics and emerging demand drivers reshaping the commercial real estate landscape.

Key Takeaways

- Birmingham achieved record prime office rents of £52 per square foot in Q4 2025, representing 20% annual growth, while Manchester is projected to reach the £50 per square foot milestone in 2026

- RICS Red Book valuation standards provide the framework for capturing AI-driven rental premiums through enhanced comparable analysis and income capitalization methods

- Limited Grade A office supply across both cities—with only 2.3 million square feet of speculative development underway—creates significant upward pressure on valuations

- Technology infrastructure and ESG credentials now serve as primary value differentiators, requiring surveyors to adjust valuation models accordingly

- Lease regearing assessments must incorporate flexibility provisions and break clauses as cost-sensitive occupiers navigate premium rental environments

Understanding the 2026 Regional Office Market Dynamics

The commercial property landscape in Manchester and Birmingham has transformed dramatically over the past 18 months. According to Lambert Smith Hampton's Regional Office Report, prime rents across the "Big Six" regional markets are on course for 10.2% average growth in 2025—the highest growth rates ever recorded[7]. This exceptional performance significantly outpaces the 8.2% average across all 15 regional markets, signaling a fundamental shift in occupier preferences toward premium regional office space.

Birmingham's Record-Breaking Performance

Birmingham's achievement of £52 per square foot prime rents represents more than just a numerical milestone[7]. The city recorded 23 new development starts in 2025—the highest figure in five years—with 40 developments currently under construction in the city centre[1]. This development activity delivered 477,223 square feet of office floorspace in 2025, with a further 733,912 square feet currently under construction[2].

Large-scale transactions underscore the strength of occupier demand. EY's lease of 94,000 square feet at Three Chamberlain Square exemplifies the corporate appetite for best-in-class city centre buildings with high-quality amenities and robust ESG credentials[7]. For professional valuation of commercial property, these transactions provide critical comparable evidence that informs rental value assessments.

Manchester's Trajectory Toward £50 Per Square Foot

Manchester's office market demonstrates equally impressive momentum. The city is expected to reach the £50 per square foot prime rent benchmark in 2026, driven by sustained occupier demand for premium regional office space[7]. Trader Media's 130,000 square foot deal at 3 Circle Square in Manchester represents one of the largest regional office transactions in recent years, highlighting the scale of corporate commitment to the city[7].

The limited supply of Grade A office space creates a supply-demand imbalance that fundamentally supports rental growth. Total speculative office development under construction across the 15 regional markets stood at just 2.3 million square feet at the end of Q3 2025, up 27% from the 12-month low but still constrained relative to demand[7]. Anticipated speculative development starts for 2026 remain modest at 589,000 square feet, suggesting continued upward pressure on prime rents.

