The UK housing market in 2026 stands at a critical juncture. After months of uncertainty, property valuations are showing signs of stabilisation, yet the path forward remains complex. As the Royal Institution of Chartered Surveyors (RICS) forecasts modest 2-5% price growth over the coming year, understanding how valuation surveys adapt to this subdued momentum has never been more important for buyers, sellers, and investors navigating affordability pressures and shifting market dynamics.

Valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments reveal how professional property assessments are evolving to reflect current market realities. With February 2026 data showing renewed weakness in buyer enquiries and regional disparities intensifying, chartered surveyors are recalibrating their methodologies to provide accurate valuations in an environment marked by cautious optimism rather than exuberant growth.

Key Takeaways

- 📊 RICS forecasts modest 2-5% house price growth over 12 months, down from earlier optimistic projections as macroeconomic headwinds intensify

- 🏘️ Regional disparities are widening dramatically, with London experiencing -40% net balance while Northern regions maintain positive momentum

- 🔍 Surveyor valuation methodologies are adapting to account for subdued market activity, affordability constraints, and heightened uncertainty

- 📉 February 2026 marked a reversal from January's brief recovery, with buyer enquiries falling to -26% net balance amid inflation and interest rate concerns

- 🏠 Professional valuation surveys remain essential for accurate property assessments in a stabilising but uncertain market environment

Understanding the Current Market Context for Valuation Surveys

The UK residential property market has undergone significant transformation throughout late 2025 and early 2026. To appreciate how valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments are shaping property assessments, it's essential to understand the broader market context.

The October 2025 to February 2026 Journey

House prices reached their lowest point in October 2025, with RICS reporting a -19% net balance indicating widespread price declines across surveyor networks [1]. This represented the nadir of market sentiment following sustained interest rate pressures and economic uncertainty.

From November through January 2026, the market showed tentative signs of recovery. By January, the net balance had improved to -10%, suggesting stabilisation [2]. New buyer enquiries also strengthened to -15% in January, up from -29% in November, creating cautious optimism among market participants [2].

However, February 2026 brought a sharp reversal. New buyer enquiries deteriorated significantly to -26% net balance, while the house price indicator slipped back to -12% [1]. This renewed weakness reflected intensified concerns over:

- 💰 Inflation pressures returning to economic forecasts

- 📈 Interest rate uncertainty dampening borrowing confidence

- 🌍 Geopolitical instability affecting investor sentiment

- 🏦 Affordability constraints limiting market participation

Why Accurate Valuations Matter More Than Ever

In this environment of subdued momentum and mixed signals, professional RICS valuations have become indispensable. Unlike automated valuation models (AVMs) that rely on historical data and algorithms, chartered surveyors provide nuanced assessments that account for:

- Current market sentiment and momentum shifts

- Property-specific condition and characteristics

- Localized demand patterns and regional variations

- Recent comparable sales in similar market conditions

- Forward-looking market expectations

For buyers and sellers navigating different types of surveys, understanding how surveyors adjust their methodologies during periods of stabilisation provides crucial context for property decisions.

How RICS Surveyors Adjust Valuation Methodologies During Market Stabilisation

Valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments demonstrate how professional assessments evolve to maintain accuracy during periods of market transition. Chartered surveyors employ several sophisticated techniques to ensure valuations reflect current realities rather than outdated assumptions.

Comparative Market Analysis in Subdued Conditions

The cornerstone of property valuation remains comparative market analysis (CMA), but during stabilisation periods, surveyors must carefully select and weight comparable properties. Key adjustments include:

Time-Weighted Comparables 📅

In rapidly changing markets, recent sales carry significantly more weight than transactions from six or twelve months ago. With February 2026 showing different momentum than January, surveyors prioritize sales completed within the most recent 8-12 weeks to capture current sentiment accurately.

