The buy-to-let landscape in 2026 faces unprecedented fiscal headwinds. For institutional investors eyeing portfolio expansion—particularly in Manchester and northern England markets—understanding the Impact of 2026 Budget Tax Rises on Buy-to-Let Valuations: Due Diligence for Institutional Investors has become mission-critical. With rental income tax rates climbing 2 percentage points from April 2027, dividend taxes rising in 2026, and regulatory reforms reshaping tenant relationships, the traditional valuation models that guided acquisition decisions are now obsolete. Smart capital is recalibrating: northern cities offer compelling yields, but only when due diligence protocols account for the full spectrum of tax-driven compression effects on net operating income.

Key Takeaways

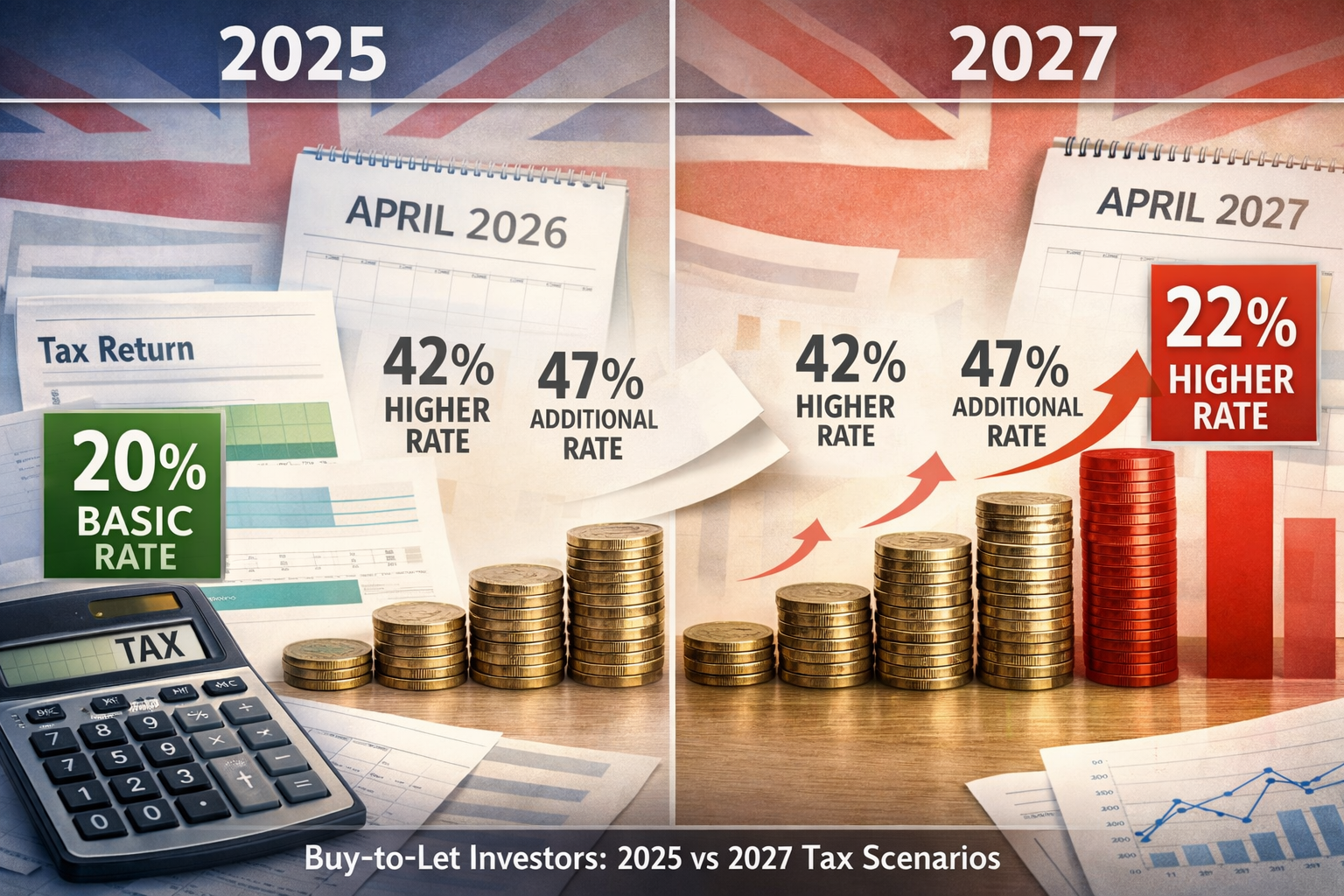

- 📊 Property income tax increases by 2% across all bands from April 2027, pushing basic rate landlords to 22%, higher rate to 42%, and additional rate to 47%—creating substantial yield compression that demands immediate valuation adjustments[2][4]