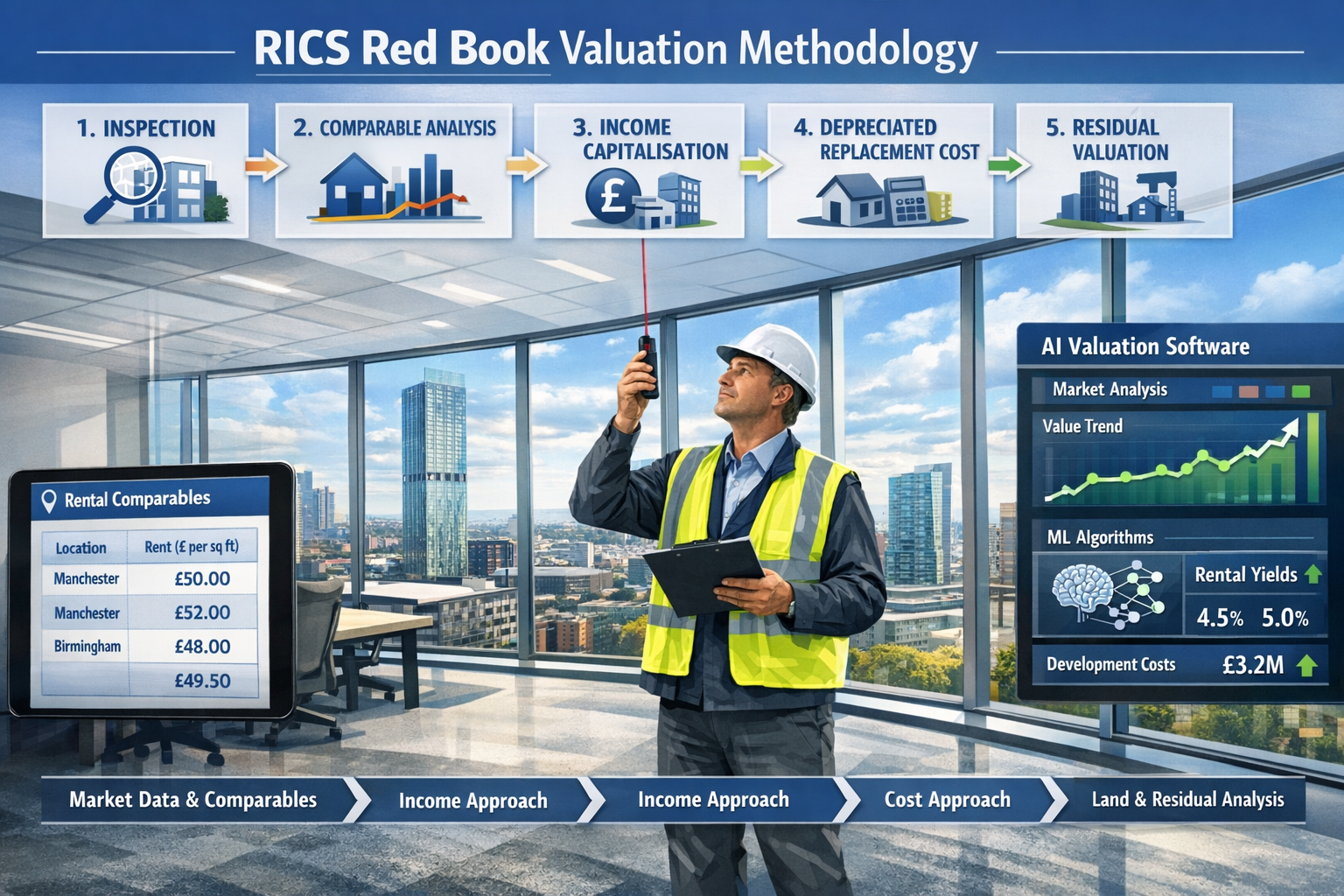

RICS Valuation Techniques for Core City Office Properties

Professional valuation of core city office properties in 2026 requires adherence to RICS Valuation Standards (the Red Book) while incorporating market intelligence that captures AI-driven rental dynamics. The RICS Red Book valuation framework provides the foundation for defensible, market-reflective assessments.

Comparable Analysis in High-Growth Markets

The comparable method remains the primary valuation approach for investment-grade office properties. However, applying this technique in markets experiencing 20% annual rental growth requires careful consideration of:

Time adjustments: Comparable transactions from 12-18 months ago may understate current values by 15-25%, necessitating robust time-adjustment factors based on quarterly rental growth indices.

Quality differentials: Not all office space commands premium rents. Grade A properties with technology infrastructure, sustainable building certifications (BREEAM Excellent or Outstanding), and amenity-rich environments achieve rental premiums of 30-40% over secondary stock.

Location micro-markets: Within Birmingham and Manchester, specific submarkets command varying rental levels. Birmingham's Colmore Row and Snow Hill districts, and Manchester's Spinningfields and Circle Square precincts, represent prime locations with distinct rental profiles.