Condition and Location Premiums 🏡

During periods of subdued demand, property condition becomes increasingly important. Well-maintained homes with modern amenities command premiums, while properties requiring work face steeper discounts than in stronger markets. Chartered surveyors carefully assess these factors to avoid over- or under-valuation.

Days-on-Market Adjustments ⏱️

Properties selling quickly may indicate pricing below market value, while extended marketing periods suggest overpricing. In February 2026, with agreed sales at -12% net balance [1], surveyors analyze time-to-sale data to calibrate valuations appropriately.

Regional Variation Considerations

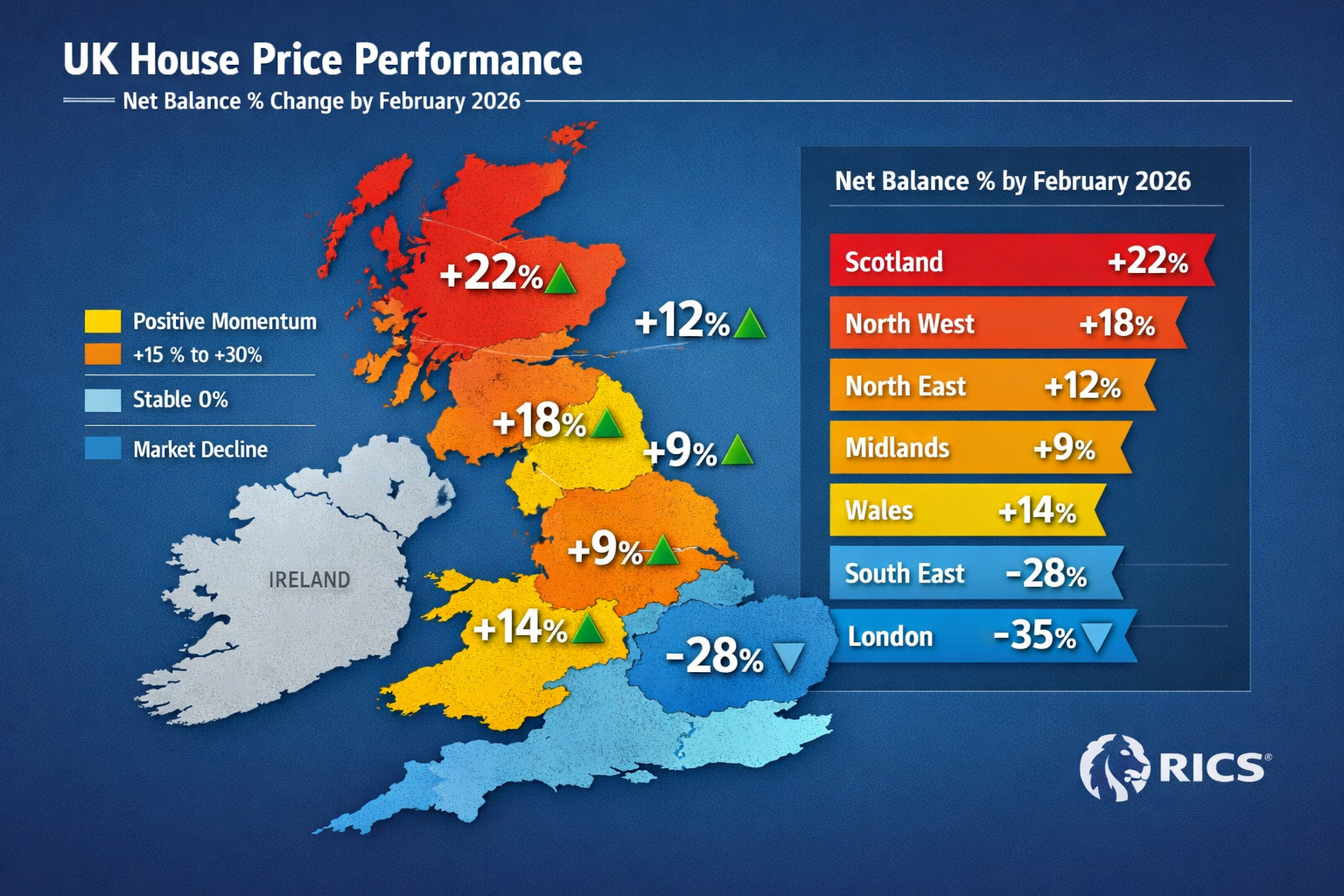

The dramatic regional disparities evident in February 2026 data require surveyors to abandon one-size-fits-all approaches. Consider these contrasts:

| Region | February 2026 Net Balance | 12-Month Outlook |

|---|---|---|

| London | -40% | +7% |

| South East | -24% | Moderate |

| East Anglia | -26% | Moderate |

| Scotland | Positive | Strong |

| Northern Ireland | Positive | Strong |

| North West | Positive | Strong |

Source: RICS UK Residential Survey February 2026 [1]

This geographic divergence means a surveyor valuing a property in London must apply fundamentally different assumptions than one assessing a comparable property in Scotland. Regional market intelligence becomes paramount, requiring surveyors to:

- Monitor local transaction volumes and pricing trends

- Understand employment and economic conditions specific to the area

- Account for regional affordability metrics and income-to-price ratios

- Consider migration patterns and demographic shifts

Forward-Looking Market Sentiment Integration

Unlike simple retrospective valuations, professional RICS valuations incorporate forward-looking market expectations. With 12-month price expectations moderating from +43% in January to +33% in February [1], surveyors must balance:

✅ Optimistic 12-Month Outlook: The +33% net balance indicates more surveyors expect prices to rise than fall over the coming year, supporting the 2-5% growth forecast

⚠️ Cautious Near-Term Sentiment: Short-term expectations fell sharply from -6% in January to -18% in February [1], suggesting immediate headwinds

🎯 Realistic Growth Projections: The moderation from earlier optimism reflects professional recognition that growth will be modest rather than robust

This nuanced approach ensures valuations neither overstate property values based on optimism nor undervalue assets due to short-term volatility.

Affordability and Mortgage Lending Considerations