- 🏢 Institutional investors must integrate multi-layered tax analysis into RICS valuations, accounting for threshold freezes extending to 2031, accelerating fiscal drag, and the new mansion tax on properties exceeding £2 million from April 2028[1][3]

- 🔍 Northern markets present strategic opportunities when rigorous due diligence protocols incorporate regulatory changes from the Renters' Rights Act, SDLT surcharges, and dividend tax increases affecting corporate holding structures[5][6]

- 💼 Corporate structuring and tax mitigation strategies require immediate review, as limited company vehicles face different impacts than individual ownership models under the new tax regime

- 📈 Valuation methodologies must evolve to reflect compressed capitalization rates, extended payback periods, and reduced internal rates of return driven by the cumulative effect of multiple tax increases

Understanding the 2026 Budget Tax Changes for Buy-to-Let Investors

The fiscal environment for rental property investment has shifted dramatically. The 2026 Budget introduced a cascade of tax increases that collectively erode landlord profitability and necessitate fundamental reassessment of asset valuations.

Property Income Tax Rise: The Core Impact

Starting April 2027, income tax on rental profits increases by 2 percentage points across all three bands[2][4]. This represents a targeted increase affecting property income specifically, while employment income tax rates remain unchanged—a clear signal of government intent to extract additional revenue from the buy-to-let sector.

The new rates are:

- Basic rate: 22% (up from 20%)

- Higher rate: 42% (up from 40%)

- Additional rate: 47% (up from 45%)

The Office for Budget Responsibility projects this single measure will generate approximately £500 million in additional annual tax revenue[3]. For institutional investors, this translates directly to reduced net yields and compressed valuations.

Example calculation: A landlord with £50,000 in annual rental profit (after allowable expenses) in the higher-rate band would pay an additional £1,000 annually purely from the 2% rate increase. Over a typical 10-year hold period, this represents £10,000 in additional tax liability that must be factored into acquisition pricing.

Threshold Freezes: The Hidden Tax Increase

Perhaps more insidious than the rate increases themselves is the extension of income tax threshold freezes until April 5, 2031[1][4]. Personal allowances and tax band thresholds remain frozen at their 2021 levels, creating "fiscal drag" as inflation pushes more landlords into higher tax brackets without any real income growth.

Between 2024/25 and 2025/26 alone, approximately 500,000 additional taxpayers entered the higher-rate bracket, bringing the total to over 7 million[4]. This accelerating migration means landlords who were basic-rate taxpayers when they acquired properties may now face higher-rate taxation on the same real income—compounding the impact of the 2% rate increase.

Thresholds are only scheduled to resume inflation indexing from 2031/32 onwards[1], meaning institutional investors must model tax liabilities assuming continued bracket compression through the end of the decade.

Dividend and Savings Income Tax Increases

For institutional investors utilizing corporate structures or dividend-paying vehicles, the April 2026 dividend tax increases add another layer of complexity[5]:

- Basic rate dividend tax: 10.75% (up from 8.75%)

- Higher rate dividend tax: 35.75% (up from 33.75%)

Similarly, savings income tax rises to 22%, 42%, and 47% across the three bands from April 2027[5], affecting reinvestment strategies and cash reserve management.

These changes particularly impact limited company structures, where profits are typically extracted via dividends. The combined effect of higher corporation tax (already at 25% for profits exceeding £250,000), increased dividend taxes, and rising property income taxes creates a complex optimization challenge for tax advisors.

The Mansion Tax: High-Value Asset Surcharge

From April 2028, a new annual surcharge applies to residential properties valued over £2 million in England[3]. The charges scale with valuation:

| Property Value | Annual Mansion Tax |

|---|---|

| £2m – £5m | £2,500 |

| £5m – £10m | £5,000 |

| £10m+ | £7,500 |

For institutional portfolios containing high-value London or prime regional assets, this represents a permanent drag on net yields. A £3 million property generating £90,000 annual rent (3% gross yield) now faces an additional £2,500 annual cost, reducing net yield by approximately 0.08%—a material impact when capitalized over the asset's holding period.