Transaction evidence: Large-scale lettings like the EY and Trader Media deals provide headline rental evidence, but surveyors must adjust for lease incentives, rent-free periods, and capital contributions that affect effective rental values.

For chartered surveyors conducting RICS valuations, maintaining comprehensive databases of comparable transactions with detailed lease terms becomes essential for accurate market positioning.

Income Capitalization and Yield Compression

The income approach to valuation involves capitalizing net rental income at an appropriate yield to determine capital value. In 2026's market, several factors influence yield selection:

Prime office yields in Birmingham and Manchester have compressed significantly as institutional investors recognize the quality and growth potential of regional office assets. Prime yields in both cities now range between 5.00-5.75%, depending on covenant strength, lease length, and building quality[8].

Rental growth expectations must be explicitly modeled. With Birmingham demonstrating 20% annual growth and Manchester approaching similar trajectories, valuation models should incorporate explicit rental growth assumptions over the investment horizon, typically using discounted cash flow (DCF) analysis for properties with lease events or rent reviews.

Reversionary potential adds significant value where properties are let below current market rents. Buildings with lease expiries or rent reviews in 2026-2028 offer substantial reversionary uplifts as rents reset to market levels.

Risk-adjusted returns reflect the relative security of regional office investments. Properties with strong ESG credentials, technology infrastructure, and long-term covenants from quality occupiers command lower yields (higher capital values) due to reduced risk profiles.

Depreciated Replacement Cost for Specialized Properties

For office properties with specialized AI infrastructure—including dedicated data centers, enhanced cooling systems, fiber optic networks, and smart building management systems—the depreciated replacement cost (DRC) method provides valuable insights, particularly when comparable evidence is limited.

This approach involves:

- Calculating the current cost of constructing an equivalent building with similar specifications

- Deducting depreciation for physical deterioration, functional obsolescence, and economic obsolescence

- Adding land value at current use

- Adjusting for locational advantages specific to Manchester or Birmingham

The DRC method proves particularly relevant for purpose-built tech headquarters or AI-enabled office campuses where traditional comparables may not fully capture the value of specialized infrastructure investments.

Capturing AI-Driven Rental Premiums in Valuation Models

The integration of artificial intelligence infrastructure into office buildings represents a paradigm shift in occupier requirements. Technology companies, financial services firms, and professional services organizations increasingly demand office environments that support AI-driven operations, hybrid working models, and advanced collaboration technologies.

Technology Infrastructure as a Value Driver

Modern office occupiers prioritize buildings with:

High-speed connectivity: Fiber optic networks with 1Gbps+ bandwidth capacity enable cloud computing, video conferencing, and data-intensive AI applications. Buildings with redundant connectivity from multiple providers command rental premiums of 8-12% over standard specifications[8].

Smart building systems: AI-powered building management systems that optimize energy consumption, space utilization, and environmental conditions enhance operational efficiency. These systems reduce occupancy costs by 15-20% while improving employee experience.

Flexible power infrastructure: AI workloads require substantial electrical capacity. Office buildings with enhanced power distribution systems (minimum 25-30 watts per square foot) accommodate technology-intensive operations without costly retrofits.

Collaborative technology: Buildings pre-equipped with video conferencing infrastructure, digital signage, and integrated booking systems reduce occupier fit-out costs by £20-30 per square foot while accelerating occupancy timelines.

When conducting Valuation Surveys for Core City Office Properties 2026: Capturing AI-Driven Rental Growth in Manchester and Birmingham, surveyors must quantify these infrastructure advantages through rental premium analysis and occupancy cost modeling.

ESG Credentials and Valuation Impact

Environmental, Social, and Governance (ESG) performance has evolved from a "nice-to-have" to a fundamental value determinant. Corporate occupiers face increasing pressure from stakeholders, regulators, and employees to operate from sustainable buildings.