Surveyors conducting valuations for mortgage purposes must consider lender risk appetite and affordability constraints. It's important to note that a mortgage valuation is not the same as a survey, but both inform lending decisions.

In the current environment of:

- Elevated interest rates compared to 2020-2021 levels

- Stricter affordability testing by lenders

- Reduced loan-to-value ratios for higher-risk segments

Surveyors must ensure valuations align with realistic lending scenarios. Overvaluation could result in mortgage rejections or subsequent downvaluations, while undervaluation may disadvantage sellers unnecessarily.

Regional Analysis: Where Valuation Surveys Show Stabilising House Prices

Understanding valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments requires examining how different UK regions are experiencing stabilisation at varying rates and from different starting points.

London and the South East: Significant Downward Pressure

The capital experienced the most dramatic weakness in February 2026, with a -40% net balance representing the sharpest regional decline [1]. This substantial negative reading indicates that far more surveyors reported falling prices than rising ones.

Key Factors Affecting London Valuations:

🏢 Affordability Crisis: London property prices relative to incomes remain at historically stretched levels, limiting buyer pools

💼 Hybrid Working Impact: Continued preference for home-office space has driven demand toward suburban and regional markets

📉 Expectation Collapse: The 12-month outlook plummeted from +56% in January to just +7% in February [1], indicating surveyors have dramatically revised growth expectations

🏘️ Prime vs. Secondary Markets: Central London prime properties show different dynamics than outer London secondary markets, requiring careful segmentation in valuations

The South East (-24% net balance) and East Anglia (-26%) mirror London's challenges, though less severely [1]. Surveyors in these regions must carefully distinguish between:

- Commuter belt properties dependent on London employment

- Self-contained regional centers with independent economic drivers

- Coastal and rural properties attracting lifestyle relocators

Northern Regions: Resilience and Relative Strength

Scotland, Northern Ireland, and the North West continue reporting firmer price trends, representing the only UK areas with positive momentum [1]. This resilience stems from several factors:

Affordability Advantage 💷

Lower absolute prices relative to incomes make these markets accessible to first-time buyers and growing families, sustaining demand even during economic uncertainty.