Professional RICS valuation services must now incorporate mansion tax liabilities into discounted cash flow models for affected properties.

Stamp Duty Land Tax Surcharges

Acquisition costs remain elevated due to the 5 percentage point SDLT surcharge on additional properties purchased for more than £40,000[1]. This effectively eliminates the nil-rate band for buy-to-let purchases, with rates starting at 5% and reaching 17% for properties exceeding £1.5 million.

For a £300,000 property, the SDLT bill reaches £17,500—capital that must be recovered through rental income over the hold period. When combined with rising income taxes compressing net yields, the payback period extends significantly, reducing internal rates of return.

Impact of 2026 Budget Tax Rises on Buy-to-Let Valuations: Adjusting Assessment Methodologies

Traditional valuation approaches require fundamental recalibration to reflect the new tax environment. Institutional investors conducting due diligence must ensure their valuation protocols incorporate multi-dimensional tax impact analysis.

Yield Compression and Capitalization Rate Adjustments

The 2% property income tax increase directly compresses net yields for all landlords. Consider a standard buy-to-let scenario:

Before tax changes (2025):

- Gross rental income: £15,000

- Allowable expenses: £3,000

- Taxable profit: £12,000

- Tax (higher rate @ 40%): £4,800

- Net income: £7,200

- Net yield (on £200,000 property): 3.6%

After tax changes (2027):

- Gross rental income: £15,000

- Allowable expenses: £3,000

- Taxable profit: £12,000

- Tax (higher rate @ 42%): £5,040

- Net income: £6,960

- Net yield (on £200,000 property): 3.48%

The 0.12% net yield compression may appear modest, but when capitalized using standard investment models, it translates to meaningful valuation adjustments. Using a simple yield-based valuation:

- 2025 valuation (7.2% net yield ÷ 4% cap rate): £200,000

- 2027 valuation (6.96% net yield ÷ 4% cap rate): £193,333

- Valuation decline: £6,667 or 3.3%

For institutional portfolios valued in the tens or hundreds of millions, these percentage adjustments represent substantial capital value erosion. Professional Red Book valuations must now explicitly model post-tax cash flows under the new regime.

Discounted Cash Flow Modeling Enhancements

Sophisticated institutional investors employ discounted cash flow (DCF) analysis for portfolio acquisitions. The 2026 tax changes necessitate several modeling enhancements:

- Year-by-year tax rate modeling: Account for the April 2026 dividend tax increase, April 2027 property income tax increase, and April 2028 mansion tax implementation

- Threshold freeze impacts: Model bracket migration as rental income grows but thresholds remain frozen through 2031

- Exit taxation: Incorporate capital gains tax implications under current or anticipated future rates

- Regulatory cost overlays: Factor in compliance costs from the Renters' Rights Act

A robust DCF model should project cash flows through at least 2031 (when threshold freezes end) and sensitivity-test multiple exit scenarios. The internal rate of return (IRR) hurdles that justified acquisitions at 8-10% may now require adjustment to 6-8% to maintain deal flow in the new environment.

Comparable Sales Analysis Adjustments

When using comparable sales to establish market value, appraisers must recognize that transactions completed before the 2026 Budget announcements reflect outdated buyer expectations. Properties sold in 2024-2025 were priced assuming the pre-existing tax regime.

Institutional buyers should apply downward adjustments to historical comparables to reflect:

- Reduced net yields from higher property income tax

- Extended payback periods from SDLT surcharges

- Regulatory compliance costs from tenant protection measures

A prudent approach applies a 3-5% valuation discount to pre-2026 comparables when establishing current market value, with the exact percentage varying by property type, location, and existing yield profile. Properties already operating on thin margins face larger percentage adjustments than high-yield assets.

Northern Markets: Valuation Opportunities with Enhanced Due Diligence

Despite the challenging tax environment, northern England markets—particularly Manchester, Liverpool, Leeds, and Sheffield—present compelling opportunities for institutional capital when rigorous due diligence protocols are applied.