Office properties with strong ESG credentials demonstrate:

- BREEAM Excellent or Outstanding ratings: Buildings with top-tier sustainability certifications achieve rental premiums of 10-15% and experience faster letting periods (30-40% reduction in void periods)

- EPC A or B ratings: Energy-efficient buildings reduce occupier operating costs while meeting regulatory requirements and corporate sustainability commitments

- Net-zero pathways: Properties with credible decarbonization strategies aligned with UK net-zero targets attract quality covenants and long-term lease commitments

- Wellness certifications: WELL Building Standard or Fitwel certifications that prioritize occupant health and wellbeing support employee attraction and retention

The valuation costs associated with comprehensive ESG assessments are justified by the material impact these factors have on rental values, void periods, and capital values.

Market Evidence from Big Six Cities

Office take-up reached 1.1 million square feet across the "Big Six" cities in Q4 2025, indicating strong occupier confidence heading into 2026[3]. This transaction volume provides robust comparable evidence for valuers, though careful analysis reveals important distinctions:

| City | Prime Rent (£/sq ft) | Annual Growth | Key Drivers |

|---|---|---|---|

| Birmingham | £52.00 | 20.0% | Limited supply, corporate relocations, HS2 connectivity |

| Manchester | £48.00 | 16.7% | Tech sector growth, media clusters, Northern Powerhouse investment |

| Leeds | £42.00 | 18.0% | Financial services expansion, cost arbitrage vs. London |

| Bristol | £45.00 | 12.5% | Technology sector, quality of life factors |

| Edinburgh | £41.00 | 9.5% | Financial services, limited Grade A supply |

| Glasgow | £35.00 | 8.5% | Public sector presence, regeneration initiatives |

This comparative analysis demonstrates that Birmingham and Manchester lead regional rental growth, driven by superior connectivity, diverse economic bases, and substantial corporate occupier demand. For why choosing an RICS chartered building surveyor matters, these professionals possess the local market knowledge and technical expertise to accurately position properties within these dynamic markets.

Lease Regearing Assessments and Occupier Cost Management

As prime rents approach £50-52 per square foot in Manchester and Birmingham, cost-sensitive occupiers increasingly explore lease restructuring options to manage occupancy expenses. Valuation Surveys for Core City Office Properties 2026: Capturing AI-Driven Rental Growth in Manchester and Birmingham must incorporate sophisticated lease regearing analysis to support both landlord and tenant decision-making.

Break Clause Valuations

Break clauses provide occupiers with flexibility to exit leases at predetermined dates, typically exercisable at the fifth or tenth anniversary of a 10-15 year lease term. The valuation impact of break clauses depends on:

Probability of exercise: In rising rental markets, tenants are unlikely to exercise breaks when paying below-market rents. Conversely, occupiers paying above-market rents (due to rent reviews or market corrections) demonstrate higher exercise probability.

Notice periods: Standard six-month notice periods affect cash flow modeling and void period assumptions in DCF valuations.

Conditions precedent: Break clauses with conditions (e.g., "tenant must not be in breach of covenants") reduce exercise probability and therefore have minimal impact on valuations.

Market positioning: Properties let at £45 per square foot with breaks exercisable in 2026-2027 face higher vacancy risk as occupiers may relocate to newer buildings or renegotiate terms.

Professional rent reviews conducted by RICS chartered surveyors provide the technical analysis necessary to determine market rent at review dates, informing both lease restructuring negotiations and investment valuations.

Lease Restructuring Scenarios

Landlords and tenants increasingly collaborate on lease regearing arrangements that balance occupier cost management with landlord income security:

Rent reductions with term extensions: Occupiers paying above-market rents may negotiate 10-15% rent reductions in exchange for extending lease terms by 3-5 years, providing landlords with income certainty.

Stepped rent profiles: Rather than immediate uplifts to market rent, parties may agree to annual stepped increases (e.g., 3-5% per annum) that gradually transition to market levels while providing occupier cost predictability.