Regional Economic Growth 📊

Investment in regional infrastructure, technology sectors, and manufacturing has created employment growth supporting housing demand independent of London-centric factors.

Migration Patterns 🚚

Continued net migration from southern regions brings equity-rich buyers who can purchase without stretching affordability, supporting prices.

For surveyors operating in these markets, valuation adjustments differ fundamentally from southern counterparts. Rather than applying downward pressure, northern surveyors may need to:

- Account for supply constraints limiting available stock

- Consider competitive bidding situations in desirable areas

- Recognize sustained demand from multiple buyer segments

The Rental Market Factor

Rental market dynamics significantly influence residential valuations, particularly for buy-to-let investors. February 2026 data showed +20% of surveyors expect rental prices to rise over the coming three months [1], driven by:

- Constrained Supply: Landlord instructions remained firmly negative at -27% net balance, indicating fewer rental properties coming to market [1]

- Regulatory Pressures: Ongoing regulatory changes continue encouraging landlord exits, tightening supply further

- Demographic Demand: Younger cohorts unable to purchase remain in rental markets longer, sustaining tenant demand

This rental strength provides a floor for residential valuations, as investment yields remain attractive despite modest capital growth expectations. Surveyors must incorporate rental market intelligence when valuing properties with investment potential.

Practical Implications: What the 2-5% Growth Forecast Means for Property Stakeholders

The RICS forecast of 2-5% house price growth over the next 12 months carries different implications for various market participants. Understanding how valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments translate into practical outcomes helps stakeholders make informed decisions.

For Homebuyers: Timing and Valuation Strategies

First-Time Buyers 🏠

The modest growth forecast suggests neither urgent pressure to buy immediately nor compelling reasons to wait indefinitely. Key considerations include:

- Affordability Windows: With interest rates stabilizing rather than falling dramatically, affordability improvements will be gradual

- Negotiation Leverage: Subdued demand (-26% new buyer enquiries) [1] provides negotiating room on asking prices

- Professional Surveys: Investing in comprehensive building surveys becomes more valuable when price growth is modest, as avoiding costly defects matters more than catching rapid appreciation

Existing Homeowners Looking to Move 🔄

For those selling one property to purchase another, the stabilisation environment presents both challenges and opportunities:

✅ Advantages: Selling and buying in the same market conditions means relative positions remain stable

⚠️ Challenges: Longer marketing periods may be necessary; realistic pricing based on professional valuations becomes essential

📋 Strategy: Obtain RICS valuations early to set appropriate asking prices and avoid extended time on market

For Property Investors: Yield vs. Capital Growth

With capital growth expectations moderated to 2-5%, investment strategies must prioritize yield over rapid appreciation. Professional valuation surveys help investors:

Assess True Investment Potential 📈

Accurate valuations incorporating rental market dynamics ensure purchase prices align with realistic return expectations. Overpaying by even 5-10% can eliminate years of modest capital growth.

Identify Regional Opportunities 🎯

The stark regional variations mean investors can potentially achieve the upper end of the 2-5% range (or better) by focusing on resilient northern markets while avoiding overheated southern areas showing -24% to -40% net balances [1].

Plan for Holding Periods ⏳

Modest growth environments favor longer holding periods. Investors should ensure valuations support sustainable financing over 5-10 year horizons rather than speculative short-term flips.