These markets offer:

- Higher gross yields (typically 5-7% versus 3-4% in London)

- Lower acquisition costs reducing SDLT impact

- Strong rental demand from universities, healthcare, and professional services sectors

- Regeneration tailwinds supporting capital appreciation

However, the Impact of 2026 Budget Tax Rises on Buy-to-Let Valuations: Due Diligence for Institutional Investors requires enhanced scrutiny of northern assets:

✅ Tenant quality assessment: Verify employment stability and income multiples exceed 30x monthly rent

✅ Property condition surveys: Commission comprehensive building surveys to identify deferred maintenance

✅ Regulatory compliance verification: Ensure EPC ratings, electrical safety certificates, and gas safety records meet current standards

✅ Comparable rental analysis: Validate asking rents against actual achieved rents in the micro-market

✅ Exit liquidity assessment: Confirm sufficient buyer depth for eventual disposition

Professional valuation cost analysis should be factored into acquisition budgets, as institutional-grade due diligence requires RICS-certified appraisals rather than automated valuation models.

Due Diligence Protocols for Institutional Investors Under the New Tax Regime

The Impact of 2026 Budget Tax Rises on Buy-to-Let Valuations: Due Diligence for Institutional Investors extends beyond pure valuation adjustments to encompass comprehensive risk assessment and structural optimization.

Enhanced Financial Modeling Requirements

Institutional investment committees now require multi-scenario financial models that stress-test acquisitions against:

Tax scenario modeling:

- Base case: All announced tax increases implemented as scheduled

- Upside case: No further tax increases through 2031

- Downside case: Additional 1% property income tax increase in 2029 Budget

Regulatory scenario modeling:

- Base case: Renters' Rights Act implemented as drafted

- Upside case: Enforcement delays and transitional relief

- Downside case: Rent controls introduced in high-demand markets

Market scenario modeling:

- Base case: Rental growth at inflation +1%

- Upside case: Rental growth at inflation +2% (supply constraints)

- Downside case: Rental growth at inflation -1% (demand softening)

Each scenario should project cash flows, tax liabilities, and IRR through at least 2031. The probability-weighted average IRR across scenarios provides a more robust investment decision framework than single-point estimates.

Corporate Structure Optimization

The divergent tax treatment of individual versus corporate ownership creates optimization opportunities. Institutional investors should model both structures:

Individual/Partnership ownership:

- ✅ Access to capital gains tax annual exemption

- ✅ Potential for principal private residence relief on mixed-use

- ❌ Property income taxed at 22%/42%/47% from April 2027

- ❌ No ability to retain and reinvest profits tax-efficiently

Limited company ownership:

- ✅ Corporation tax at 19% (profits up to £50,000) or 25% (profits above £250,000)

- ✅ Mortgage interest fully deductible

- ✅ Ability to retain profits for portfolio expansion

- ❌ Dividend extraction taxed at 10.75%/35.75%

- ❌ Corporation tax on capital gains at 25%

- ❌ Stamp duty surcharge of 5% on acquisitions

For high-volume institutional investors, limited company structures typically provide superior tax efficiency despite the dividend extraction costs. The ability to deduct full mortgage interest (rather than claiming the restricted 20% tax credit available to individuals) and retain profits at 25% corporation tax (versus 42% higher-rate income tax) creates meaningful advantages.

However, each portfolio requires bespoke analysis. Engaging specialist tax advisors to model the total tax leakage under both structures across the full investment lifecycle is essential due diligence.

Regulatory Compliance and the Renters' Rights Act

The Renters' Rights Act, effective May 2026, fundamentally alters landlord-tenant dynamics[5]. Key provisions affecting valuations include:

Elimination of Section 21 'no-fault' evictions: Landlords can only regain possession for specified grounds (sale, personal occupation, tenant breach). This reduces flexibility and extends void periods when problematic tenancies arise.

Conversion to open-ended tenancies: All fixed-term tenancies become periodic, eliminating the certainty of lease expiry dates. Institutional portfolios must budget for higher tenant retention costs and extended average tenancy durations.

Rent increase restrictions: Landlords can only increase rent once annually with two months' notice. In high-inflation environments, this creates a lag between cost increases and revenue adjustments.

Enhanced repair obligations: Stricter standards for property condition and response times for maintenance requests increase operating costs.

Due diligence protocols must now include:

- Legal compliance audits verifying all properties meet enhanced standards

- Operating cost uplift modeling (typically 10-15% increase for professional management)

- Void period extensions in cash flow models (from 2-3 weeks to 4-6 weeks)

- Tenant default provisions reflecting reduced eviction flexibility

Properties with existing compliance issues should be discounted heavily or excluded from acquisition consideration, as remediation costs can exceed 10% of purchase price for older stock.