Capital expenditure contributions: Landlords may fund tenant improvements (£30-50 per square foot) in exchange for rental uplifts or lease extensions, enhancing building quality while securing occupancy.

Turnover rents: For retail-adjacent office uses (ground floor cafes, co-working operators), hybrid rent structures combining base rent plus turnover percentages align landlord-tenant interests.

Surveyors conducting lease regearing assessments must model multiple scenarios, quantifying the net present value implications of each option to support informed decision-making. This analysis often involves collaboration with commercial property surveying specialists who understand the operational and strategic considerations beyond pure financial metrics.

Tenant Incentive Packages

In competitive letting markets, landlord incentives significantly affect effective rental values:

Rent-free periods: Typical incentives range from 12-24 months on 10-15 year leases for Grade A space, effectively reducing headline rents by 8-15%.

Capital contributions: Landlords commonly contribute £40-70 per square foot toward tenant fit-out costs for quality covenants, particularly for large floor plates (20,000+ square feet).

Service charge caps: Occupiers increasingly negotiate fixed or capped service charges to manage operating cost volatility, transferring risk to landlords.

Flexibility provisions: Rights to assign, sublet, or break provide occupiers with strategic flexibility valued at 5-10% of headline rent.

Accurate valuation requires adjusting headline rents to effective rents that reflect the true economic terms of lettings. This adjustment proves critical when using recent transactions as comparable evidence, as headline rents may overstate actual rental values by 10-20% depending on incentive packages.

Surveyor Tools and Methodologies for 2026 Valuations

Modern valuation practice combines traditional surveying techniques with advanced analytical tools that enhance accuracy and defensibility. Professional surveyors conducting Valuation Surveys for Core City Office Properties 2026: Capturing AI-Driven Rental Growth in Manchester and Birmingham employ:

Digital Measurement and Building Information

Laser measurement devices and 3D scanning technology provide precise floor area measurements compliant with RICS measurement standards (IPMS 3 for office space). Accurate measurement proves essential as rental values of £50-52 per square foot translate to significant value differences for measurement discrepancies.

Building Information Modeling (BIM) data, when available, offers comprehensive building specifications including:

- Structural systems and load-bearing capacities

- Mechanical, electrical, and plumbing (MEP) infrastructure

- Space planning and circulation efficiency

- Maintenance histories and capital expenditure requirements

This technical data informs depreciation assessments and enables accurate comparison of building quality across comparable properties.

Market Intelligence Platforms

Subscription-based commercial property databases (CoStar, EGi, Radius Data Exchange) provide transaction evidence, rental comparables, and market analytics. However, surveyors must supplement database information with direct market intelligence from letting agents, occupiers, and property managers to capture:

- Actual deal terms including incentives and break clauses

- Tenant requirements and decision-making criteria

- Emerging submarkets and location preferences

- Development pipeline and future supply dynamics

The Valuation Office Agency also provides rating list data that offers insights into assessed rental values, though these figures typically lag market movements and require adjustment for current conditions[5].

Financial Modeling and Sensitivity Analysis

Discounted cash flow (DCF) models enable sophisticated valuation analysis that explicitly incorporates:

- Rental growth assumptions (base case, upside, downside scenarios)

- Lease event timing (expiries, breaks, reviews)

- Capital expenditure requirements (refurbishment, ESG upgrades)

- Exit yield assumptions and terminal value calculations

Sensitivity analysis tests how valuation conclusions respond to changes in key assumptions:

- ±2% variation in rental growth rates

- ±0.25% variation in discount rates and exit yields

- Alternative lease event outcomes (renewal vs. vacancy)

- Capital expenditure timing and quantum variations

This analytical rigor supports insurance reinstatement valuations and other specialized valuation purposes where precision and defensibility are paramount.

Site Inspections and Due Diligence

Despite technological advances, physical site inspections remain fundamental to professional valuation practice. Comprehensive inspections assess:

Building condition: Structural integrity, façade condition, roof condition, and MEP systems age and functionality inform depreciation assessments and capital expenditure forecasts.

Specification quality: Ceiling heights, floor loading, column spacing, natural light, and finishes quality directly affect rental value and occupier appeal.

Location attributes: Proximity to transport hubs, amenities, competing buildings, and urban regeneration initiatives influence location premiums.

ESG performance: On-site assessment of energy systems, waste management, water efficiency, and occupant wellness features validates sustainability credentials.

Surveyors conducting building surveys bring this technical inspection expertise to valuation assignments, ensuring that valuation conclusions reflect actual property condition and quality rather than marketing representations.

Regulatory Considerations and Business Rates Revaluation

The 2026 Business Rates Revaluation represents a significant regulatory event affecting office property valuations in Birmingham and Manchester. The Valuation Office Agency will reassess rateable values based on rental evidence from April 2023, though the revaluation takes effect from April 2026[6].

Impact on Occupier Costs

Business rates represent approximately 50% of headline rent for most office properties (based on the 49.9p multiplier for 2025/26). For properties with prime rents of £50-52 per square foot, business rates add approximately £25-26 per square foot to total occupancy costs, bringing all-in costs to £75-78 per square foot before service charges and utilities.

The 2026 revaluation will likely result in rateable value increases for Birmingham and Manchester office properties reflecting the substantial rental growth achieved since the April 2023 valuation date. Properties experiencing 20% rental growth may face corresponding increases in rateable values, though transitional relief schemes typically phase in significant increases over 3-5 years.

Occupiers evaluating lease commitments must model total occupancy costs including anticipated business rates increases, influencing demand for premium office space and potentially moderating rental growth if total costs approach occupier affordability thresholds.

Valuation Challenges and Appeals

The business rates revaluation creates opportunities for rating appeals where rateable values appear excessive relative to market evidence. Professional surveyors experienced in rating valuations can challenge assessments by demonstrating:

- Comparable properties with lower rateable values

- Market rental evidence below assumed rental values

- Property-specific factors (configuration, condition, location) warranting adjustments

- Changes in local market conditions affecting rental values

For property owners and occupiers, coordinating investment valuations with rating assessments ensures consistency across valuation purposes and identifies potential appeal opportunities that reduce occupancy costs.

Strategic Implications for Property Investors and Occupiers

The exceptional rental growth trajectory in Birmingham and Manchester creates distinct opportunities and challenges for different market participants.

Investor Considerations

Property investors benefit from multiple value-creation drivers:

Income growth: Properties let below market rent or with upcoming rent reviews offer substantial reversionary potential. A building let at £42 per square foot in Birmingham with a 2026 rent review could achieve £52 per square foot, representing a 24% income increase.

Yield compression: As regional office markets mature and institutional capital flows increase, prime yields may compress further from current 5.00-5.75% levels toward 4.50-5.00%, driving capital value appreciation independent of rental growth.

Development opportunities: With limited speculative development and strong occupier demand, opportunistic investors may pursue office conversions, refurbishments, or ground-up developments capturing premium rents.

ESG enhancement: Capital investment in sustainability upgrades (£30-50 per square foot) can transform secondary stock into Grade A space commanding 25-35% rental premiums, generating attractive risk-adjusted returns.

Professional valuation for capital gains tax purposes becomes essential when realizing investment gains, ensuring accurate tax treatment of disposal proceeds.

Occupier Strategies

Corporate occupiers must balance cost management with workplace quality:

Lease timing: Occupiers with lease expiries in 2026-2027 face significant rental increases (15-25% in many cases). Early engagement with landlords or proactive space searches provide negotiating leverage and alternative options.

Space efficiency: Hybrid working models enable space consolidation, with many organizations reducing office footprints by 20-30% while upgrading to premium buildings. This strategy maintains or reduces total occupancy costs while enhancing employee experience.

Flexible leasing: Shorter lease terms (5-7 years) with breaks provide strategic flexibility but typically command 5-10% rental premiums. Occupiers must balance flexibility value against cost implications.

Build-to-suit opportunities: Large occupiers (50,000+ square feet) may negotiate pre-let agreements with developers, securing bespoke space at fixed rents while developers benefit from pre-let funding advantages.

Conclusion

Valuation Surveys for Core City Office Properties 2026: Capturing AI-Driven Rental Growth in Manchester and Birmingham requires sophisticated methodologies that extend beyond traditional comparable analysis. As Birmingham achieves record prime rents of £52 per square foot and Manchester approaches the £50 per square foot benchmark, professional surveyors must integrate multiple value drivers into comprehensive valuation models.

The convergence of limited Grade A supply, strong occupier demand, technology infrastructure requirements, and ESG imperatives creates a complex valuation environment where traditional metrics alone prove insufficient. Successful valuation practice in 2026 demands:

✅ Rigorous comparable analysis with robust time adjustments and quality differentials

✅ Sophisticated income modeling incorporating explicit rental growth and reversionary potential

✅ Technology infrastructure assessment quantifying AI-enabled building premiums

✅ ESG credential evaluation measuring sustainability impact on rental values and void periods

✅ Lease regearing expertise supporting occupier cost management and landlord income optimization

✅ Regulatory awareness of business rates implications and total occupancy cost modeling

Actionable Next Steps

For Property Owners and Investors:

- Commission comprehensive RICS valuations from chartered surveyors with regional office market expertise

- Evaluate ESG enhancement opportunities that drive rental premiums and reduce void periods

- Model multiple exit scenarios incorporating rental growth and yield compression assumptions

- Engage proactively with potential occupiers to understand evolving space requirements

For Corporate Occupiers:

- Conduct total occupancy cost analysis including business rates revaluation impacts

- Explore lease regearing options with existing landlords before committing to relocations

- Evaluate space efficiency opportunities enabled by hybrid working models

- Prioritize buildings with technology infrastructure and ESG credentials that support corporate objectives

For Professional Surveyors:

- Maintain comprehensive databases of comparable transactions with detailed lease terms

- Develop specialized expertise in technology infrastructure and ESG valuation

- Invest in digital measurement tools and financial modeling capabilities

- Cultivate market intelligence networks providing real-time transaction insights

The Birmingham and Manchester office markets demonstrate that regional cities can achieve rental growth rivaling London when supply constraints meet strong occupier demand. Professional valuation practice that accurately captures these dynamics provides the foundation for informed investment decisions, effective asset management, and strategic occupier planning throughout 2026 and beyond.

References

[1] Birmingham Crane Survey – https://www.deloitte.com/uk/en/Industries/real-estate/research/birmingham-crane-survey.html

[2] Latest Birmingham Crane Survey Reveales 5 Year High – https://selectproperty.com/insights/latest-birmingham-crane-survey-reveales-5-year-high/

[3] Take Up Hits 1.1 Million Sq Ft Across Big 6 Cities In Q4 Highlights Improving Confidence And Results In A Positive Start For 2026 – https://www.insidermedia.com/news/national/take-up-hits-1.1-million-sq-ft-across-big-6-cities-in-q4-highlights-improving-confidence-and-results-in-a-positive-start-for-2026

[5] Valuation Office Agency – https://www.gov.uk/government/organisations/valuation-office-agency

[6] Business Rates Revaluation 2026 – https://www.birmingham.gov.uk/info/20012/business_and_licensing/3145/business_rates_revaluation_2026

[7] Regional Offices Report 2025 – https://www.lsh.co.uk/explore/research-and-views/research/2025/december/regional-offices-report-2025

[8] Manchester Birmingham Vs London Property Investment 2026 – https://www.10acre.co.uk/post/manchester-birmingham-vs-london-property-investment-2026