For Sellers: Realistic Pricing in a Stabilising Market

Perhaps no group benefits more from understanding valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments than property sellers. The data provides clear guidance:

Avoid Overpricing 🚫

With buyer enquiries at -26% net balance [1], overpriced properties will languish on the market. Professional valuations provide objective pricing guidance that maximizes the probability of sale within reasonable timeframes.

Regional Reality Check 📍

Sellers in London and the South East must recognize that their markets face significant headwinds. Pricing based on 2023-2024 valuations will result in disappointment. Current professional assessments reflecting February 2026 market conditions are essential.

Timing Considerations ⏰

The short-term outlook (-18% net balance for near-term expectations) [1] suggests that waiting for market recovery may be counterproductive. Sellers with genuine need or desire to move should price realistically now rather than hoping for imminent improvement.

For Lenders and Financial Institutions

Mortgage lenders rely heavily on professional valuation surveys to manage lending risk. The current market context requires:

Conservative Loan-to-Value Ratios 🏦

With modest growth expectations and regional disparities, lenders should maintain prudent LTV limits, particularly in markets showing significant weakness like London (-40% net balance) [1].

Enhanced Due Diligence 🔍

Standard automated valuation models (AVMs) may not adequately capture the nuances of stabilising markets. Professional surveyor input becomes more valuable for lending decisions, particularly for higher-value properties or unusual assets.

Regional Risk Differentiation 🗺️

Blanket national lending policies fail to recognize the substantial differences between resilient northern markets and struggling southern regions. Risk pricing should reflect these regional realities.

The Role of Professional Chartered Surveyors in Market Stabilisation

Professional chartered surveyors play an indispensable role in maintaining market stability and transparency. Their expertise becomes particularly valuable during periods of transition and uncertainty.

Beyond Simple Valuations: Comprehensive Property Assessment

While headline valuations receive the most attention, chartered surveyors provide comprehensive property assessments that inform multiple aspects of property transactions:

Structural and Condition Reporting 🏗️

Identifying defects, maintenance requirements, and potential issues that affect value. Specific defect surveys can uncover problems that significantly impact valuations and negotiating positions.

Reinstatement Cost Assessments 🔥

For insurance purposes, reinstatement valuations ensure properties are adequately covered, which becomes increasingly important as building costs fluctuate independently of market values.

Specialized Valuation Scenarios 📋

From probate valuations to matrimonial valuations, professional surveyors provide objective assessments for legal and financial purposes where accuracy and defensibility are paramount.

Market Intelligence and Trend Analysis

The RICS monthly residential survey, which provides the data underlying the 2-5% growth forecast, represents aggregated intelligence from hundreds of chartered surveyors across the UK. This collective expertise offers:

Early Warning Indicators ⚠️

Changes in new buyer enquiries, agreed sales, and price expectations provide leading indicators of market direction months before official price indices reflect changes.

Regional Granularity 🔬

National averages mask significant regional variations. RICS survey data reveals these disparities, enabling more informed local decision-making.

Professional Consensus 🤝

When +33% of surveyors expect price rises over 12 months [1], this represents professional consensus based on direct market engagement rather than theoretical modeling.

Ethical Standards and Professional Accountability

RICS members operate under strict professional and ethical standards, including:

- Independence: Valuations must be objective and uninfluenced by parties with vested interests in specific outcomes

- Competence: Surveyors must operate within their areas of expertise and geographic knowledge

- Transparency: Methodologies and assumptions must be clearly documented and defensible

- Continuing Education: Regular professional development ensures surveyors remain current with market conditions and best practices

These standards provide confidence that professional valuations reflect genuine market conditions rather than optimistic or pessimistic biases.

Looking Ahead: What to Expect Through 2026 and Beyond

As we progress through 2026, several factors will influence whether the 2-5% growth forecast materializes and how valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments continue evolving.

Macroeconomic Factors to Monitor

Interest Rate Trajectory 📊

The renewed concerns over inflation and interest rates that emerged in February [1] will significantly influence housing affordability and demand. If rates stabilize or decline modestly, the upper end of the 2-5% range becomes more achievable. Conversely, further rate increases could suppress growth toward the lower end or even negative territory.