RICS Valuation Standards and Reporting

All institutional acquisitions should be supported by RICS Red Book compliant valuations prepared by chartered surveyors. The Impact of 2026 Budget Tax Rises on Buy-to-Let Valuations: Due Diligence for Institutional Investors requires valuers to explicitly address:

✅ Tax assumption clarity: State whether valuation reflects pre-tax or post-tax cash flows and which tax regime is assumed

✅ Regulatory compliance verification: Confirm property meets all current regulatory standards or quantify remediation costs

✅ Market evidence recency: Use comparables from post-Budget 2026 transactions where available

✅ Yield compression acknowledgment: Explicitly adjust capitalization rates to reflect reduced net yields

✅ Special assumptions disclosure: Clearly state any assumptions about future tax changes, regulatory modifications, or market conditions

Institutional investors should engage RICS-registered valuers with specific expertise in investment property and current tax regime familiarity. Generic residential valuations lack the sophistication required for institutional decision-making.

Portfolio-Level Risk Management

Beyond individual asset due diligence, institutional investors must assess portfolio-level risks:

Geographic concentration: Overweight positions in single cities or regions create exposure to localized economic shocks. Diversification across Manchester, Leeds, Liverpool, and Sheffield mitigates this risk.

Tenant concentration: Portfolios heavily weighted toward student lets, professional singles, or families face different regulatory and economic risks. Balanced tenant mix reduces volatility.

Lease expiry clustering: Avoid portfolios where significant percentages of leases expire simultaneously, creating refinancing or disposition pressure.

Debt maturity laddering: Stagger mortgage maturities to avoid concentrated refinancing risk when interest rates may be elevated.

Tax structure consistency: Mixing individual and corporate ownership within a single fund creates administrative complexity and tax inefficiency. Standardize structures where possible.

Strategic Responses: Maximizing Value Under the New Tax Framework

Sophisticated institutional investors are adapting strategies to maintain acceptable returns despite the challenging fiscal environment.

Value-Add Repositioning

Rather than acquiring stabilized assets at compressed yields, many institutions are pursuing value-add strategies:

Property upgrades: Acquire below-market properties, invest in renovations to achieve higher rents, and improve energy efficiency ratings. The capital investment creates tax-deductible depreciation while supporting rental growth.

Planning gains: Acquire properties with conversion or extension potential (subject to planning permission). Converting single-family homes to HMOs or adding extensions can increase rental income by 30-50%.

Repositioning distressed assets: Target properties sold by individual landlords exiting due to tax pressures. These often transact at discounts to replacement cost, creating embedded value.

Geographic Arbitrage

The tax increases affect all UK landlords equally, but yield differentials between regions create opportunities. A property generating 6% gross yield in Manchester faces the same tax treatment as a 3% gross yield London property, but the northern asset has significantly more margin to absorb tax increases.

Institutional capital is increasingly flowing to:

- Manchester: Strong rental demand from professional services and tech sectors

- Leeds: Healthcare and financial services employment growth

- Liverpool: Regeneration projects and university expansion

- Sheffield: Affordable housing stock with renovation potential

These markets offer 3-4% net yields even after accounting for the April 2027 tax increases—substantially above the 1-2% net yields common in London and the Southeast.

Build-to-Rent Conversion

Some institutional investors are converting buy-to-let portfolios to build-to-rent (BTR) structures. BTR developments benefit from:

- Professional management reducing regulatory compliance risk

- Economies of scale in maintenance and administration

- Potential for local authority partnerships and planning support

- Enhanced tenant experience supporting premium rents

While BTR faces the same income tax treatment as traditional buy-to-let, the operational efficiencies and rental premiums can offset tax headwinds.

Tax Loss Harvesting and Offset Strategies

Sophisticated tax planning can mitigate the impact of higher rates:

Capital loss realization: Dispose of underperforming assets to crystallize capital losses that can offset gains on future disposals.

Interest cost maximization: Ensure all allowable interest costs are claimed, particularly for corporate structures where full deductibility remains available.

Expense timing optimization: Accelerate deductible repairs and maintenance into high-income years to maximize tax relief.

Group relief planning: For corporate structures, utilize group relief to offset profits in one entity against losses in another.

Alternative Investment Structures

Some institutional investors are exploring alternative structures to mitigate tax impacts:

Real Estate Investment Trusts (REITs): REITs enjoy tax-exempt status on rental income and capital gains, though they must distribute 90% of profits as dividends (which are then taxed in investors' hands).

Pension fund investment: Self-invested personal pensions (SIPPs) can hold commercial property (though residential is generally prohibited), offering tax-free rental income and capital gains.

Offshore structures: Non-UK domiciled investors may utilize offshore holding companies, though increasingly stringent reporting requirements and anti-avoidance measures limit benefits.

Each alternative carries specific regulatory requirements, compliance costs, and investor eligibility restrictions. Professional legal and tax advice is essential before restructuring.

Conclusion

The Impact of 2026 Budget Tax Rises on Buy-to-Let Valuations: Due Diligence for Institutional Investors represents a fundamental recalibration of the UK rental property investment landscape. The 2% property income tax increase from April 2027, combined with threshold freezes through 2031, dividend tax rises, the new mansion tax, and the Renters' Rights Act, collectively compress net yields by 10-20% for most investors[2][4][5].

Institutional investors cannot rely on historical valuation methodologies or pre-2026 comparable sales. Rigorous due diligence now requires:

✅ Multi-scenario financial modeling incorporating all tax changes through 2031

✅ RICS Red Book valuations explicitly addressing post-tax cash flows

✅ Enhanced regulatory compliance verification

✅ Corporate structure optimization analysis

✅ Geographic diversification favoring higher-yield northern markets

Despite the challenging environment, opportunities persist for disciplined institutional capital. Northern England markets—particularly Manchester and surrounding cities—offer gross yields of 5-7% that, even after accounting for the new tax regime, deliver acceptable risk-adjusted returns[9]. Properties acquired with comprehensive building surveys, proper valuation protocols, and tax-efficient structures can still achieve 6-8% IRRs over 10-year hold periods.

Actionable Next Steps for Institutional Investors

Immediate actions (Q2 2026):

- Commission portfolio revaluations using RICS-certified surveyors incorporating April 2027 tax assumptions

- Engage tax advisors to model individual versus corporate structure optimization for existing holdings

- Review acquisition underwriting models to incorporate yield compression and extended payback periods

- Audit regulatory compliance across all properties to identify Renters' Rights Act exposure

Medium-term actions (Q3-Q4 2026):

- Reallocate acquisition focus toward northern markets with higher gross yields

- Implement value-add strategies targeting below-market properties with renovation potential

- Establish vendor relationships with individual landlords considering portfolio exits

- Develop scenario planning frameworks for potential additional tax changes in future Budgets

Long-term strategic positioning (2027-2031):

- Build BTR capabilities to capture operational efficiencies and rental premiums

- Monitor threshold indexation resumption in 2031/32 for potential tax relief

- Maintain acquisition discipline focusing only on assets delivering post-tax returns above cost of capital

- Preserve exit optionality through diversified holdings and staggered debt maturities

The UK buy-to-let market remains viable for institutional investors who adapt their due diligence protocols, valuation methodologies, and investment strategies to the new fiscal reality. Those who fail to adjust will experience compressed returns and capital erosion; those who embrace rigorous analysis and strategic repositioning will identify opportunities others overlook.

For professional guidance on institutional-grade property valuations incorporating the latest tax changes, get a quote from RICS-certified surveyors with expertise in investment property assessment.

References

[1] Deloitte Uk Tax Rates 2026 27 – https://taxscape.deloitte.com/taxtables/deloitte-uk-tax-rates-2026-27.pdf

[2] Buy To Let Tax Changes – https://www.simplybusiness.co.uk/knowledge/landlord-tax/buy-to-let-tax-changes/

[3] New Property Tax – https://hoa.org.uk/news/new-property-tax/

[4] Income Tax Increase For Landlords What The April 2027 Changes Mean For You – https://www.championgroup.co.uk/income-tax-increase-for-landlords-what-the-april-2027-changes-mean-for-you/

[5] Autumn Budget Dividend Income Tax Increase – https://www.evelyn.com/insights-and-events/insights/autumn-budget-dividend-income-tax-increase/

[6] 4 Key Budget Announcements That Could Affect Landlords – https://infinityfinancialadvice.co.uk/4-key-budget-announcements-that-could-affect-landlords/

[7] Nobody Will Like This Budget Including Landlords – https://www.propertynotify.co.uk/news/nobody-will-like-this-budget-including-landlords/

[8] Autumn Budget Inheritance Tax And Other Possible Changes – https://www.fidelity.co.uk/markets-insights/personal-finance/inheritance-legacy/autumn-budget-inheritance-tax-and-other-possible-changes/

[9] Key Changes In The Housing Market – https://millbankfs.co.uk/2026/02/10/key-changes-in-the-housing-market/