Employment and Income Growth 💼

Real wage growth relative to inflation determines affordability improvements. Positive real wage growth supports housing demand and price stability, while stagnant or declining real incomes constrain market activity.

Geopolitical Stability 🌍

The geopolitical uncertainty referenced in February survey results [1] affects business confidence, investment decisions, and consumer sentiment—all of which influence housing market activity.

Supply-Side Considerations

New Construction Rates 🏗️

Housing supply relative to demand fundamentally influences price dynamics. Current construction rates remain below long-term housing formation needs, providing underlying support for prices even in subdued markets.

Rental Sector Evolution 🏘️

With landlord instructions remaining negative at -27% net balance [1], continued contraction in rental supply may push more households toward ownership, supporting demand despite affordability challenges.

Planning and Regulatory Changes 📜

Government policies affecting housing supply, rental regulations, and planning permissions will influence market dynamics throughout 2026 and beyond.

Regional Divergence Likely to Continue

The dramatic disparities between London (-40% net balance) and northern regions (positive momentum) [1] suggest regional divergence will persist. This creates a two-speed market where:

- Southern markets may struggle to achieve even the lower end of 2-5% growth

- Northern and regional markets could exceed 5% growth in specific locations

- National averages mask significant local variations

Professional valuation surveys must continue accounting for these regional realities rather than applying blanket national assumptions.

Technology and Valuation Methodologies

While this article focuses on professional surveyor expertise, technology continues evolving to support (not replace) human judgment:

Enhanced Data Analytics 💻

Big data and machine learning tools provide surveyors with more comprehensive comparable property databases and market trend analysis.

Remote Assessment Technologies 📱

Drone surveys, 3D imaging, and virtual inspection tools supplement (but don't replace) physical property inspections, improving efficiency while maintaining accuracy.

Real-Time Market Intelligence 📡

Digital platforms providing instant access to transaction data, days-on-market statistics, and pricing trends enable surveyors to incorporate the most current information into valuations.

Conclusion

Valuation surveys for stabilising house prices: RICS insights on 2-5% growth and surveyor adjustments reveal a UK housing market navigating complex crosscurrents in 2026. After brief optimism in January, February brought renewed weakness with buyer enquiries falling to -26% net balance and dramatic regional disparities emerging—from London's -40% to positive momentum in northern regions [1].

The modest 2-5% growth forecast over the next 12 months reflects professional surveyor consensus that the market is stabilising rather than rebounding strongly. This environment demands sophisticated valuation methodologies that account for:

✅ Regional variations requiring location-specific assumptions

✅ Subdued demand dynamics affecting time-to-sale and negotiating positions

✅ Affordability constraints limiting buyer pools and price growth potential

✅ Forward-looking sentiment balancing cautious near-term outlook with modest 12-month optimism

For property stakeholders, the key takeaway is clear: professional valuation surveys from qualified chartered surveyors are more valuable than ever. Whether buying, selling, investing, or lending, accurate property assessments that reflect current market realities rather than outdated assumptions or wishful thinking provide the foundation for sound decision-making.

Next Steps

🔍 For Buyers: Obtain comprehensive RICS valuations and building surveys before committing to purchases, ensuring you understand both value and condition

📋 For Sellers: Commission professional valuations early to set realistic asking prices that maximize sale probability in a market with subdued demand

💼 For Investors: Focus on yield-generating properties in resilient regional markets, using professional valuations to avoid overpaying in weakening areas

🏦 For Lenders: Enhance due diligence with professional surveyor input, particularly in markets showing significant weakness or unusual characteristics

The UK housing market's journey through 2026 will continue unfolding, but armed with professional valuation expertise and realistic expectations of 2-5% growth, stakeholders can navigate this stabilising environment with confidence and clarity.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution